ENVA - Enova: Significant Changes In Business Insignificant Changes In Valuation

2023-03-17 09:40:57 ET

Summary

- Enova is facing regulatory uncertainties.

- Enova diversifies this risk with growing its SMB lending business.

- Enova derives its competitive advantage through it's online only model and its underwriting system.

- Enova is at least 30% undervalued if compared to its benchmarks.

Thesis

The last article I wrote on Enova ( ENVA ) had the conclusion that the company is at least 30% undervalued. Since then Enova has experienced a strong share appreciation with its shares rising as high as $53. However due to an even stronger execution on its business strategy Enova is arguably cheaper now than before its 25% appreciation vs. a negative 6% development of the S&P 500 since my last post . In this article I will assess Enova’s development in the last year and give an estimate where the business is headed in the future and will conclude with at least a 30% upside to current values.

Business overview and development

Enova International is an online financial service company which focuses on sub- or near prime private customers and small to medium sized businesses. They are offering loans and lines of credit for their customers in 37 states in the US and Brazil and financing for small businesses in the US, Australia and Canada. Being one of the first movers in the online lending business enabled them to collect a significant amount of data which they incorporate in their machine learning models to enable better decision making regarding underwriting.

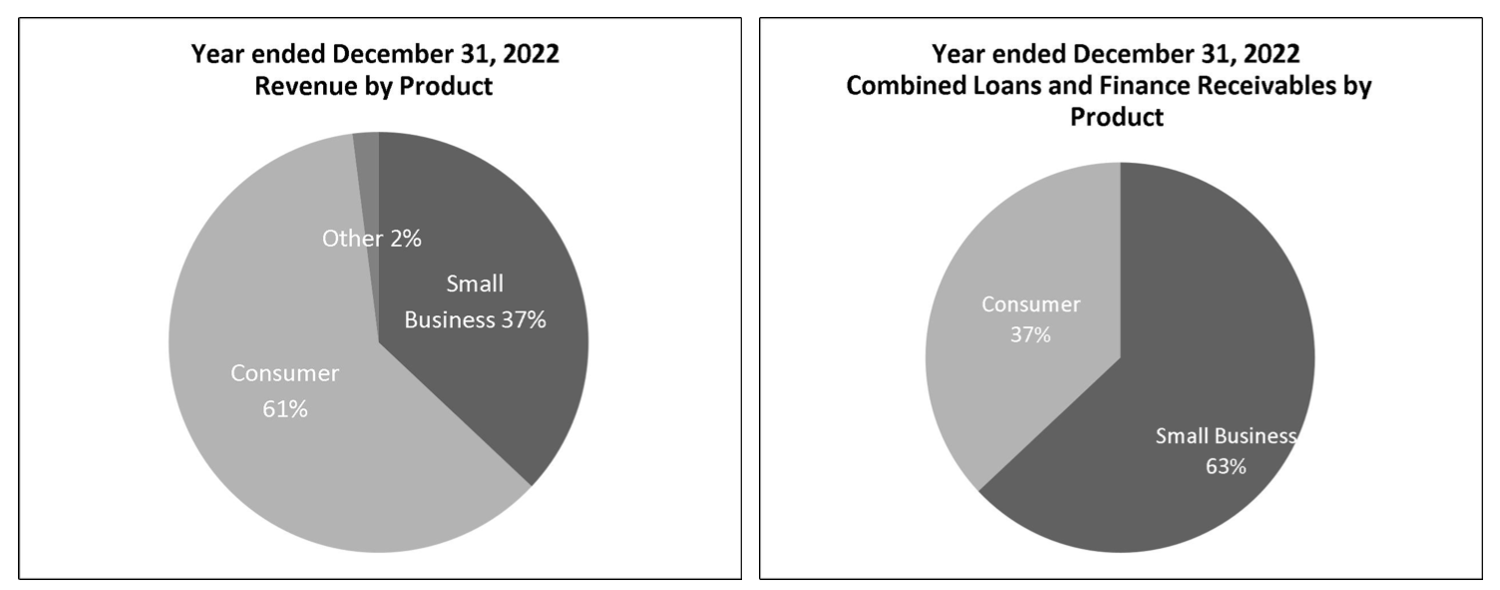

The biggest change in Enova's Business in the recent time was the increased focus on growing the small and medium business ((SMB)) lending part of its business through the acquisition of OnDeck. The portfolio value for the SMB lending business increased from 10% to 60% during 2017 to 2022. The small business revenue increased 71.9% versus 30.6% for consumer loans in 2022. Already SMB is now more important than consumer loans with a 60% contribution to full company EBITDA. It can be expected that this trend will continue as their focus is still on reasonably growing small business originations while being more careful with consumer loans and focusing mainly on lines of credit. The advantage of this is diversification of economic and regulatory risk.

{kind=link}

Figure 1:Revenue and Portfolio by Product (ir.enova.com/quarterly-and-annual-results)

The increased focus to small business led to higher net revenue margins and lower 30 day delinquencies of loans and as well as charge-offs as shown in the Figure 2 and 3 below: This led the company to increase their ROE targets and will also enable them to increase the net revenue margins in the long term (compared to 2021 the net revenue margin was lower due to unsustainably low rates of charge-offs in said year).

{kind=link}

Figure 2: Consumer loans being 30 days delinquent/charged off for all quarters 2022 (ir.enova.com/quarterly-and-annual-results)

{kind=link}

Figure 3: Small business loans being 30 days delinquent/charged off for all quarters 2022 (ir.enova.com/quarterly-and-annual-results)

