ENSG - Ensign Group: Unit Economics Ratcheting Back To Pre-Pandemic Highs

2023-07-18 04:02:25 ET

Summary

- Ensign Group is a long-term investment with potential for growth, operating in the skilled services segment and owning healthcare REIT, Standard Bearer.

- ENSG has seen earnings compound at 2.4x that of sales over the last 5-6 years, beating EPS estimates every quarter since 2018, and this is primed to continue moving forward.

- Valuations making sense at 19x forward in my eyes, reiterate buy.

Investment briefing

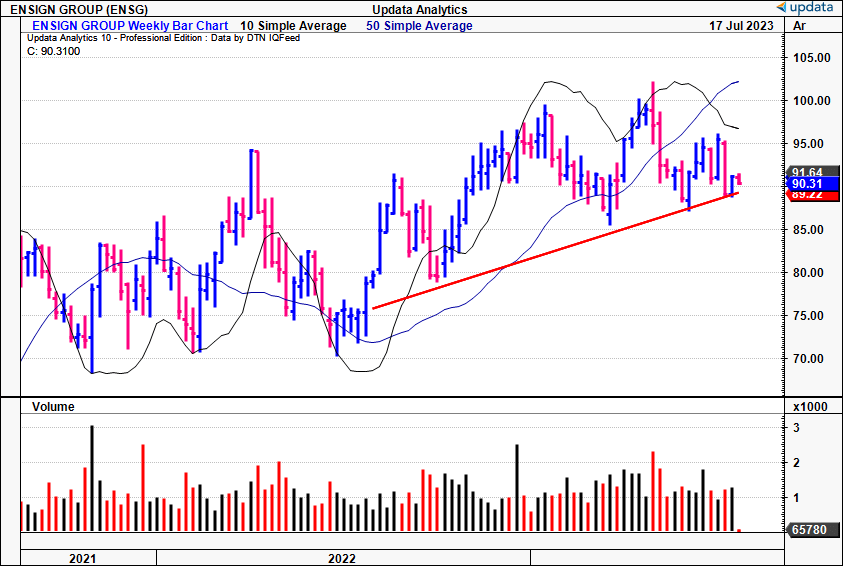

Following the last publication on The Ensign Group, Inc. ( ENSG ), shares have congested sideways with no major action to the upside. The company now trades at 19.3x forward earnings, a shade off its prior multiples during the last report.

Make no mistake, investing is a long-game, and ENSG is the epitome of the same. Those oriented for the long-term, with patience, and a knack for appreciating the economic characteristics of a business will be wise to read on further.

As a reminder, ENSG operates through its skilled services segment and the ownership of its subsidiary healthcare REIT, Standard Bearer ("SB"). This is tremendously attractive to my investment cortex. On the one hand you have access to the skilled labour portion of healthcare, one that has commanded a large premium in recent years due to shortages and overall demand. The pandemic only heightened this. Then, you're exposed to $1.3Bn in healthcare real estate through SB, with a total of 10,104 operational beds on the books.

It is no wonder that earnings have compounded at 2.4x that of sales over the last 5-6 years for the company. It's also:

- Beaten The Street's EPS estimates every quarter since 2018.

- Compounded its intrinsic value at c.17% over this same time (on my numbers).

- It also paid $0.57 in quarterly dividends last period.

Here I'll run through all the major updates to the ENSG investment debate, making spectacle of the company's unit economics, and how they are ratcheting up back to pre-pandemic highs. This is critical for the company to trade back at prior highs. I'll also show the positive changes in sentiment, and that valuations make sense at 19x forward. Net-net, reiterate buy, looking for objectives of $122 then $133.

Figure 1.

{kind=link}

Critical facts to ENSG buy thesis

There's been a number of updates to the key investment facts in my ENSG thesis. Chief among these are fundamental, sentimental and valuation factors. The fundamental factors stem from the unit economics displayed in the company's core operations-these set ENSG up for a qualified growth period ahead-combined with SB's outlook.

