NPO - EnPro: Successful Divestitures M&A And New Stock Repurchase Imply Undervaluation

2023-05-11 06:14:29 ET

Summary

- EnPro specializes in designing, developing, manufacturing, and marketing high-tech proprietary products and solutions for critical applications in growing end markets.

- In my view, further investments in businesses with compelling margins, leading technology, high cash flow, and return on investment can be expected.

- I would expect further attention from new investors after the recent increase in quarterly dividends and the new stock repurchase program from 2022 to 2024.

EnPro Industries, Inc. ( NPO ) recently delivered a conservative guidance for 2023. In addition, it continues to report successful divestitures and M&A operations. After noticing the recent dividend increase and the new stock repurchase program, I believe that more investors will likely have a look at NPO. Under my own financial model that includes more innovative products and new acquisition of targets, I obtained a fair valuation that is significantly higher than the current stock price. There are risks from the total amount of debt, potential goodwill impairments, or lack of raw materials, however I believe that the stock price could trade higher.

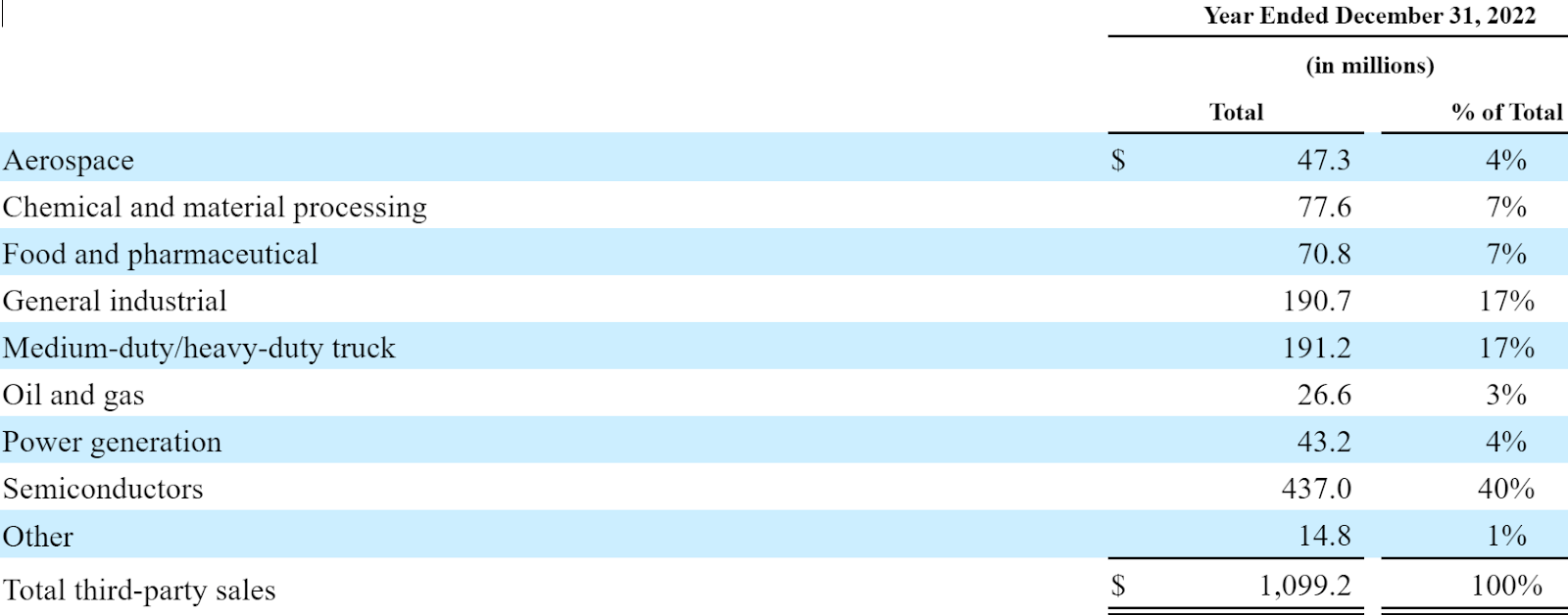

EnPro Is Geographically Diversified. It Is Working For Many Different End Markets.

