ENVA - Enova: Small Upside But Not A Screaming Buy

2023-07-10 15:15:31 ET

Summary

- ENVA has solid fundamentals and positioning to address a very large TAM.

- Growth may slow down in the near term despite a projected increase in marketing spend.

- I rate the stock neutral. My target price model suggests a 4% upside at year's end, which is not a compelling return in my view.

Enova (ENVA) is a financial technology / fintech company developing an AI-driven proprietary credit scoring and loan underwriting technology.

ENVA provides online-only loan and credit financing to non-prime consumers and SMBs in the US and Brazil, and generates revenues from fees and interests on the loan it provides to its customers.

In the non-prime loan and credit space, there is a competition from both traditional financing companies and other fintech companies, such as Avant, CURO ( CURO ), and Elevate. Over time, I expect the fintech players to continue gaining market share over the more traditional ones.

It seems to me that ENVA is a leader in the fintech segment. With annual revenue of ~$1.7 billion last year, ENVA is the largest business in terms of revenue compared to its peers. Elevate is a much smaller private company, while CURO is about third of ENVA in terms of revenue. Furthermore, CURO has been less profitable than ENVA.

ENVA went public in 2014 and traded at around ~$28 on the opening day. Since then, the stock has been through ups and downs, though overall it has trended up and gained ~84%. YTD alone, it is up by ~36%, trading at ~$52.

I rate ENVA neutral. My target price model suggests that ENVA may see a ~4% upside in FY 2023, which is rather minimal. I advise investors to explore other opportunities before allocating to ENVA.

Catalyst

Overall, I think ENVA has been executing well against its profitable growth objective . In recent times, ENVA’s fundamentals across growth, profitability, and cash flow generation have been solid. ENVA also has a strong balance sheet.

