NPO - EnPro Industries: Guiding For A Flat 2023 Isn't Very Exciting

2023-08-16 16:32:44 ET

Summary

- EnPro Industries Inc. reported disappointing financial results and revised its guidance for 2023, indicating flat or minimal growth.

- The company operates in the industrial sector and has a diversified set of end markets, with the largest being semiconductors.

- The company faces risks related to its debt levels, potential goodwill impairments, and a high valuation compared to its sector.

Investment Rundown

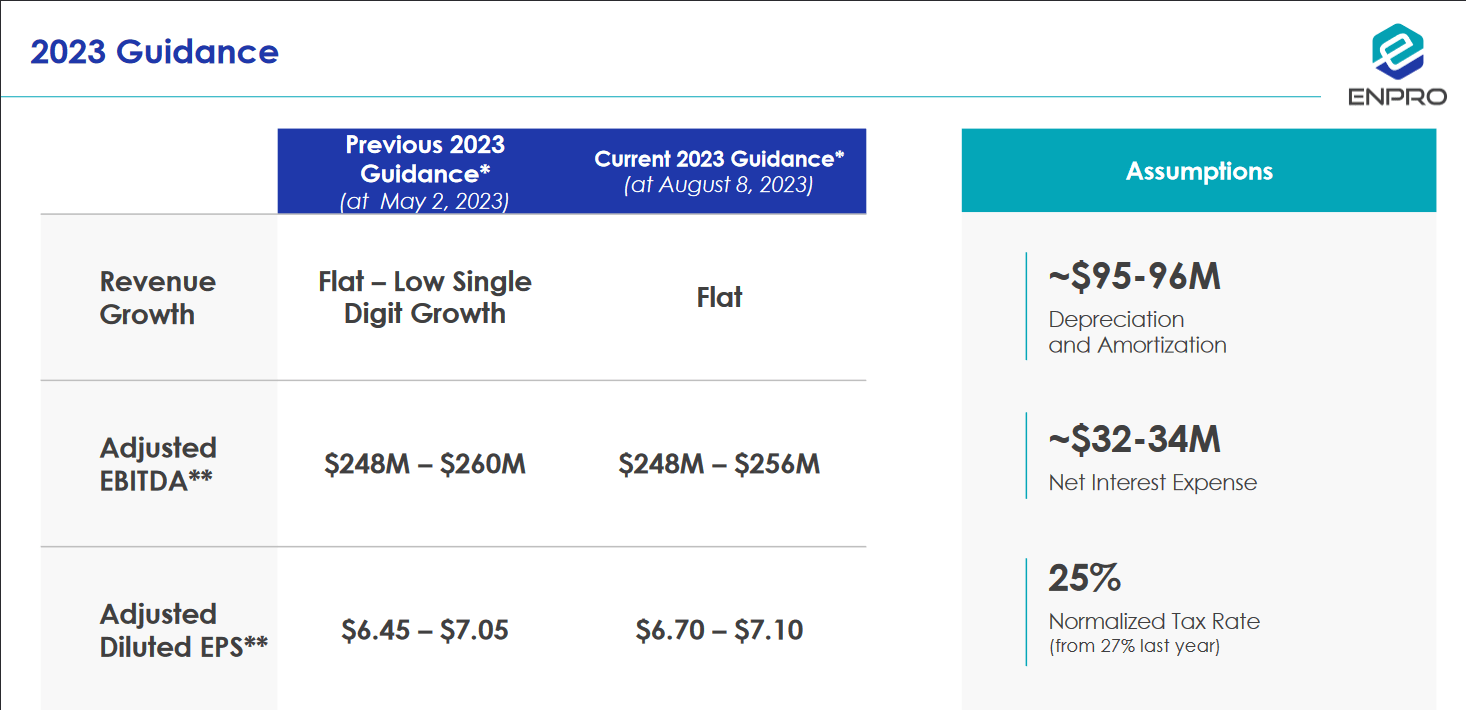

The last report from EnPro Industries, Inc. ( NPO ) showcased a beat on both the top and bottom lines, which should have made the market excited but with the revised guidance for 2023, it looks like 2023 will be a relatively flat year in terms of growth. Previous guidance was for low single-digit growth, but with new predictions, I don’t think paying around 20x earnings is worth paying for that type of outlook.

A slight increase in the outstanding shares YoY seems to cloud where the actual value is with the company. NPO operates in the industrial sector, and growth has been immense as the market looked positively at what NPO might be able to grow into. The markets that NPO deals with are very diverse and include the likes of semiconductor and power generation. However positive the outlook might be for the company there needs to be solid execution and growth before I think a buy rating will be established for them. In the meantime, I am rating NPO a hold instead.

