XOP - EOG Resources: Continues To Reward Shareholders Higher Oil Helps

2023-12-21 10:02:23 ET

Summary

- Oil prices are rebounding, benefiting domestic oil and gas exploration companies like EOG Resources, a possible 2024 tailwind.

- Generating $1.5 billion in free cash flow last quarter, EOG is undervalued and offers significant dividends to shareholders.

- The technical chart for EOG Resources shows some resistance and lackluster momentum, but the overall outlook is positive.

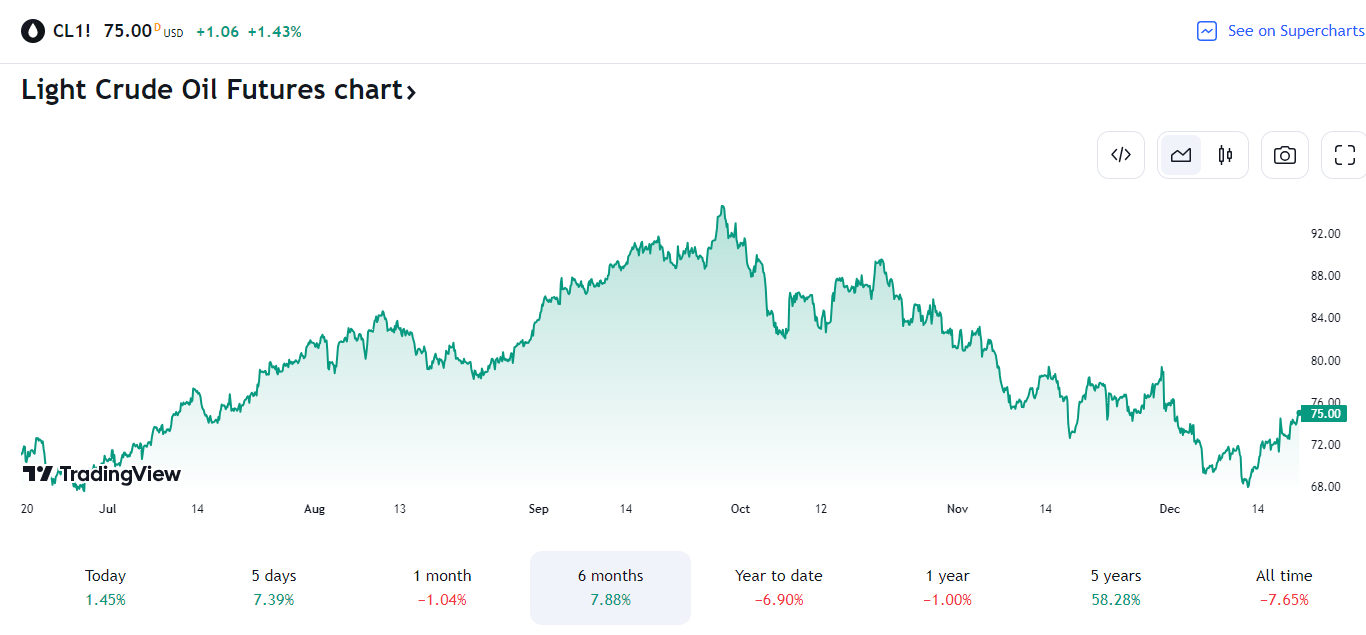

Oil prices are finally making some headway as we approach the end of 2023. WTI peaked about three months ago just shy of $100, but as geopolitical fears ebbed, the bid to oil retreated. A weaker dollar in that span, normally a tailwind, didn't provide much of a Q4 boost. Still, domestic oil prices are significantly off the lows as a new bout of global supply uncertainty makes headlines. This bullish reversal may benefit key domestic oil and gas exploration and production companies.

I have a buy rating on EOG Resources ( EOG ). I see the stock as undervalued while its management team continues to reward shareholders with significant dividends (regular and special). The technical chart, which I will detail later, still has work to do, however.

