EXC - Entergy Corporation: Stock Punished But Not Underpriced Compared To Peers

2023-07-10 18:46:52 ET

Summary

- Entergy Corporation is a regulated electric utility that serves the Gulf Coast region of the United States.

- The company has a surprisingly strong focus on renewable energy and is spending a substantial amount of money to expand the proportion of renewables in its portfolio.

- Entergy's stock price has been punished, apparently due to a series of power outages in Louisiana and Arkansas.

- The company is a bit more leveraged than its peers and sports a very attractive 4.39% dividend yield.

- The valuation is better than it has been in a while, but it is not especially cheap compared to its peers.

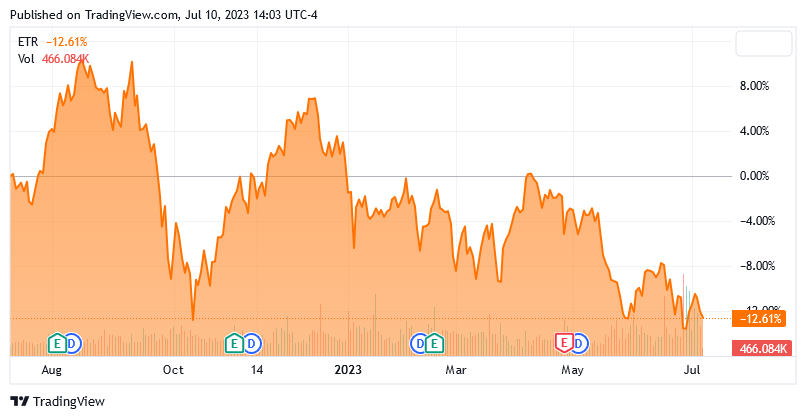

Entergy Corporation ( ETR ) is a major regulated electric utility that serves the Gulf Coast states of Texas, Louisiana, Mississippi, and Arkansas. The utility sector in general has long been a favorite of conservative investors such as retirees due to its very stable cash flows and generally high dividend yields. Entergy Corporation is no exception to this as the stock yields 4.39% at the current price. This is one of the highest yields in the sector, which is the result of the company's stock price declining by 12.61% over the past twelve months:

{kind=link}

One of the reasons for this is that the company has been under fire for a series of power outages across Arkansas and Louisiana. It is uncertain how much responsibility the company actually bears for this, however, and indeed its stock price decline started long before any of these problems began. It is possible that the market weakness has provided an opportunity for its shareholders as the company is affordably priced relative to many of its peers. As I discussed in prior articles on the company, it has also been one of the most aggressive utilities in the nation when it comes to the deployment of renewable sources of energy, which could be an appealing thing for many shareholders. I last discussed this company back in April, so let us revisit it and see if it still makes sense for a portfolio today.