EnPro specializes in designing, developing, manufacturing, and marketing high-tech proprietary products and solutions for critical applications in growing end markets.

Its portfolio of businesses offers products with high barriers to entry, compelling margins, strong cash flow, and perpetual recurring/post-sale revenue.

With 13 primary manufacturing and service facilities in 6 countries, I believe that geographic diversification will most likely help the company report less revenue volatility. With most of the revenue coming from the United States and Europe, more than 20% of the total amount of sales comes from other jurisdictions.

{kind=link}

The business is divided into two segments: Sealing Technologies and Advanced Surface Technologies. The business model is focused on offering innovative and personalized solutions to its end customers in various markets. The number of industries served is quite meaningful, which may be appreciated by investors looking for diversification. EnPro works with clients in the semiconductor industry, the Aerospace industry, the truck industry, oil and gas, and the chemical industry among others.

{kind=link}

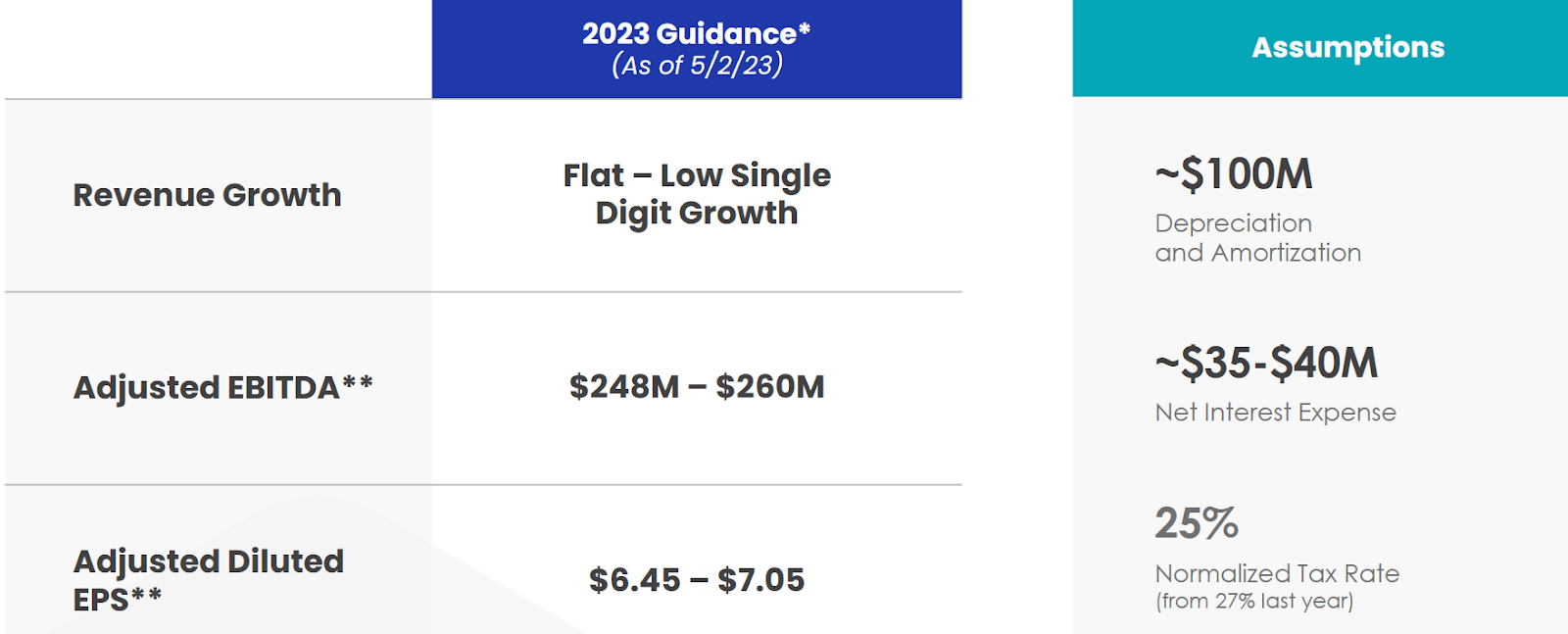

Conservative Market Expectations That Include Sales Growth And Positive EPS

I believe that EnPro did not convince the market with the most recent quarterly release. Even though the EPS was better than expected , I believe that the guidance was not that optimistic. EnPro expects revenue growth, but only low single digit growth, with an adjusted EBITDA of close to $248-$260 million and EPS close to $6.45-$7.05. Considering that these numbers are conservative, I cannot discard more EPS surprises in the coming years.