Oil Prices Bouncing Amid Rising Geopolitical Risks

{kind=link}

According to Bank of America Global Research, EOG Resources is one of the largest independent E&P companies operating in the United States. The company, together with its subsidiaries, explores for, develops, produces, and markets crude oil, and natural gas and natural gas liquids. Its principal producing areas are in New Mexico and Texas in the US; and the Republic of Trinidad and Tobago.

The Houston-based $71.5 billion market cap Oil and Gas Exploration and Production industry company within the Energy sector trades at a low 10.2 forward non-GAAP price-to-earnings ratio and pays an above-market 3.0% forward dividend yield (not including the special dividend). Ahead of earnings due out in February, shares trade with a modest, though above-market, 26% implied volatility percentage, while short interest on the stock is modest at just 1.4% as of December 19, 2023.

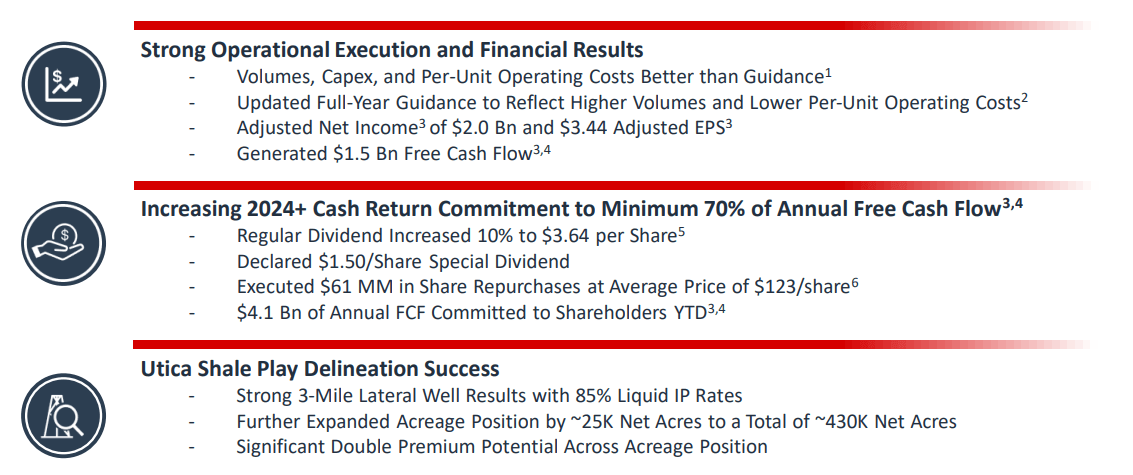

Back in November, EOG reported a strong Q3. Non-GAAP EPS of $3.44 topped analysts' estimates of $2.99 while an 18% year-on-year fall in revenue to $6.2 billion was actually a modest beat. Generating $1.5 billion of free cash flow in the period, the management team raised its quarterly dividend to $0.91 from $0.825 and, in early November, announced a $1.50 special dividend in a clear commitment to returning cash to shareholders.

Overall, EOG aims to return about 70% of free cash flow to stockholders, and the firm has a small share repurchase program. Operationally, production beat estimates at 998k boed in Q3, driven by more efficient activity in the Eagle Ford region. On the call, the management team noted flat capex spending guidance, so the cash position should continue to grow, helping the already liquid company.

