ESGR - Enstar Group: Solid Performance But Still Unappealing Price Point

2023-08-23 11:39:20 ET

Summary

- Enstar Group Limited has a sound balance sheet and earnings potential, but the premium prices may not be worth paying.

- ESGR specializes in "run-off" insurance, helping insurance companies streamline operations and eliminate future liabilities.

- The preferred stocks ESGRO and ESGRP offer stable income streams and attractive yields, making them a better investment option than ESGR.

Introduction

The appealing factor about Enstar Group Limited ( ESGR ) right now has to be the sound balance sheet and earnings potential for the company. However, the company is trading at some premium prices that I am unsure are worth paying for. There are however some solid buybacks happening over the last couple of years and with robust margins the company is likely to keep this up I think. Because of this, I am rather seeing ESGR as a hold right now instead of a buy for investors. There is value to be extracted, just not enough share appreciation to warrant a buy case though. Net earnings landing at $21 million for the last quarter though is solid and provides holding incentives and the earnings helps build up the buyback program.

Company Structure

ESGR stands out as an insurance company with specialized expertise in the realm of "run-off" insurance. This distinctive approach comes into play when insurance companies seek to streamline their operations or exit particular lines of business. In scenarios where an insurance company wishes to liquidate, a critical requirement is to eliminate any future liabilities. To achieve this, they turn to ESGR, essentially transferring their existing insurance policies to offload potential future obligations, thereby facilitating their liquidation process.

{kind=link}

Furthermore, ESGR's services extend to those insurance companies that wish to discontinue specific segments of their insurance business. In such cases, these companies choose to entrust ESGR with taking over the management of these policies, allowing them to concentrate on other aspects of their business strategy. ESGR's adeptness at assessing and managing the risk associated with these policies has enabled the company to excel in this unique niche, as indicated by the compelling performance illustrated in the chart below.

