TFC - Ensemble Capital Management Quarterly Letter Q1 2023

2023-05-03 12:00:00 ET

Summary

- Ensemble Capital Management, LLC is based in Burlingame, California, midway between Silicon Valley and San Francisco. The firm offers customized portfolio management and philanthropic solutions with unparalleled client service.

- The first quarter of 2023 saw continued strong performance across most of our portfolio, but this strength was offset by the decline in our long time portfolio holding First Republic Bank.

- Excluding First Republic, the rest of our portfolio was up approximately 11.5%, or about 4% more than the S&P 500.

- Despite all of the reasonable worries about a recession or high inflation stopping consumers from spending, these worries have remained entirely absent from the global travel industry.

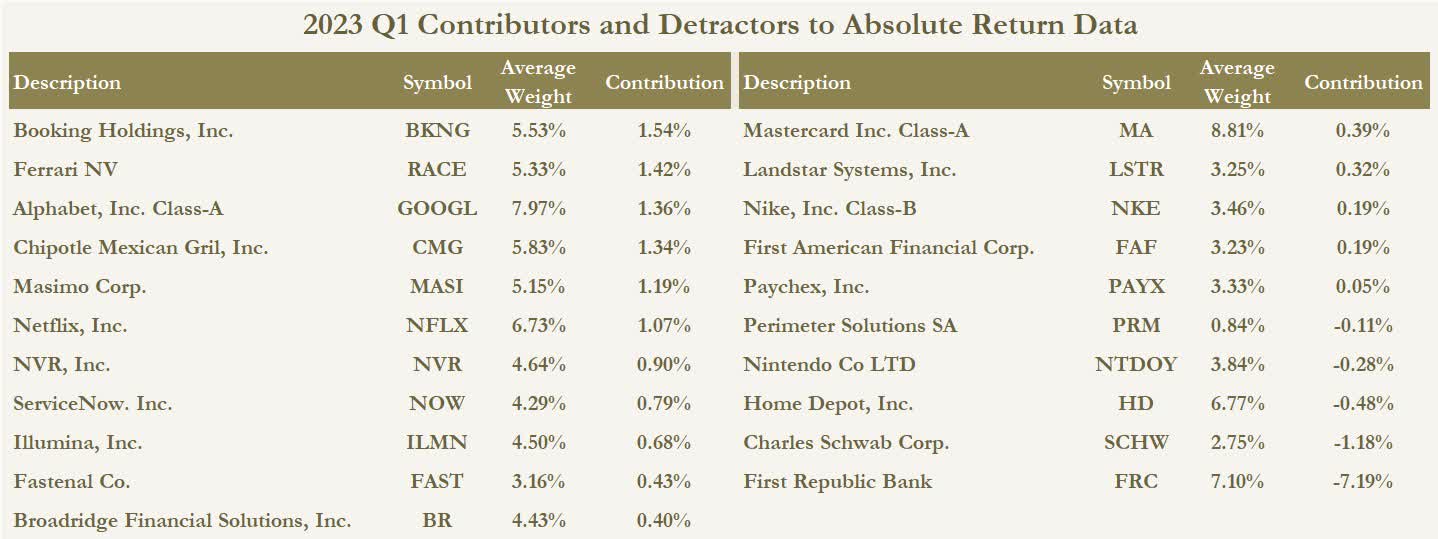

The performance of securities mentioned within this letter refers to how the security performed in the market and does not reflect the performance attributed to the core equity portfolio. Please see the chart at the end of letter, which reflects the full list of contributors and detractors based on each security's weighting within the core equity portfolio.

For a copy of Ensemble Capital's equity strategy performance track record, please email a request to info@ensemblecapital.com .

The first quarter of 2023 saw continued strong performance across most of our portfolio, but this strength was offset by the decline in our long time portfolio holding First Republic Bank ( FRC ). The bank runs triggered by Silicon Valley Bank's failure spread to First Republic causing the stock to fall dramatically. We exited our investment in First Republic as it became clear that the scale of the deposit withdrawals was of a magnitude that makes it very unlikely, in our view, that the bank can remain a standalone entity for more than a short period of time absent a raise of capital that would dramatically dilute current shareholders.

In the first quarter, our equity strategy was up 3.48%, while the S&P 500 was up 7.50%. Excluding First Republic, the rest of our portfolio was up approximately 11.5%, or about 4% more than the S&P 500.

{kind=link}

Past performance is not an indication of future returns.

Please see disclosures on final page. Performance figures with the Ensemble Equity Composite are shown after deducting management fees.

In this quarterly letter, we are going to cover four topics.

- Our investment in First Republic.

- The drivers behind why 12 of our holdings, slightly over half of our total holdings, were up between 10% and 32% this quarter.

- The broader impact of the banking crisis on the economy and financial markets.