3Q 2023 Results & Highlights

{kind=link}

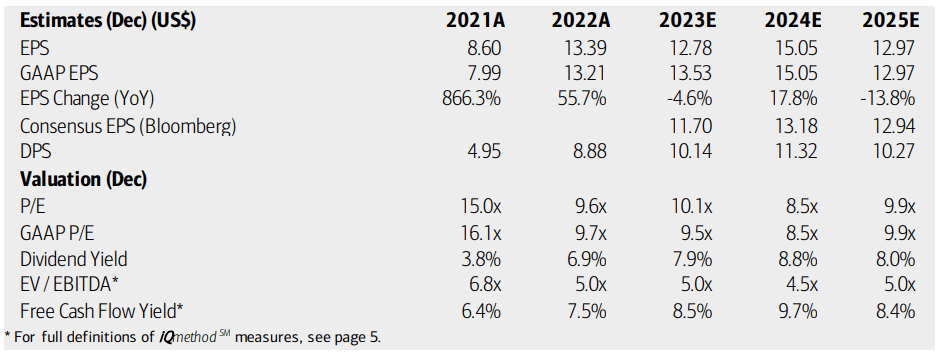

On valuation , analysts at BofA see earnings falling by about 5% this year but then snapping back with an 18% annual climb in 2024. Per-share profits are then expected to turn lower and normalize around $13 by 2025. The current consensus, per Seeking Alpha, shows operating EPS rising and holding near $13.50 with sales growth climbing 9% next year and just 4% in 2025.

Dividends, meanwhile, are expected to swing with how earnings trends progress. Still, the firm's earnings multiple appears low even with volatility in profitability ebbs and flows. Its recurring dividend , currently at $0.91, is complemented with special dividends depending on how earnings and cash flow perform. With a high free cash flow yield, in the upper single digits, I expect healthy future payouts.

EOG: Earnings, Valuation, Free Cash Flow, Dividend Yield Forecasts

{kind=link}

If we assume normalized EPS of $13.50 and apply a modest 11 multiple, well below the broad market's 20x forward P/E, then shares should be near $148. Also consider that EOG produces robust free cash flow and has a track record of prioritizing shareholder-friendly activities.