{kind=link}

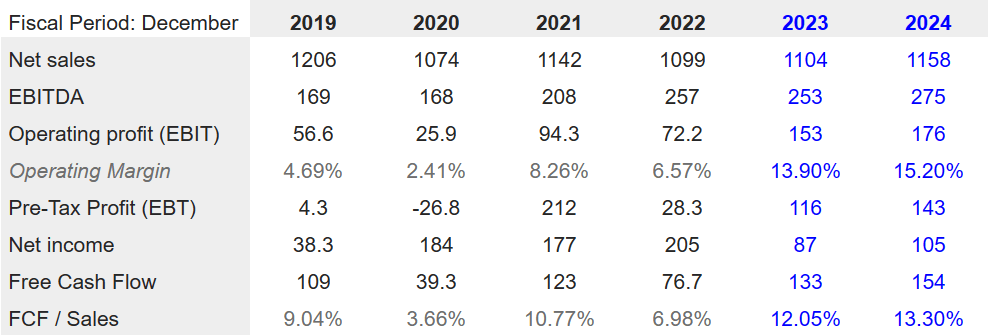

The expectations from other market analysts are a bit more optimistic than that of management. Analysts expect sales growth in 2023 and 2024 with operating margin increases and FCF margin increases. In my view, most investors are expecting better numbers in 2024 than that in 2023.

2023 net sales are expected to be close to $1104 million. 2023 EBITDA would be close to $253 million, with 2023 operating margin of 13%, 2023 net income of $87 million, and 2023 free cash flow of $133 million. Market expectations also include 2024 net sales of $1158 million, 2024 EBITDA close to $275 million, and 2024 operating margin close to 15.20%. Finally, 2024 net income would stand at $105 million with 2024 free cash flow of $154 million.

{kind=link}

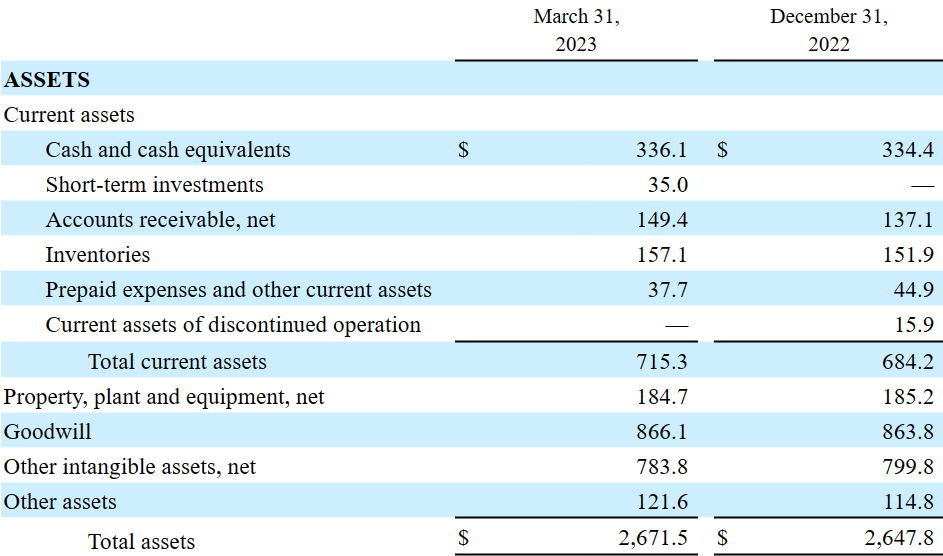

Solid Balance Sheet, But Investors May Need To Monitor The Total Amount Of Debt

As of March 31, 2023, the company reported cash and cash equivalents close to $336.1 million, short-term investments of around $35 million, and accounts receivable of $149.4 million. Also, with inventories close to $157.1 million, prepaid expenses and other current assets stood at $37.7 million. Total current assets are equal to $715.3 million, which appear significantly larger than the total amount of current liabilities.

