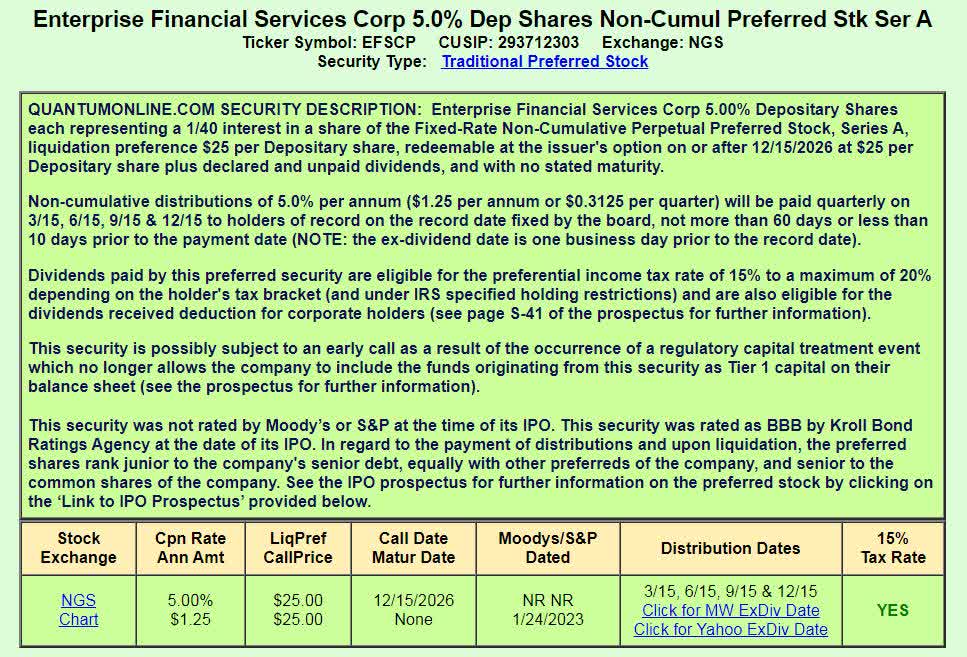

EFSCP - Enterprise Financial Services: Curtail Risk With 7.6% Yielding Preferred Shares

2023-05-01 14:44:10 ET

Summary

- Enterprise Financial Services is the parent company of Enterprise Bank & Trust.

- The bank reported first quarter earnings last week.

- The bank outperformed its sector in loan growth and deposit growth.

- Risks are present but are likely to impact the value of the common shares.

Enterprise Financial Services Corp ( EFSC ) is the parent company of a bank that operates throughout the Midwest and southwestern United States. Following the failures of SVB and Signature Bank, regional bank shares broadly sold off, including the preferred share offering of Enterprise Financial ( EFSCP ). Enterprise's preferred shares are now paying income yielding over 7.6%, and based on recent earnings, I believe the preferred shares are a good pick for income investors.