About Entergy Corporation

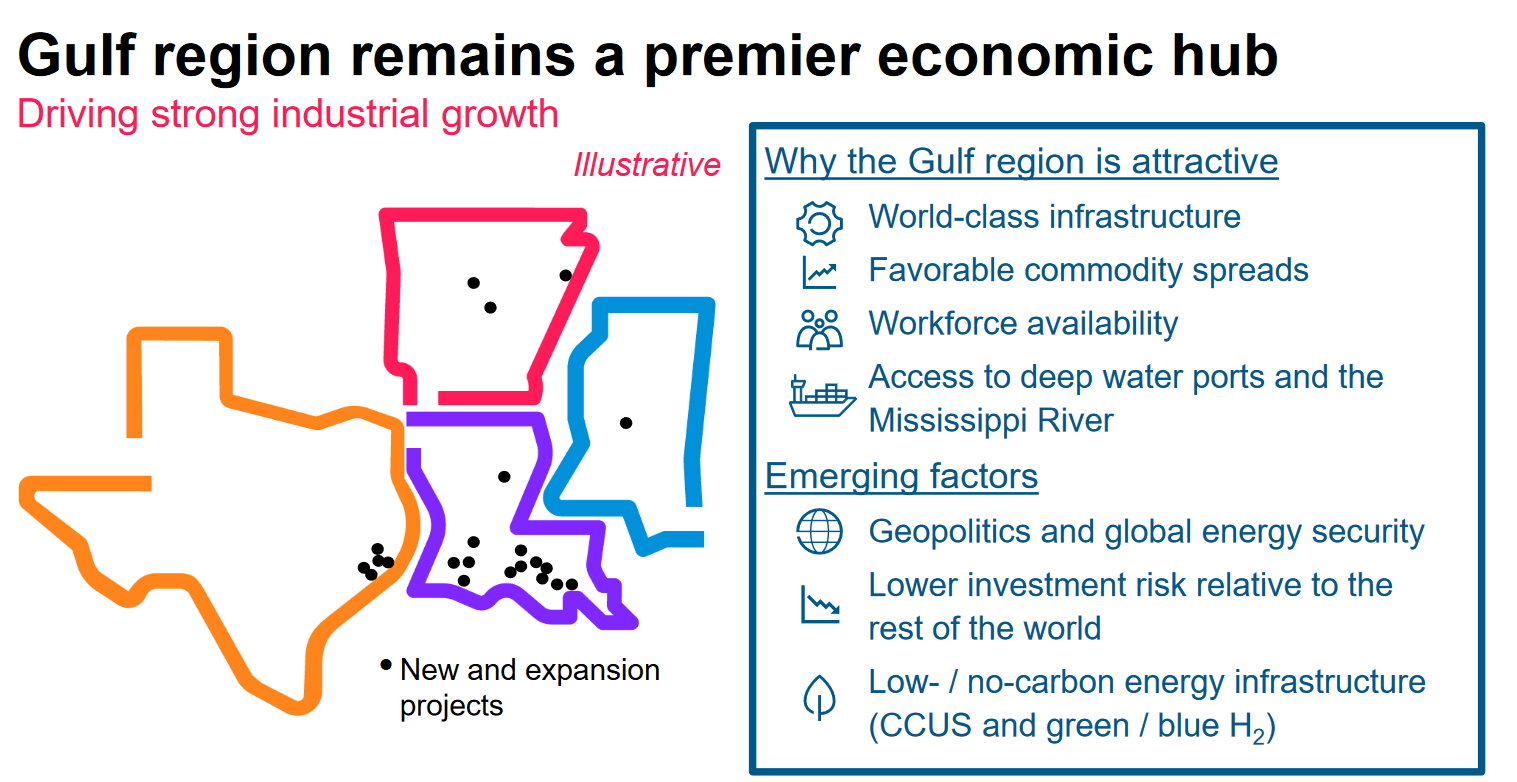

As stated in the introduction, Entergy Corporation is a regulated electric utility that serves the Gulf Coast states of Texas, Louisiana, Mississippi, and Arkansas.

