SBUX - Enterprise Products Partners: Stable Income In A Rocky Environment

2023-09-12 13:00:00 ET

Summary

- EPD is a dividend aristocrat that offers investors a safe, and stable income stream.

- Because of this, the MLP is fairly valued and investors should wait for any signs of share price weakness to add a position.

- EPD is the only stock that has an A credit rating that offers a >7% yield.

- EPD had $4 billion in liquidity at the end of Q2 and no debt maturities remaining in 2023.

- EPD has grown its net income by 32% over the last 5 years and free cash flow by 219% during the same period.

Introduction

Enterprise Products Partners ( EPD ) in my opinion is probably one of the safest stocks on the planet right now. I don't say that about many. And while I don't hold them in my portfolio, I used to. I actually sold them last year and allocated the funds into other dividend paying stocks. Just because someone sells a stock doesn't always mean it was a bad investment. And I can say EPD was definitely not. But I sold and sometimes I look back and say, "Maybe I should have kept them." Especially now since there is so much uncertainty surrounding the market. Many REITs are seeing new 52-week lows while some dividend stocks are flourishing, like a few BDCs.

I view my dividend stocks differently than other investors. I don't just view them as stocks that pay dividends. Some I consider dividend stabilizers (slow & steady growth), some dividend showers (stable dividend; little to no growth), and dividend growers (medium to high growth). I think every investor should consider using this strategy. This keeps me disciplined and helps manage my expectations. For example, Starwood Property Trust ( STWD ) is a dividend shower not a grower . Anyone who holds this stock should not expect dividend growth. No special, no increase, just a steady dividend that hasn't changed since 2014. If they do decide to raise that's great but should not be expected with their track record.

One stock I consider a grower is Starbucks ( SBUX ). One with a low dividend yield but double-digit dividend growth over the last 5 & 10 years. But EPD is a combination of both, a grower and a shower, and dividend investors should consider this aristocrat for their portfolio.

Why EPD?

One thing I like about EPD is their predictability. Like I mentioned earlier, I held the stock for a few years before selling. In my observation they typically trade in a range of $23 to $27. So this tells me they're stable. And who doesn't want something stable especially with so much uncertainty in the economy right now. Several stocks have seen their prices drop over these last few months, REITs especially. And with another rate hike expected, there could be more rockiness in the market in the coming months.

Stocks usually see their prices drop towards the end of the year as many investors cut their losses to offset their gains. In other words, tax-loss harvesting. I'm not complaining though. This is normally my favorite time of the year. I can pick up some quality stocks for a cheaper price. That way I can get a little price appreciation while also collecting a dividend. And EPD has been growing theirs for 25 years which is not common in the midstream industry. So I think this speaks volumes for EPD.

Rock-Solid Dividend

As my name states I collect dividends. So this is the first thing I look for when investing. Does it offer a nice dividend and is it safe? EPD has 25 years of growth so I would say that's a pretty safe dividend. And I know readers are going to say they don't pay dividends, they pay distributions, there's a difference! I'm well aware. Below you can see the dividend growth trajectory of EPD. Additionally, they raised their dividend in July by 2% for a total annual payout of $2.00.

{kind=link}

Stock analysis

One thing to note for investors. Because EPD is a Master Limited Partnership it does issue a K-1 form. I used to read about these all the time. Mainly how investors didn't like dealing with them during tax season. To be honest it wasn't that bad. It's a little different than a 1099 form but I didn't find it too troubling. And for those who don't want to deal with it, you can easily pay a tax professional to do it for you. One thing I did notice is that the form did seem to come later than say a W-2 or 1099. So if you're one of those people who like to file your taxes right away, just expect a delay of a month to a month and a half.

