ENSG - Ensign Group: Occupancy Rates Normalizing To Pre-Covid Range

Summary

- The Ensign Group posted its Q4 and FY22 accounts with earnings in-line and outsized result at the top-line.

- Occupancy rates are normalizing toward pre-pandemic range and net leverage was clipped to ~2x.

- Management guide double digit growth estimates in FY23E'.

- Net-net, reiterate buy.

Investment Summary

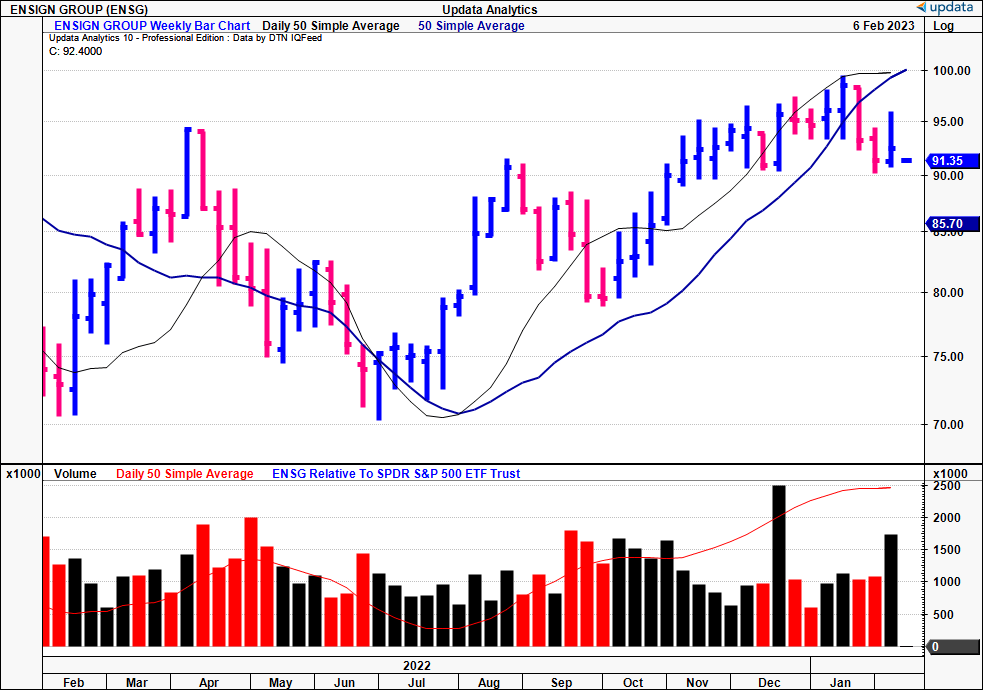

Since our last publication on The Ensign Group, Inc. ( ENSG ) we've noted its rally from October FY22' lows has begun to lose steam and shares have congested sideways into the new year. Since the original thesis, ENSG has climbed c.8.5% to the time of writing.

{kind=link}

Following the company's FY22' full-year numbers last week we believe there's scope for the stock to rate higher once again, given a solid deleveraging of its portfolio to ~2x and forward guidance of ~13% YoY growth at the top-line. Net-net, we reiterate ENSG as a long-term buy and believe the company is still attractively priced trading at ~20x forward earnings.

ENSG price evolution across FY22–date

{kind=link}

ENSG FY22' growth resilient in face of weaker macroeconomic climate

A key standout from ENSG's FY22' numbers was the sequential growth in the aggregate occupancy rate, now seeing growth for 8 consecutive quarters. This pulled through to a YoY 430bps YoY increase same-store transitional operations. In fact, the same-store occupancy rate continued to track towards pre-pandemic ranges of 80.1% [March FY20'], reaching 77.8% by the year end. We'd note management confirmed acquisitions of 17 operations and 37 affiliated operations from July FY22'–February 1st.

Switching to the full-year numbers, there were several data points worth mentioning. Our main takeaway's include the following:

- ENSG recorded a noteworthy increase in consolidated and adjusted revenues, which reached $3.025 billion, a YoY growth of 15.1% . It pulled this down to earnings of $224.7 million, demonstrating a 15.4% YoY rise, while it reported non-GAAP earnings of $235.7 million [a 13.8% increment].