Products and work culture

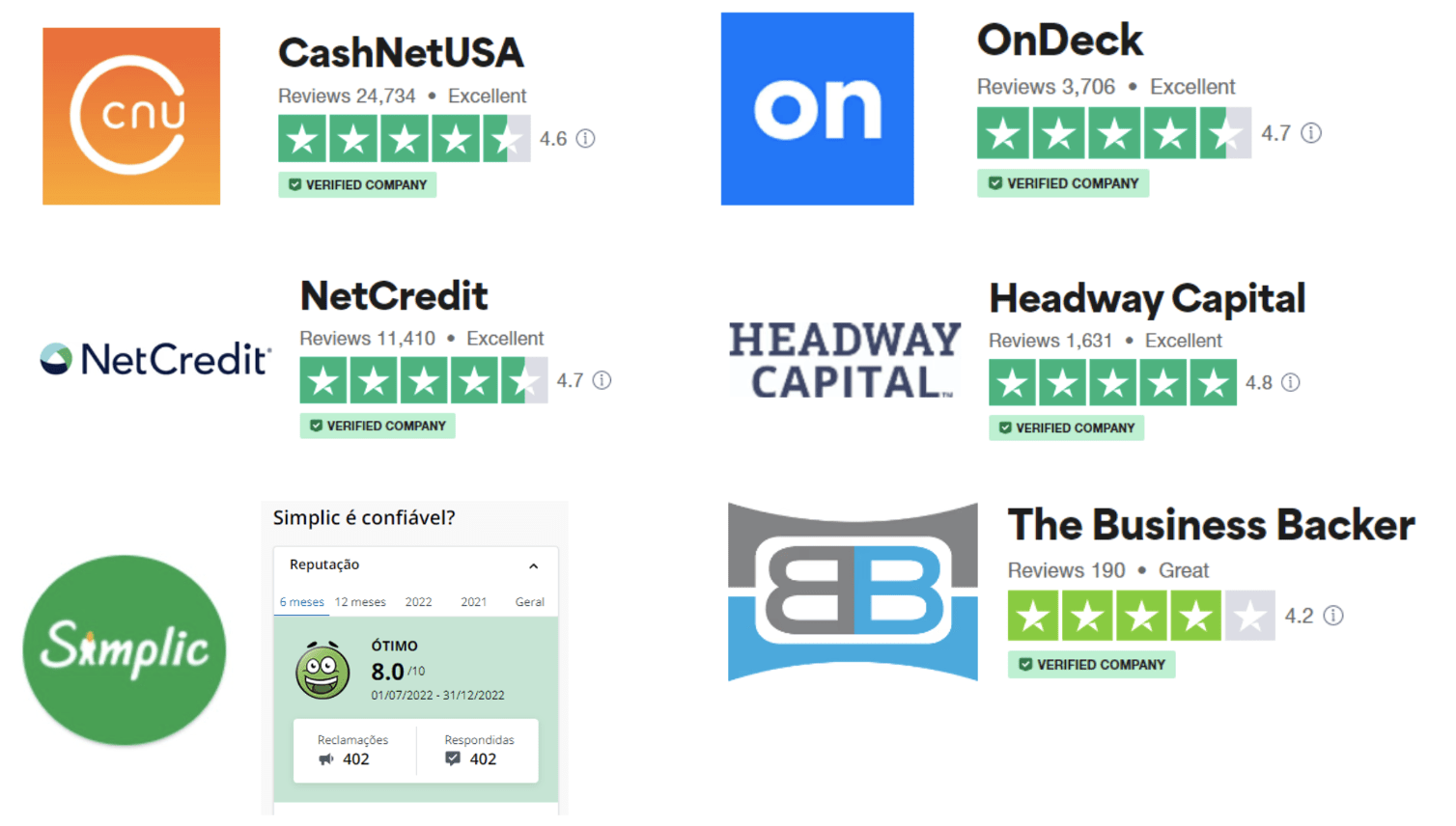

On the product side, Enova's products are still seen as excellent as an overview of Trustpilot shows us. In the last year there was a big focus on marketing to attract new customers. This was achieved through significant spending on marketing campaigns with 20% of revenue dedicated to it. This strategy seems to have paid off with 42% percent of originations coming from new customers. Total loans and finance receivables grew 46% to $2.9 billion. This shows that on the one side the marketing campaign was effective while on the other side there is still much room for Enova to grow its business. Next year Enova expects to have similar spendings on marketing for attracting new customers

{kind=link}

Figure 4: Customer reviews of Enova's products (ir.enova.com/presentations-events)

At the same time Enova's working culture seems to be very healthy with great focus on diversity and inclusion leading to satisfied employees. Enova was nominated as one of the best places to work for computer places a tenth consecutive year in a row. This leads to a higher employer attractiveness which in turn leads to hiring the most talented people in the industry.

{kind=link}

Figure 5: Awards for work place attractiveness (ir.enova.com/presentations-events)

Regulatory risk

The elephant in the room for Enova are regulatory risks which affect all of its business parts but mainly the ones regarding consumer lending. For example Enova had to cease its consumer lending business (QuickQuid)in the UK due to unfavourable regulatory changes. This led to a one-time after-tax charge of $74.5 million which was equivalent of approximately 1 year of revenue.

Since Enova derives more than 90% of its revenue from the United States this regulatory environment is of particular interest. In October 2017 the so called "Small Dollar Rule" was issued by the Consumer Financial Protection Bureau (CFPB). The rule is of such importance because it would mean that after a consumer has two failed payment attempts the lender needs the consumers new authorisation to make further withdrawals from the customer's bank account. This would have a huge impact on Enova's consumer lending business with significant negative effects on charge-offs. However this rule is not in place as of now. It was rejected in November 2022 by a three-judge panel of the Fifth Circuit U.S. Circuit Court of Appeals. Currently this rule is under Investigation at the Supreme Court.

