FRT - EPR: 8% Yield For Your Retirement

2023-11-03 02:42:46 ET

Summary

- EPR Properties has a unique portfolio in real estate investments, focusing on theaters, amusement parks, recreational facilities, and educational institutions.

- The company has successfully addressed concerns regarding its reliance on AMC theaters and has positioned itself well to adapt to industry dynamics.

- EPR offers attractive financials, including a solid top-line margin, healthy net income margin, and potential for income-focused investors with high dividend and free cash flow yields.

- We believe ERP can be rated as a buy.

Introduction

EPR Properties stands out in real estate investments due to its distinct portfolio, which includes assets like theaters, amusement parks, recreational facilities, and educational institutions. This specialized approach has allowed them to build a diversified portfolio within these niche sectors, making them an exciting choice for investors looking to diversify their real estate holdings.

In this article, we will primarily focus on their historical financials and their latest third-quarter earnings. In addition, we will briefly discuss one of the significant concerns regarding EPR's revenue sources: the AMC theaters.

The Primary Worry Is Gone

AMC Entertainment's ( AMC ) recent performance presents a notable challenge for EPR Properties (NYSE: EPR), a triple-net lease experiential REIT. In short, A triple net lease ((NNN)) is a type of rental agreement where the tenant pays for the rent and property taxes, building insurance, and maintenance costs. The landlord usually handles some or all of these expenses in regular leases. EPR Properties, previously a significant part of my investment portfolio, faced a pivotal evaluation during the summer, leading to a sell rating.

AMC's difficulties primarily influenced this evaluation in executing its preferred share conversion plan. Consequently, EPR's shares experienced a decline of approximately 9%, echoing the broader stock market's reaction to the Federal Reserve's announcement of a prolonged rate pause in September.

However, the largest US cinema chain, AMC, salvaged its preferred share conversion plan and embarked on a multi-year effort to tackle its substantial debt by increasing its share count. The injection of $325 million through the first tranche significantly fortified AMC's cash reserves, raising them by 75% by the end of the second quarter.

As a result, AMC has exhibited promising signs, including a substantial reduction in negative free cash flow during the second quarter of fiscal 2023. The anticipation of the release of movies such as Barbie and Oppenheimer, along with Taylor Swift's Eras Tour, is expected to enhance AMC's performance soon.

Companies like EPR are adapting to provide enhanced experiences in the growing consumer demand for experiential entertainment. EPR encountered challenges when both AMC and Regal Cinemas were in danger of filing for bankruptcy, but AMC's success with movies like Barbie and Oppenheimer provided temporary relief.

Nonetheless, AMC and Regal Cinemas have accumulated substantial debt since the pandemic. In response, EPR announced a restructuring agreement with a new master lease , ensuring a stable income with $65 million in annual fixed rent and built-in rent escalators.

{kind=link}

Nonetheless, uncertainties persist for EPR. You may ask yourself one question: how will EPR navigate future challenges, especially given the ongoing issues in the movie theater industry and recent events such as the writer's strike?

While short-term problems are to be expected, the strike's duration remains uncertain, even though historical strikes have ultimately reached resolutions. The future will ultimately unveil whether the moviegoing experience will revert to its previous norm, with audiences enthusiastically attending blockbuster releases on weekends.