Property, plant and equipment was equal to $184.7 million, with goodwill of $866.1 million, other intangible assets of $783.8 million, and total assets of $2.671 billion. The asset/liability ratio stands at more than 2x, so I would say that the balance sheet remains solid. With that, I believe that investors will do good by having a close look at the total amount of debt.

{kind=link}

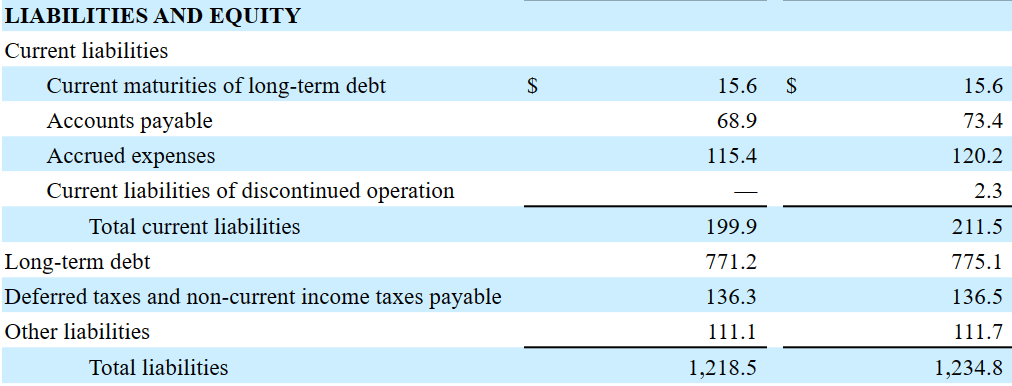

Current maturities of long-term debt stood at $15.6 million, with accounts payable worth $68.9 million, accrued expenses of $115.4 million, and long-term debt of $771.2 million. Also, with deferred taxes and non-current income taxes payable of close to $136.3 million, total liabilities stood at $1.218 billion.

{kind=link}

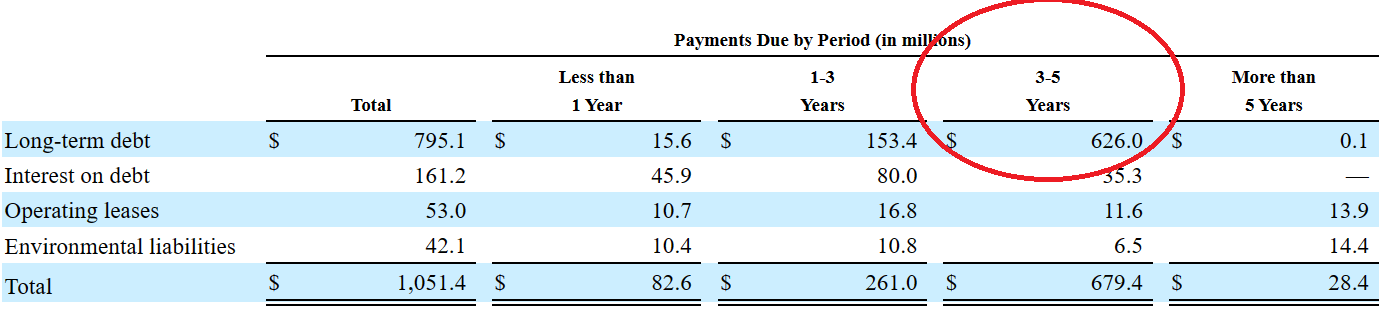

I studied when EnPro Industries will likely pay its debt obligations and contractual obligations. I believe that the most traumatic period is in 3-5 years, when EnPro may have to pay long-term debt worth $626 million, interest on debt close to $35.3 million, operating leases worth $11.6 million, and environmental liabilities of $6.5 million. I believe that the accumulation of future FCF and perhaps negotiations with debt holders will allow management to pay its contractual obligations.

{kind=link}

My DCF Model Includes Innovation, Successful New Acquisitions, Divestitures, And Stock Demand Thanks To Recent Dividend Increases And The Stock Repurchase Program

Under my DCF model, I assumed that EnPro Industries will continue to show successful disciplined organic growth as well as innovation. In my view, further investments in businesses with compelling margins, leading technology, high cash flow, and return on investment can be expected.