- Our outlook for our strategy over the balance of 2023 and into 2024.

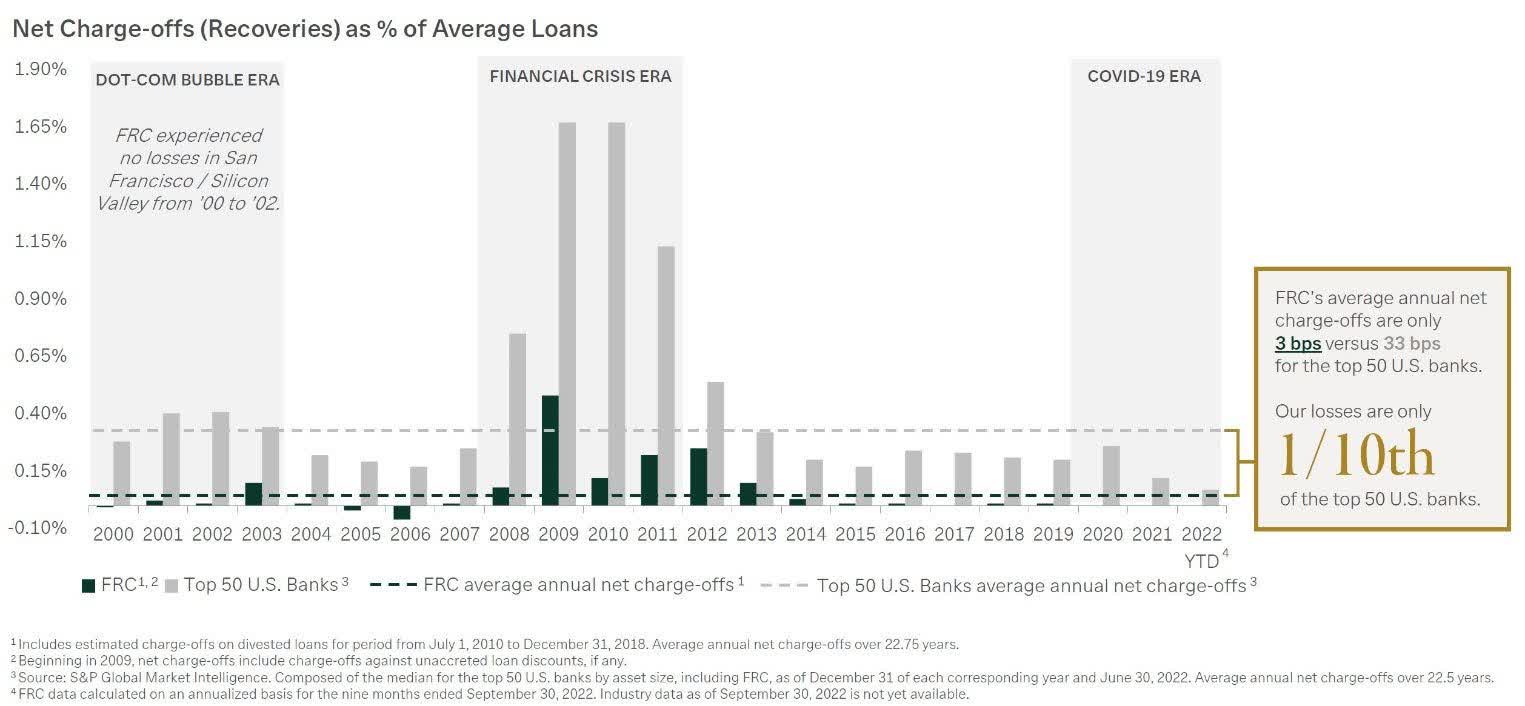

We first invested in First Republic Bank in 2012. In the wreckage of the financial crisis, the bank was notable in the way it had distinguished itself in having written far fewer bad mortgages compared to the top 50 banks.

As the chart below shows, going back 23 years, including the Dot Com bust that roiled the bank's home region in the San Francisco Bay Area and the housing bubble bust of 2008-2012, First Republic experienced credit losses of less than 1/10th of the credit losses experienced by the top 50 banks on average over that time period.

{kind=link}

How did First Republic achieve this? No bank wants to write loans that won't be repaid, so why was First Republic so much better at making sure their borrowers would repay them? First Republic made mortgage loans to high net worth families who had lots of wealth, cash, and high incomes. On average, their borrowers put down 42% of the home purchase amount as a down payment. Less than 1% of the mortgages they offered included a down payment of less than 20%.

Why then did high net worth families choose to borrow from First Republic? If they planned to borrow such a low portion of a home's price, they could easily borrow the money from most any other bank. The answer is customer service. As we've written about many times in the past, First Republic was unique in the industry in providing exceptional levels of customer service. For a high net worth family, time is money, and having a private banking relationship where customer service was top notch drove intense customer loyalty.

