XLF - Enova International: Should You Take Some Profit Now?

Summary

- Lenders have not performed well so far, and the short-term outlook doesn't look promising.

- Enova International, Inc. will face severe headwinds due to the expected deterioration in credit market sector conditions.

- Stocks aren't low and actually look expensive.

Amid Severe Macroeconomic and Geopolitical Headwinds, the Financial Sector Has Not Performed Well and the Near Term Does Not Promise Any Better

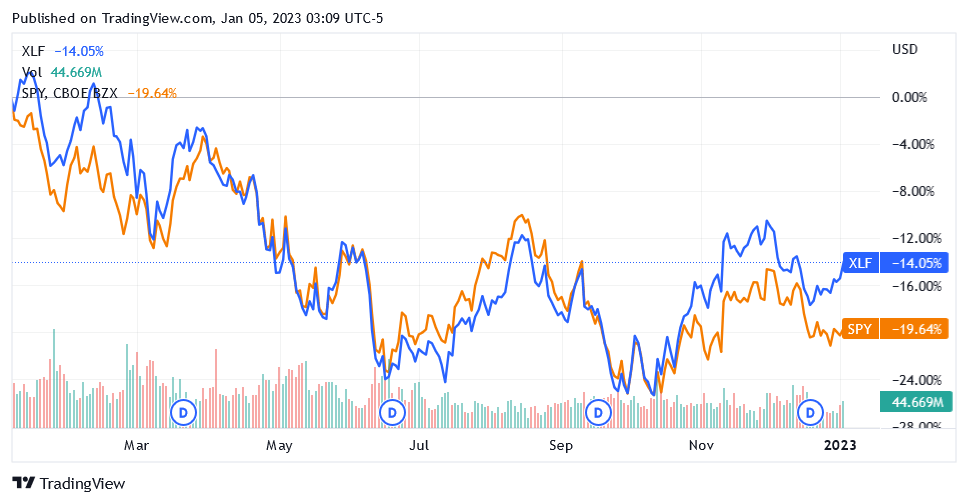

Not as bad as the US stock market, but still financial stocks have fallen sharply over the past year.

This is a clear signal that the market does not see the increase in the cost of money as an advantage for the profitability of banks and financial service providers, but as a brake on consumption, which also needs to be fueled by credit to grow.

And so, following the Federal Reserve's monetary tightening with the first-rate hike from the mid-December 2021 meeting, the SPDR S&P 500 Trust ETF ( SPY ) fell 19.64%, while the Financial Select Sector SPDR ETF ( XLF ) declined by 14.05%. The SPDR S&P 500 Trust ETF is the benchmark index for the US stock market, while the Financial Select Sector SPDR ETF is the benchmark for US-listed financial services stocks.

{kind=link}

With inflation still elevated at 7.1% versus the 2% target, which has yet to be addressed by tighter monetary policy, further interest rate hikes and the rapid rise in goods and services prices will continue to signal a recession and weigh on consumers' willingness to buy.

Both factors should be reflected in lower stock prices of US-listed consumer lenders going forward, as deteriorating household economic conditions tend to result in higher default rates which, combined with falling demand for consumer credit, will hurt these companies' profitability.

Given the Challenging Near-Term Outlook for a Credit Servicer Like Enova International, Inc., Investors May Want to Soften Their Positions

Investors should therefore consider reducing the portion of their portfolio invested in US-listed credit servicer stocks, starting with Enova International, Inc. ( ENVA ).

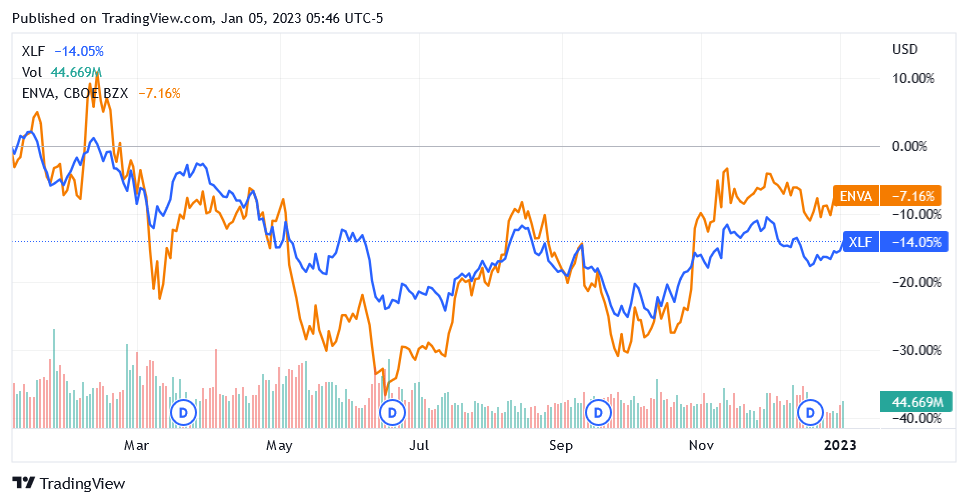

Enova International's share price has recently outperformed many of its peers in the financial sector, mainly thanks to some progress in certain profitability and default rates metrics, which are being held at better than pre-pandemic levels.