{kind=link}

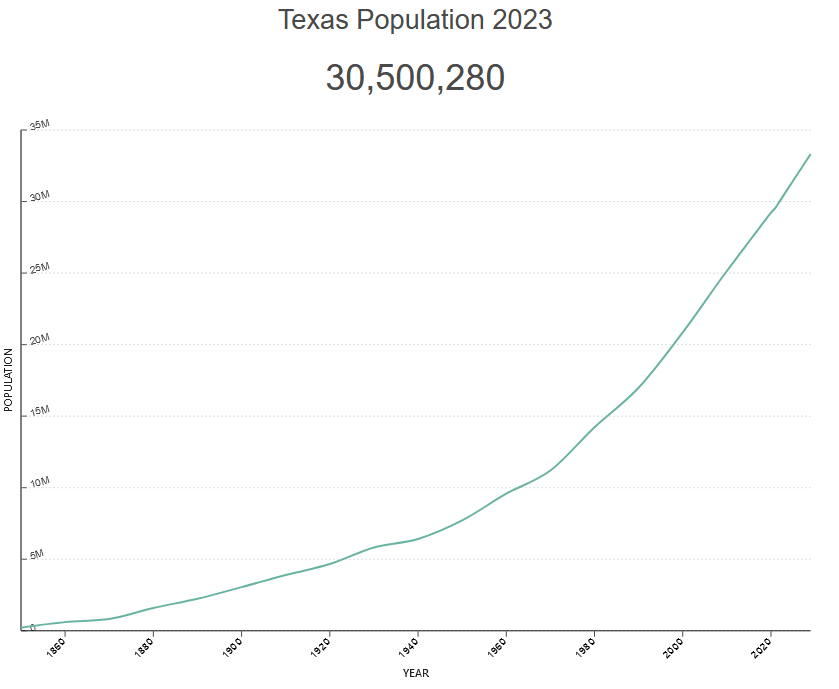

This is one of the more rapidly growing regions of the United States, particularly the state of Texas. As we can see here, the state of Texas has seen its population grow significantly since the outbreak of the COVID-19 pandemic in 2020, going from 29.2 million people at the time to 30.5 million today:

{kind=link}

This is a continuation of a trend that began long before 2020, but that year is generally considered a turning point for demographers. The reason for this is that remote work became an extremely popular concept for many companies and employees, which resulted in people living where they want to as opposed to where they have to because of work. We have seen some states, such as California, lose population ever since that development happened as people flee to other states that appeal more to them.

The reason that this is important for Entergy is that population growth is one of the only ways that a utility can grow, and it is completely out of the utility's control. This is because Entergy is a monopoly that is restricted to operating in a specific region by law and it cannot expand by convincing customers outside of its service area to switch. The fact, then, that Texas is one of the fastest-growing states in terms of population provides a tailwind to the company's growth. The same is true of Arkansas, however, both Louisiana and Mississippi have been experiencing population declines since 2020. Overall, though, the trend is positive and Entergy currently serves approximately 3 million electric and 204,000 natural gas customers throughout its service area. When I first started covering the company back in October 2020 , the number was 2.9 million customers. Thus, it appears that Entergy is growing its customer base at a respectable rate.

The fact that Entergy currently has more than 3 million customers, makes it one of the largest utilities in the United States. However, as I have pointed out numerous times in the past, a utility's customer count does not affect the fact that it possesses certain characteristics. The most important of these is that Entergy will enjoy relatively stable cash flows over time regardless of macroeconomic conditions. We can see this quite clearly by looking at the company's operating cash flow. Here are its figures over the past eleven twelve-month periods:

{kind=link}

(all figures in millions of U.S. dollars.)

As we can see, the company's operating cash flow figures generally fall within the $2 billion to $3 billion range during any given twelve-month period. This remains true regardless of the broader macroeconomic conditions. For instance, the earliest periods on the above chart include the months at the outbreak of the pandemic when the country was locked down and the unemployment rate skyrocketed. It also includes the recovery period that was characterized by very high inflation, which continues today. The economy has, so far in 2023, shown numerous signs of weakening compared to its performance in 2021 and 2022. However, none of these things had a significant effect on weakening or strengthening Entergy's cash flows.

The reason for this general cash flow stability is the nature of Entergy's business. The company provides a product that is generally considered to be a necessity for modern life. After all, how many people do not have electric service in their homes? Indeed, electric service is pretty much necessary for just about anything else that someone might have in their homes for entertainment or work. As such, most people will prioritize paying their electric bill ahead of making discretionary expenses during times when money gets tight. After all, nobody will want to go out to a meal or two in a restaurant with their last $100 and risk having their electricity turned off.

As I have pointed out in a few recent blog posts (such as this one ), the high inflation that has been dominating the economy has strained the budgets of most ordinary consumers in the nation. In addition, most economists are predicting that the economy will descend into a recession during the second half of the year, and recessions normally result in job losses and weakening consumer finances. Entergy is exactly the kind of company that we want to be holding in such a situation, as it should not be affected very much by such an environment.