Banks make money primarily by taking in customer deposits on which they pay a relatively low interest rate, and then lending that money out at higher interest rates. This function is critical to the economy. Money that is lent to buy houses and finance business investments needs to come from somewhere. That "somewhere" is the cash that other households and businesses hold in checking and savings accounts.

Because the interest rate that banks must pay to depositors and charge to lenders fluctuates over time, the spread between these two rates, known as the net interest margin, can rise and fall. However, in this area too, First Republic has a stable long term history. Importantly, this stable level of net interest margin was even on display in 2006-2007 when the Federal Reserve raised the Federal Funds interest rate to 5.25%. Or even higher than where the Fed Funds rate stands today.

So, what then went wrong? If First Republic didn't take excessive credit risk, what triggered a run on their bank that has destroyed what many people in banking refer to as the "crown jewel" of the industry?

When a customer deposits money into a bank, they want to be sure that even if that money is lent out, that in the event the customer wants to withdraw their cash it is sure to be there. One reason the money may not be there is if the bank has written a bad loan that isn't going to be repaid. This is a risk that First Republic managed to avoid across its history. The other reason is that if interest rates rise significantly, the value of the loans and investment securities that a bank has deployed customer deposits into will fall. But unlike a bad credit where the loss will never be recouped, an interest rate driven decline in the value of a credit good loan or security will be recouped in the years ahead as the value recovers as the loan or security reaches its maturity date.

Because of this important distinction between permanent losses due to credit risk vs the temporary losses resulting from increased interest rates, banking regulators treat these two types of losses very differently. When calculating whether a bank is well capitalized, and thus customers can trust that their money will be there should they want to withdraw their deposits, regulators exclude these temporary losses from consideration. Their rationale for this approach is that the bank has no need to sell these assets and instead can expect to hold them to maturity at which point any lost value will have been fully recouped.

But what if a bank does need to sell assets at a loss? This can happen if depositors pull so much money out of checking and savings accounts that the bank must sell more assets than they ever expected. This is what happened to Silicon Valley Bank ("SVB").

Even before the run on SVB in early March, the bank was already seeing rapid withdrawals of deposits. This was not occurring because of particular worries about the health of SVB, but rather because SVB focused on serving a customer base of cash burning startups, venture capital firms, and technology companies.

In the fourth quarter of 2022, SVB saw deposit outflows of 9% vs the prior year, or down 13% vs their peak levels earlier in 2022. In general, deposits across the banking system do not experience declines. From the 1985 founding of First Republic to the end of 2022, the banking system in aggregate did not see any quarter in which bank deposits were lower than the prior year.

While deposits at SVB were falling rapidly, deposits at First Republic grew by 13% in the fourth quarter and stood at all-time highs. Far from needing to deal with depositors pulling out their money First Republic was seeing one of the best rates of deposit growth of any meaningfully sized bank in the country.

Why was First Republic growing deposits even as SVB was losing deposits and the average bank was seeing no growth? A big part of the reason was First Republic's excellent customer service was leading happy customers to make referrals, which was causing their number of customers to grow at a double digit rate in 2022.

So why then was there a run on First Republic?