{kind=link}

But firing on all cylinders could fail if the company's profitability and/or default rates deteriorate instead of improving further as economic conditions for consumers worsen amid difficult macro factors with the expected recession.

If this scenario materializes, which is highly possible given the macroeconomic outlook, the market could experience severe downward pressure on Enova International's share price.

As such, the resilience that has shown Enova International's share price outperforming the industry in recent weeks, despite severe headwinds from bearish market sentiment, could be significantly dampened.

The following few statistics show deteriorating trends in money consumers borrow to pay for goods or services and loan default rates.

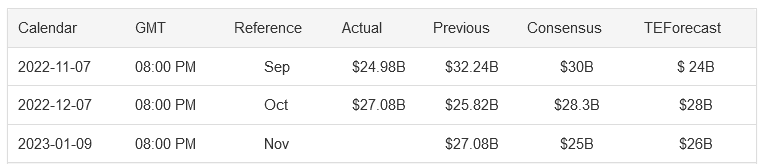

US consumer credit of $27.1 billion in October 2022, which among other things missed market forecasts by $1.2 billion, is expected to be significantly lower at $25 billion for the month of November 2022, as shown in the screenshot of the Trading Economics table (see data in consensus column).

{kind=link}

Looking ahead to 2023, TransUnion ( TRU ) forecasts that the consumer credit market will see significant declines in all categories in terms of originations except home equity and auto loans, which will determine a reversal from the past two years when lending has grown aggressively.

From a default standpoint, TransUnion predicts that default rates for credit cards and unsecured personal loans will increase in 2023, reaching unprecedented levels in the last 14 years.

As the largest economy in the world, US consumer credit trends and default rates provide a very good gauge of the situation that could potentially exist overseas.

Abroad, where current economic conditions and near-term prospects appear broadly like those in the US, consumer credit and default rates are also likely to worsen in 2023 compared to previous years, when they benefited from the strong recovery after the pandemic caused by the COVID-19 virus.

Enova International, Inc. in the Credit Services Sector

Enova International, based in Chicago, Illinois, is a provider of online financial services through a lending platform that leverages artificial intelligence and machine learning technologies.

Enova's lending platform is primarily used by consumers and private small businesses among North American, Brazilian and Australian non-prime customers.

Non-prime borrowers are borrowers who have a high probability of bankruptcy due to bad credit scores or other problems and are therefore typically not qualified to access the loans provided through traditional financial channels.

Enova International, Inc. Will Face Deteriorating Conditions in The Credit Market Sector

Enova says it has served more than 7.5 million customers and facilitated access to approximately $40 billion in credit, helping many borrowers without top credit ratings improve their financial health.

This portfolio must survive in an economic environment that is expected to be characterized by greater volatility and uncertainty in 2023 than in the previous year.

This is the agenda dubbed Bogeyman 2023. The economic slowdown due to the expected recession and the negative impact of the worrying resurgence of COVID-19 infection in the People's Republic of China on the global economy will come on top of runaway inflation, risky monetary tightening and the war in Ukraine.

These factors could impact Enova International's total portfolio of loans, which totaled $1.2 billion as of Q3 2022, for increases of 10% quarter over quarter and 40% year over year, and in line with TransUnion forecasts for the entire U.S. consumer credit market, could lead to a significant decline in the company's new originations.

The economic slowdown could lead to more modest overall sales growth and falling profits as a result of a credit crunch.

