ENTG - Entegris: Strengthened Balance Sheet Allows For More Focus On R&D

2023-10-03 15:52:25 ET

Summary

- Entegris' sequential growth analysis shows positive traction in its investments, indicating an eventual recovery.

- The company is focused on strengthening R&D investment capabilities to drive growth.

- Despite near-term challenges, management's actions to improve the balance sheet and increase cash reserves position Entegris for long-term success.

Summary

I am recommending a buy rating for Entegris ( ENTG ). While the y/y figures might not be the best, sequential growth analysis shows that ENTG's efforts in investing in the business are showing positive traction. I expect growth to eventually recover after ENTG works through the current volume and challenges. More importantly, management is steadfast in improving the business through corporate actions to strengthen R&D investment capabilities, which is, in my opinion, a key driver of growth.

Business

ENTG is a worldwide supplier of advanced materials and process solutions, mainly to the semiconductor and life sciences industries. Some of the solutions include gas and liquid purifying filters, gas delivery systems to safely store and deliver toxic gases, and many others, as shown below. As of FY22, the business has nearly ~$3.9 billion of revenue on a pro-forma [PF] basis, holds 4,400 active patents, and has almost 9,500 thousand worldwide.

{kind=link}

Financials / Valuation

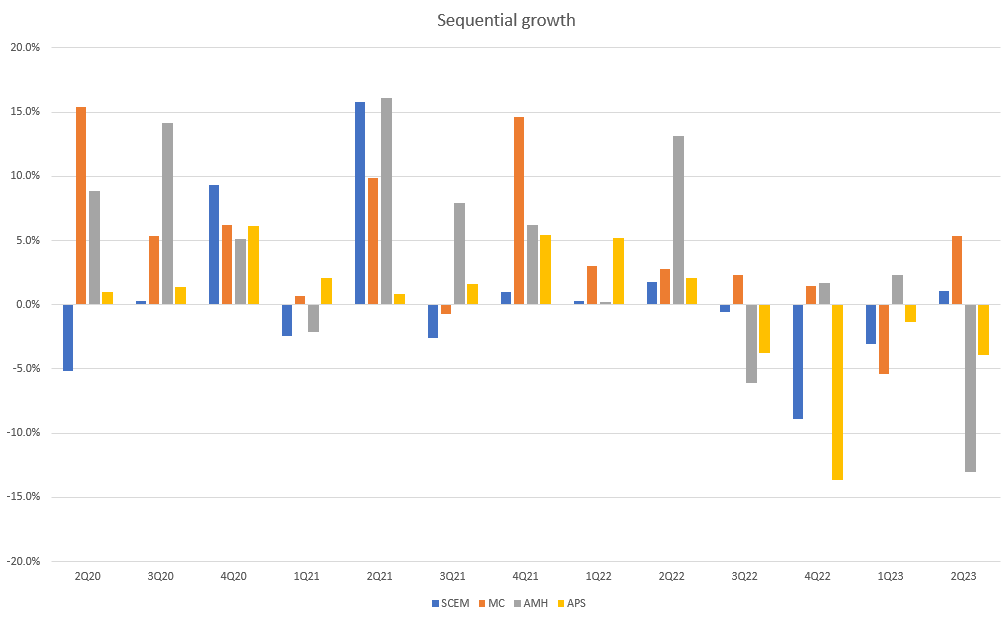

ENTG reported second-quarter 2023 revenue of $901 million, surpassing expectations by 2%. However, it saw an 11% decline compared to the previous year when adjusting for certain factors. Looking at the different segments on a pro forma [PF] basis, Specialty Chemicals and Engineered Materials [SCEM] generated $200 million in revenue, marking an 11% decrease. Microcontamination Control [MC] revenue increased by 3.2% to reach $284 million. Advanced Planarization Solutions [APS] revenue dropped by 21% to $241 million, and Advanced Materials Handling [AMH] revenue declined by 15% to $190 million.

The overall performance suffered due to a decrease in the non-GAAP gross margin, which fell to 44.3%, a decline of 170 basis points. However, it's worth noting that the adjusted EPS came in at $0.66, surpassing consensus estimates by more than 15%, which suggests that cost control has been top-notch.

Based on author's own math

Based on my view of the business, ENTG should see 10% growth in FY23, which I assumed based on extrapolating management revenue guidance (range of $875 million to $900 million) to 4Q23, which implies revenue of ~$3.6 billion. However, given the near-term headwinds that ENTG is facing (declining volume, etc.), I expect FY24 to be a weaker year, followed by a recovery to 10% growth in FY25. Despite that, margins should continue to increase as management has divested and ended business units with a lower margin profile. I assumed ENTG would continue to trade at 28x forward PE as the current spread (~30+ premium vs. historical premium of 40%) between itself and its peers is in line with history.