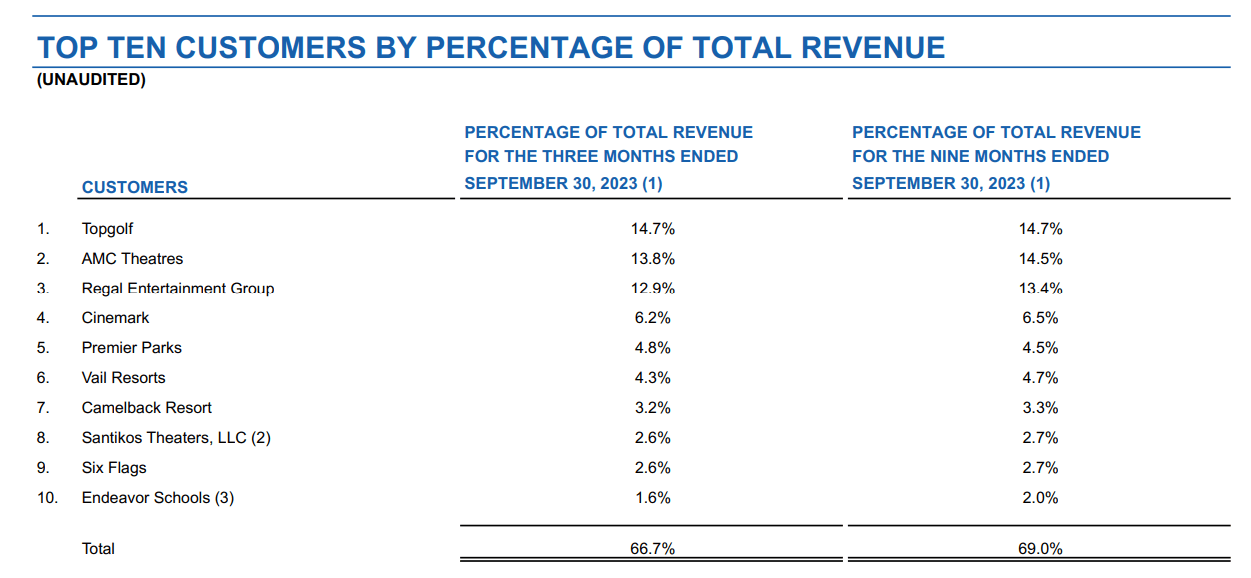

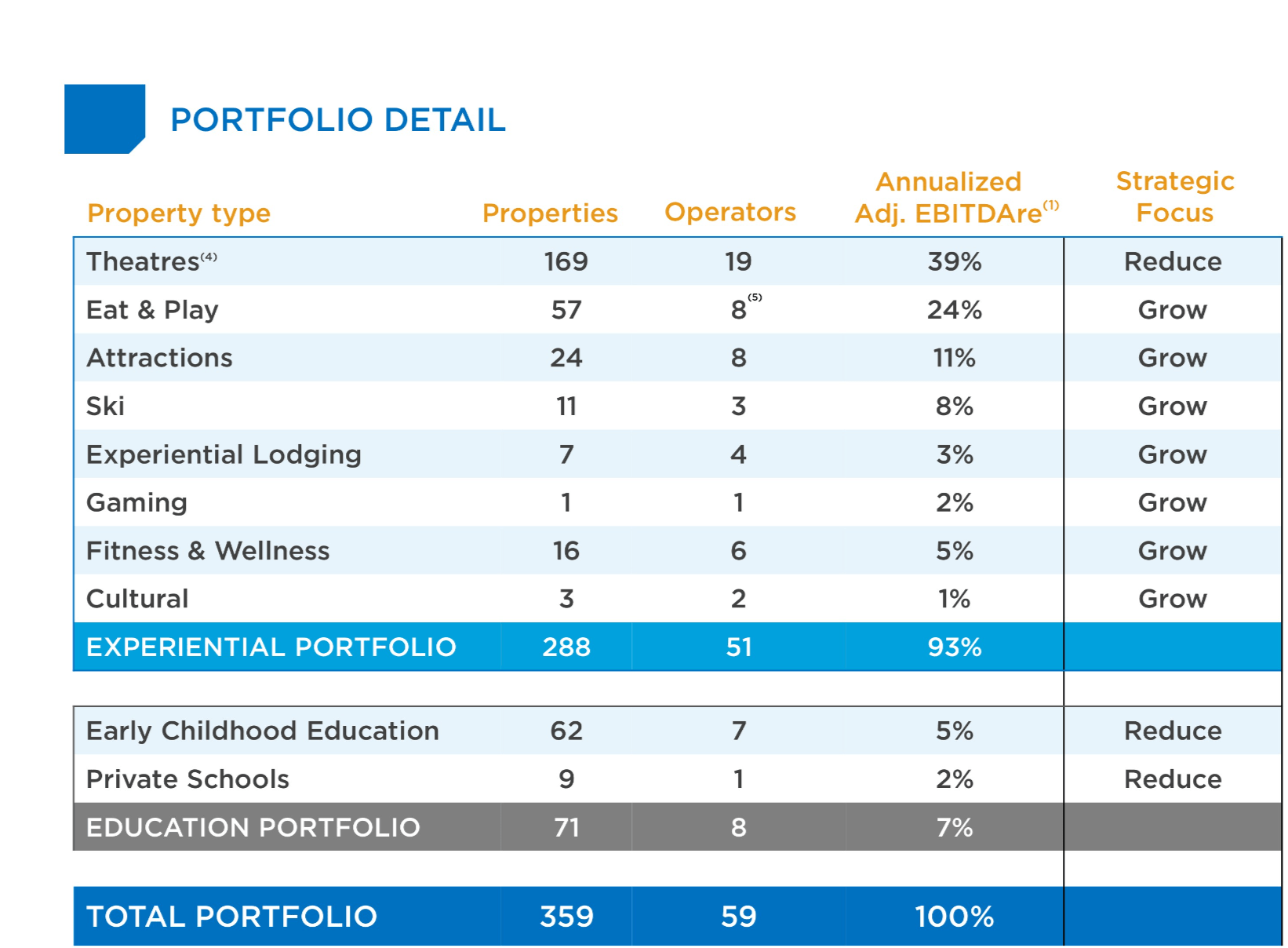

In this context, it's reasonable to harbor concerns about EPR's significant reliance on AMC theaters as a primary revenue source. It's likely that EPR's management shares these concerns, as they have made a strategic decision to reduce their exposure to theaters while increasing their presence in various other sectors.

{kind=link}

The key takeaway from their Q3 presentation is their smart move to emphasize smaller revenue streams and work on growing them. This choice reflects that movie theaters aren't drawing the same crowds they used to. Historical financials

Now, let's dive into EPR's historical financial performance and use our set criteria for various margins to evaluate how their profitability has evolved.

First and foremost, EPR shines with its impressive gross margin, consistently exceeding 85% since 2018. Their ability to maintain a low SG&A (Selling, General, and Administrative) margin reflects their effective cost management without unnecessary expenses.

However, the picture isn't as rosy when we focus on the depreciation and interest margins. EPR has been grappling with substantial interest payments and considerable depreciation on its income statement for years. This issue persists into their third quarter, as we'll delve into later.

That said, EPR has managed to maintain a net income margin consistently above 20%, except for 2020 and 2021, which were significantly impacted by COVID-19 lockdowns and restrictions. This positive trend must continue, along with further earnings per share ((EPS)) growth, which regrettably hasn't been the case in most years except for 2022. Notably, the high growth in 2022 is partly due to EPS having decreased significantly in the preceding three years.