{kind=link}

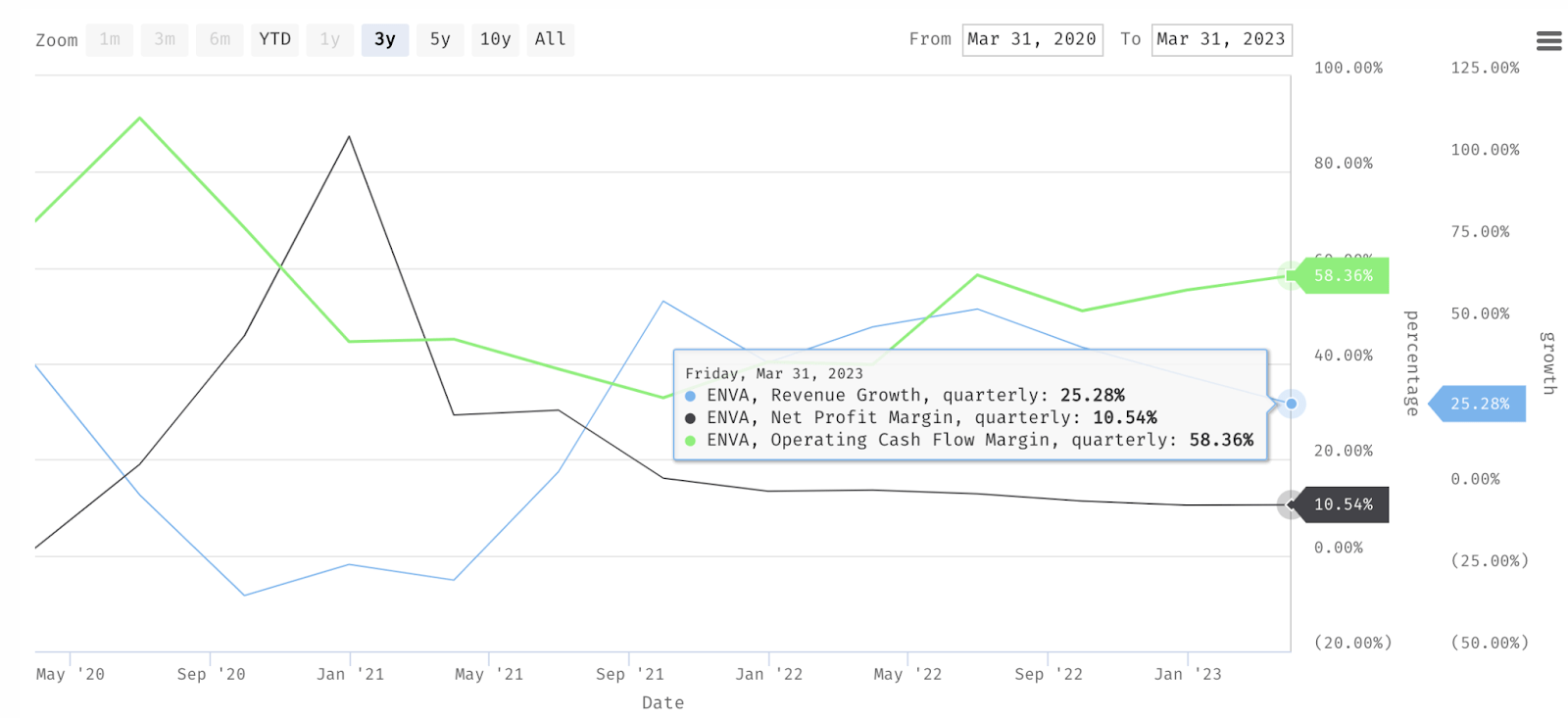

The business was heavily impacted by COVID-19 between 2020 and 2021 when revenue growth declined. However, since then, growth has accelerated to 40% - 50%. In Q1, revenue growth decelerated slightly to ~25%, a relatively solid performance despite the ongoing tough macro situation and Q1’s seasonally weak demand. Net margin has also expanded to 10% - 30% from merely single-digits pre-COVID, demonstrating ENVA’s ability to improve profitability while maintaining a solid growth outlook. Meanwhile, ENVA’s cash flow generation has been exceptional. The operating cash flow / OCF margin was ~58% in Q1 and has been on an expansion since last year.