EOG: Modest Valuation Multiples

{kind=link}

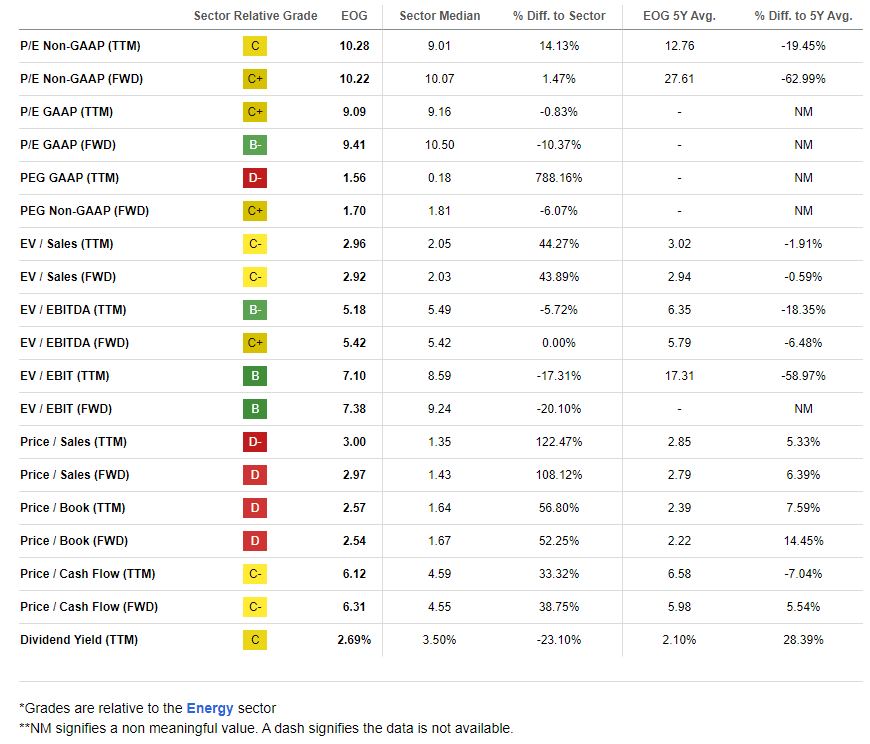

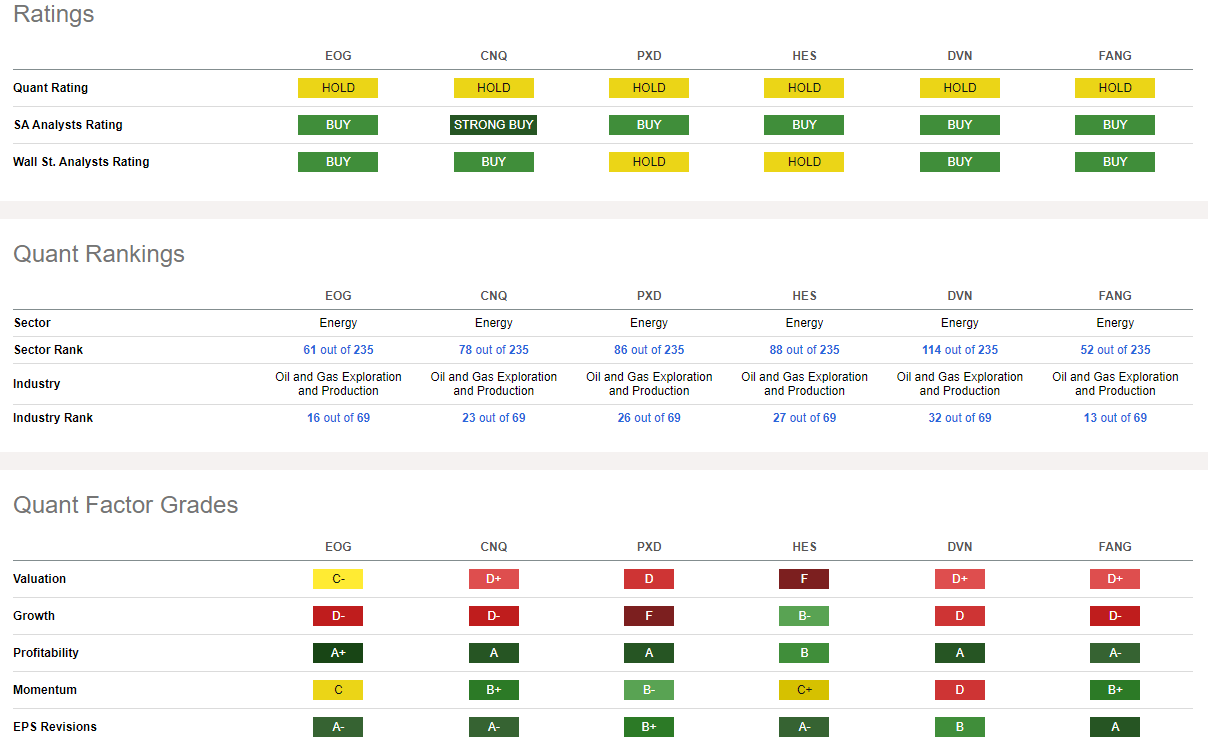

Compared to its peers , EOG features a relatively strong valuation grade, though I assert a 10x P/E multiple is too cheap. If we see oil prices continue higher, then larger cash flow can be expected. Underscoring that point, EOG sports a very strong profitability rating, the best among its peers, though uncertain growth trends amid a recent weak oil and gas market have led to poor grades there. Still, share-price momentum is not all that bad and EPS revisions are quite sanguine across the industry.