{kind=link}

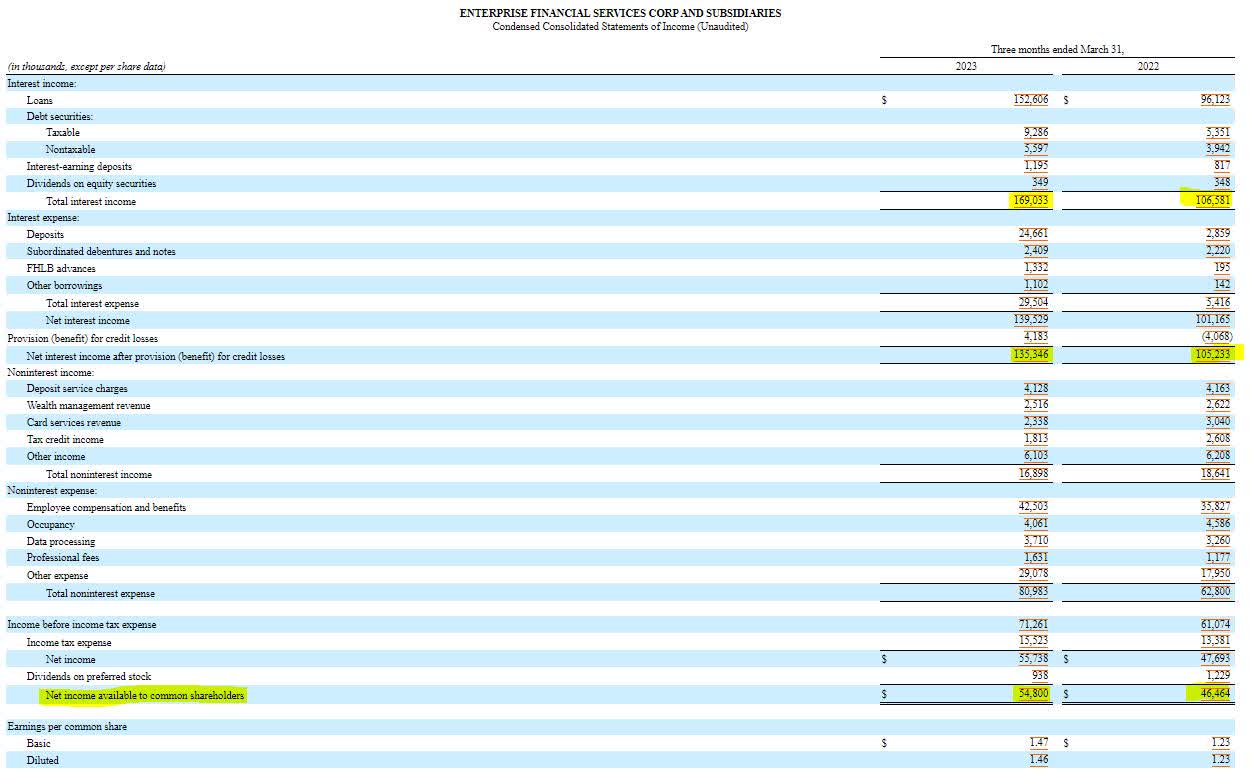

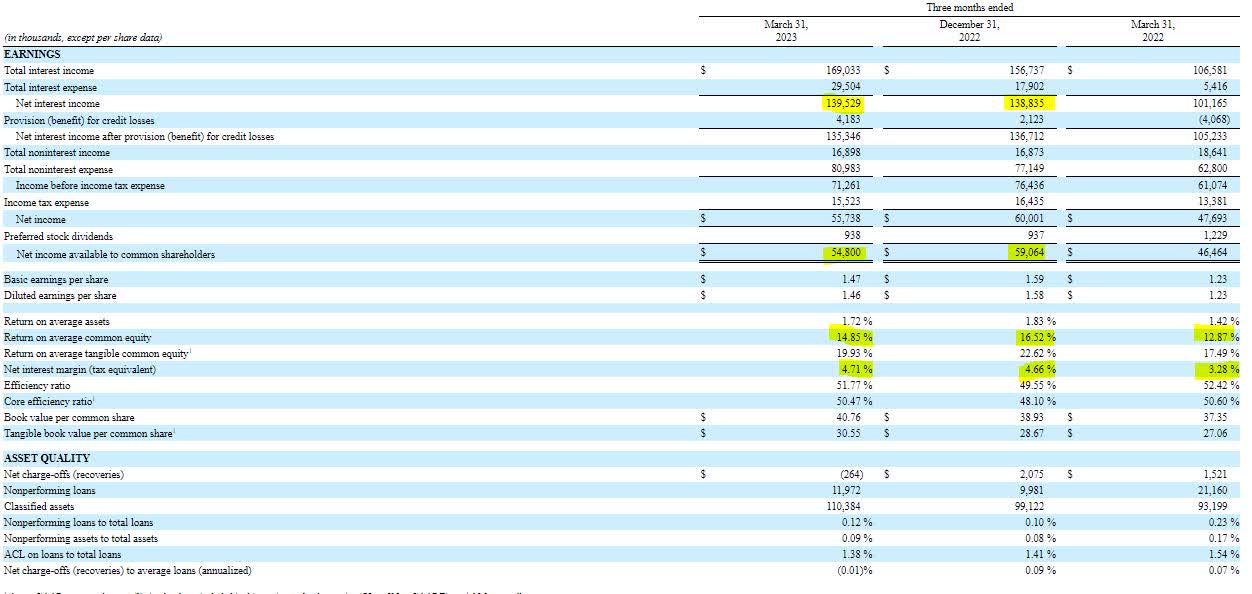

Despite the unprecedented rise in interest rates over the last year, Enterprise Financial has managed to grow earnings. Interest income in the first quarter was $169 million, 60% higher than the same quarter a year ago. Interest expenses grew by less than income, therefore the net interest margin grew by $30 million to $135 million. Despite the increase in fixed expenses, the bank's net income outpaced last year's by nearly 20% at $54.8 million. Enterprise Financial's net interest margin continued increasing to 4.71% in the first quarter, outpacing the same quarter a year ago, and the fourth quarter of 2022.