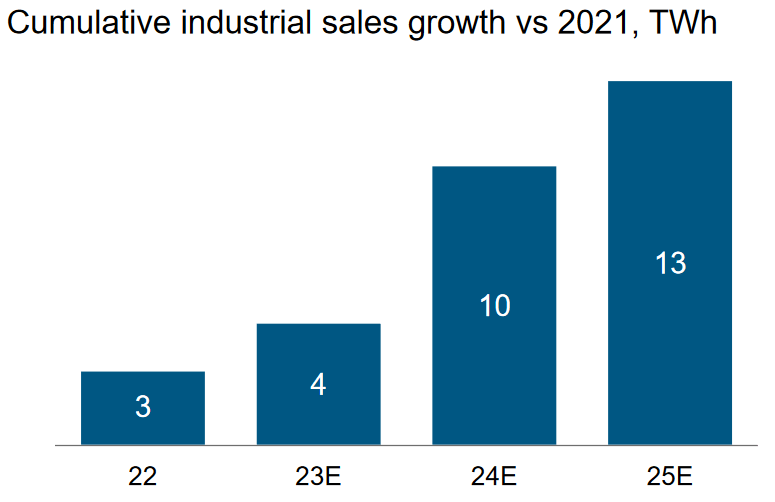

One of the major news stories over the past decade has been the growth of American manufacturing. While this growth has slowed down significantly over the past year or two, Texas and Louisiana still continue to exhibit fairly strong industrial and production growth. This is very nice from Entergy's perspective because industrial users typically use considerable amounts of electricity. As we can see here, industrial customers in 2022 used approximately three terawatt-hours more than they did in 2021. By 2025, the company expects that its industrial customers will be using thirteen terawatt-hours more annually than they did in 2021:

{kind=link}

If this growth trend actually plays out as projected, it will represent a 6% compound growth rate for the company's industrial sales. As the amount that the company's customers pay is in direct relationship to their consumption, this should result in growing revenues for Entergy over the period. However, there is an added benefit here in the fact that many industrial jobs are hands-on and cannot be home-shored in the way that an office job can. Thus, the growth of the industrial base in Entergy's service territory should result in a growing number of residential customers as the employees of these industries move into the area. This is a very good place for the company to be from a growth perspective.