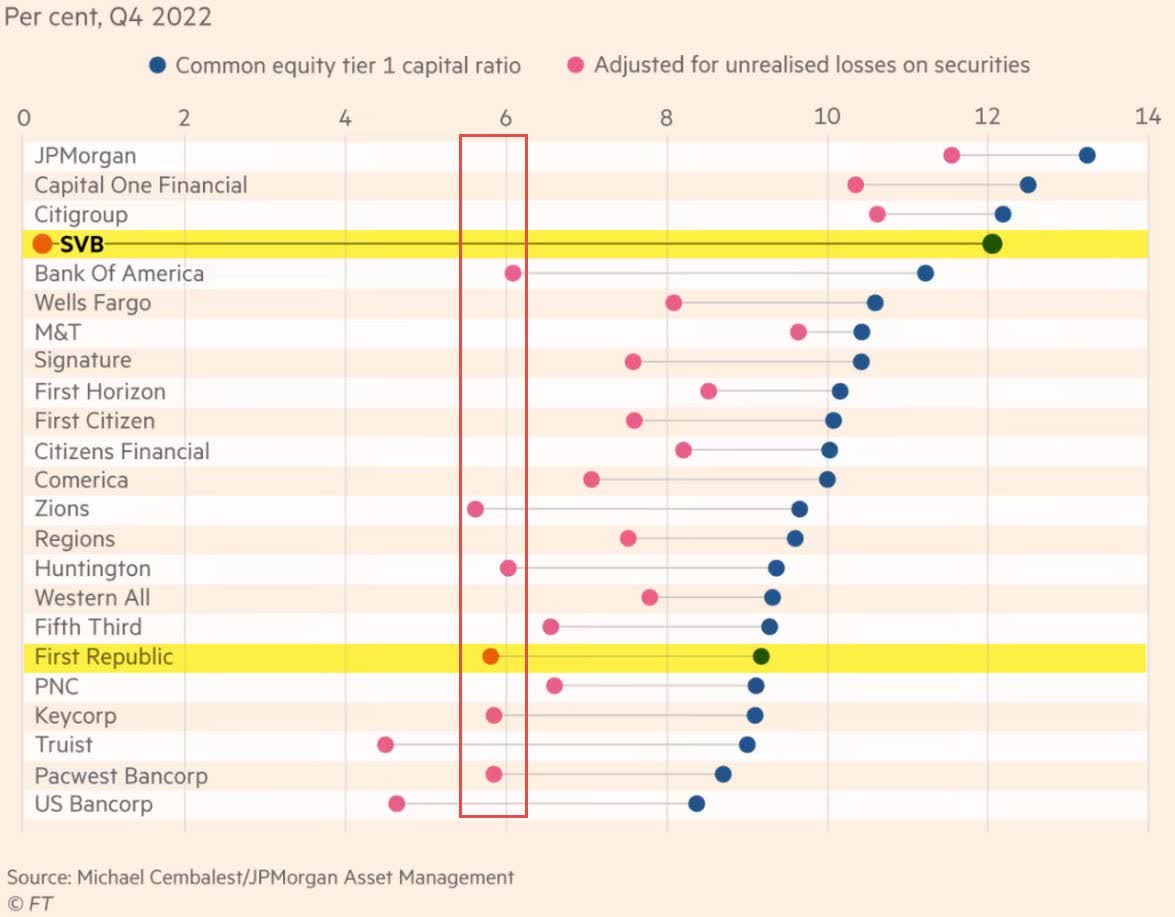

Recall how earlier we discussed the way that regulators ignore declines in the value of bank assets so long as the decline is due to interest rate increases and not credit losses. Under the regulators' definition of a well-capitalized bank, First Republic was well-capitalized. But as deposits began to leave SVB, that bank's investors and depositor began to take note of the large unrealized losses in SVB's investments that were due to the increase in interest rates. They observed that if deposits flowed out of the bank to the extent that all of those unrealized losses were forced to be realized as the bank sold securities to meet withdrawals, that the bank's capital would fall to near zero.

But this was never the case with First Republic. As the chart below shows, if all of the losses on banks' balance sheet securities were realized, their capital would be impaired. But while SVB was an extreme outlier, First Republic would have remained nearly as well capitalized as Bank of America, and similarly or better capitalized as US Bancorp ( USB ), PacWest ( PACW ), Truist ( TFC ), KeyCorp ( KEY ), Huntington ( HBAN ), and Zions ( ZION ), all of whom have avoided a run on their bank.

{kind=link}

But on March 9th, SVB announced they were raising capital from outside investors and said that deposits had continued to flow out of the bank to the extent that as of the end of February, deposits had declined by 17% vs the peak level seen in early 2022.

The announcement sparked the fastest bank run in history. After losing a quarter of their deposits the day of their announcement, the bank faced withdrawal requests of $100 billion the following day, or 80% of their remaining deposits. The FDIC seized the bank mid-morning, rather than waiting until the more typical end of the day, as it became obvious the withdrawal requests could not be met.

Initially, many SVB customers fled into the arms of First Republic. What better place to go when you are fleeing a bank run than a bank with a well-earned reputation for conservative lending, a rapidly growing deposit franchise, and a customer base that loves them?

But bank runs are driven by panic and fear. And it is true that the value of the investments on First Republic's balance sheet had declined, as nearly every bank in the country has experienced. And First Republic is the other large, well known regional bank in the San Francisco Bay Area. While they might not bank startups, and only 4% of their customer base are technology companies, in the midst of a panic, the surface level similarities between First Republic and Silicon Valley Bank were enough to cause customers of First Republic to wonder if maybe their bank had a problem too.

Given our knowledge of First Republic's balance sheet, how different it was from SVB given First Republic's deposit growth vs SVB's deposits already being in decline when the run struck, their access to liquidity via the Federal Home Loan Bank giving them access to liquidity equal to approximately half of their entire deposit base, and the way SVB customers initially fled to First Republic, we initially believed that any contagion from SVB to First Republic would be manageable.

During the turbulent days after SVB's collapse, there was little to no indications of the depth of the run on First Republic. Then on Thursday, March 16, CNBC's David Faber reported that sources said that the level of deposit outflows stood at $25 billion and had moderated. While a decline equal to 14% of deposits would certainly be a problem for any bank, we knew that they had the liquidity to meet that level of withdrawals, and we believed that should the bank be able to survive the run, that many customers would bring their deposits back to the bank once the storm had passed.