{kind=link}

{kind=link}

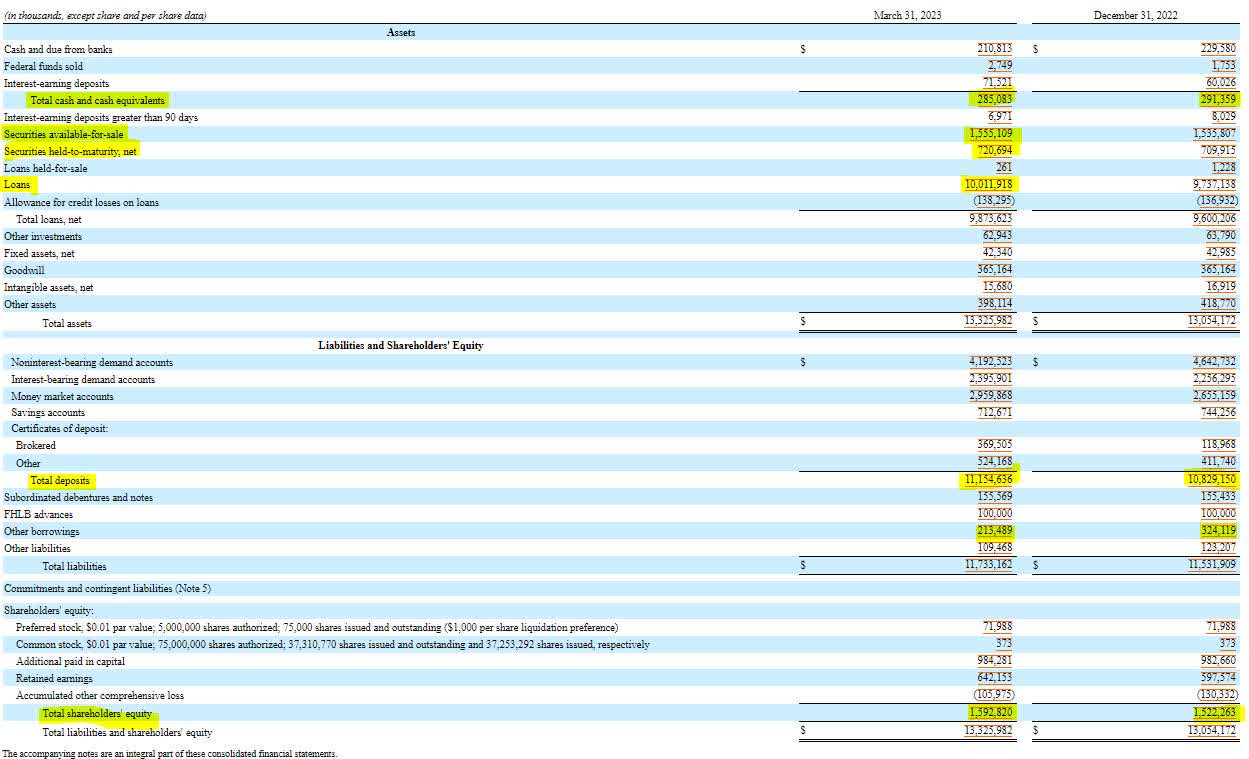

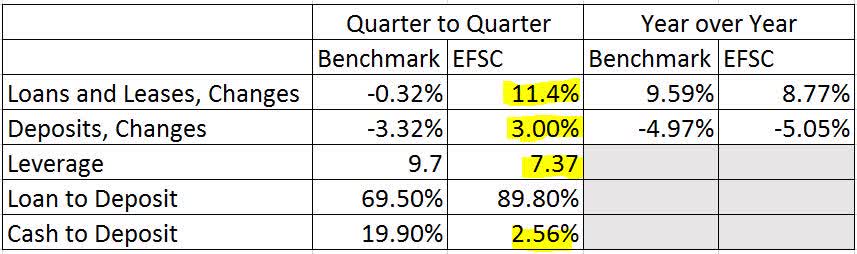

Like many smaller banks, Enterprise Financial's balance sheet consists of mostly loans on the asset side and deposits on the liability side. Enterprise Financial did grow loans in the first quarter by more than $250 million. The 11% growth in loans bucked the trend of flat loan growth in the banking system. Enterprise Financial also grew deposits by 3% or more than $300 million, which also bucked the sector trend of a 3% decline. The bank's leverage ratio was also impressive at 7.4 to 1, well below the industry average of nearly 10 to 1.

{kind=link}

{kind=link}

Another important statistic to monitor with smaller banks is the amount of uninsured deposits, which measures the bank's susceptibility to a run. In what may be its most impressive feat of the first quarter, Enterprise Financial grew its insured deposits from $4.9 billion to $7.7 billion. The bank used reciprocal deposits and pass-through insurance to accomplish this success. The $3.4 billion in uninsured deposits can be covered by nearly $4.4 billion in borrowing capacity the bank has should it need additional cash on hand.