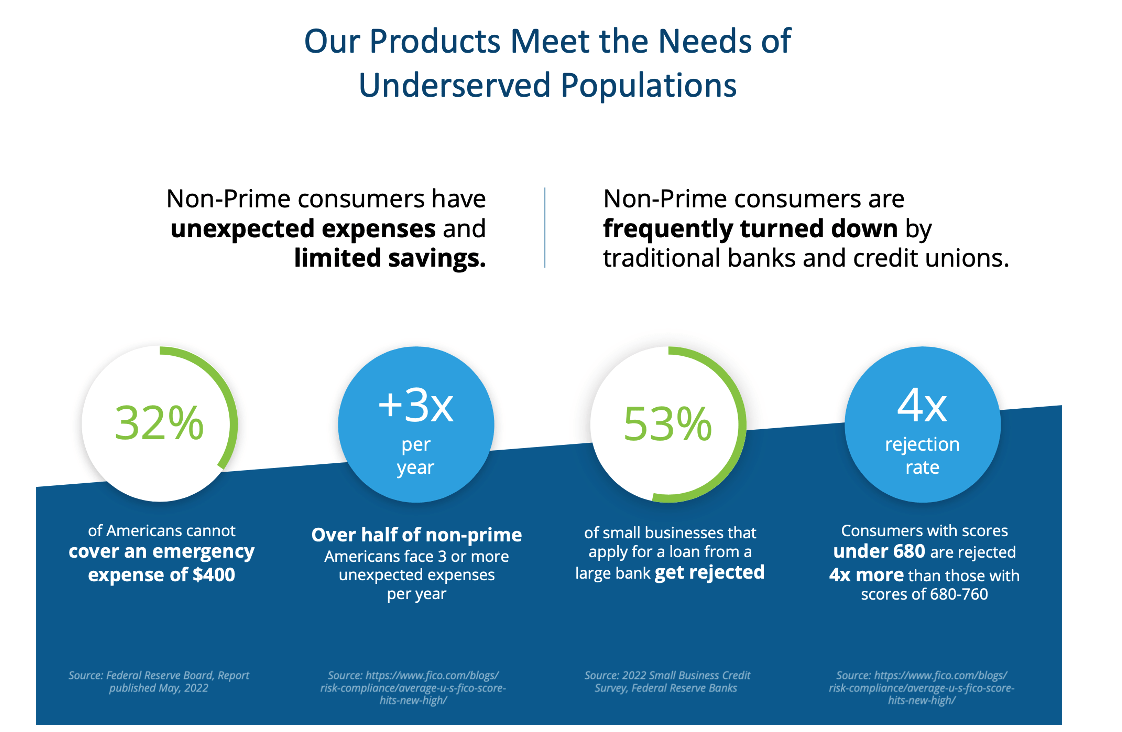

However I do believe this rule to not be approved since many people have no other access to credit than through lenders like Enova. Many non-prime credit consumers get rejected by traditional banks while at the same time having many unexpected expenses due every year (Fig. 6). Enova's loans are not meant to be something long-term but for unexpected emergencies like a car repair, debt consolidation or medical/dental and monthly bills. Often lenders like Enova are also the only way for non-prime customers to improve their credit score since they don't have access to loans from traditional banks. This gives them the chance for better credit conditions the next time they want a loan. Therefore non-prime consumers would be worse off without lenders like Enova.

{kind=link}

Figure 6: Needs of underserved customers (ir.enova.com/presentations-events)

If this regulation would get through 46% of Americas population that are sub-prime or below would be left with hardly any access to external financing and therefore leaving them completely vulnerable against unexpected expenses.

What is way more likely is that the Supreme Court leaves it to the individual states to decide about interest rate caps or other regulations. Currently Enova offer consumer loans only in 37 States which could of course change in the future if some of the States decide to implement regulatory changes regarding high interest loans.

However the management of Enova has seen these threats coming and is already reacting to it. They are diversifying their business more and more towards the SMB lending to make them less vulnerable to regulatory changes which mainly could have adverse effects on consumer loans. As stated before Enova is already actively restructuring and diversifying its business with currently 60% of its EBITDA coming from SMB loans.

Shareholder friendliness

Enova has repurchased nearly $140 million worth of shares representing around 10% of its current market cap. Since the average repurchase price was $35.59 they have bought back even more than 10%. For 2023 $158 million for share repurchase are authorised. This in general shows the management's confidence in their own company. They also state in their earnings calls that Enova is not fairly priced as a justification for their aggressive buyback strategy.