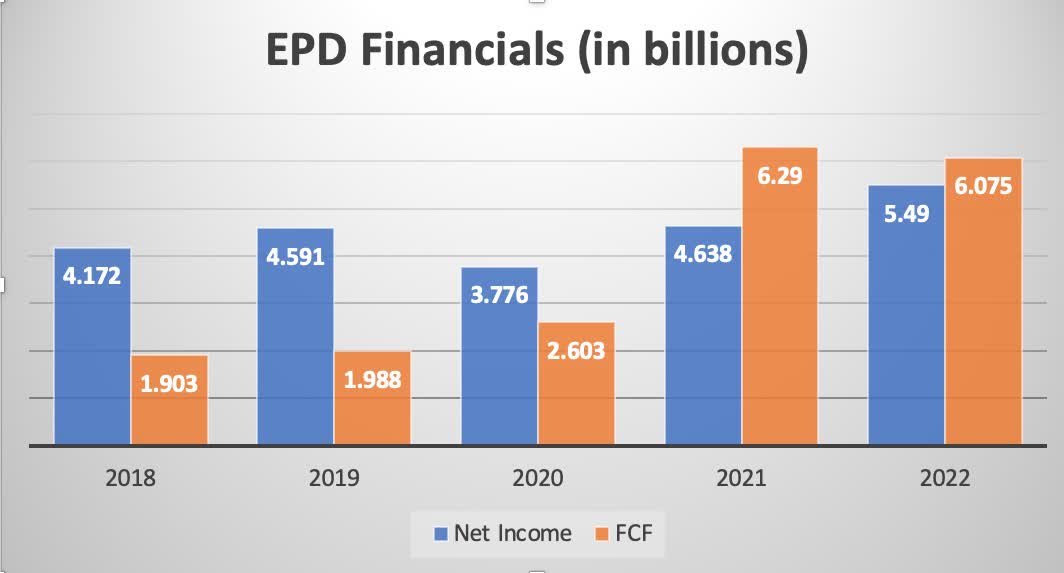

Growing Net Income & Cash Flows

Although growing dividends are great, if the income and cash flows aren't growing as well, the dividend will not be sustainable. One thing I like when researching is a beautiful financial chart. I always imagine the stairway to heaven. Going up and to the right. And EPD has just that. I like to look at minimum 5 years' worth of financials and pay special attention to times of economic downturn. I'm sure many investors do the same, especially with dividend stocks. How a company did during a time of crisis can tell a story about not only the company's strength & resilience, but a lot about the management team. Below is EPD's net income & free cash flow growth since 2018.

{kind=link}

Author creation

Aside from 2020, EPD grew its net income every year for the last 5 years and free cash flow with the exception of last year. Their net income grew almost 32% while their FCF grew a whopping 219% during the same period. One thing to note, the company's net income and adjusted cash from operations did decline slightly year-over-year to $1.3 billion from $1.4 billion, and $1.9 billion from $2.1 billion. Every company will face headwinds no matter the sector, as no business is without risk.

But there isn't much to not like about EPD. A growing dividend, steady income & cash flows, and a company that rewards shareholders with buybacks. During Q2 earnings management announced they had completed 41% of their $2 billion share buyback program. CAPEX is also expected to range from $2.4 to $2.8 billion, lower than the last 8 years with the exception of the last 2 (years). With $4.1 billion of major growth projects under construction and lower capital expenditures, I expect continued growth in net income and FCF over the next several years.