{kind=link}

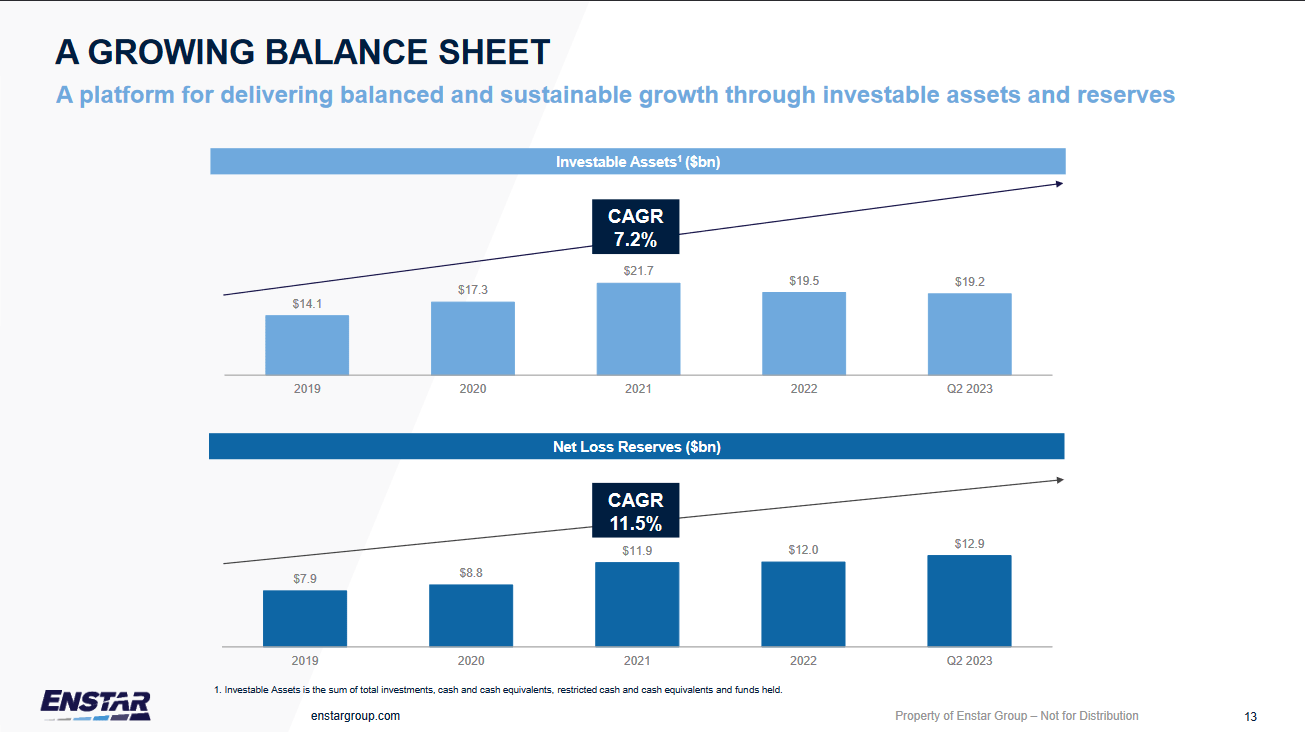

The balance sheet for ESGR has been steadily climbing over the years and has extruded a 7.2% CAGR between 2019 and Q2 2023. The TTM ROA for the company is at 1.26% currently and is below where the company has traditionally been the last 5 years, but I think as interest rates grow the company will be able to increase its yields substantially. The company will continue to deliver a sound shareholder return as buybacks continue. But I don’t think it's impossible that a slight pullback in the price happens over the short term. The shares have climbed by nearly 30% and that could warrant a correction quite frankly.

Preferred Share Opportunity

One of the appealing parts of ESGR is the preferred stock it has, which is ESGRO and ESGRP. Below is a summary of the two which also highlights the differences between the two.

ESGRO shares offer a fixed-rate coupon of $1.75 annually, with non-cumulative dividends paid quarterly. ESGRO presents a stripped current yield of 7.36%. There is the possibility of shares being called on 3/1/2024 at $25. Dividends provided by ESGRO are qualified for the favorable 15% tax rate. The shares have remained largely stable as the yield remains around the market-appreciating target of 7 - 8%. I don’t think we will see it approach 10% as that would most likely trigger more investment firms to go in and drive up the price again. Factors that could drive the yield higher though is poor market sentiments.

{kind=link}

ESGRPs are fixed-to-floating rate preferred stocks that offer a stable income stream. Currently, they carry a fixed-rate coupon of $1.75 annually, accompanied by non-cumulative dividends paid quarterly. ESGRP reflects an attractive stripped current yield of 7.38%. Investors should note that there is a possibility of shares being called on 9/20/2028 at $25.

If ESGRP shares are not called on the specified date, it's important to be aware that the dividend structure will transition to a floating rate. This floating rate will be determined by LIBOR plus 4.015%, introducing an element of variability to the dividend payments. Furthermore, it's noteworthy that dividends from ESGRP are qualified for the favorable 15% tax rate. This blend of fixed and potential floating dividends, coupled with the potential for a call, adds a layer of complexity to the investment, which investors should consider when evaluating its suitability for their portfolio.

As for the one that I prefer, I think it would be ESGRP just because of the higher yield. Both of them offer a sound yield opportunity and they are both very stable, which is why I think one can go with the highest-yielding one without risking too much.

Earnings Transcript

From the last earnings call, the CEO Dominic Silvester had some words to share about the company's performance and their outlook for themselves and the industry.

"We refinanced and upsized our revolving credit agreement from $600 million to $800 million, and extended its term by five years through May 2028, thereby strengthening our balance sheet and further increasing our liquidity position. Our pipeline continues to be robust, and we remain disciplined in our search for appropriate opportunities that meet our internal hurdle for risk-adjusted returns".

By growing and enhancing its liquidity levels, the company once again manages to sit in a very solid position to deliver shareholder value over the long term. The size up deleverages them in my opinion and based on the p/b ratio of 0.8 the company does look appealing as an investment holding still in my opinion.

Investor Takeaway

ESGR has been able to deliver a solid few quarters and the share price has increased by nearly 30% which has been a great reward to shareholders, but the price does not look too appealing to buy into currently though. A pullback seems probable and when comparing ESGR to its two preferred stocks I think those offer more buying incentives than ESGR right now, as they have a higher yield and more stability too. In conclusion, though, I am rating ESGR a hold for now.

For further details see:

Enstar Group: Solid Performance, But Still Unappealing Price Point