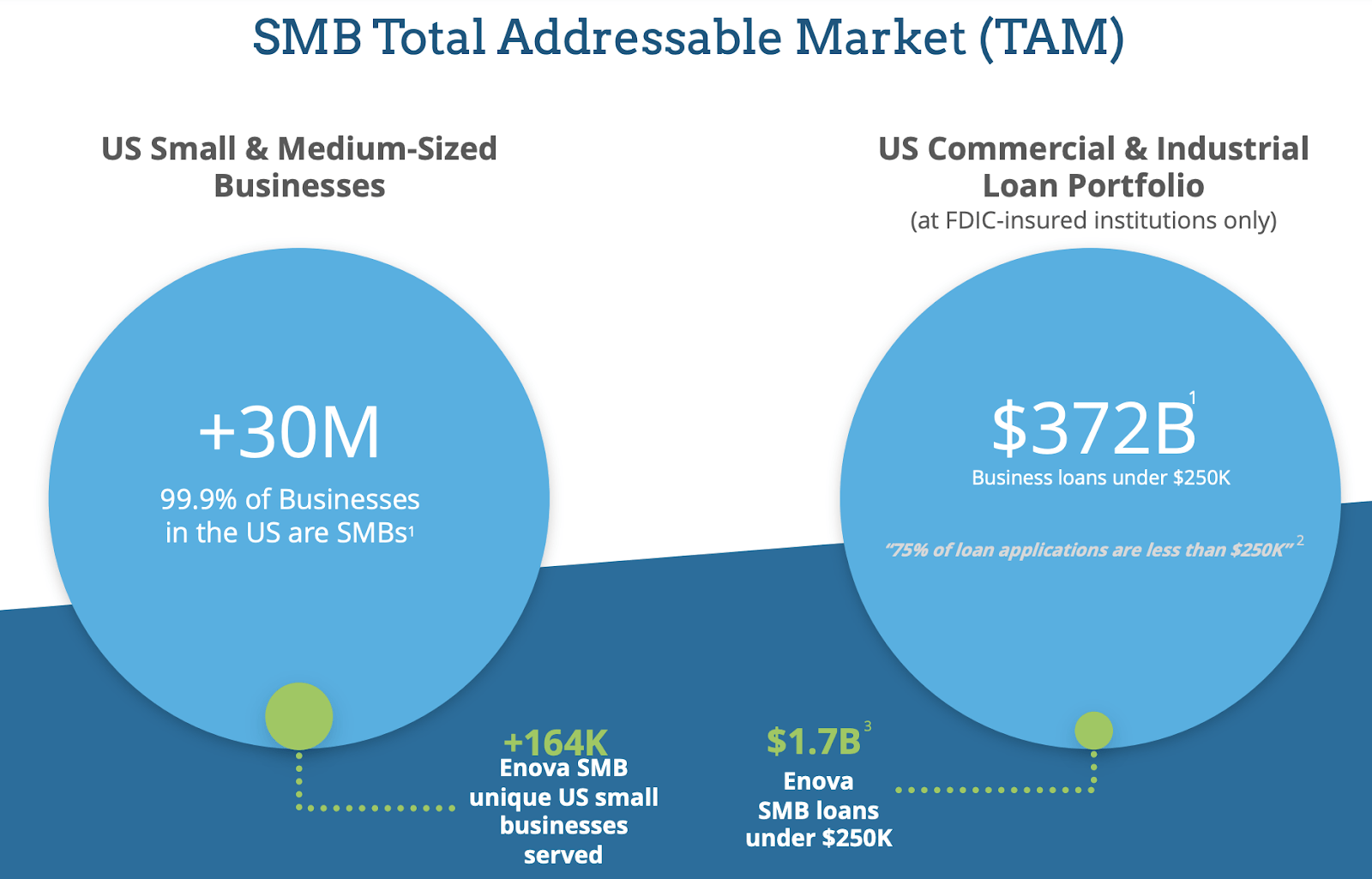

I believe that ENVA is in a good position to maintain profitable growth. To begin with, the TAM is still very large for both the non-prime consumer and SMB loan and credit market in the US.

{kind=link}

With a TAM of $372 billion and under 1% penetration, I see a long runway for growth for ENVA in the SMB segment alone. Furthermore, given ENVA’s proven AI-driven technology and online-only application and disbursement systems, I expect it to continue disrupting the brick-and-mortar competitors like traditional savings and loans or banks. I think that all of these are captured in ENVA’s solid double-digit growth despite its large scale as a ~$1.7 billion company and SMB being the largest segment.

Though growth will slow down further in Q2, and potentially FY 2023 too, growth may also accelerate sometime next year. To me, it seems that given the temporary macro weakness, ENVA has not been firing on all cylinders just yet. ENVA only spent 17% of its revenue on marketing in Q1, lower than 24% of revenue last year, suggesting a lot of room for higher growth opportunities here once it ramps up marketing.

