NVST - Envista: Current Valuations Don't Fully Reflect Growth Potential

2023-04-20 08:49:44 ET

Summary

- Envista is valued by the market at a discount to its peers based on the EV/EBITDA multiple, although its revenue and earnings growth prospects are comparable to that of peers.

- NVST has both organic and inorganic growth drivers in place to support its long term financial targets.

- I am rating Envista's stock as a Buy, as NVST's current valuations aren't reflective of the company's faster top line expansion and profit margin improvement in the long run.

Elevator Pitch

My investment rating for Envista Holdings Corporation's ( NVST ) shares is a Buy. NVST is trading at a lower EV/EBITDA multiple as compared to the company's peers, even though Envista's growth outlook is as good, if not better, than its peers. I believe that the mispricing of NVST's shares won't continue forever, and the stock should eventually re-rate when the company delivers on its long term financial targets by leveraging on both organic and inorganic growth drivers.

Company Overview

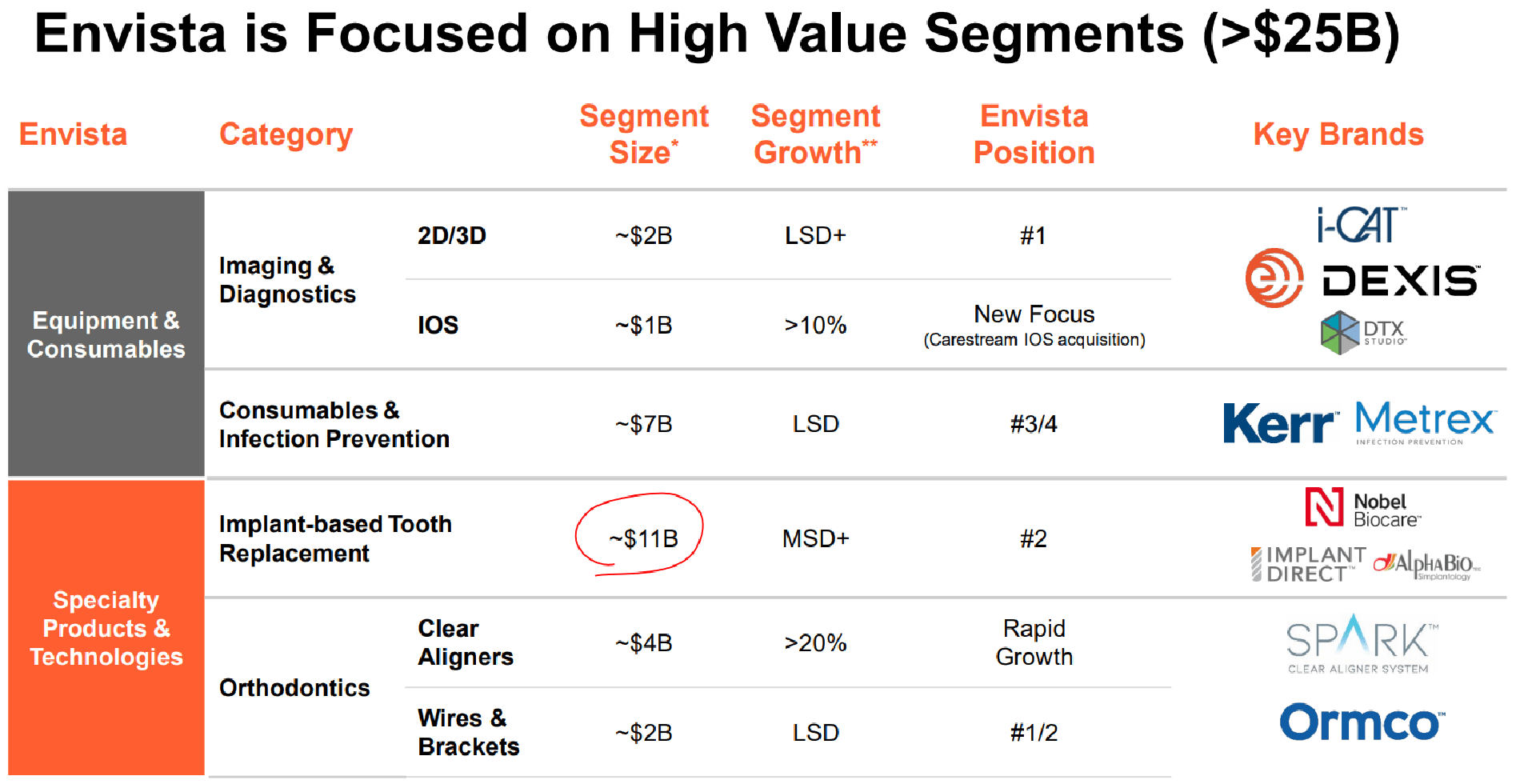

Envista describes itself as a provider of "industry-leading dental consumables, solutions, technology, and services" in the company's media releases .