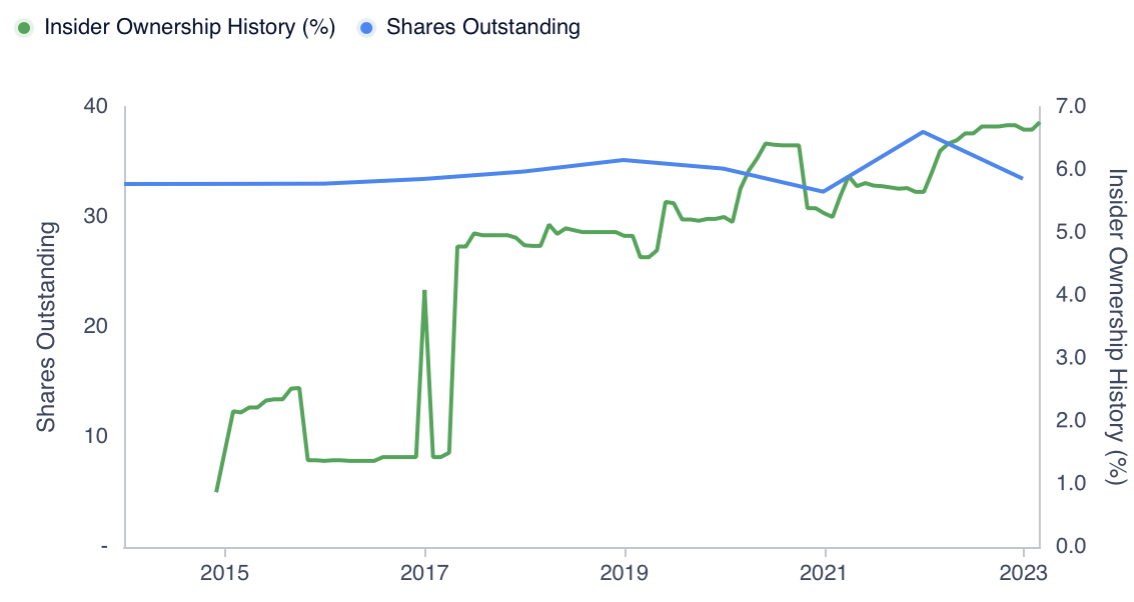

On the other hand Enova also uses share based compensation plans to motivate their employees. In the past two years there where around $18 million spent on these share based compensations which of course has a counter effect on the buybacks. This of course is not beneficial to the investor directly but nowadays it is a common practice to give share based compensation since it also aligns the employees interests with the ones of the shareholders. Therefore even though it does not seem good on first sight in my eyes it is acceptable. Especially since share buybacks exceed the share based compensation by far. As a result of these share based compensations insider ownership is growing steadily over the years which will possibly have a positive effect on motivation of the employees to give the best for "their" company (Fig.7).

{kind=link}

Figure 7: Insider Ownership (gurufocus.com)

Competitive advantage

After discussing all the above mentioned points we have to ask ourselves how can Enova ensure that it will continue to produce outstanding results. In other words where is Enova's competitive advantage?

The first big advantage for Enova is that their products are solely available online. This reduces costs and makes their products easier and faster to obtain. It also makes them more flexible to (regulatory) changes since they don't have to worry about having physical locations they have to close and open in a new place.