Growth Potential

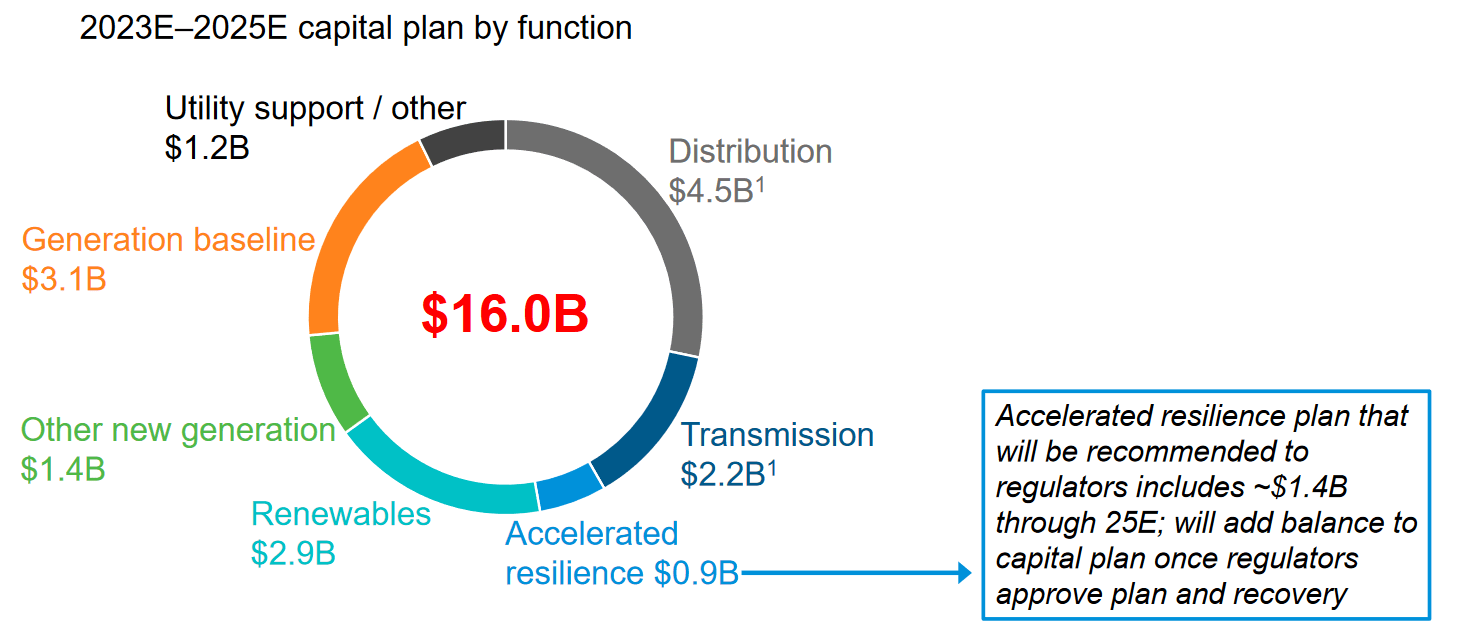

As we have just seen, the population and industrial base of Entergy's service territory is undergoing respectable growth. This positions Entergy quite well to grow its own business, although it will need to invest in its infrastructure in order to ensure adequate levels of service for its customers. The company is doing exactly this, as it is currently planning to spend $16.0 billion over the 2023 to 2025 period to improve its infrastructure:

{kind=link}

I will admit that it would be nice to have more guidance than this. Many of Entergy's peers have provided their 2023 to 2027 investment programs, which provide an extra two years of guidance. That is a very nice thing for long-term investors because the more information that we have, the easier it is to project where the company will be five to ten years from now. As it stands, it would be much easier to make these projections for one of the company's peers than for Entergy.

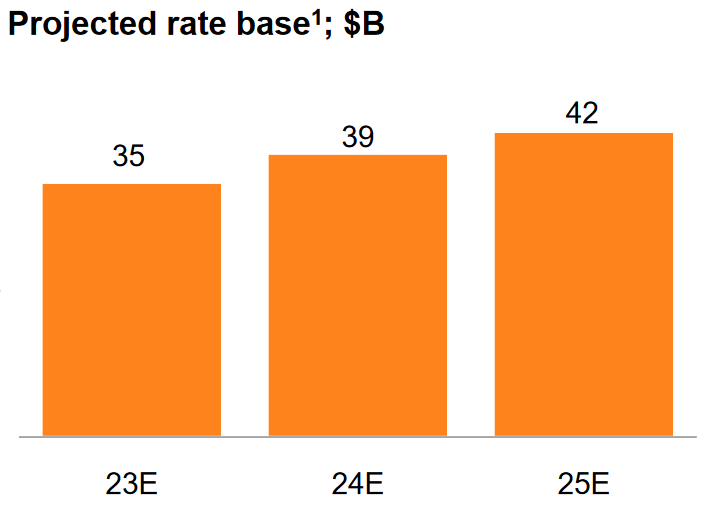

We can still make some projections from the information that Entergy has provided, however. The capital investment plan as outlined above will grow the company's rate base from $35 billion today to $42 billion in 2025:

{kind=link}

The rate base is the value of the company's assets upon which regulators allow the company to earn a specified rate of return. As this rate of return is a percentage, any increase in the rate base allows Entergy to adjust the prices that it charges its customers in order to earn more money. Thus, the fact that the rate base will be growing over the 2023 to 2025 period should result in earnings growth.

With that said, many readers may point out that Entergy's rate base will grow by much less than the amount that the company is investing in it. There are two reasons for this. The first is depreciation, which is constantly reducing the value of the assets that the company has in service. In order to overcome this, Entergy must spend enough to cover all of the depreciation and more if it wants to actually grow the rate base. In addition to this, Entergy will be retiring some of its assets during the period, which will result in the full remaining value of these assets being removed from the company's rate base. That will offset some of the spending that the company embarks on during the period.