Risk

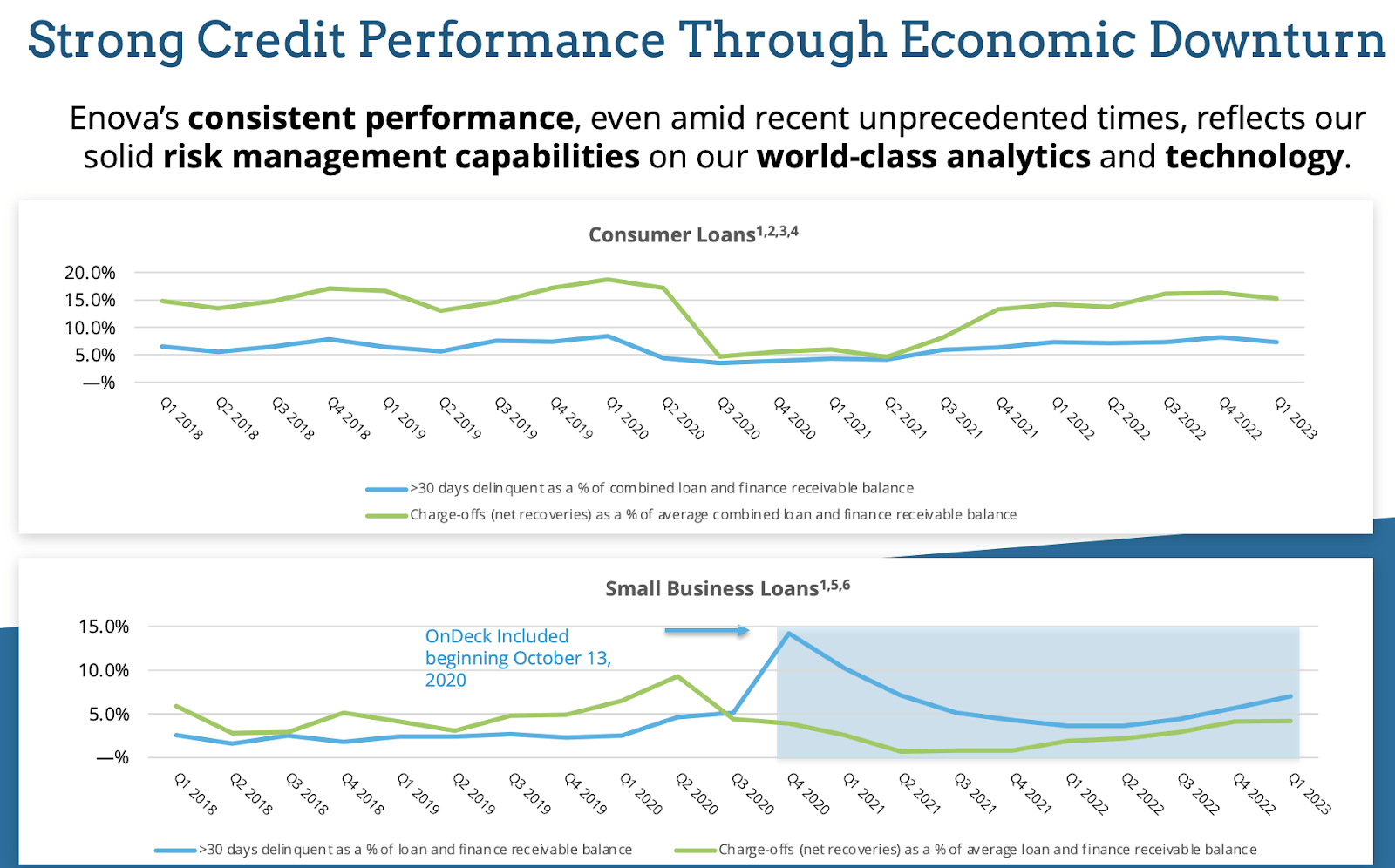

As per my earlier comment, the reason why growth will slow down in Q2 is because ENVA may also continue to be a bit cautious in opening up its credit model to disburse more loans given the macro situation.

{kind=link}

ENVA’s more balanced approach as of Q1 has been reflected in the rather plateauing net charge-offs and >30 days delinquency rate. However, these figures seem to have been trending up for SMB loans, implying that ENVA may wish to tighten its credit model a bit more into Q2 and FY 2023 to balance risk and growth.

As such, despite the attractive growth potential longer-term, ENVA will potentially maintain a more cautious stance in FY 2023, resulting in lower growth expectation for the full year. In Q2 alone, ENVA will actually project a sequentially flat revenue, implying a growth deceleration from Q1. Moreover, it seems that being more selective in its lending approach may also make growth a bit more expensive for ENVA - it is interesting to learn that growth may decelerate in Q2 despite ENVA projecting an increase of its marketing expenses to 20% of revenue.