Shortly thereafter, many of the biggest banks in the country, in coordination with the nation's top regulators, announced they were depositing $30 billion into First Republic. Given reports that First Republic had lost about $25 billion in deposits, it appeared to us that those deposits had likely fled to the nation's largest banks, who were now redepositing the money at First Republic.

But subsequent reporting emerged the following week that changed our outlook. Despite all the rational reasons why First Republic customers could have felt confident that their deposits at First Republic would be there in the event they tried to withdraw them, on Monday, March 20th multiple media reports stated that First Republic customers had made withdrawals of approximately $70 billion or 40% of First Republic's deposits.

With a deposit hole that large, and the big banks efforts to plug the deposit hole coming up far too short, we concluded that it was highly unlikely that First Republic could survive as a standalone entity unless they received external capital at a level that would dilute existing shareholders dramatically. In the event of a purchase of First Republic, the value received by existing shareholders would likely be minimal. We exited our investment in First Republic at this point.

All businesses face the risk of existential threats arriving quickly. First Republic remained well capitalized as our analysis had expected them to. But we did not forecast that a bank run on a different bank, serving very different customers, and subject to very different trends in deposit growth, would spark a panic among First Republic customers and drive a bank run on them.

Fortunately, the balance of our portfolio had a strong quarter. 12 of the 21 stocks we held during the quarter generated double digit positive returns ranging from up 10% to 32%. All but six of our holdings generated positive returns. In the aggregate, our portfolio excluding First Republic was up approximately 11.5% while the S&P 500 was up 7.5%.

This is an acceleration of the outperformance we achieved in the 3rd and 4th quarter of last year, but of course it excludes the negative impact of First Republic. It is total returns, not returns excluding a poorly performing investment, that our clients actually earn. But in thinking about our portfolio's underperformance from the fourth quarter of 2021 through the second quarter of 2022, followed by our relative outperformance vs the S&P 500 of 3.93% during the second half of 2022, we believe it is worth noting that our broader portfolio, excluding First Republic, saw this outperformance accelerate in the first quarter of 2023.

We have made the contention, since our underperformance first became significant in March of 2022, that it was a panic over stagflation risk that was driving our performance weakness. As inflation faded to some extent in the second half of 2022, and real economic growth remained robust, undermining stagflationary fears, our strategy began to outperform notably. During the first quarter of 2023, real economic growth has remained robust, and while inflation has not faded as much as it appeared it might, both year over year headline and core CPI measured inflation still declined during each month of the quarter.

While the run on First Republic led to sharp underperformance for our strategy, the balance of our portfolio continues to rebound on both an absolute and relative basis as we expected it would as stagflationary fears began to subside.

Some comments on the stocks driving our strong performance excluding First Republic.

Booking Holdings (BKNG) (+31.61%): Despite all of the reasonable worries about a recession or high inflation stopping consumers from spending, these worries have remained entirely absent from the global travel industry. In February, Booking, the largest global online travel agency, reported 39% growth in the number of hotel room nights booked despite large increases in the average price of hotel rooms. The company said that demand accelerated in January. The company has been busily buying back shares, causing total shares outstanding to drop by 8% over the course of 2022. The company guided to continued double digit growth in 2023 and announced a new buyback plan equal to 24% of the company's market capitalization.

Ferrari ( RACE ) (+26.48%): The luxury automaker's long awaited Purosangue, their first four door, four seater vehicle, has proven so popular that the company announced that they have ceased accepting new orders as they are sold out through all of this year and into 2024. The Purosangue is designed not as copycat sports utility vehicle that many other luxury automakers sell, but as a true Ferrari car that their devoted fan base can use for more practical transportation needs. Since the average Ferrari is only driven a few thousand miles a year or less, they are best understood as mechanical works of art rather than a means of transportation. But with the introduction of the Purosangue, Ferrari enthusiasts will have a vehicle that meets transportation needs, while still delivering the extremely high end experience that you would expect from a car that costs about $500,000.

Masimo (MASI) (+24.73%): While Masimo's acquisition of Sound United in February of 2022 caused the stock to drop dramatically and was one of the catalysts of our underperformance last year, since the day the stock dropped on the deal it has subsequently been the best performing stock in our portfolio, outperforming the S&P 500 by 31%. In February, the company raised their guidance for the year as they announced a price increase on their core pulse oximetry products that are so mission critical for hospitals. In response to pressure from an activist investor and shareholders more generally, the company also made changes to some of their governance practices and will expand the size of their board to include new, independent board members.