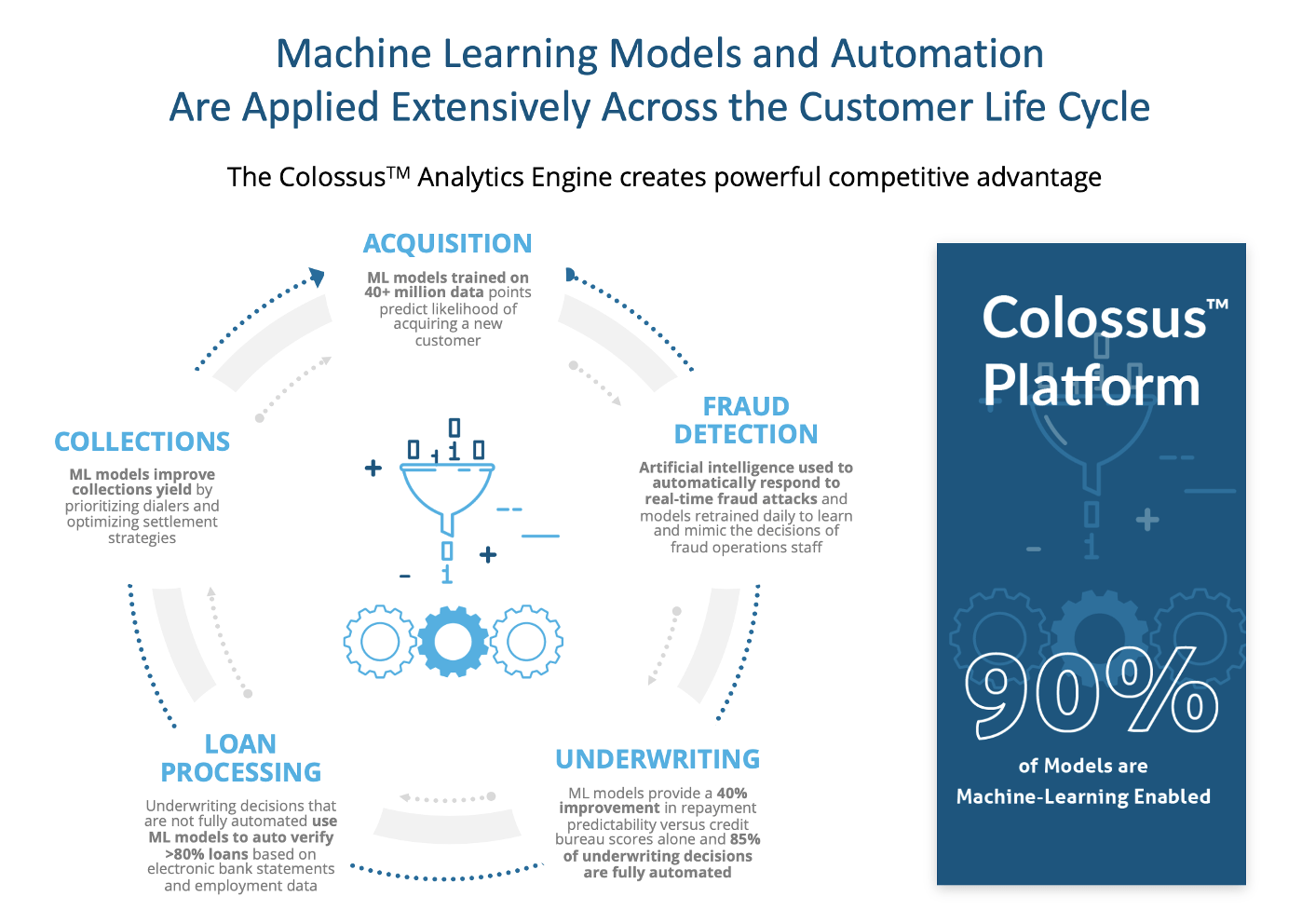

However one of their biggest advantages of their online only business model is their direct link from their products to their machine learning based underwriting algorithm. Enova has been an early entrant into the online lending business. This enabled them to collect data out of 57 million customer transactions which in turn enabled them to improve their underwriting algorithms.