Overall, EPR boasts a solid financial track record, but the goal is to see them progressively reduce their interest and depreciation margins. As investors seeking high dividend yields, we aim for companies to generate as much net income as possible, which can then be shared with us as dividends.

Stock Info

We've also performed some calculations based on EPR's balance sheet. This isn't the definitive assessment of their balance sheet quality but serves as a way to spot any significant concerns quickly.

One area of concern with EPR is its relatively high adjusted debt-to-equity ratio. While it has gradually decreased since 2020, it's still somewhat higher than what would be considered comfortable. Ideally, we'd prefer to see it closer to 1, indicating a more robustly built balance sheet.

Additionally, it's worth noting that having no preferred stock on their balance sheet would be preferable. In EPR's case, just $0.15 million in preferred stock is not significant.

On a positive note, EPR has effectively retained and even grown its earnings from 2019 to 2022. They have also consistently maintained more cash on hand than short-term debt, except for 2022.

However, it's important to highlight that the gap between their cash and debt has been diminishing since 2020. Ideally, we would like to see this trend reverse and start moving in the opposite direction by the end of 2023.

Stock Info

What have we discovered about EPR up to this point?

In essence, the company has a solid top-line margin and a healthy net income margin, with the main challenges occurring during the years marked by the COVID-19 pandemic.

While some areas could be improved, like their interest costs and equity levels, we still believe EPR has a solid foundation to stay profitable and continue delivering reliable dividends for the foreseeable future.