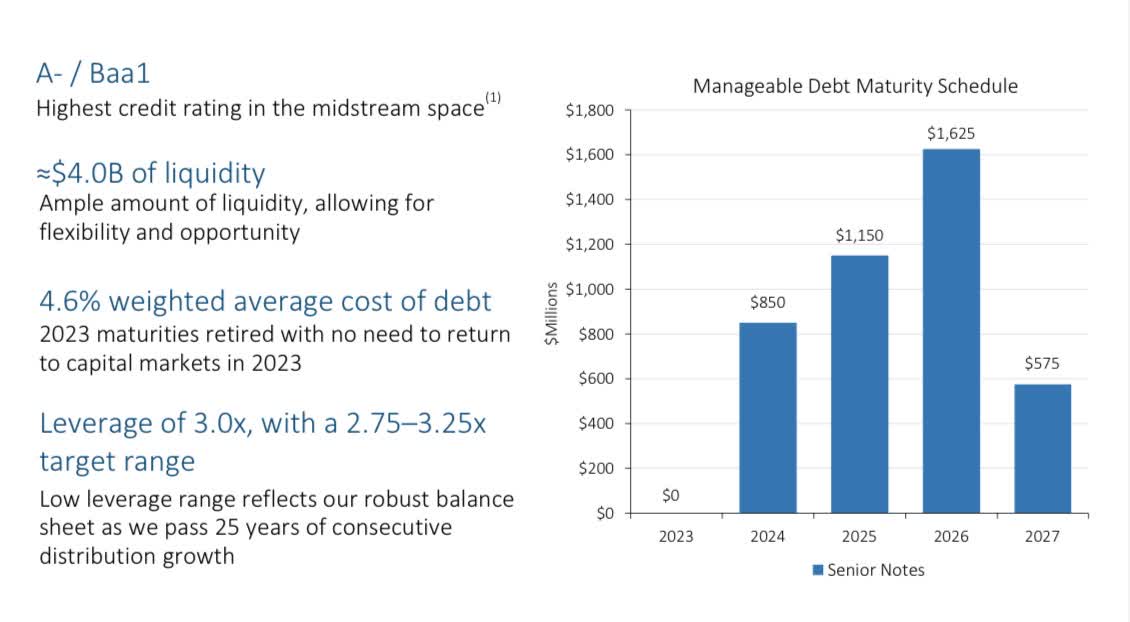

Conservative Balance Sheet

At quarter-end the company had $4 billion in liquidity and $28.9 billion in debt. Their debt had a weighted average cost of 4.6% with 97% being fixed rate. They also managed to increase adjusted EBITDA by almost 3.5% to $9.1 million from $8.8 million YOY and by 8.4% since 2017. Did I also mention they're the only A rated company with a >7% yield and the highest credit rating in the midstream space? I don't know how readers/investors feel about that but that's pretty impressive.

To be honest EPD does everything right. When researching companies I pay close attention to outliers. It's like looking at reviews for your favorite restaurant, we all go to the negative reviews first to see what customers said. EPD has $850 million in senior notes due next year but with their liquidity of $4 billion available under their credit facilities and unrestricted cash this is an insignificant amount. I know the FED has stated higher for longer rates and some are saying no cuts until 2025, but I think we'll see our first cut in 2H 2024. Again that's my opinion. But even if we didn't EPD has no worries.

{kind=link}

EPD investor presentation

Valuation

EPD's dividend yield and P/DCF both trade in-line with their 5-year average. As I stated earlier EPD normally trades in a range between $23-$27. At its current price of $26.70 at the time of writing, EPD is fairly valued. This is less than $1 from their 52-week high of $27.28. The company offers a yield higher than the average money market or bond right now at 7.32%, and it's also one of the safest companies on the planet. And although it does offer some upside to its price target, I like the stock under $24.

If you have a long-term outlook I don't think EPD is a bad buy right now. But investors should be aware that September & October are historically the worst months for stocks so a price decline could be in the works. Some of this has to do with tax-loss harvesting. EPD is a low-growth stable company that deserves a spot in every investor's dividend portfolio. Using a desired annual return of 12.5% and a historical P/FCF average, I have a 1-year price target of $30.