Chipotle (CMG) (+23.12%): The company continues to attract loyal customers to their all natural, fresh food alternative to the highly processes, junk food sold by most fast food companies. Despite needing to raise prices by double digit rates to offset inflation in food prices and higher labor costs, the company has seen resilient customer demand. While digital orders have fallen from peak COVID levels, digital sales stabilized in the fourth quarter at approximately 40% of all orders or twice the volume seen pre-COVID. The company has remained busy opening new locations with a focus on those that can support a Chipotlane, the company's drive through concept that leverages customers' ability to order ahead on their phones to make pick up times very short. Today, 18% of all locations have a Chipotlane pick up option compared to just 3% pre-COVID.

NVR (NVR) (+20.80%): Despite the large decline in home sales, a decline in home prices, and mortgage rates that are still twice as high as the lows of 2021, NVR's stock is trading at its all-time high other than a brief period from December 2021 to January 2022. Our investment thesis on housing related stocks has been that the very low levels of new home building between the great financial crisis and COVID created a significant shortage of single family housing. While NVR, like all home builders, are seeing the impact of higher mortgage rates on their business, the inventory of existing homes on the market today stands at record low levels. The lack of existing homes available for sale, something we think will persist due to existing homeowners having locked in low mortgage rates and so not being interested in moving unless they have to, means that the home buyers who do want to buy a home will need to turn more frequently to the new home market.

Google ( GOOG ) ( GOOGL ) (+17.57%): Prior to the bank runs, we had planned for this letter to include an extended discussion of ChatGPT, the new artificial intelligence ((AI)) features available in Microsoft's Bing search engine, and the threats and opportunities to Google of AI powered chatbots. We will revisit an in-depth discussion of this topic in a future letter, but we do want to comment on it briefly here.

If you step back and think about what is happening with AI, two things are clear. First, AI is not new. All sorts of services you use today are powered by AI. This is particularly true of Google's existing services. In fact, Sundar Pichai's first speech after assuming the role of CEO was about how the age of AI was arriving and why Google was an "A.I.-first" company. But with ChatGPT, OpenAI has absolutely launched an amazing tool in allowing everyday people to use natural language chat to interface with a highly advanced AI system.

Usually when a new technology launches, people instantly try to label it using an analogy to an older technology. This is why cars were initially referred to as "horseless carriages," and it is why so many people are thinking about AI powered chatbots as a new form of Search. But AI is about much, much more than Search and when it is used for Search-like needs, it often changes the way that people go about meeting those needs. And of course, Google has already launched their own version of this technology, validating the idea that they are not behind so much as have been taking a prudent, risk adverse approach to rolling out this technology. Meanwhile, Microsoft and OpenAI have chosen to release technology that they ended up needing to roll back just weeks later as its behavior was erratic and downright creepy. But there is no putting the genie back in bottle. AI powered chatbots are not going away. We think Google is very well positioned to thrive during the era of AI and we'll have more to say about this later.

So where do we go from here? First, we'll address the broad implications of the banking crisis, and then we'll conclude with some comments on our outlook for our investment strategy.

As painful as the bank runs were for our portfolio's performance this past quarter, at an economy wide level it is not yet clear what the impact will be. Over the year prior to the collapse of SVB, the Federal Reserve had raised interest rates from zero to 4.75%. While this action had a significant impact on debt focused industries like housing, the broader economy has powered through. Over that year, the US economy added 4.3 million new jobs, the largest one year increase in jobs in American history prior to COVID. Very strong job growth continued in the first quarter to the extent that the Federal Reserve continues to be worried not that the economy is slowing, but that employment demand is too strong and inflationary wage increases will continue.

While rising interest rates may not be slowing the US economy as much as the Federal Reserve would like, a banking crisis may do their job for them. While higher interest rates decrease households' and businesses' demand for borrowing, worries about bank runs will chill many banks' willingness to lend. The regional banks at the center of the banking crisis are smaller than the big Wall Street banks, but collectively they are major lenders to businesses.

While the Federal Reserve chose to raise the Federal Funds interest rate once again even after the failure of SVB, they indicated that they will likely only raise rates one more time in May.

High interest rates themselves do not slow the economy. Rather, higher interest rates are one input to tighter financial conditions, and it is tight financial conditions, conditions under which households and businesses are less able to gain easy access to capital, that slow inflation and economic growth.

The reduction in banks' willingness to lend that appears to be a very likely outcome of the bank run issues that have yet to be resolved, would act as a separate driver of tighter financial conditions. How likely this is and how large the magnitude of the impact is not clear, but many economists suggest that the impact of tighter willingness to lend is equivalent to the Fed hiking interest rates between 0.25% and 0.75%. If this is correct, then it means all else equal the Fed can stop raising rates sooner, and at a lower peak rate, than if the banking crisis had never happened.

That being said, if the impact of the bank runs does not slow the economy, the Fed may need to continue rate hikes. Or if the impact is instead very large, the US economy may tip into recession. Macroeconomic conditions are part of a complex dynamic system that is extraordinarily difficult to forecast.