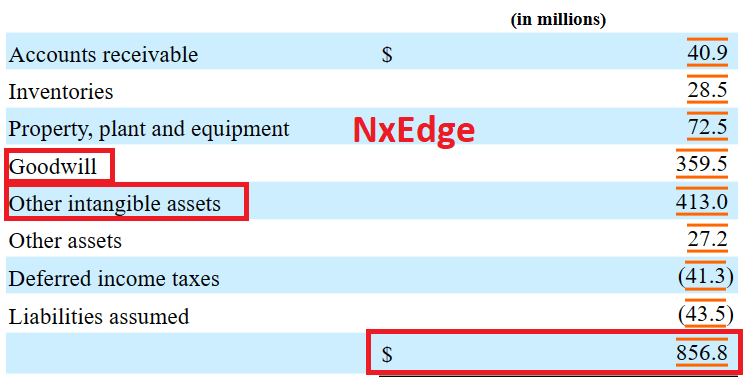

EnPro Industries is constantly evaluating further acquisitions, so I assumed that management will successfully find new targets like NxEdge. In this regard, I believe that offering some more information about recent acquisitions makes sense. EnPro Industries acquired NxEdge because of its know-how and qualifications at top customers, which were ideal for the Advanced Surface Technologies segment. With a total valuation of $856 million, EnPro included goodwill of $359 million and other intangible assets of $413 million, so in my view, what matters in the acquisitions is the intangibles acquired.

NxEdge is a leading supplier offering a set of integrated capabilities with unique processes resulting in a broad range of qualifications at top customers. NxEdge is included in our Advanced Surface Technologies segment. Source: 2021 10-k

{kind=link}

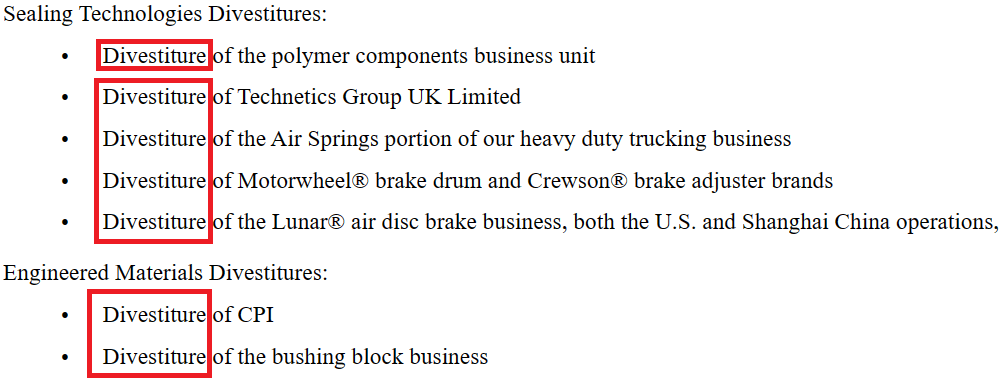

I also assumed that EnPro may continue to design new successful divestitures. The most recent divestiture of Garlock Pipeline Technologies, Inc. included a pre-tax gain, however management has done many other divestitures in the past. The company has a lot of expertise in the M&A markets, so I believe that future divestitures will also be profitable.

On January 30, 2023 we completed the sale of Garlock Pipeline Technologies, Inc. ("GPT") for gross proceeds of $31.4 million. We recorded a pre-tax gain on the sale of discontinued operations of $14.6 million in the first quarter of 2023.

In the third quarter of 2022, we entered into an agreement to sell our GGB business and announced our intention to sell Garlock Pipeline Technologies, Inc. ((GPT)). These businesses, along with Compressor Products International ((CPI)), which was divested on December 21, 2021, comprised our entire Engineered Materials segment ("Engineered Materials"). Source: 10-Q

{kind=link}

Besides, I would expect further attention from new investors after the recent increase in quarterly dividends and the new stock repurchase program from 2022 to 2024. In my view, once investors learn that management is taking care of shareholders, we may see an increase in stock demand, which may drive the stock price up.