Competitor Analysis

{kind=link}

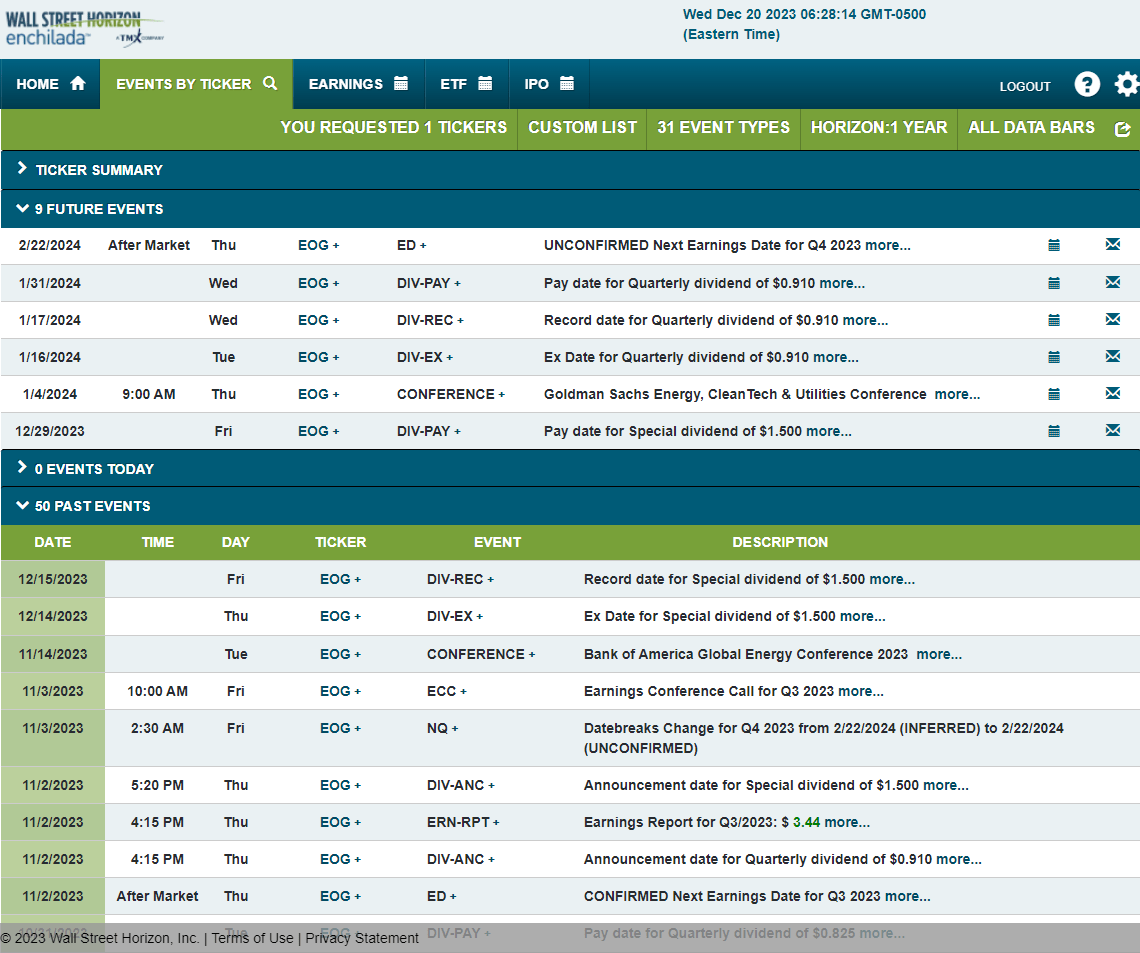

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q4 2023 earnings date of Thursday, February 20 AMC. Before that, its $1.50 special dividend will be paid to shareholders on Friday, December 29 and EOG trades ex its normal $0.91 quarterly payout on Tuesday, January 16. Be on the lookout for possible share-price volatility on January 4 and 5 as Lloyd Helms, President, and COO, is slated to speak at the Goldman Sachs Energy, CleanTech & Utilities Conference 2024.