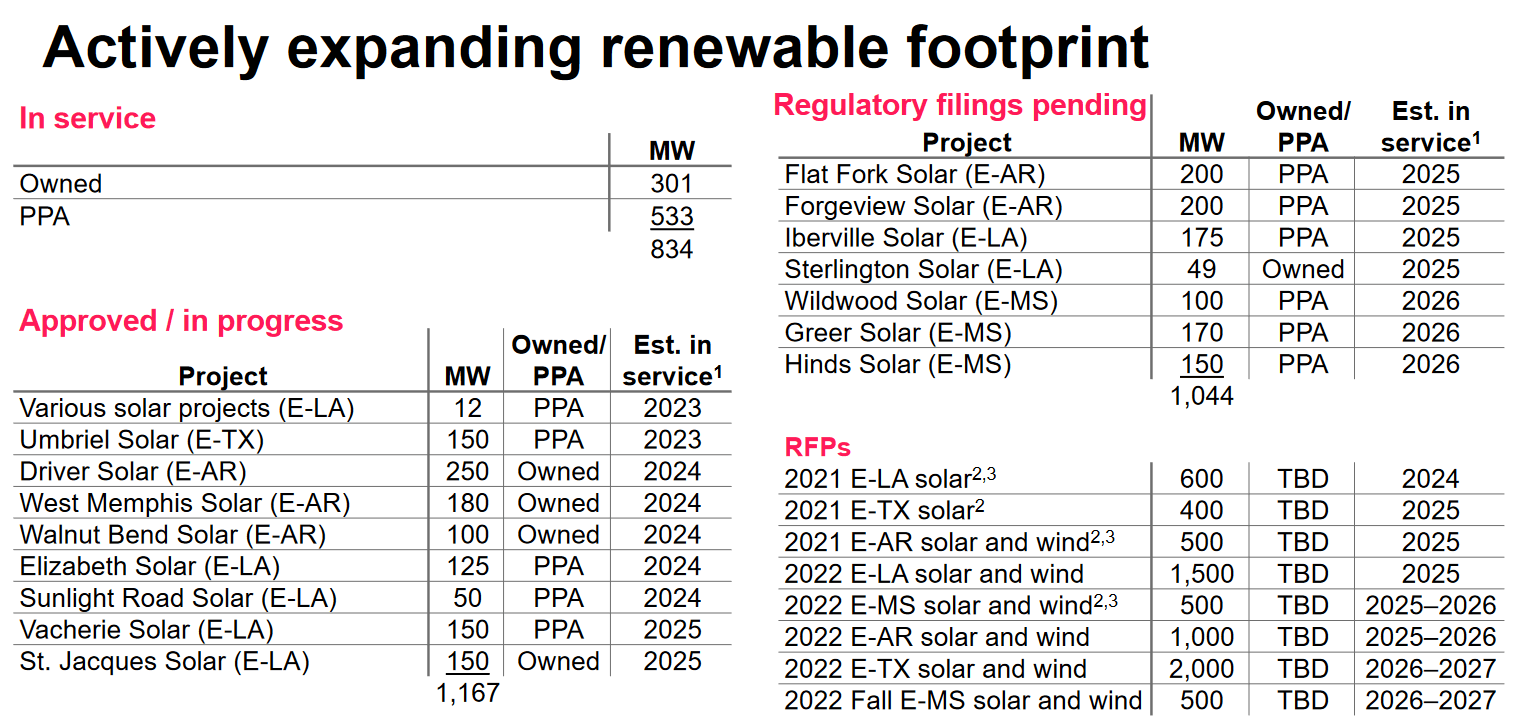

One of the company's goals is to completely retire all of its coal generation assets by 2030. This is a very common goal for many of the electric utilities in the United States as coal is generally considered to be a more polluting way to produce electricity than any other fossil fuel. Thus, the retirement of the company's coal plants will be one of the factors that offsets a certain proportion of its capital spending over the period. In place of these plants, Entergy is planning to use renewable energy. This may be surprising as Texas and the rest of the Gulf Coast is not normally considered to be a particularly progressive area of the United States, but it is already one of the furthest areas along in the transition to "green energy." This is partly because the geography and climate of the area are much friendlier to the use of solar and wind power than most other regions. As we can see here, Entergy has a number of wind and solar projects under development that are expected to be brought online by the end of 2027:

{kind=link}

The company's work on expanding its wind and solar plants may endear it to the various environmental, social, and governance funds that have sprung up over the past five years or so. This is especially true later in the decade as Entergy has the goal of generating about half of its electricity from renewable sources by 2031. Although these funds have fallen off a bit in popularity ever since the global monetary tightening began, environmental, social, and governance funds still have an enormous amount of money under management. I discussed this in a previous article . If Entergy's growing renewable portfolio begins to attract the attention of the managers of these funds, it could put a substantial amount of buy-side pressure under the stock price that drives it up. Admittedly, though, that is almost certainly a long-term story. As already mentioned, the stock seems to be experiencing some selling pressure right now due to a few widespread power outages that will hurt the company's revenue and profit for a quarter or two.

Financial Considerations

It is always important that we investigate the way that a company is financing its operations before we make an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. That is typically accomplished by issuing new debt and using the proceeds to repay the existing debt since very few companies have sufficient cash on hand to completely pay off their debt as it matures. As new debt is issued with an interest rate that corresponds to the market rate at the time of issuance, this can cause a company's interest expenses to go up following the rollover. As of the time of writing, the federal funds rate is at the highest level that it has been since 2007 so it is almost certain that any debt rollover will cause a company's interest expenses to rise. As such, this is a risk that we should be very cognizant of right now. In addition to this risk, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes its cash flows to decline could push a company into financial distress if it has too much debt. Although utilities such as Entergy Corporation tend to have remarkably stable cash flows, there have been bankruptcies in the sector before so this is still a risk that we should not ignore.

One metric that we can use to analyze a company's financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. It also tells us how well a company's equity can cover its debt obligations in the event of a bankruptcy or liquidation event. This second consideration is probably going to be more important.

As of March 31, 2023, Entergy had a net debt of $25.6184 billion compared to a shareholders' equity of $13.3863 billion. This gives the company a net debt-to-equity ratio of 1.91 today. Here is how that compares to some of the company's peers:

| Company |

| Net Debt-to-Equity Ratio |

| Entergy Corporation |

| 1.91 |

| DTE Energy ( DTE ) |

| 1.83 |

| Eversource Energy ( ES ) |

| 1.49 |

| CMS Energy ( CMS ) |

| 1.82 |

| Exelon Corporation ( EXC ) |

| 1.65 |

As we can see here, Entergy Corporation is somewhat more leveraged than its peers. That has been the case since we started discussing this company nearly three years ago so this is not surprising. However, it could still be a sign that this company is overly reliant on debt, which poses a risk to us as investors. It does not appear to be an especially outsized risk though, since both DTE Energy and CMS Energy have somewhat similar debt loads. Investors may still want to be cautious though, especially considering that interest rates on rollovers are going to be much higher now than they were in the past.

Dividend Analysis

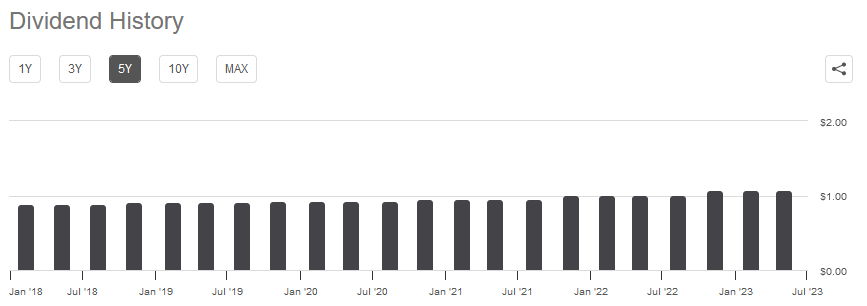

As mentioned in the introduction, one of the biggest reasons why investors purchase shares of utility companies is that these companies typically pay out higher dividend yields than most other things in the market. Entergy is certainly no exception to this as the company's current 4.39% yield is well above the 1.49% yield of the S&P 500 Index (SP500). This high yield comes from the fact that Entergy's growth rate is much lower than that of companies in some other sectors, so the market does not reward it with strong stock price appreciation. It, therefore, pays out a substantial percentage of its cash flows to investors to provide its shareholders with a reasonably competitive return. In addition to a high yield, Entergy also typically increases its dividend on an annual basis:

{kind=link}

As such, someone that purchases the stock today will almost certainly have a much higher yield-on-cost after a few years. A dividend that grows with the passage of time is also very nice to see during periods of high inflation, such as the one that we are experiencing today. This is because inflation is constantly reducing the number of goods and services that we can purchase with the dividend that the company pays out. This is a problem for anyone that is depending on their portfolio to generate the income that they need to cover their living expenses. The fact that the company increases the amount that it pays every year helps to offset this effect and maintains the purchasing power of the dividend over time.

As is always the case though, it is important that we ensure that the company can actually afford the dividends that it pays out. After all, we do not want to be the victims of a dividend cut since that would reduce our incomes and almost certainly cause the stock price to decline.

The usual way that we evaluate a company's ability to pay its dividend is by looking at its free cash flow. The free cash flow is the amount of money that was generated by a company's ordinary operations and is left over after it pays all of its bills and makes all necessary capital expenditures. This is therefore the amount that is available for tasks that benefit the shareholders such as reducing debt, buying back stock, or paying a dividend. During the twelve-month period that ended on March 31, 2023, Entergy Corporation reported a negative levered free cash flow of $2.8959 billion, which is obviously not enough for the company to be able to pay out any dividends. Nevertheless, it actually paid out $862.8 million to its shareholders during the period. At first glance, this is likely to be concerning as the company had nowhere close to enough free cash flow to cover its dividends.

However, it is common for a utility to finance its capital expenditures through the issuance of debt and equity. It will then pay its dividends out of operating cash flow. This is necessary because otherwise, the incredibly high costs involved in constructing and maintaining utility-grade infrastructure over a wide geographic area would prohibit the company from ever providing a return to its investors. During the twelve-month period that ended on March 31, 2023, Entergy reported an operating cash flow of $3.0071 billion. That was easily enough to cover the $862.8 million that the company paid out in dividends as well as provide it with a substantial amount of money for other purposes. Thus, it does appear that Entergy's dividend is sustainable and investors should not need to worry about a dividend cut in the near future.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a utility like Entergy, we can value it by looking at the price-to-earnings growth ratio. This is a modified version of the familiar price-to-earnings ratio that takes a company's earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that the stock may be undervalued relative to its forward earnings per share growth and vice versa. However, there are very few companies that have such undervaluation in today's fairly hot market. As such, the best way to use this ratio today is to compare Entergy's valuation to that of its peers in order to determine which company looks the best relatively speaking.

According to Zacks Investment Research , Entergy Corporation will grow its earnings per share at a 5.69% rate over the next three to five years. This gives the company a price-to-earnings growth ratio of 2.57 at the current stock price. Here is how that compares to some of the company's peers:

| Company |

| PEG Ratio |

| Entergy Corporation |

| 2.57 |

| DTE Energy |

| 2.96 |

| Eversource Energy |

| 2.56 |

| CMS Energy |

| 2.55 |

| Exelon Corporation |

| 2.60 |

Here we can see that Entergy Corporation appears to be fairly valued relative to its peers, with the notable exception of DTE Energy. However, DTE Energy tends to always be fairly expensive compared to the rest of the sector. I will admit that I would have hoped that Entergy would be cheaper than its peers considering the steep share price decline that it has experienced lately and the comparatively high debt load, but that does not appear to be the case. It may be best to wait for a better time to buy in, as there are a few reasons why this company should be trading at a discount to its peers. The current valuation is more attractive than we have seen in a while though, so I cannot blame anyone for purchasing shares today.

Conclusion

In conclusion, Entergy Corporation is a large regulated utility that operates in the Gulf Coast and has a surprisingly strong focus on green energy. The stock price has gotten battered in recent months, which has provided an opportunity to buy in and get a very high dividend yield. However, the current valuation does not really appear to be much better than its peers despite the company's fairly high relative debt load. The current opportunity here is as good as we have seen in several months, though.

For further details see:

Entergy Corporation: Stock Punished, But Not Underpriced Compared To Peers