{kind=link}

Tipranks

Outlook

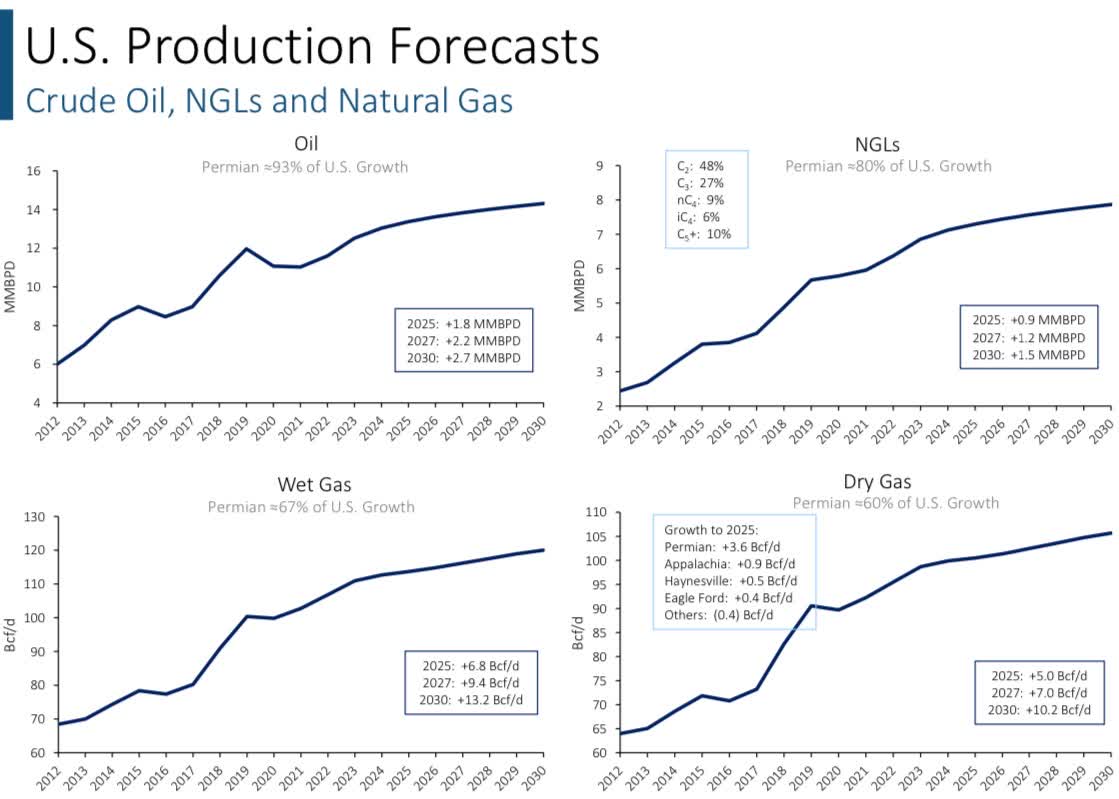

Billionaire Lee Cooperman talked positively about the midstream industry earlier this month. One reason is surging oil prices. And most of us know oil impacts the price of gas. I've noticed this over the last month as gas in California is now close to $6 a gallon. A few months ago it was around $5. Cooperman also stated he thinks a recession is still on the horizon because of this. I agree and high oil prices may be the final piece that pushes the economy into a recession.

But oil prices could also be a catalyst for EPD as 96% of manufactured goods are touched by oil & gas through petrochemicals. As you can see below crude oil, NGLs, and related liquids are expected to continue growing over the next several years. With 3 additional natural gas processing plants expected to go into service late '23 and early '24, EPD will continue to benefit from this growth.

{kind=link}

EPD investor presentation

Takeaway

EPD is a great investment for those looking for long-term, stable income. With the expected growth in the midstream industry, EPD will continue to be a top performer in the space. The company is one of the best in the business as seen by their consistent growth and conservative balance sheet. As the price of oil surges, EPD will benefit in the 2H of '23 and investors can most likely expect an increase in earnings.

Due to economic uncertainty and an A- credit rating combined with a 7.32% dividend yield, I believe this has pushed the stock into fair valued territory as it offers a safe, and stable income stream. Because of this investors should wait for a pullback in price before adding. If you have a longer-term outlook on the stock, this may be a good price to add as the stock normally trades within a tight range. Because of this I rate EPD a hold.

For further details see:

Enterprise Products Partners: Stable Income In A Rocky Environment