Company Segments

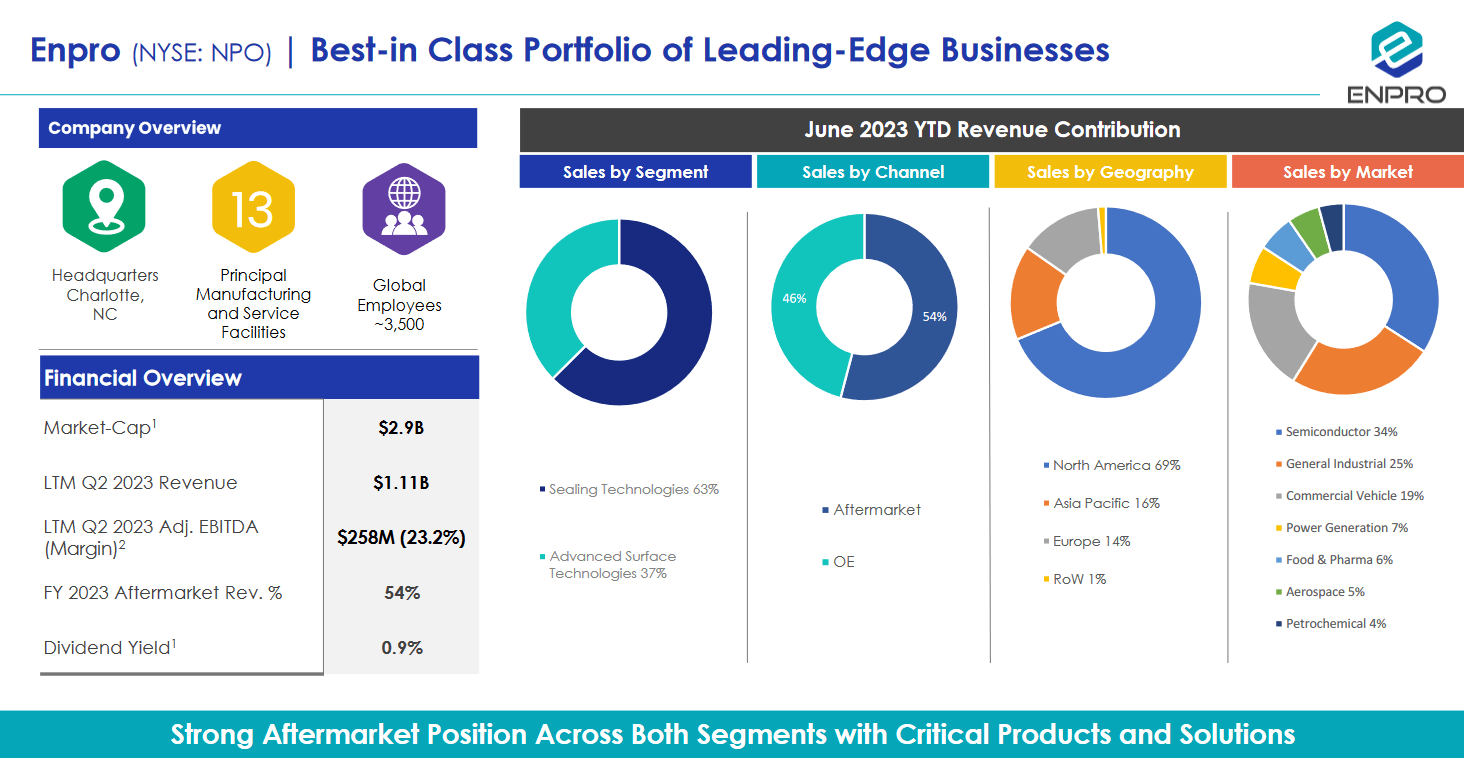

NPO is a company that specializes in the development, manufacturing, and distribution of products and solutions aimed at safeguarding critical environments both domestically and across international markets NPO operates efficiently across two key segments: Sealing Technologies and Advanced Surface Technologies.

{kind=link}

In the Sealing Technologies segment, NPO focuses on providing a variety of critical solutions that cater to the various needs of industries around the world. Offering within this segment include single-use hygienic seals, which play a pivotal role in industries such as pharmaceuticals and food processing. These specialized seals are designed to maintain strict hygiene standards while preventing contamination, making them essential components for applications where purity is paramount.