- Teradyne, Inc.

- Onto Innovation Inc.

- Allegro MicroSystems, Inc.

- MKS Instruments, Inc.

- Amkor Technology, Inc.

- Axcelis Technologies, Inc.

- FormFactor, Inc.

- Veeco Instruments Inc.

- Aehr Test Systems

- Ultra Clean Holdings, Inc.

According to my model, there is a 17% upside at a price target of $109.

Comments

{kind=link}

In 2Q23, MC was the only business segment to grow at an annual rate of growth, so its performance stands out. As dies get bigger and new complexities arise from technology shifts like gate-all-around transistors and advanced packaging, I think yield optimization will become increasingly important in the semiconductor industry, so I don't see any impediments to the MC segment's continued growth. While the headline growth numbers aren't encouraging, a sequential analysis of 2Q23 results reveals an encouraging trend: SCEM has turned positive after three consecutive quarters of negative growth. SCEM's management is placing a premium on research and development [R&D], which should propel growth as the company develops innovative solutions to capitalize on the many expansion opportunities in fields like advanced deposition materials. I believe that growth will result from these expenditures. However, I should warn readers that it could be a short-term drag on operating margins within the segments. The SCEM segment's operating margins were 10% in 2Q23, down 700 basis points from 2Q22. I think the investments are warranted, and investors who are willing to hold out for the long haul should be rewarded.

The good news is that all of those roadmaps are becoming much more demanding. In advanced packaging, I think we expect a much greater degree of precision of automation, a degree of cleanliness required in their processes. We also believe there will be more polishing steps required with the bonding of the wafers. And all of that will open up opportunities for our AMH products in terms of wafer carriers, slurries, and pads for the polishing applications, and very likely also opportunities for our filtration and cleaning product lines. Source: 2Q23 earnings

In addition, I applaud management's efforts to bolster the balance sheet through corporate actions. On October 2, 2023, the most notable event was the sale of ENTG's Electronic Chemicals business to Fujifilm for $700 million. Remember that ENTG is currently investing heavily in R&D, which could increase the company's need for liquid assets, so this infusion of $700 million is welcome news. With this infusion of $700 million and the $200 million from the termination agreement with Element Solutions, the company's cash position has increased to $1.4 billion from $565 million as of 2Q23, and net debt to EBITDA has decreased from 5.5x to 4.3x. I also anticipate that the potential sales of the pipeline and industrial materials business will provide ENTG with additional funds to increase their R&D spending. Reducing debt on a regular basis (management target is 3.5x net debt to EBITDA by the end of FY24) and using the proceeds from various strategic actions is something I think will do more than just boost EPS but could also help prop up the company's valuation.

In the short term, ENTG is grappling with several challenges that are negatively impacting its gross margins. These include reduced volumes, increased fixed costs related to the new manufacturing facility in Taiwan, and the termination of the distribution agreement with Element Solutions. Nevertheless, I anticipate that these obstacles will diminish in the coming quarters, and investors will shift their attention towards ENTG's growth prospects and the potential for expanding margins, especially now that the company has divested its lower-margin business units.

Risk & conclusion

One particular risk specific to ENTG is the uncertainty related to the cyclical nature of the AMH segment. This segment relies heavily on investments in Wafer Fab Equipment. In the second quarter of 2023, the AMH business saw a sequential decline of 13% and an annual decline of 15%. This decline occurred despite strong performance in fluid handling, as it was outweighed by weakness in Front Opening Unified Pods (FOUPs). It is likely that performance will be volatile for the near-term as there is limited visibility into the trajectory of a WFE recovery.

In conclusion, I recommend a buy rating for ENTG. While year-over-year figures may not be ideal, a closer look at sequential growth suggests that ENTG's investments in the business are gaining traction. Despite the current challenges, ENTG's management has taken significant steps to strengthen its balance sheet, with notable actions such as selling its Electronic Chemicals business and increasing cash reserves. While there are uncertainties in the cyclical AMH segment, I believe ENTG's focus on innovation and cost control, coupled with its improved financial position, positions it for long-term success. Investors should monitor the company's progress as it navigates through these challenges and seizes opportunities for growth and margin expansion.

For further details see:

Entegris: Strengthened Balance Sheet Allows For More Focus On R&D