{kind=link}

{kind=link}

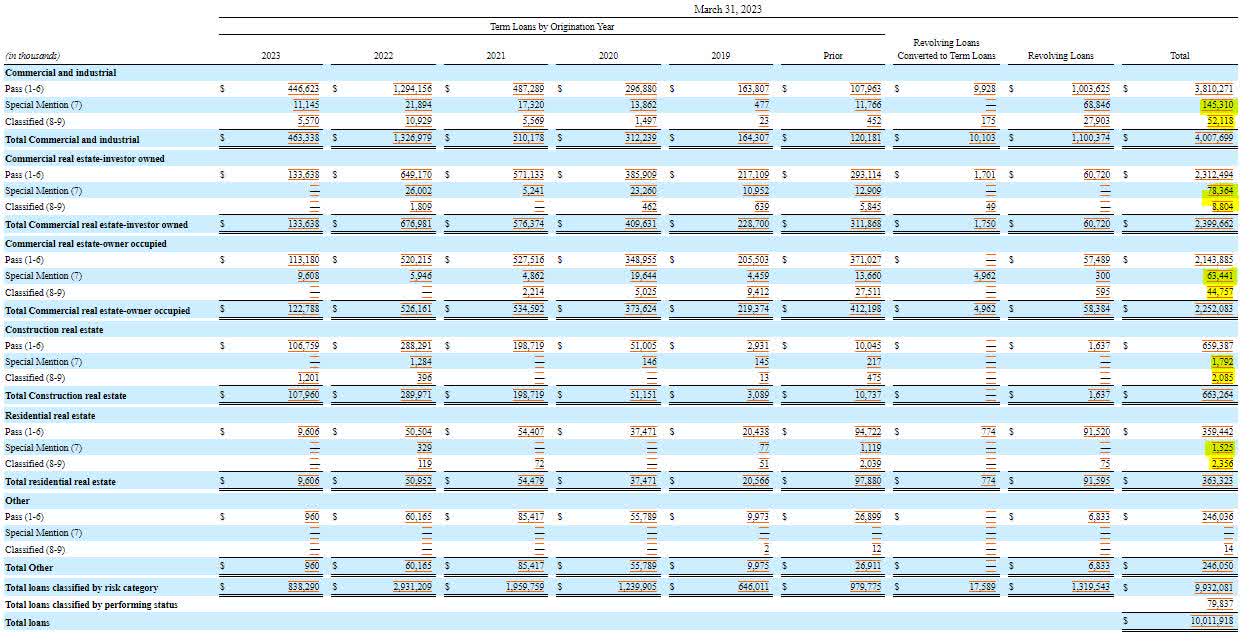

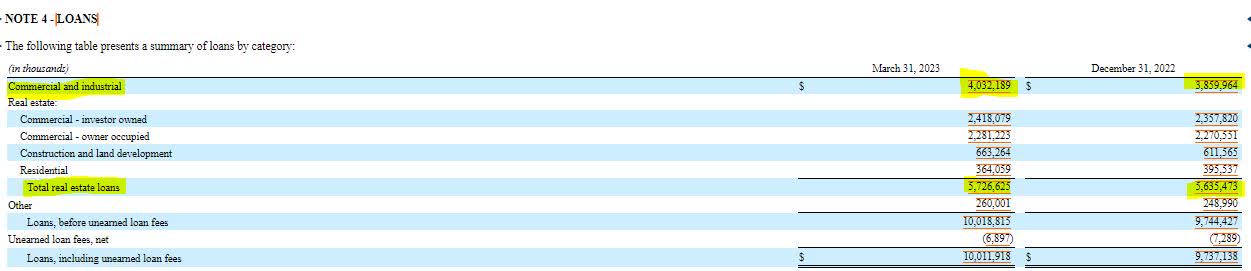

Enterprise Financial's loans are mostly commercial in nature, with residential real estate comprising less than 4% of the company's total portfolio. Problems with commercial real estate or corporate earnings, in general, could put the bank at risk of taking large losses. So far, approximately 4% of the bank's loans have not received a passing grade, based on its own internal metrics.

{kind=link}

{kind=link}

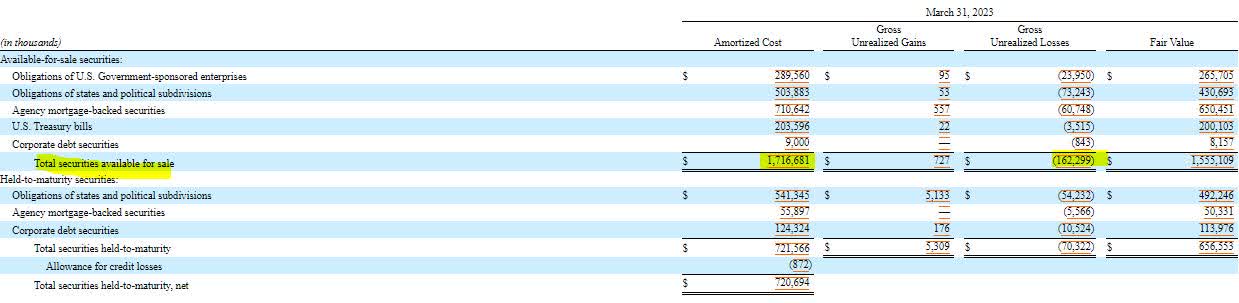

Enterprise Financial also faces the risk of either unrealized losses or capital erosion should it face the need to raise additional cash. Under a scenario where the bank would need cash, the bank would either sell securities and take a loss or borrow from its unused lines of credit, where the interest rate would erode equity. Either way, the bank needing to raise cash would be detrimental to the common equity, which is why I prefer the preferred shares.

{kind=link}

Enterprise Financial's commercial real estate and unrealized loss risk are the two reasons why I am avoiding the common shares. The bank's preferred shares rank senior to the common shares, offer a 7.6% dividend yield, and are not callable until December 2026. The fear discount incurred across the sector provides a good entry point for income investors.

For further details see:

Enterprise Financial Services: Curtail Risk With 7.6% Yielding Preferred Shares