ENSG - Ensign Group: Compounding Earnings At 27% Is It Worth It?

2023-04-27 10:14:53 ET

Summary

- The market continues rewarding ENSG with higher multiples, now paying 21x forward earnings.

- Taking a deeper look at the business economics, it becomes clear why.

- It continues to compound revenue and earnings at double-digit rates.

- Reiterate buy.

Investment summary

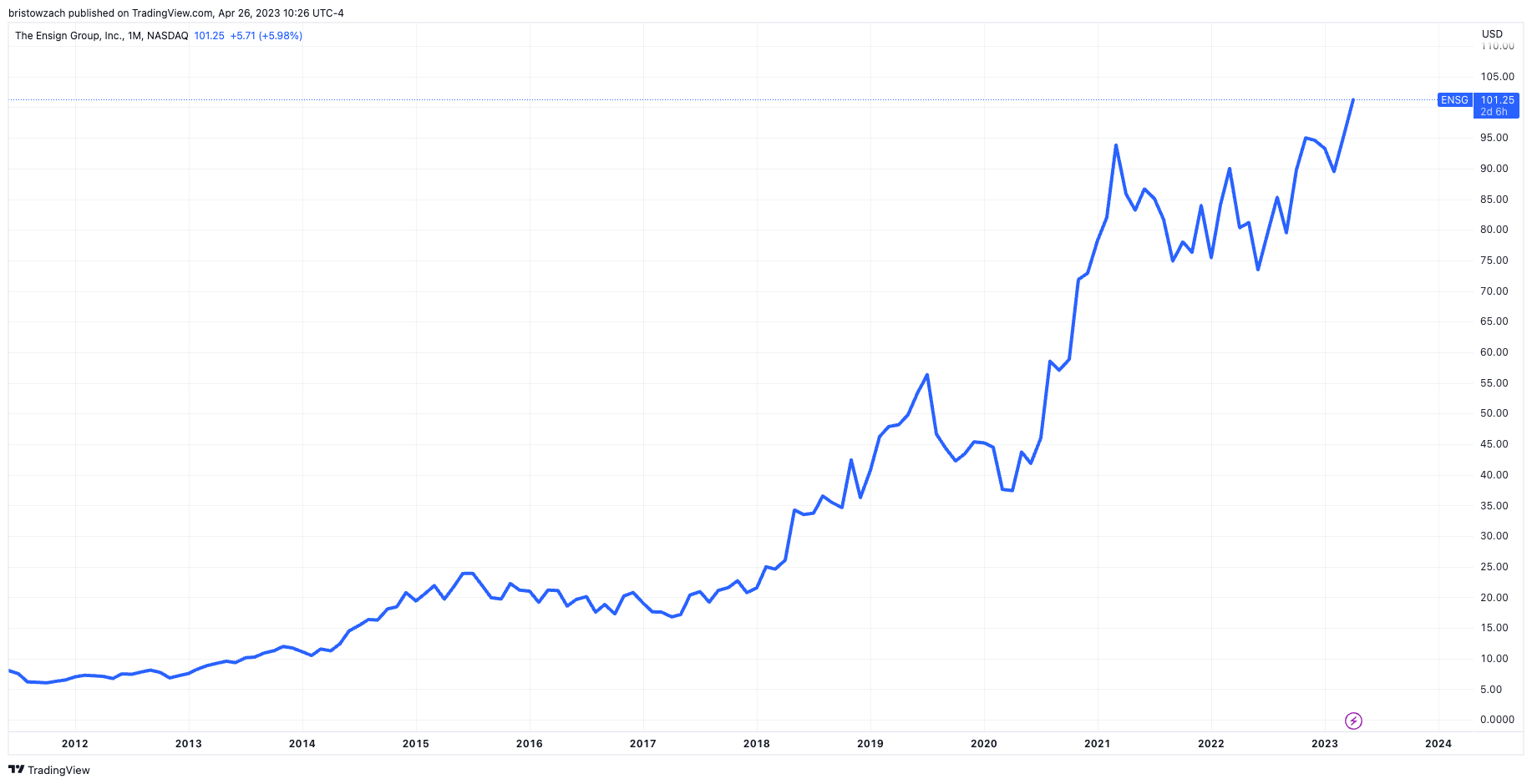

It's not often you get a long-term compounder that is able to withstand the bulk of market extremes. In buying The Ensign Group, Inc. (ENSG) at any point since FY'18, you would have done well. Now the stock has again lifted off a low in April and that is more reason to believe the market is agreeing that ENSG is "top of the mantelpiece in service-based healthcare" , as was mentioned on ENSG back in August last year. Since then, it has rallied 18%, in-line with the S&P 500's return. It has now taken out the $100 price target, and with the latest earnings data, there's plenty of reason to think this could continue.

The market is paying $21.70 per $1 of earnings for ENSG, a clear sign of the expectation of bottom-line growth. It would not surprise me to see the company do $3.4Bn in turnover this year on $4.65 in per-share earnings, or 13% growth. This could be very attractive to the market. Net-net, there is still value in this long-term compounder, and it looks attractive all the way to $130. Reiterate buy.

Fig. 1 - ENSG price evolution = long-term compounder

{kind=link}

Revenue, earnings growth a key driver

It's important to consider a few points that underline my thesis here.

One, ENSG primarily books its revenue from Medicare and Medicaid, along with managed care and commercial insurance customers. Skilled nursing is the company's major revenue driver, given the commingling with Medicare and Medicaid. Another point, is that 82% of its Medicaid revenue comes from 5 states (Arizona, California, Texas, Utah, Colorado). As a potential tailwind, the California program expects its budget to increase to $38Bn by FY'26-27.