{kind=link}

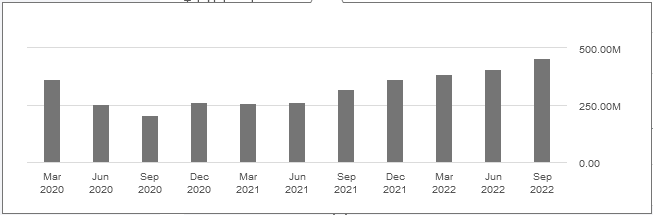

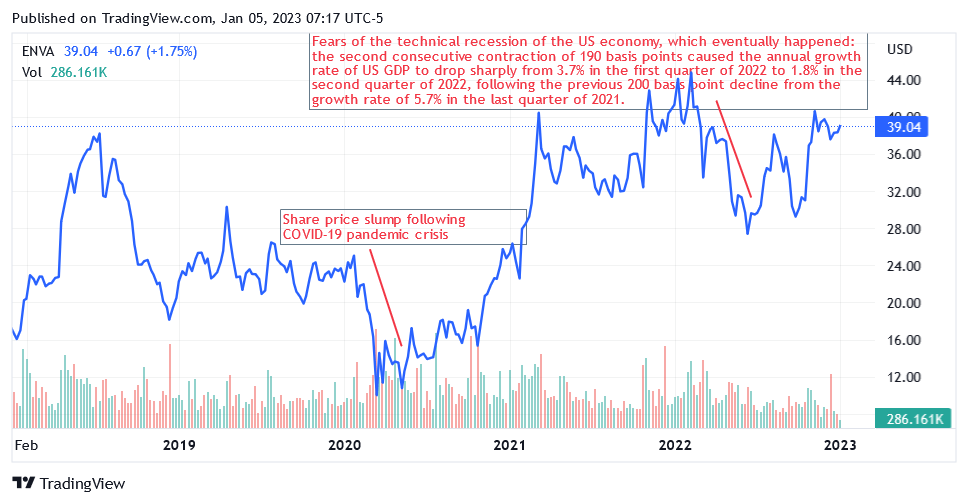

Perhaps not as severe as after the COVID-19 virus crisis, when lockdowns and restrictions curbed consumption to the point where Enova International sales reported sequential and annual declines of up to 30%. See the chart above comparing total revenue of $362.3 million in Q3 2020 to $253.1 million in Q2 2020 and $259.4 million in Q1 2021.

However, according to analysts' estimates , Enova International's revenue growth should slow down significantly in 2023 compared to 2022. They forecast an annual growth rate of 16% in 2023 compared to 43.70% in 2022.

As for adjusted earnings, despite the strong performance in the third quarter of 2022 (the adjusted earnings of $1.74 per diluted share rose 16% year over year), analysts believe these have declined 10.40% year on year to $6.78 per diluted share in 2022.

Additionally, analysts expect earnings to grow just 7.50% in 2023, compared to a 43.36% compound annual growth rate over the past 5 years.

Analysts are likely to lower these estimates further based on the results from the minutes of the Federal Reserve Board's last meeting.

The US Federal Reserve minutes from 13-14 December meeting shows the consensus of policymakers on the inadequacy of reducing the cost of money in 2023, as this maneuver is still seen as premature and therefore risky for the economy.

Therefore, an inflation rate of 7.1% in November 2022, although significantly lower than the peak of 9.1% in June 2022, and given the delay in passing on the impact of interest rate hikes on consumption and investment, further sharp rate hikes will be needed to bring the rapid rise in the prices of goods and services back under control.

The 10% Job Loss at Salesforce, Inc. ( CRM ), the 18,000 job cuts, 8,000 more than originally planned, at Amazon.com, Inc. ( AMZN ), and the expected new round of job cuts at Tesla, Inc. ( TSLA ) and other large companies are reliable predictors of the magnitude of the 2023 recession that will affect Enova's overall loan portfolio.

As the portfolio includes loans to sub-prime borrowers, implying a high risk of non-performing loans, there will be an impact in terms of net write-offs ( 8.4% in Q3 2022 or below pre-pandemic levels) and the ratio of total receivables 30 days or longer overdue (it was 5.6% in Q3 2022 or flat year over year).

Stock Valuation: Shares Are Not Low and Look Expensive

Shares of Enova International traded at $39.04 per unit for a market cap of $1.23 billion as of this writing.

{kind=link}

From a technical perspective, shares are not low today when their current levels are compared to recent market valuations, which basically come from the long-term trend of the 200-day simple moving average line of $34.61 and the midpoint of $36.84 of the 52-week range from $25.80 to $47.88.

With the recession expected for this year leading to a slowdown in project sales, falling margins and higher default rates, the current levels are most likely also an overvaluation by the market.

Similar to the outbreak of the COVID-19 crisis in mid-March 2020 and the technical recession of the US economy in the early summer of 2022, a beta of 1.45 over 24 months implies a sharp decline in the shares of Enova, should a sell-off in US-listed stocks be triggered by the expected recession.

{kind=link}

Enova's shares could also rise instead of fall but given the severity of the factors that will weigh on the market valuations of the securities, this event has very limited chances of it happening.

Conclusion

Enova International has a portfolio of loans to high-risk borrowers and this characteristic makes the company vulnerable to the challenges that economic development is about to bring.

The portfolio's fair value has improved due to the rise in interest rates. Even if interest rates continue to rise, this type of improvement in the portfolio's credit outlook may still not be enough to account for the risk that 3 aspects configure:

- expected lower new originations on slowing down of the demand for consumer credit amid very difficult macroeconomic conditions.

- expected higher default rates and portfolio write-downs amid an uncertain outlook for consumers due to job losses.

- the negative impact of a high positive market beta on Enova International's stock in the event of a recession causes a sell-off in the stock markets.

Investors may want to get some profit from their investments by taking advantage of the current high share prices.

For further details see:

Enova International: Should You Take Some Profit Now?