ENTG - Entegris: Better Growth And Margin Outlook

2023-11-29 03:32:38 ET

Summary

- ENTG has shown signs of growth recovery and gross margin expansion.

- The MC segment displayed sequential and annual growth.

- Management's efforts to optimize the portfolio and reduce inventory have positively impacted gross margins and free cash flow.

Summary

Readers may find my previous coverage via this link . My previous rating was a buy, as I believed Entegris ( ENTG ) would continue to see positive business traction and eventually recover from the previous challenges it was facing. Importantly, management remained focused on reinvesting in R&D. I am reiterating my buy rating as ENTG has shown signs of growth recovery and gross margin is expected to continue expanding. The market has also re-rated ENTG multiples upwards, which I expect to sustain at the current level.

Financials / Valuation

ENTG reported 3Q23 revenue of $888 million, representing a negative y/y growth of 10% and 1% sequentially. By segment, Materials Solutions reported revenue of $436 million, representing a negative y/y growth of 16% and 1% sequentially, on a pro-forma [PF] basis; Microcontamination Control [MC] reported revenue of $286 million (PF basis), growing 1% sequentially and 2% annually; and Advanced Materials Handling [AMH] reported revenue of $180 million (PF basis), representing a 5% sequential decline and 14% annually. ENTG also saw non-GAAP gross profit margin decrease sequentially by 120bps to 41.4% and non-GAAP EPS of $0.68.

Based on author's own math

Based on the updates provided in the 3Q23 earnings, I have adjusted my FY23 growth estimates down to 6.4% (3Q23 performance was not as good as I thought, but directionally has improved) and to also reflect management 4Q23 guidance. With a slightly more positive outlook into FY24 (MC segment did turn positive this quarter), I believe ENTG should be able to sustain the current growth rate into FY24. My estimates for 10% growth in FY25 remain the same. However, I have bumped up my margins assumption over the next 2 years, given that inventory headwind is going to taper down and management continues to optimize the portfolio. I believe the 3Q23 results have made the market realize that ENTG is on track to recover its growth, which can be seen from the increase in valuation multiple from 28x to the current 32x. At 32x, ENTG is trading at roughly the same premium it has traded over its peers historically, so it is not in the stage of "overvalued," albeit the high absolute multiple. With a better outlook for growth and margin, I am valuing ENTG using 32x forward PE.

Comments

There are several positives in this quarter that are moving in the right direction. Firstly, ENTG finally shows signs of positive growth. Revenue in the MC segment increased on a yearly and sequential basis, even though the semiconductor market remains difficult. Products for gas purification, wet etch, and clean filtration were particularly in high demand. I believe that the requirement for more purity in Logic/Foundry and Memory is the driving force behind this robust underlying demand. Consequently, this should keep the MC segment's growth momentum going forward. One important thing to keep an eye on is the construction of new fabrication facilities. In my opinion, this will be a major factor in the growth of MC in the coming years, especially when localization initiatives gain traction.

In particular, we saw growth in advanced deposition materials and wet etch and clean liquid filters. In addition, we had another strong quarter in SiC slurries and pads, reflecting the growth of that industry segment and our strong market position.

There are two sides to the opportunity. I mean, one, it would be things related to the new fab construction. So wafer carriers, large gas purification systems, so products that you're all very familiar with. Source: 3Q23 earnings

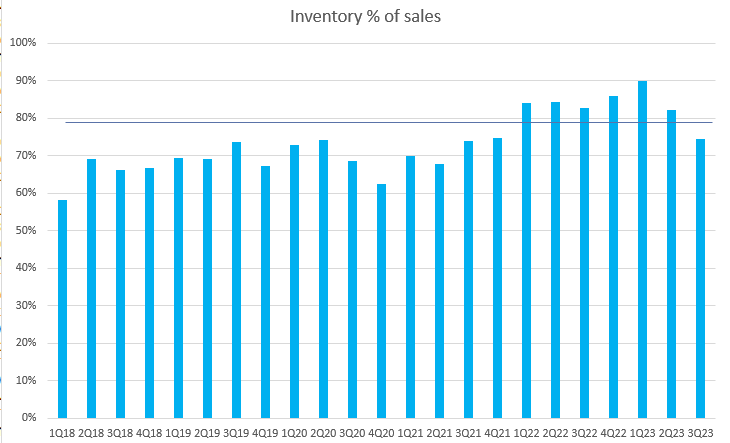

Another positive indicator of recovery is that gross margins are bottoming and should expand sequentially in the next few quarters. This was guided by management, in that gross margin is expected to come in at 42.5% in 4Q23, representing an expansion of 110bps. There are two factors impacting the gross margin. Firstly, the success of management’s effort to optimize the portfolio is bearing fruit. Notably, management has completed three divestitures year-to-date, with the sale of the Electronic Chemicals business being the most significant one, and since all of these have lower margins, it drove an improvement in gross margin. Secondly, management is on point with inventory levels. Over the past few quarters, inventory as a percentage of sales has been running at an elevated level (>80%), and management made the decision to reduce inventory significantly this quarter, which led to gross margin pressure due to lower utilization rates. In the quarter, management reduced inventory by $80 million on a sequential basis and plans to reduce inventory again in 4Q23 by ~$45 million.

Looking ahead, given that inventory is tracking back to a more normalized level and the reduction in inventory is of lesser magnitude compared to 3Q23, I don’t expect this to be a major headwind again. In addition, management has plans to continue optimizing its portfolio, which I take as an indication that they are going to divest away low-margin businesses (like Electronic Chemicals). As such, I expect the gross margin to expand sequentially.

{kind=link}

I also like how management is managing its FCF generation and capital allocation. While the reduction in inventory has impacted gross margins, it has helped with FCF generation (reduction in working capital), leading to ENTG generating the highest FCF since 4Q20. On-point inventory management and portfolio optimization gave ENTG the capability to pay down its debt, and management plans to use the proceeds from its Electronic Chemicals divestiture to pay down an additional $730 million in debt. As of 3Q23, ENTG has ~$5.5 billion in debt and $600 million in cash.

Elsewhere, it was great hearing from management that there is no need to worry about the China export restriction as it is expected to have no material direct impact.

Risk & conclusion

Nevertheless, regardless of the positives from the quarter, my growth estimates would be negatively affected by a slower-than-expected turnaround in production rates because of how unpredictable the macroeconomic environment is.

In conclusion, 3Q23 results showed that ENTG is seeing signs of growth recovery and margin expansion. The MC segment displayed sequential and annual revenue growth, attributed to increased demand for certain products amid the semiconductor market challenges. Management's efforts to optimize the portfolio and inventory management bode well for margin expansion. While inventory reduction temporarily impacted margins, it significantly improved free cash flow and facilitated debt repayment. Overall, I maintain a positive outlook for ENTG.

For further details see:

Entegris: Better Growth And Margin Outlook