As for our portfolio, its relative performance rebound in the second half of 2022 was strong, and excluding First Republic, which is no longer part of our portfolio, this relative performance recovery accelerated in the first quarter. As we have said consistently, our strategy has performed well during periods featuring recessions or recession worries, as well as periods when inflation was elevated. But stagflationary conditions, those that combine high inflation and weak or negative real growth, reduce the value of businesses that relentlessly invest in building a better, more profitable future.

With inflation having declined considerably from its highs, even while the unemployment rate has also declined over the last year, it is clear that at least some of the inflation pressures has faded without the need for a recession. The idea that we might suffer from a decade of high inflation and weak growth, as was experienced in the 1970s, is fading dramatically as a possibility. With goods inflation mitigated, home prices declining, rents growing slowly or not at all, the remaining inflation is mostly due to wage pressures in some sectors of the economy.

Given this, it is very difficult to see how inflation could persist in a recessionary environment where employment demand fell far enough to push up the unemployment rate. And so, while elevated inflation or a recession is still a very real risk, the stagflationary worries that gave rise to our performance struggles in the first part of 2022 no longer seem to be a likely outcome.

We believe this is why our strategy performed so strongly in the second half of 2022 and saw accelerating outperformance, excluding First Republic, in the most recent quarter.

To be blunt, the failure of our investment in First Republic was an emotionally painful experience for our team. We had followed the company closely for over a decade and deeply admired the way the bank was able

to deliver high end customer service despite the banking industry historically being one of the least client friendly industries.

With the benefit of hindsight, we would have preserved client capital if we had sold First Republic at the first sign of trouble at Silicon Valley Bank. However, we believe that selling at the first sign of trouble would be a terrible lesson for us to learn from this experience. By and large, our most successful long term investments have all gone through difficult periods. To have sold them at the first signs of trouble would have deprived us and our clients of long term gains.

A recent example of this was when Masimo made their acquisition of Sound United. This large, unexpected acquisition was extremely concerning to us. However, we also believed that the market was wildly overreacting, and we put in the work to understand what the company was doing. It would have been an emotional relief to have sold Masimo right away. But I'm very glad we didn't sell given the stock subsequently has been the best performing stock in our portfolio since then, outperforming the S&P 500 by 31%.

Or consider Google, which has recently been the focus of investor fears related to ChatGPT and AI more generally. And yet by taking our time to understand what is going on and thinking long term, we were able to enjoy the stock's strong performance in the first quarter. Shooting first and asking questions later is not an effective way to invest. And yet, from time to time, with the benefit of hindsight, this sort of behavior can work out well.

Not every set of difficulties can be overcome. While we initially believed that First Republic would avoid a run that was deep enough to threaten their viability, once we determined that this indeed had happened, we sold out of the position. We never hold an investment based on hope, we only ever hold through difficult times because we have an informed opinion that the company will emerge on the other side and continue to be an outstanding business.

Like all investors, we have experienced past periods of significant underperformance prior to our current period. Subsequent to each of those periods we have generated outperformance that rebuilt our long term track record. We expect that this dynamic will play out again in the years ahead.

We are going to be at this work for many, many years to come. We have deep conviction in the philosophy and approach we have spent two decades developing and fine tuning. We have experience working through periods of difficult performance, and all manner of economic environments. We are confident that our approach and timeless philosophy of investing in some of the highest quality businesses operating today will yield the strong results we expect it to in the years ahead.

As damaging as the fall of First Republic was to our relative returns, we note that our diversified portfolio still delivered 3.5% in gains on the quarter. When a large investment performs poorly in our portfolio, it is natural for clients to wonder if we should hold more stocks in smaller size to control risk. However, a focused portfolio is one of the critical elements that drive superior performance. In the most recent quarter, the significant gains from our large investments in stocks such as Google and Ferrari were critical to helping offset the decline in First Republic.

We know that periods of performance difficulties are trying for our clients. And the events surrounding First Republic are a clear disappointment. We also deeply appreciate the large cohort of our long time clients who have invested with us for so many years. Our 99%+ annual client retention rate is a key reason why we are able to pursue a long term approach. Managers whose clients are short term in nature end up being forced to be short term investors whether they think that is best or not. But that is not the case at Ensemble.

The years ahead will likely be bumpy. The geopolitical framework of the past decades is in flux. COVID will leave a lasting mark on how society and businesses operate. New technologies, such as artificial intelligence, will give rise to new businesses and destroy others.

But none of this is new. This is the nature of human society, the nature of economics. Creative destruction, and the new forms of value it gives rise to, has always been at the heart of business and investing.

We look to the future not with apprehension, but with a keen awareness of the ever changing world in which all of us live, the risks and opportunities that arise from these changes, and a deep sense of responsibility to be good stewards of our clients' capital.