In February 2023, our board of directors approved an increase in the quarterly dividend to $0.29 per share, from $0.28, representing our eighth consecutive year of dividend increases. Source: 10-k

In October 2022, our board of directors authorized the expenditure of up to $50.0 million for the repurchase of our outstanding common shares through October 2024. Source: 10-Q

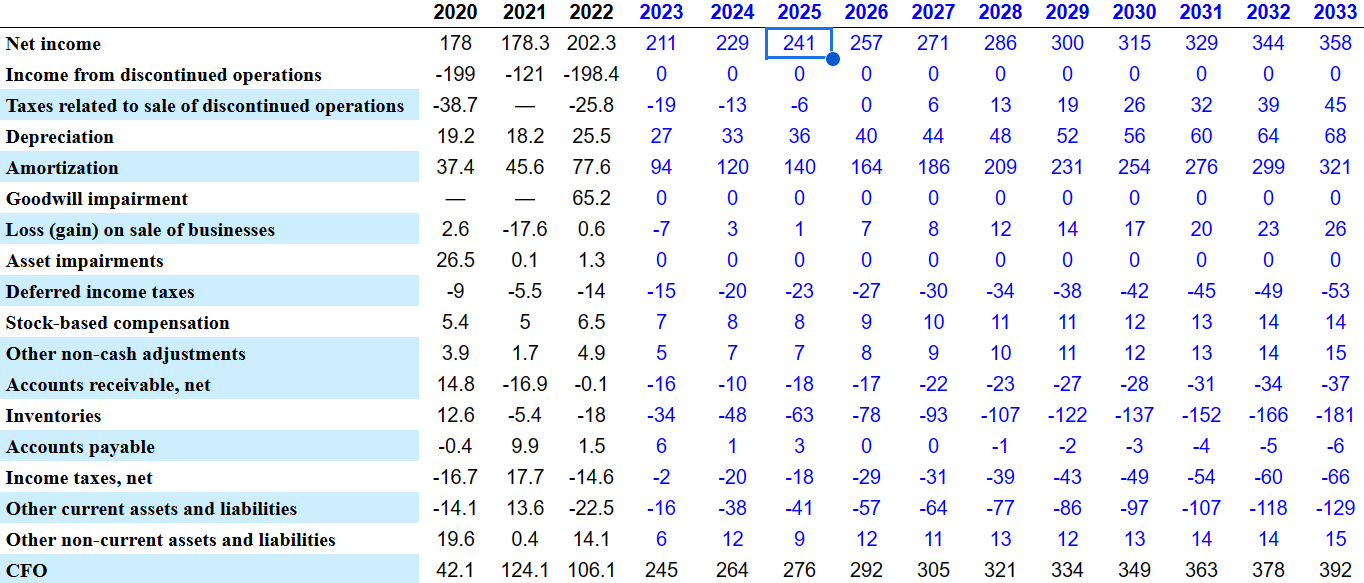

My financial model includes conservative assumptions like net income growth close to 4%-5.7%, D&A growth, stock-based compensation growth, growing accounts receivable, growing changes in inventories, and CFO growth. Note that I have not included losses from discontinued operations.

{kind=link}

More in particular, my numbers included 2033 net income of $358 million, taxes related to sale of discontinued operations worth $45 million, depreciation of $67 million, amortization close to $321 million, and 2033 stock-based compensation of $14 million. Also, with 2033 changes in accounts receivable of -$37 million, changes in inventories of -$182 million, and 2033 changes in accounts payable of -$6 million, 2033 CFO would stand at $392 million.