{kind=link}

Figure 8: Machine learning enabled platform of Enova (ir.enova.com/presentations-events)

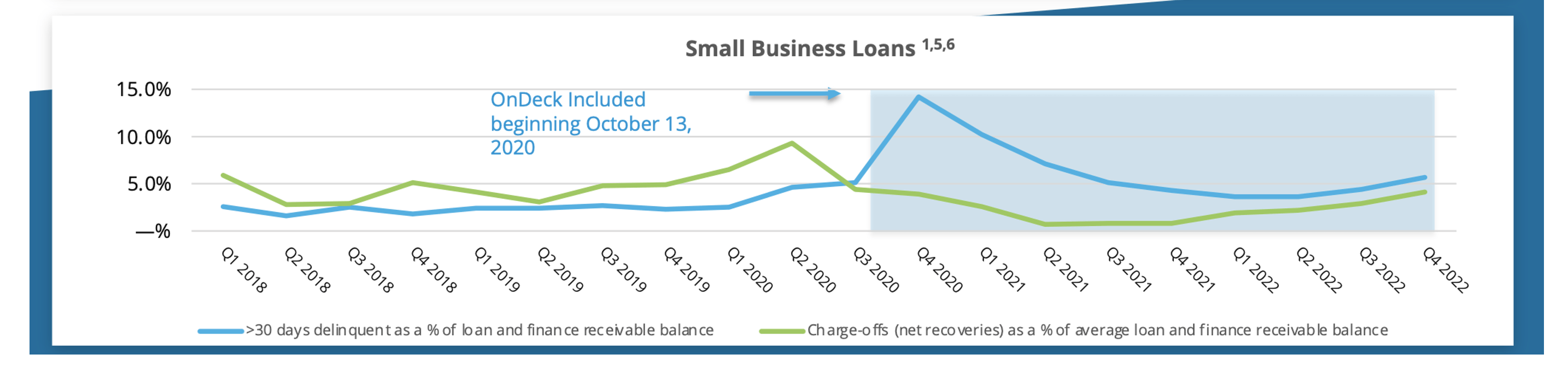

The power of their underwriting system is hinted through the acquisition of OnDeck. Due to the acquisition the loans that were >30 days delinquent rose strongly while afterwards falling again to normal levels. This could mean that Enova was able to implement their machine learning underwriting system into OnDeck and therefore was able to get the delinquencies back to normal.

{kind=link}

Figure 9: Delinquencies and charge offs before and after OnDeck integration (ir.enova.com/presentations-events)

Outlook and valuation

Enova is expecting to grow its originations between 10-15% and is expecting that it's revenue and earnings per share to grow even stronger than this. Q1 23 earnings will be flat to Q4 22 which is still an improvement if you look at the natural seasonality of their business with the highest earnings in Q3/Q4 and the lowest in Q1. Overall Enova wants to focus on more shorter maturity products to be less dependent to macro risk. They will focus further on expanding their SMB business but they don't want to maximise market share as they focus on quality of loans rather than quantity. This is why certain sectors are avoided like trucking for example. Enova continues with its aggressive marketing strategy and again plans to spend around 20% of its revenue on marketing.

Despite its stable financial position and strong growth outlook Enova is trading below its peers and all benchmarks with a forward P/E of around 6.3 (now it will be around 5.7 since Enova share price declined since the Investor presentation).

{kind=link}

Figure 10: Enova's P/E ratios and benchmarks ( https://ir.enova.com/presentations-events)

Enova trades at cheaper valuations despite its strong growth outlook and basically the same as 5 years ago when their product portfolio was far more concentrated on consumer loans. Therefore Enova should trade at least on par with its benchmark; the S&P 600 Consumer Finance Index. This implies an upside of at least 30%. When taking into account that Enova is growing at levels above the benchmark growth Enova should trade at even higher multiples.

Investor’s takeaway

Enova is a company with considerable regulatory challenges. However the management is well aware of these challenges and has successfully diversified its risk by increasing exposure to SMB lending which is now already bigger than consumer loans. The management of Enova has shown a consistent track record on execution. It has included OnDeck into its portfolio of businesses, diversified its business while at the same time maintaining a high quality of its products and also making sure that their company is attractive for new talent. Despite all these improvements Enova's valuation has not changed over the years. Therefore there exist a mismatch between valuation and value of the company. These findings imply an upside of at least 30% with a good possibility of an even higher upside when taking into account Enova's strong growth.

For further details see:

Enova: Significant Changes In Business, Insignificant Changes In Valuation