In the Advanced Surface Technologies segment, NPO focuses on providing a variety of services that are aimed at giving important service solutions to modern industries. Cleaning services, coating, and testing are some of the services offered but also verification services for critical components and assemblies used in the semiconductor industry for example.

{kind=link}

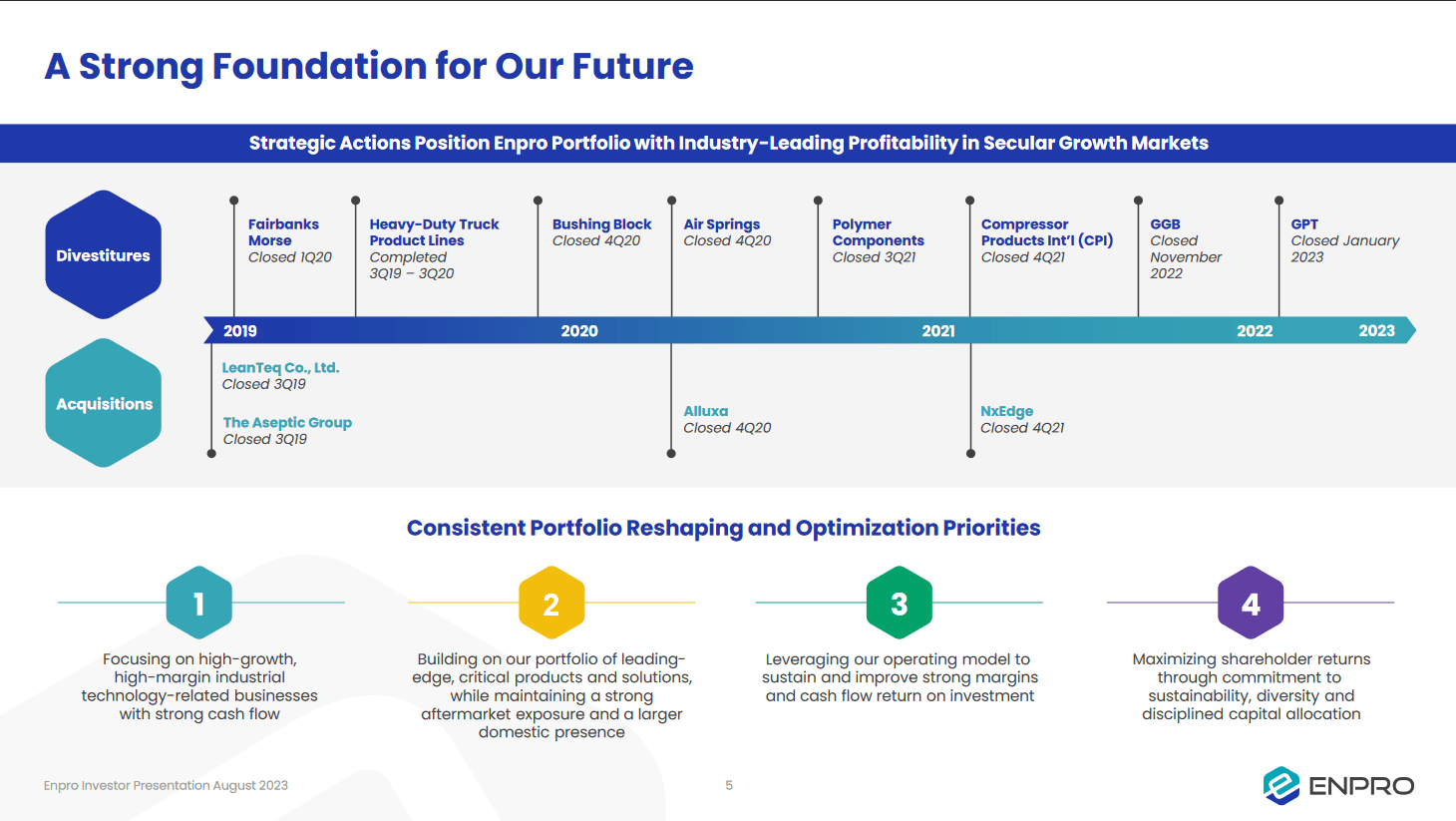

As we briefly went over before, the company has a diversified set of end markets that it caters to. The largest one is semiconductors which as we have discovered is a rather cyclical industry that had a big bull run in the last few years but right now seems to be consolidating somewhat instead. This has meant that demand has been more difficult to find for NPO and it seems that ultimately was what led to the poor guidance for 2023 indicating flat or extremely little growth at all. As for the segments in the business, the largest one is the sealing technologies which helped offset some of the losses in the other segment as demand from aerospace and nuclear supported sales growth.