{kind=link}

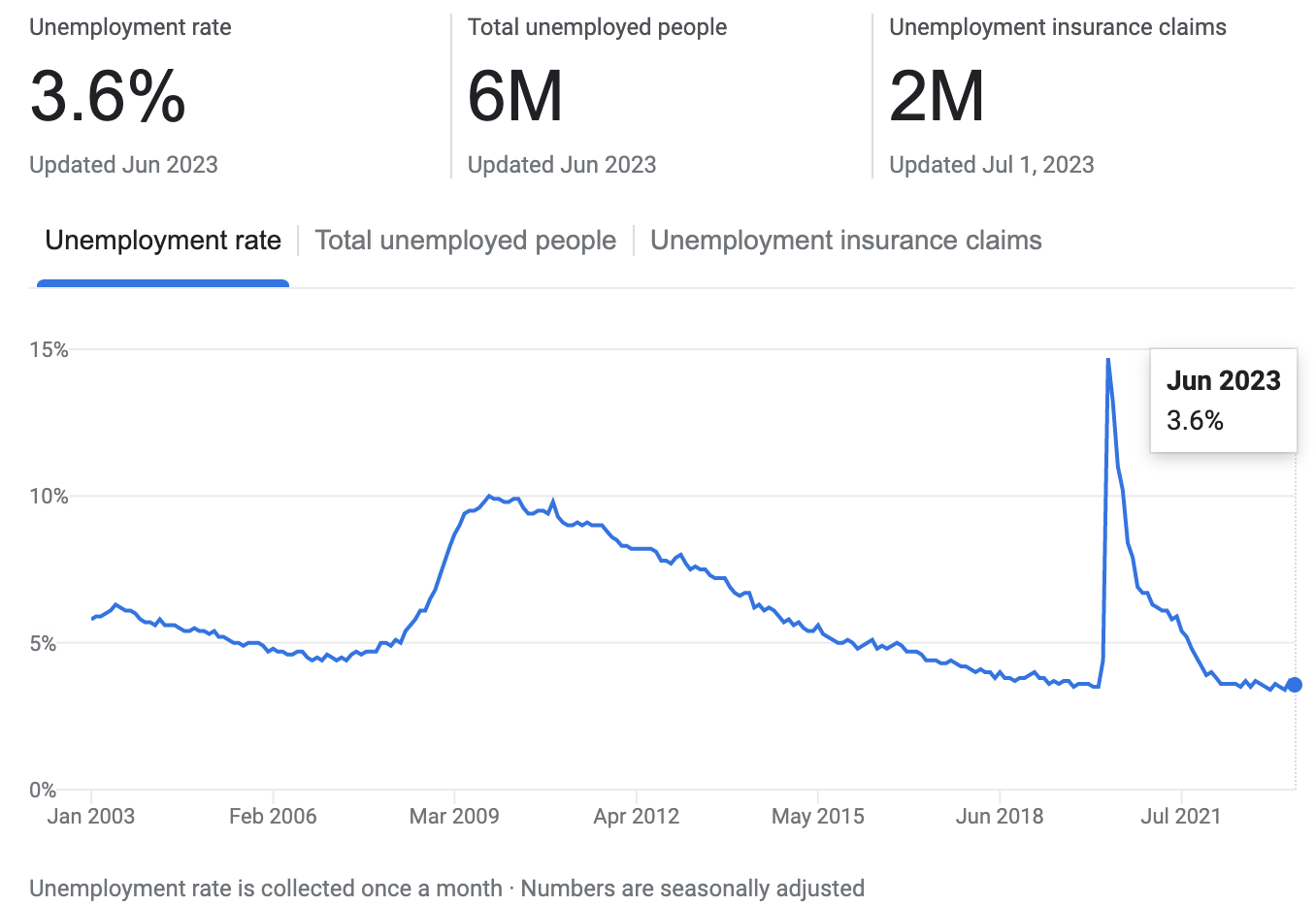

The unemployment rate also saw an elevated level to 3.7% and 3.6% in May and June after ENVA released its earnings report in April. Though the hike was minimal in my opinion, it remains uncertain if the situation will continue or how it will affect ENVA’s SMB customers. In a worse-case scenario, though, this may affect demand for SMB loans to some extent, considering that payroll payment is one of the main reasons why SMBs borrow money from ENVA.

Valuation / Pricing

My target price for ENVA is driven by the following assumptions for the bull vs bear scenarios of the FY 2023 target price model:

-

Bull scenario (60% probability) assumptions - ENVA to finish FY 2023 with diluted EPS of ~$7.2, implying a ~16% EPS growth, in line with the management’s suggestion in Q1 earnings call that EPS growth may surpass the loan origination growth range of 10% - 15%. I assign ENVA a P/E multiple of 8x across both scenarios, where it is currently trading at.

-

Bear scenario (40% probability) assumptions - ENVA to finish FY 2023 with diluted EPS of ~$6.2, pretty much flat YoY.

author's own analysis

Consolidating all the information above into my model, I arrived at an FY 2023 weighted target price of ~$54 per share. With ENVA trading closer to ~$52 per share recently, this represents a 4% upside.

I would rate ENVA neutral at this point. Given the 4% expected return, ENVA does not seem to be a highly interesting buy. However, my target model also further suggests that there is a possibility for ENVA to unlock a ~10% upside, which may only happen if ENVA somehow can outperform its EPS growth expectation according to my bull case projection. Given the rather limited upside, I feel that it is worth exploring other opportunities before deciding to allocate to ENVA.

Conclusion

ENVA has demonstrated strong execution in achieving its profitable growth objective, with solid fundamentals in terms of growth, profitability, and cash flow generation. However, considering the challenging macroeconomic conditions, ENVA may exercise caution in expanding its credit model to increase loan disbursement, effectively resulting in a slower growth outlook.

Based on the expected 4% return according to my target price model, I maintain a neutral rating on ENVA. The stock does not appear to be a particularly compelling buy, considering the limited upside potential. It may be worthwhile to revisit ENVA later or explore alternative investment opportunities before making a buying decision.

For further details see:

Enova: Small Upside, But Not A Screaming Buy