Fig. 2 Payor by Type

Data: ENSG 10-K

In addition, it's important to talk about how the company's grown tremendously over the last few years, and looks to going ahead. It has recycled capital to buying 223 facilities over the last 10-years. For the firm's efforts, it has added:

- 18,443 skilled nursing beds, and

- 5,000 senior living units under its banner of operations.

It is reasonable to expect these trends could continue. Using the earning growth over the same 10-year time frame, it has definitely created value. The earnings-per store has increased to $1mm from $0.11mm on a same-store basis. That's certainly a nice compounding rate going forward too. The number of skilled operational and senior living operations has lifted from 103 in FY'19 to 231 last count. That's good growth in the core operating assets. The operational skilled nursing beds have been most cumulative, however - 19,615 in FY'18, hitting 28,130 by the end of last year [Figure 3]. The growth curve is worth mentioning, and can be seen below.

Fig. 3

Data: Author, ENSG 10-K's

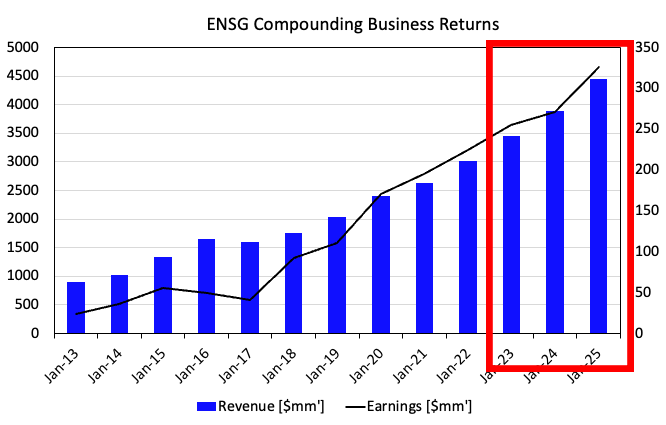

Two, it clipped $3Bn in revenue last year, 15% YoY growth, adding to a long line of revenue upside from the last 10-years. For starters, top-line growth is so important in these murky times to distinguish the more quality companies, in my opinion. The 15% growth comes at a time when many competing investments have dropped revenues 5-10%. Further, who doesn't want to buy companies growing at such attractive rates? Consider these basic facts:

- That ENSG has grown annual revenues from $1.6Bn in FY'17 to $3.02Bn last year, 11% CAGR. I believe these rates can continue, and project 14% YoY growth in turnover this year, 18% gross margin.

