SRE - EOG: Getting Gassier Expect Lower Income This Year

2023-05-03 11:21:17 ET

Summary

- EOG's production profile is turning gassier, and now, the price of oil is dropping. I downgrade EOG from hold to sell.

- Inflation in the oil services sector will significantly impact EOG this year, as its large shale production profile means more drilling just to keep production flat.

- I'm much more positive on EOG's prospects in 2024, once additional U.S. LNG export capacity comes online and firms up the domestic price of natural gas.

- EOG is scheduled to release Q1 results before the market opens on Friday. That being the case, today, I'll also review current consensus EPS estimates.

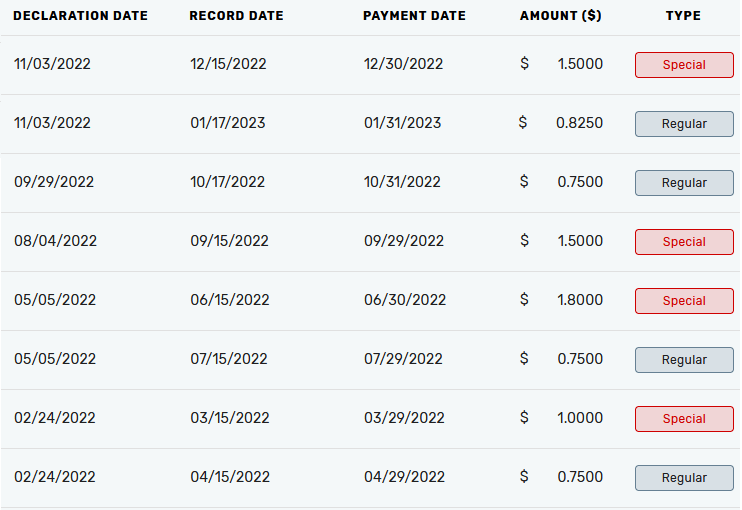

EOG Resources ( EOG ) was one of the first shale O&G producers to focus on capital efficiency and shareholder returns. Indeed, the company has an impressive (base+special) dividend record going back to 2021. Last year, EOG returned an impressive total of $8.875/share in aggregate dividends to shareholders (see graphic below). That currently equates to a 7.93% yield after the stock's swoon today (Tuesday, May 2) on the market sell-off and an even weaker energy sector: The SPDR Energy ETF ( XLE ) is currently -4.2% while the Vanguard S&P 500 ETF ( VOO ) is down only 1.2%. Meantime, it's important to acknowledge that EOG's quarterly base dividend is currently $0.825 ($3.30/share on an annual basis) and that the majority of dividends last year (~65%) came from special dividends. Considering the recent swoon in the price of oil - and especially the weakness in natural gas due to still high production and storage levels - EOG shareholders should prepare themselves for significantly less income this year. Indeed, the special dividend declared in February was $1.00, down 50% from the $1.50 declared in the previous quarter. In addition, EOG is facing a rising GOR (gas-to-oil ratio) and appears to be dealing with some relatively high oil service cost inflation, which could put additional downward pressure on dividends this year.

{kind=link}

Recent Developments

EOG's Q4 report was released on Feb. 23 and non-GAAP EPS of $3.30 missed estimates by $0.10 . However, what raised my eyebrows was that EOG announced a $6.0 billion capital plan which is expected to grow oil production by 3% and total production by 9%. That's a big year-over-year jump in capex (FY2022's cap-ex was $4.6 billion) while EOG's production mix will be getting even gassier going forward, a trend that was already taking place.

Indeed, in Q4, oil production averaged 465,600 bpd out of total production of 909,100 boe/d, or roughly 51%. That compares to a 53.7% oil-to-gas split for full-year 2021. That is, EOG's oil split is falling (or, alternately, the GOR is rising). This is caused primarily by two developments: First, and on a mid- to long-term basis, EOG has a very large shale base production profile and - as my followers know - older shale wells get gassier over time. That's important when capex has been very disciplined and fewer new wells are being drilled - wells that typically have a relatively higher oil split over the first 12 months of production. And EOG has a lot of old shale wells. Secondly, EOG has started to put a priority on the El Dorado discovery, which is primarily a gas play. For more detail on El Dorado, see EOG Resources: Pumping Income From Oil With A Natural Gas Kicker .