Corporate Event Risk Calendar

{kind=link}

The Technical Take

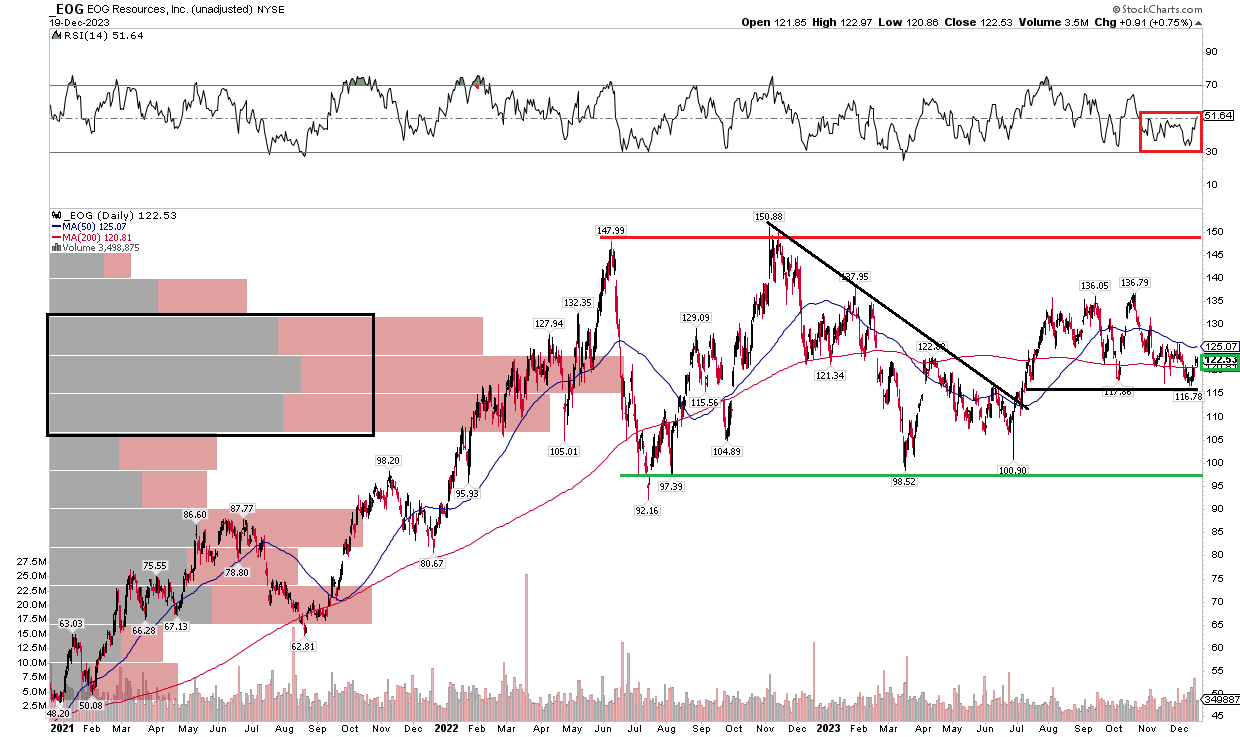

With a solid valuation and prospects for a better 2024 ahead given the bounce in oil, the chart has some work to do as far as the bulls are concerned. Notice in the graph below that shares have merely traded sideways since early last year. A broad trading range with support in the $92 to $100 area and resistance in the $148 to $151 zone has frustrated both the bulls and bears. I see near-term support near $117 - that is the breakout point from a downtrend resistance line off the Q4 2022 peak to the mid-2023 low. Moreover, a possible double bottom in the last few months has emerged there.

Bigger picture, with a long-term 200-day moving average that is flat in its slope and with an RSI momentum oscillator that is near 50, there are quite a few 'neutral' technical indicators. What's more, take a look at the volume by price construct on the left side of the graph - there is a high amount of shares traded between $105 and $130, making the current range tough sledding for the longs and shorts. I would like to see EOG rally above the $138 mark to help support the case for a rally up to the all-time highs.

Overall, EOG's chart is lackluster with no imminent signs of improving momentum.

EOG: Neutral Range Last 2 Years, $138 Resistance, $117 Support

{kind=link}

The Bottom Line

I have a buy rating on EOG. I see shares as undervalued, and if oil prices manage to rebound in 2024, the currently strong profitability picture will improve even more. Technicals, meanwhile, are not quite as sanguine but by no means are they bearish.

For further details see:

EOG Resources: Continues To Reward Shareholders, Higher Oil Helps