- The firm has beaten earnings consensus estimates 100% of the time in the last 2 years.

- Even more impressive, is the earnings leverage ENSG has delivered over the same time frame. With revenues compounding 11% per year, earnings have compounded at 27%, tremendous leverage of 2.4x. This tells me ENSG is able to convert revenues to earnings growth, which I am projecting to continue.

With this kind of impressive record, it is no wonder the market is paying 22x forward earnings, about right to get in for this growth. It certainly isn't a discount, that's for sure.

Fig. 4

{kind=link}

Three, to maintain this ramp, cash flow will be paramount. The company had a $270mm run rate for operating cash flow and this is on a $160-170mm CapEx. Management expects further capital investments into the physical plants. This can be expensive, but the returns are showing for themselves. Further, acquisitions are management's preferred way of growth. In that vein, the balance sheet remains strong - $1.2Bn of equity holding up $3.4Bn of assets, ex-leases this is $2.6Bn of equity on this amount. Further, it has $316mm in cash and further liquidity available.

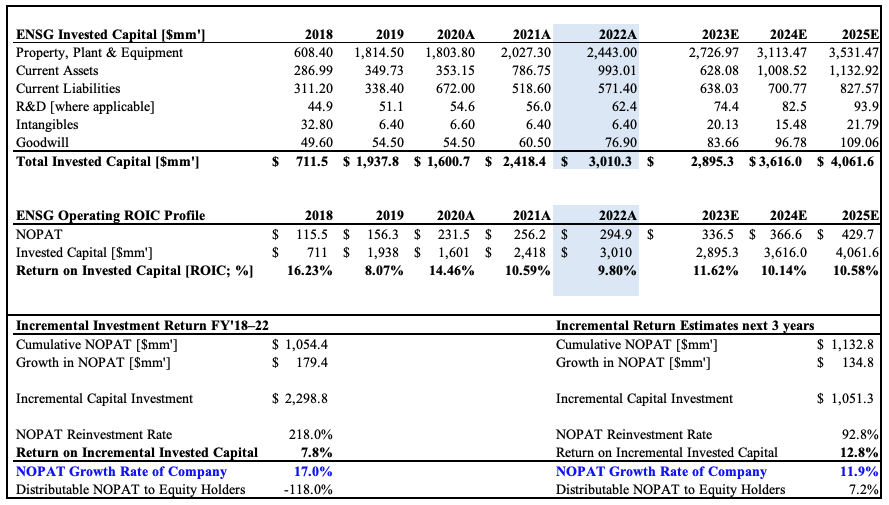

You can see the performance over the company's capital budgeting below. Looking at FY'18-'22:

- Returns on incremental and existing capital were quite impressive, ranging from 9-16% annually, 7% on the incremental growth.

- It invested $2.3Bn to generate $1Bn in total NOPAT and additional $179mm in NOPAT growth.

- Given these actions, the company's valuation increased 17% YoY over this time frame.

Going forward my estimates are for this kind of trend to continue, and project another $1Bn capital investment at least over the next 3 years, where the firm can grow NOPAT $130mm to $430mm, curling up to ~10% post-tax margin. This tells me the projected valuation growth of 12% per year into FY'25 could be driven by profitability, even with capital turnover at 1x [Figure 6].

Fig. 5

{kind=link}

Fig. 6

Data: Author, ENSG 10-K's

It is important to put this into context. By investing in ENSG, we want to be buying a business that can generate a return on its own investments above the market's return. We can get dividends and buybacks. But if the firm retains the earnings, we'd expect it to invest the capital at a rate of return better than what we can obtain elsewhere.

This is a major strength of ENSG, and demonstrates to me why this is such a good company, and why investors are paying $22 for every $1 of the company's earnings. The persistently high returns on capital just exhibit the productivity of that capital that's not returned to shareholders. Instead, they have been rewarded with capital gains on their position. Not to mention, 20% trailing ROE is one that's crept up from 17% in FY'18, illustrating the value created. Speaking of this, the economic profit is where the most value is seen, in my estimation. You can see the company's return on incremental capital above the hurdle rate below.