{kind=link}

Guidance for the year suggests the revenue producing no growth at all. However, there is a slight improvement as the projected EPS got a slight raise as the management expects themselves to be able and rein in costs like wage inflation and materials. I think achieving these results will be heavily reliant on operational excellence and no further drops in sales from the segments. If the smallest segment once again showcases double-digit YoY declines then I think the share price will begin to tumble to reflect the difficult nature of the market right now.

{kind=link}

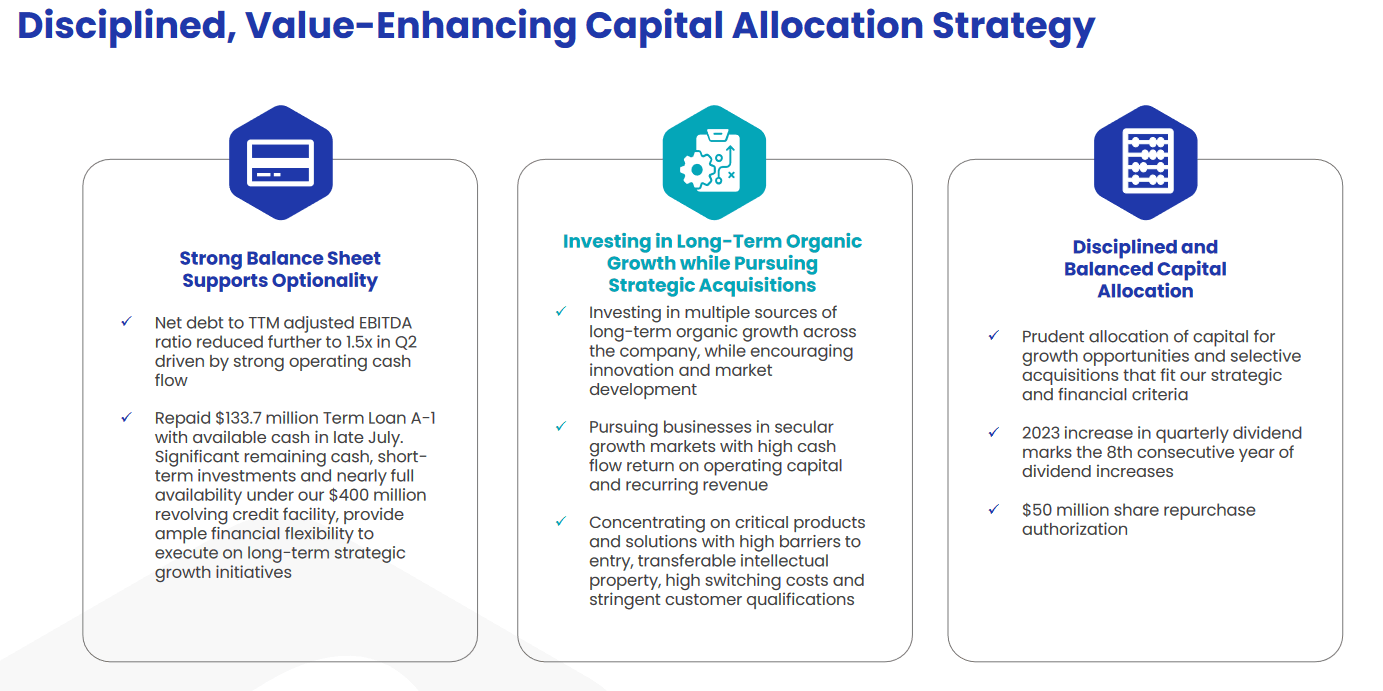

If you are an investor in the company then I think it's reasonable to assume that the company will continue distributing value to shareholders. Some of how they do this is through a dividend and buying back shares. Right now the company has $50 million in share repurchases authorized which wouldn't make such a big difference as the market cap is over $2.8 billion. However, as the FCF margin continues to grow I think it's likely to assume the buybacks will too.