1. Fundamental factors

When analysing the company, it helps to think in first principles. For ENSG, that means a thoughtful analysis of its unit economics. Looking back to the company's Q1 numbers (posted all the way back in the dinosaur age of April 2023), much is gleaned. You get to see ENSG's economic flywheel in full motion. Just have a look at some of these additions to its portfolio:

- 17 skilled nursing operations in California, resulting in the addition of 1,462 operational beds.

- 2 professional nursing operations in Colorado, contributing 302 new operational beds.

- Over the 12 months to March 31, 2023, this pulled in to a total of 42 new operations, building in another 4,640 beds to its portfolio.

None of these stats would mean much if there wasn't the occupancies to back them up. This came to 78.8% in Q1, and has more or less recovered to pre-pandemic highs of 80%. Several crosscurrents are driving this recovery, including the reduction in agency labour, and an increase in patient turnover with restrictions fully lifted.

As a result, ENSG got to 5.4% growth in same-facility operations, coupled with 350bps gain in skilled mix days. Same-store managed care census and collected care revenue were also up 9% and 11.9% YoY, respectively.

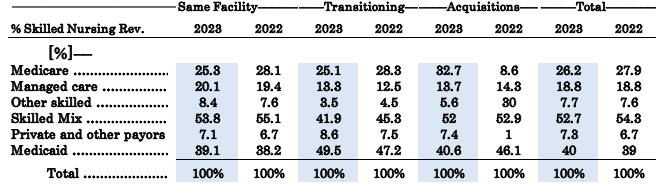

Back to first principles, each of these numbers tell me ENSG is ratcheting up key drivers in its growth matrix. You also see the positive trends in payor source as further evidence of this. What's pleasing, as shown in Table 1, is the drift in skilled nursing revenue from Medicare to managed care, private payors and the other skilled sources.

Table 1. Skilled services revenue contributions

{kind=link}

Standard Bearer contributions:

As a quick reminder, SB currently holds 103 wholly-owned assets that are leased to 75 affiliated skilled nursing and senior living operations. An additional 29 senior living operations are leased to The Pennant Group ( PNTG ). Each property is subject to long-term triple-net leases, generating rental revenue of $19.7mm for the quarter. Of this, $15.9mm was derived from Ensign-affiliated operations.

I'd consider these additional facts:

- SB generated $13.2 mm in FFO last quarter, and 84 of its owned assets are currently debt-free.

- It left Q1 on earnings before interest, taxes, depreciation, amortization, and rent (EBITDAR) to rent coverage ratio of 2.5x [i.e.: EBITDAR:rent cover = 2.5x]. Looking ahead, ENSG is prepared for further growth in 2023.

- Additionally, the company remains committed to deleveraging its portfolio given the current rates' situation. It is eyeing lease-adjusted net leverage (net debt-to-EBITDA) of 2.06x by the coming two years.

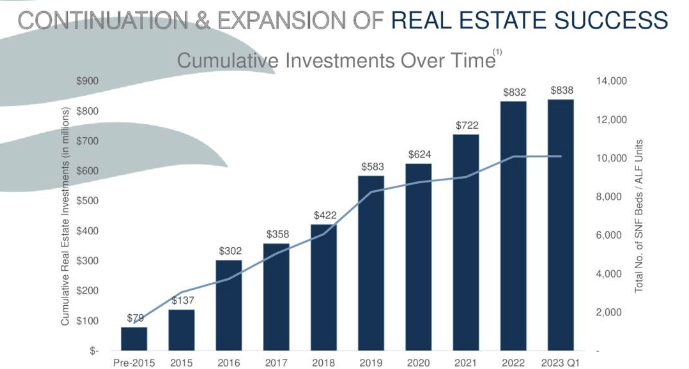

With respect to liquidity, ENSG has >$590mm in available capacity under its line of credit, complemented by a healthy cash balance, and thus is ~$900mm liquid as we speak. That's ample capital ready to deploy for future investments in my view. You can see the asset growth via the capital commitments shown in Figure 2. Lastly, ENSG disbursed a cash dividend of $0.0575 per share during the quarter.

Figure 2.