Two observations:

- The return on capital has rolled lower in recent years, and could head sideways again.

- What hasn't changed is the spread of investment return above the hurdle rate, which explains the long-term performance in my opinion.

What's really important is that when combining the points discussed here the thesis rounds out. One, the revenue sources from Medicare and Medicaid, and growth of these particularly in California. Two, the tremendous top-bottom line growth ENSG exhibits yearly, which could certainly continue if my numbers are correct. Three, the returns on incremental capital above the hurdle rate, paving the way to create value for shareholders. That's a fairly concise view of it all.

Fig. 7

Data: Author, ENSG 10-K's

Valuation and conclusion

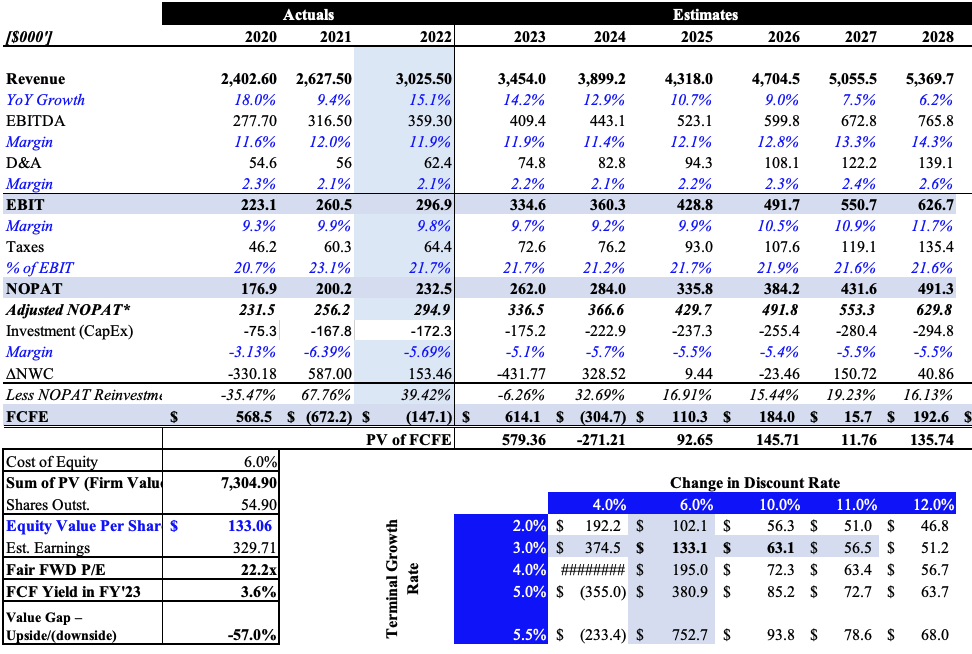

As mentioned the market is paying a premium for ENSG. At $21 for every $1 of earnings (P/E of 21x), that's more than 7% above the sector. I don't believe you'd be left behind if you paid this, however.

The business economics are quite attractive. In particular, how profitable ENSG has become, and there's plenty left in the tank to keep this going. At 21x my FY'23 estimates this values ENSG at $130. I believe the firm could throw off $614mm in cash this year, and will reinvest this back into future growth measures. I could see the firm rated fairly at $130, based on growth multiples and DCF below.

Fig. 8

{kind=link}

In conclusion, there is substantial evidence to suggest ENSG can be a long-term buy. This is a name with strong business economics where it can invest loads of capital at high rates of return. You can be sure this kind of return will at least match, if not outpace the market. Just look at the returns to date. This is a firm committed to capital productivity and growing owner cash flows. It said there are literally countless opportunities for investment out there on the earnings call, and this will likely be a growth point going ahead. That, and it just keeps on compounding earnings and growth capital, which might be worth paying a good price for. I do see value in the name up to $130. Rate buy.

For further details see:

Ensign Group: Compounding Earnings At 27%, Is It Worth It?