The Key Dental Segments Which Envista Operates In

{kind=link}

NVST's 2022 Investor Day Presentation

NVST generated 62% and 38% of the company's full year fiscal 2022 sales from the Specialty Products & Technologies and Equipment & Consumables business segments, respectively as disclosed in its 10-K filing . With respect to geographic exposure, North America is Envista's largest market which contributed 53% of the company's FY 2022 top line. The Emerging Markets, Western Europe, and Other Developed Markets geographic regions accounted for 22%, 20%, and 5% of NVST's revenue, respectively in the most recent fiscal year.

A Comparison Of NVST's Long Term Financial Targets With Its Valuations

At the company's 2022 Investor Day on April 1 last year, Envista outlined its financial goals of top line growth acceleration and operating margin expansion for the next five years.

In terms of the top line, NVST is targeting to achieve a more rapid pace of revenue expansion in the next few years. Envista's revenue grew by +2.4% in FY 2022, and the company wants to deliver annual sales growth at the mid-single to high-single digit percentage level between 2023 and 2026. With regards to operating profitability, Envista's goal is to improve the company's EBITDA margin from 20.1% for FY 2022 to 22.5% in FY 2026. NVST's revenue growth and EBITDA margin targets translate into an earnings per share or EPS CAGR goal of above +10% for the long run.

Peer Valuation Comparison For Envista

| Stock |

| Consensus Forward Next Twelve Months' EV/EBITDA Multiple |

| Expected FY 2023-2026 Revenue CAGR Estimate |

| Expected Forward FY 2023-2026 Normalized EPS CAGR Estimate |

| Envista |

| 13.3 |

| High Single-Digit Percentage (Source: company's targets) |

| Higher Than 10% (Source: company's targets) |

| DENTSPLY SIRONA Inc. ( XRAY ) |

| 14.4 |

| +6.4% (Source: sell-side's consensus forecasts) |

| +9.5% (Source: sell-side's consensus forecasts) |

| Zimmer Biomet Holdings, Inc. ( ZBH ) |

| 14.6 |

| +3.8% (Source: sell-side's consensus forecasts) |

| +6.0% (Source: sell-side's consensus forecasts) |

Source: S&P Capital IQ

As indicated in the peer comparison table presented above, NVST is currently trading at a discount to the company's listed peers based on the forward EV/EBITDA metric, even though Envista's expected top line and bottom line growth rates are on par or even better than its peers.

In other words, Envista's current valuation multiples should expand over time to narrow the gap with its peers, assuming that the company can deliver on its financial targets for the long run. I explain why I am confident that NVST can meet the company's long term goals in the next section of the article.

Organic And Inorganic Growth Drivers For Envista

I see both organic and inorganic growth drivers which should help NVST attain its long term financial targets.

The orthodontics segment is one with strong organic growth potential.

As disclosed at the company's 2022 Investor Day, Envista's wires & brackets business is already among the top two leading players in this space globally. Looking ahead, NVST's wires & brackets business should continue to take share from smaller competitors with its Damon Ultima system first introduced in mid 2021 which has appealing features highlighted below.

The Merits Of NVST's New Damon Ultima System First Launched In The Middle Of 2021

{kind=link}

NVST's 2022 Investor Day Presentation

Another driver of the orthodontics segment is NVST's Spark clear aligner product. Clear aligners are a new, growing market for Envista with an estimated addressable market ($4 billion) that is twice that of wires & brackets as per NVST's internal forecasts. NVST disclosed at its Q4 2022 results call in early February this year that the number of doctors who are using Spark clear aligners grew by almost +100% last year. This supports the company's guidance of tripling of its Spark clear aligner sales for the 2021-2024 period.

The Key Features Of Envista's Spark Clear Aligners

{kind=link}

NVST's 2022 Investor Day Presentation

Separately, inorganic growth remains an important pillar of Envista's corporate strategy. In its FY 2022 10-K filing, NVST stressed that the company got to where it is today with "the acquisition and integration of over 25 leading dental businesses and brands" in a decade and a half.

Using the purchase of Carestream Dental's intra-oral scanner business last year as an example, acquisitions can help to expand NVST's addressable market and expand its overall profit margins. Envista indicated in its 2022 Investor Day presentation that the size of the global intra-oral scanner market is around $1 billion and growing at the teens percentage level every year. Furthermore, Carestream Dental's intra-oral scanner business boasts EBITDA margins of more than 30%. This implies that NVST has entered a new market with superior growth prospects (intra-oral scanner market is growing faster than Envista's top line), and taking over a business which is more profitable than the company as a whole in terms of EBITDA margins.

It is realistic to assume that Envista will have an eye on similar acquisition opportunities which could increase the proportion of faster growing businesses with higher margins as part of its overall revenue mix. At the Envista Summit investor event held on February 24, 2023, NVST specifically referred to acquisitions as a "lever to manage the portfolio" where "we are under-indexed or is changing rapidly" and "expanding our presence in different geographies."

Closing Thoughts

I think that NVST's shares are undervalued compared to its listed peers and this is based on a comparison of its valuations and growth outlook. This explains my Buy rating for Envista.

For further details see:

Envista: Current Valuations Don't Fully Reflect Growth Potential