{kind=link}

2. Sentimental changes

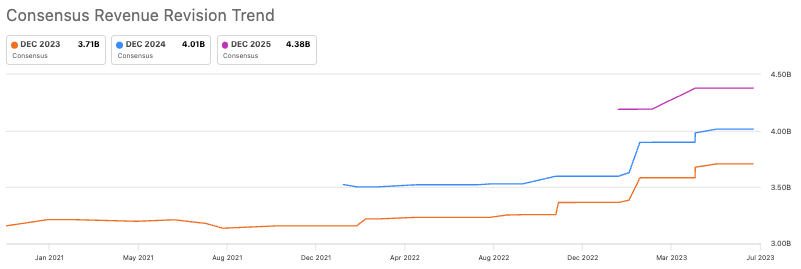

I was looking for potential catalysts to what might move ENSG's equity stock from the previous analysis. Current sentiment in the stock has delivered just that in my view. Analysts on The Street have made 4 revisions to the upside on both revenue and earnings for the company, key to seeing the stock trade higher in my view. In these estimates, you have the view of an entire substrata of the market populous, whom go by these numbers. Hence, a shift higher in these estimates also signifies a positive shift in sentiment in my view.

Consensus now projects $3.71Bn in sales this year on earnings of $4.72, 22% and 14% YoY growth percentages respectively.

Figure 3. Positive upshifts in revenue estimates

{kind=link}

Meanwhile, options-generated data tells me that investors-those with actual money at risk in ENSG-have the stock to stretch up past the $100/share mark by August/September. You see this in the open interest and volume of calls with strikes at this depth. Hence, you've got actual money positioned for ENSG to drive past its current mark, up another $10/share at least. There's even demand for calls out to $120 strike depth, adding to this bullish view.

Finally, price momentum is also improving. ENSG is pushing up towards its moving averages, and trades more-or-less in line with its short and long term average prices (10, 50, 100 and 200-day moving averages). This, combined with the data above, tells me that sentiment is likely shifting higher, and that investors are paying the current market multiples without too much resistance. Collectively, my estimation is that sentiment could be a key driver to see ENSG rate higher in the mid term.

3. Valuation factors

Investors are still selling the stock at 19x forward earnings and $3.83 book value. I'm not concerned about the premium to book value- it's a weak indicator of value, and the premium to the sector tells me investors value ENSG's net assets higher than peers, and it also shows ENSG has created $3.80 in market value for every $1 in book value over time- very attractive.

Question one has to ask, is paying $19 for every $1 in forward earnings worth it in this instance? Well, consider a few things. Using my own estimates, I wouldn't be surprised to see ENSG hit $3.5-$3.8Bn in turnover this year, especially after management raised its forecasts to $3.7Bn at the upper end of range. I'd look for $336mm in post-tax earnings on this, puling to $650-$700mm in owner earnings, given reductions in NWC density.

Critically, at 19x my estimates of post-tax earnings, gets me to $115/share in equity value. As a reminder, extending the owner earnings' forecast out to FY'28 gets me to $7.3Bn in firm value and an equity value of $133/share, in line with my previous forecasts (see: previous analysis, "Fig. 8" ). Thus with the revised forecasts I'm still seeing an upside range of $122 and then $133 per share into the coming periods. This supports a reiterated bullish view.

Discussion

Based on the culmination of investment facts discussed here today, that build on my previous ENSG deep dive, there is ample evidence of the company's long term good fortunes. With a history of strong earnings leverage, attractive returns on capital, and the multi-modal revenue stream of skilled nursing + SB- my investment cortex is switched right on. The company remains committed to its disciplined purchase of either flourishing or distressed assets, thereby adding to its organic growth profile. Valuations make sense to me at 19x forward and applying this to my FY'23 numbers gets me to $122 in value, and extending these out to FY'28 gets me to $133 discounting back to the present.

With the growth percentages shown in Q1, there is all reason to suspect these numbers will continue going forward. What's exciting is the fact total occupancy rates, along with skilled nursing mix, are each pushing to pre-pandemic highs. That, and the more than 4,000 new beds it's added under its wings in the last 12 months or so. This kind of momentum cannot go un-noticed in my view. Net-net, I am reiterating ENSG as a buy for all these reasons.

Figure 4.

Data: ENSG Investor Presentation

For further details see:

Ensign Group: Unit Economics Ratcheting Back To Pre-Pandemic Highs