{kind=link}

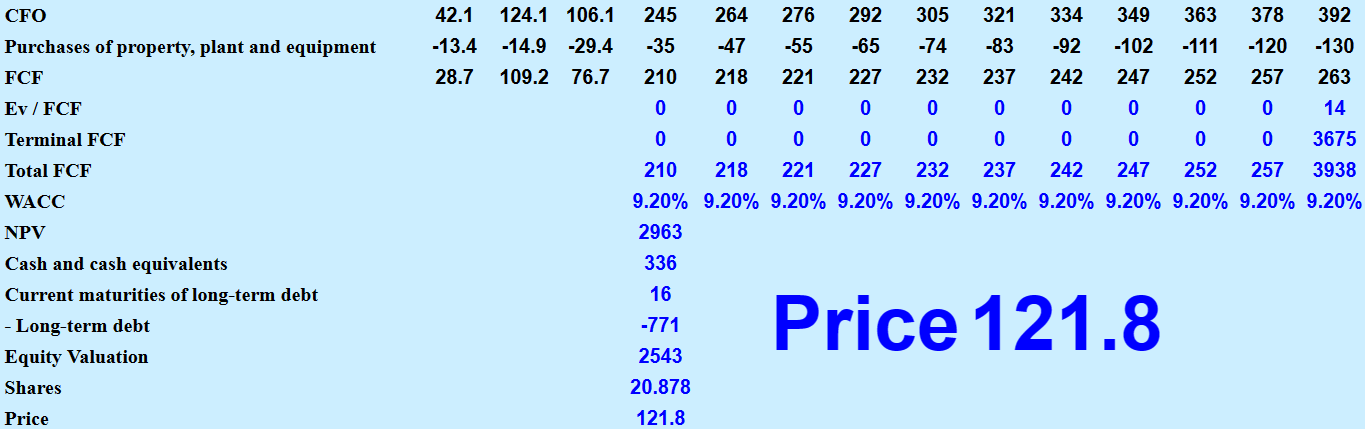

If we also assume 2033 purchases of property, plant and equipment of -$130 million, 2033 FCF would stand at $262 million. Finally, with EV/FCF ratio of 14x, the terminal 2033 FCF would be close to $3.675

If we assume a WACC of 9.2%, the enterprise value would stand at $2.962 billion. Summing cash and cash equivalents of $336.1 million, and subtracting current maturities of long-term debt worth $15.6 million and long-term debt of -$771.2 million, the equity valuation would be $2.543 billion, and the implied price would be $121 per share.

{kind=link}

Competitors

Intense competition in all areas of business presents challenges in maintaining a competitive position and meeting customer needs. The reduction in the number of providers and the commodification of some products and solutions may affect market demand.

In addition, low-cost foreign competition and improved product and service quality may affect the replacement cycle. I believe that continued investment in manufacturing, marketing, customer service and support, distribution networks, and development of new products and solutions is necessary to remain competitive. However, lack of resources and competitive pressure can adversely affect the business and financial situation.

Risks

The company faces multiple risks from lack of raw material costs, new technological disruptions of emerging competitors, and loss of key personnel. In addition, external factors such as climate change and environmental laws and regulations may affect the business and operating results.

In particular, in this case, I believe that risks related to previous acquisitions are quite relevant. If management finds that the acquisitions recently executed will not provide the synergies expected, or the products acquired are not as innovative as expected, shareholders may suffer goodwill impairments. As a result, EnPro may see declines in book value per share, which would most likely lead to decreases in the stock price.

EnPro Industries may also suffer from restrictions from debt covenants or other agreements with debt holders. EnPro may not be able to acquire certain targets, which may lower future sales growth or FCF generation. In this regard, management made a comment about its agreements with debt holders.

The agreement governing our senior secured revolving credit facility and the indenture governing our senior notes impose limitations on our operations, such as limitations on certain restricted payments, investments, incurrence or repayment of indebtedness, and maintenance of a consolidated net leverage ratio and an interest coverage financial ratio. In addition, the indenture governing our senior notes contains limitations on certain restricted payments, investments and incurrence or repayment of indebtedness. These limitations could impede our ability to respond to market conditions, address unanticipated capital investment needs and/or pursue business opportunities. Source: 10-k

My Conclusion

EnPro is a company that has proven to have a solid business strategy, focused on growing end markets and the development of high-tech products and solutions. Despite the risks and intense competition in all areas of its business, the company has managed to maintain a competitive position, and has continually sought to improve its technologies and processes to meet the changing needs of its customers. I assumed that the sale of some of its businesses and assets may generate future gains, and EnPro will also find new targets at beneficial prices. Besides, I would also expect further interest from investors after they learn about the recent dividend increases and the stock repurchase program. Even considering the risks from the potential failure of M&A, divestitures, or debt, I believe that the stock could be worth more than what the market currently discounts.

For further details see:

EnPro: Successful Divestitures, M&A, And New Stock Repurchase Imply Undervaluation