In my opinion, that's not a good combination at the present time considering the bottom has fallen out of natural gas pricing (see below) due to strong and growing domestic production and - as the EIA reported last week - a massive 2 Tcf in storage, which is "525 Bcf higher than last year at this time and 365 Bcf above the five-year average of 1,644 Bcf."

MarketWatch

Meantime, EOG's NGLs volumes increased 37% last year - driven in part by increased extraction of ethane. The U.S. is currently awash in an abundance of NGLs too.

Also of note is that EOG's capex plan for 2023 jumped by $1.4 billion ($6 billion vs $4.6 billion last year) but is only expected to grow oil production by ~3%. Last year, when capex spending was 30% less than the 2023 plan, oil production grew by 3.7% (i.e., more for less ). What this tells me is that EOG is not only facing some significant inflationary increases in drilling costs (in the neighborhood of an estimated ~10% after taking into account EOG plans to run two additional rigs and drill ~80 more net new wells as compared to last year), but EOG is at the same time expecting a higher GOR (gas-to-oil ratio) on its overall production base. That's not a good combination considering additional LNG export capacity is not expected to come online until after the new year and even then EOG's gas production will likely face increasing associated gas production from Permian drillers targeting oil as well as competition from the Haynesville gas play, which also is relatively close to the Sabine Pass LNG terminal. That is, EOG is expecting to significantly increase gas production into an already very well-supplied domestic gas market.

Q1 Earnings Estimates

The following graphic is courtesy of Yahoo Finance and shows that EOG's Q1 and FY2023 EPS estimates have been steadily falling - and significantly so - over the past 90 days as the price of both natural gas and oil have weakened:

Yahoo Finance

Indeed, the current $2.48/share estimate is a large step-down from the non-GAAP EPS of $3.30/share posted in the previous quarter. Further, and as I suggested in my last article on EOG (see EOG Resources: What To Expect From Next Week's Q4 Report):

... going forward - and in consideration of the plunge in natural gas and NGLs pricing - I suspect EOG will have trouble repeating the $8.80/share in dividends paid out last year.

And even though EOG's Q4 report was a significant top-line beat , the company clearly saw weakness coming and dropped its Q1 special dividend declaration to $1.00/share versus the previous quarter's $1.50/share.

On top of all that, energy investors also have to deal with the self-inflicted debt-ceiling drama, arguably due to the Republican House not automatically increasing the U.S. debt ceiling (as it did three times during the previous administration). A U.S. debt default would likely cause a significant downturn in global economic growth, a recession in the U.S., growth in unemployment, a potential financial panic, and a big downturn in global oil demand. Those fears hit the market today with the result that WTI was down big-time (almost $4/bbl):

MarketWatch

That being the case, I suspect EOG's full-year earnings estimates will begin to move lower.

Valuation

The following chart compares the TTM P/E, Forward P/E, and annual base dividend amounts and base dividend yield of EOG and its two biggest independent E&P peers: Pioneer Natural Resources ( PXD ) and ConocoPhillips ( COP ):

| TTM P/E |

| Forward P/E |

| Annual Base Div |

| Base Div Yield |

| EOG |

| 8.44x |

| 10.00x |

| $3.30 |

| 2.96% |

| PXD |

| 7.41x |

| 10.13x |

| $5.00 |

| 2.39% |

| COP |

| 6.77x |

| 10.42x |

| $2.04 |

| 2.07% |

On an TTM basis, EOG is the highest valued of the three. Going forward all three are roughly equally valued while EOG's base dividend yield is the highest. The following chart compares the five-year total returns of the three:

Clearly, COP has been the leader, likely due to its greater exposure to international Brent based oil production as well as higher LNG prices.

Summary and Conclusion

EOG has been a tier-1 shale player since the start of the shale revolution. However, its GOR is rising, and I don't understand the company's emphasis on the El Dorado gas play at this time. Also, I can't say that I understand what appears to be a more significant uptick in oil services inflation for EOG (an estimated 10%) as compared to that being seen by other shale operators ( COP expects "low single-digit inflation vs. 2022 exit rate"). As a result, I'm downgrading EOG from hold to sell and consider COP to be better positioned here with larger exposure to higher Brent prices and better exposure to global LNG. In addition, COP has a larger gas marketing business and the deal with Sempra ( SRE ) not only gives COP an equity stake in the LNG terminal but also an outlet for its associated gas production in the Eagle Ford and Permian Basins. See COP Shifts Focus To LNG .

For further details see:

EOG: Getting Gassier, Expect Lower Income This Year