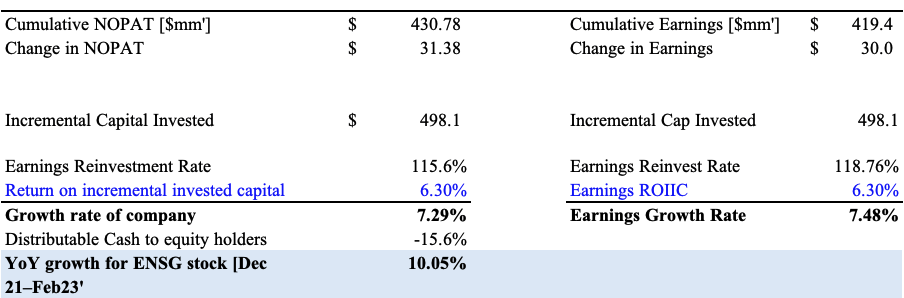

- It also generated a cumulative $430mm in NOPAT, on an additional YoY growth of $31.4mm in NOPAT. It achieved this with an additional $498mm net capital investment, incurring a return on incremental invested capital of 6.3% over the period [Exhibit 1]. This was behind the FY22' annual ROIC of 8.7%, demonstrating the tail of profitability on its legacy portfolio continues to create value, and is above the hurdle rate.

- With respect to Standard Bearer, we noted it generated rental revenues of $19.4 million for the quarter, of which $15.6 million was derived from the Ensign affiliated operations . As a reminder, each property is subjected to triple-net long-term leases, and is comprised of 103 properties, owned by ENSG. Of this total,75 are leased to affiliated skilled nursing and senior living operations, and the remainder, 29 senior living operations, are leased to the Pennant Group ( PNTG ). Furthermore, Standard Bearer generated $13 million in FFO on an EBITDA-to-rent coverage ratio of 2.4x.

- ENSG also continues deleveraging is balance sheet and it ended the year on a [lease-adjusted] net debt-to-EBITDAR ratio of 1.98x, a decrease of ~2.1x from the previous year. It also reported the possession of 108 assets, 84 of these being unlevered, that increased in equity value and can provide additional liquidity.

- Given the heavy reinvestment over the period, we were pleased to see the company delivering a $54mm levered free cash inflow with the positive ROIC/WACC spread . It also repaid ~$4mm in net debt with a slight YoY pullback in CFFO to $272mm.

- It's also worth noting the company increased its Q4 cash dividend to $0.053 per share. As a result, this marks ENSG's 20th consecutive annual dividend increase.

- As a result of the growth trajectory in FY22' ENSG guided for a ~13% YoY growth in revenue for FY23E', calling for $3.63Bn at the top-line [upper end of range] . It hope to pull this down to an earnings range of $4.60–$4.74 per diluted share.

Exhibit 1. FY21–22' NOPAT growth, incremental ROIC [including dividend payout]

{kind=link}

Valuation and conclusion

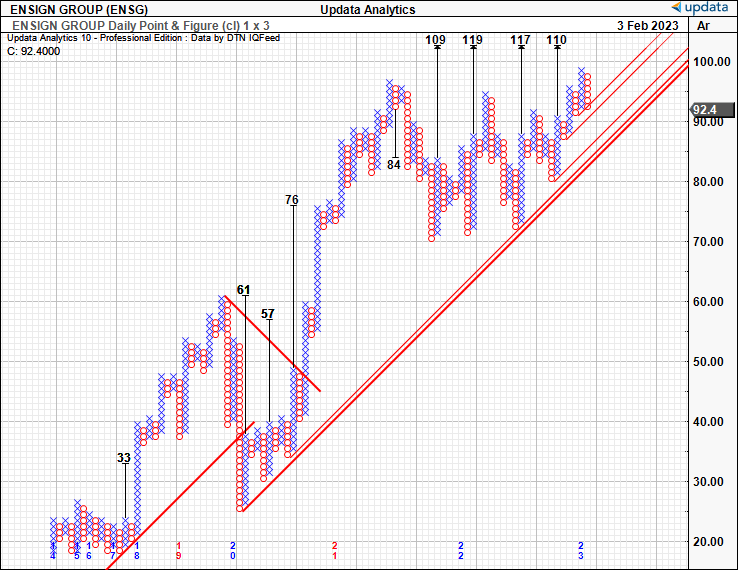

ENSG stock trades at 20x forward P/E and hence at a ~6/5% discount to the sector. It's trading at a substantial premium of 4x book value which could demonstrate the value management have added to date. Nevertheless, taking management's estimates $4.60 in diluted EPS for FY23E' on face value, the stock appears to be fairly priced at ~$92–$93. Adding the dividend stream and growth prospects we reiterate our $100 base case target outlined in the previous analysis. We also have upside targets on our point and figure studies to $110, adding additional weight to our thesis.

Exhibit 2. Upside targets to $110

{kind=link}

Net-net, we reiterate ENSG as a buy following its FY22' numbers. Growth was strong in the face of the macro-climate, and occupancy rates are tracking back toward pre-pandemic levels. We noted the tail of its asset returns continues to generate value and the company is well capitalized to continue funding its growth initiatives. We are seeking our original target of $100, and are eyeing additional upsides to $110.

For further details see:

Ensign Group: Occupancy Rates Normalizing To Pre-Covid Range