Disclosures

{kind=link}

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. It should not be assumed that the recommendations made in the future will be profitable or will equal the performance of the securities listed above. The performance information shown above has been calculated using a representative client account managed by the firm in our core equity strategy and represents the securities held for the quarter ended 3/31/2023. Information on the methodology used to calculate the performance information is available upon request. The performance shown in this chart will not equal Ensemble's composite performance due to, among other things, the deduction of fees and expenses from the composite performance and the timing of transactions in Ensemble's clients' accounts.

Additional Important Disclosures

Ensemble Capital is an SEC registered investment adviser; however, this does not imply any level of skill or training and no inference of such should be made. The opinions expressed herein are as of the date of publication and are provided for informational purposes only. Content will not be updated after publication and should not be considered current after the publication date. We provide historical content for transparency purposes only. All opinions are subject to change without notice and due to changes in the market or economic conditions may not necessarily come to pass. Nothing contained herein should be construed as a comprehensive statement of the matters discussed, considered investment, financial, legal, or tax advice, or a recommendation to buy or sell any securities, and no investment decision should be made based solely on any information provided herein. Ensemble Capital does not become a fiduciary to any reader or other person or entity by the person's use of or access to the material. The reader assumes the responsibility of evaluating the merits and risks associated with the use of any information or other content and for any decisions based on such content.

Ensemble's Equity strategy is intended to maximize the long-term value of the underlying accounts. The strategy generally invests in U.S. common stocks, but from time to time the underlying accounts may hold cash and/or fixed income investments in an attempt to maximize capital gains. The strategy holds mostly large and medium-capitalization stocks, although accounts may also hold small-capitalization stocks.

Performance results for the Ensemble Equity composite since the composite's inception on December 31, 2003, are unaudited and are subject to change. The Ensemble Equity composite includes realized and unrealized gains and losses, the reinvestment of dividends and other earnings, and is net of management fees, brokerage transaction costs and other expenses. Taxes have not been deducted. Net of fee performance was calculated using actual management fees. Management fees for an Ensemble Equity account range from 1.00% to 0.50% on an annual basis and are typically deducted quarterly. Fees are negotiable, and not all accounts included in the composite are charged the same rate. Results are based on fee paying, fully discretionary, unconstrained accounts managed with an Ensemble Equity objective and include those Ensemble Equity accounts no longer with the firm. Accounts must exceed $500,000 to be included in the composite. Accounts with assets below $500,000 and accounts with objectives other than Ensemble Equity are excluded.

Unless otherwise stated, returns for periods exceeding 1 year are annualized.

The comparative benchmark is the Standard and Poor's Total Return Index of 500 Stocks ("S&P 500"), an index of 500 large capitalization equities, generally considered a comprehensive indicator of market performance. The S&P 500 Total Return Index includes realized and unrealized gains and losses, the reinvestment of dividends and other earnings and is not subject to fees and expenses. It is not possible to invest directly in an index. The holdings in the Ensemble Equity strategy may differ significantly from the securities that comprise the benchmark.

All investments in securities carry risks, including the risk of losing one's entire investment. Investing in stocks, bonds, exchange traded funds, mutual funds, and money market funds involve risk of loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable or suitable for a particular investor's financial situation or risk tolerance. Some securities rely on leverage which accentuates gains & losses. Foreign investing involves greater volatility and political, economic and currency risks and differences in accounting methods. Future investments will be made under different economic and market conditions than those that prevailed during past periods. Past performance of an individual security is no guarantee of future results. Past performance of Ensemble Capital client investment accounts is no guarantee of future results. In addition, there is no guarantee that the investment objectives of Ensemble Capital's equity strategy will be met. Asset allocation and portfolio diversification cannot ensure or guarantee better performance and cannot eliminate the risk of investment losses.

As a result of client-specific circumstances, individual clients may hold positions that are not part of Ensemble Capital's equity strategy. Ensemble is a fully discretionary adviser and may exit a portfolio position at any time without notice, in its own discretion. Ensemble Capital employees and related persons may hold positions or other interests in the securities mentioned herein. Employees and related persons trade for their own accounts on the basis of their personal investment goals and financial circumstances.

Some of the information provided herein has been obtained from third party sources that we believe to be reliable, but it is not guaranteed. This content may contain forward-looking statements using terminology such as "may", "will", "expect", "intend", "anticipate", "estimate", "believe", "continue", "potential" or other similar terms. Although we make such statements based on assumptions that we believe to be reasonable, there can be no assurance that actual results will not differ materially from those expressed in the forward-looking statements. Such statements involve risks, uncertainties and assumptions and should not be construed as any kind of guarantee. Readers are cautioned not to put undue reliance on forward-looking statements.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Ensemble Capital Management Quarterly Letter Q1 2023