Risks

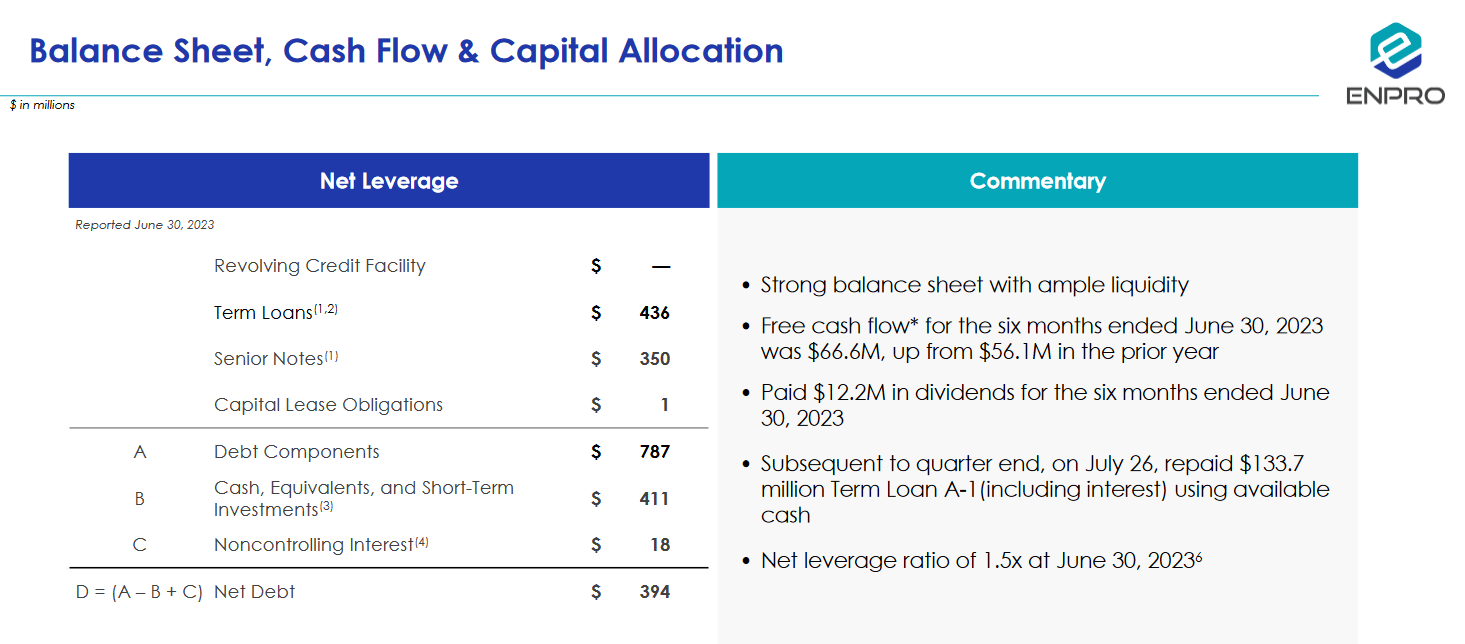

Navigating the landscape of risks, it becomes evident that NPO is not immune to the challenges in the current market environment of quickly shifting demand from one year or even one quarter to another. One of the notable risks stems from the company's total amount of debt, which can introduce financial constraints and impact its ability to invest in growth initiatives. Long-term debts sit at $767 million and during the quarter the company paid back $7.9 million. The company paid out more dividends than paying back debt. I think that priority should lie on reducing debt rather than keeping up the quite low dividend yield, which is right now even below 1%.

Another risk that shouldn't be overlooked is the potential for goodwill impairments. As changes in economic conditions or shifts in business strategies could result in the need for a reassessment of the carrying value of goodwill. This will likely cause the balance sheet to drop in value and result in NPO trading at a high p/b. The risk of the share price being reduced by this to reflect the previous multiple is quite likely in my opinion.

Financials

It's worth highlighting some of the parts of the balance sheet a bit more I think as we have been critiquing it above here.

{kind=link}

The company has as we know $767 million of long-term debt, which has been reduced slightly on a YoY basis. Cash does sit quite high at over $400 million so seeing the company being able to pay off at least 50% of the debt should keep any challenges at bay for the next several years at least. If FCF continues like they are, resulting in $66 million in the first six months of 2023 then NPO is in a great spot to continue paying down debt and become less leveraged. The company isn't very leveraged right now either, the net leverage ratio is just at 1.5 which is a healthy spot to be in.

Final Words

One of the issues I have right now with NPO and what ultimately makes me not rate it a buy is the fact that the valuation isn't looking very attractive, especially not in combination with the rather lackluster growth outlook the company has. With flat revenue growths, the p/s of 2.6 continues to look expensive. It's a premium of over 80% to the rest of the sector.

Besides that, there aren't enough incentives here to make me want to buy. The company doesn't have a large amount of capital authorized for buybacks, and the dividend is below 1%. This leads me to rate NPO a hold rather than a buy right now.

For further details see:

EnPro Industries: Guiding For A Flat 2023 Isn't Very Exciting