Their Q3 Earnings and Market Expectations For The Future

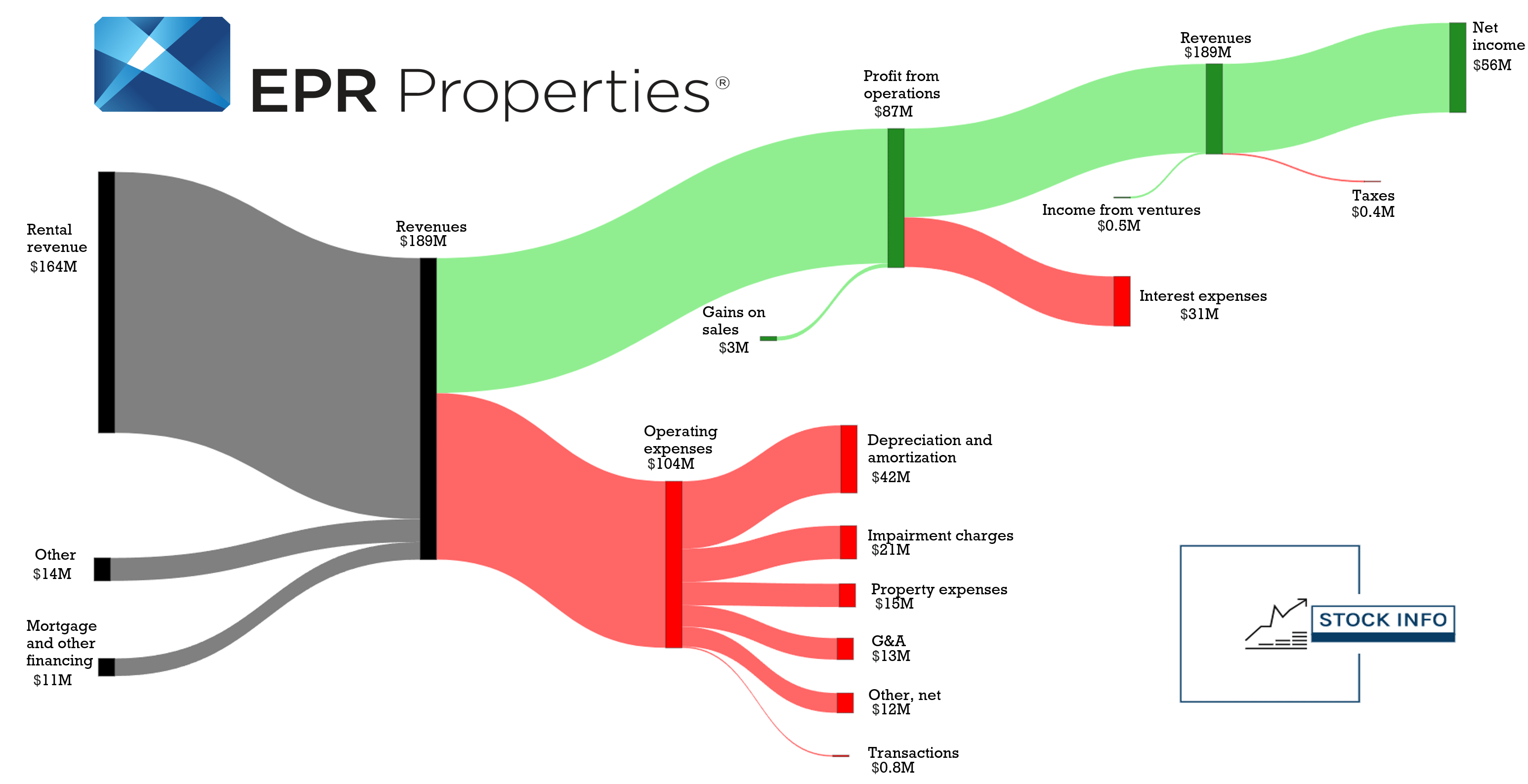

Now, let's delve into their most recent earnings to get a more up-to-date picture. In the chart below, we've simplified how their revenues eventually translate into net income and where their expenses are allocated. This essentially provides a snapshot of how EPR generates its revenue. It's probably no surprise that the lion's share of their revenue, nearly 87% in Q3, comes from their rental segment.

EPR has substantial operating expenses, but we'd like you to focus on their interest expenses, which stand at $31 million. Operating profits of $87 million resulted in interest margins of approximately 35.6% in Q3.

If this margin trend persists through the end of FY2023, it could significantly improve EPR's financial performance.

{kind=link}

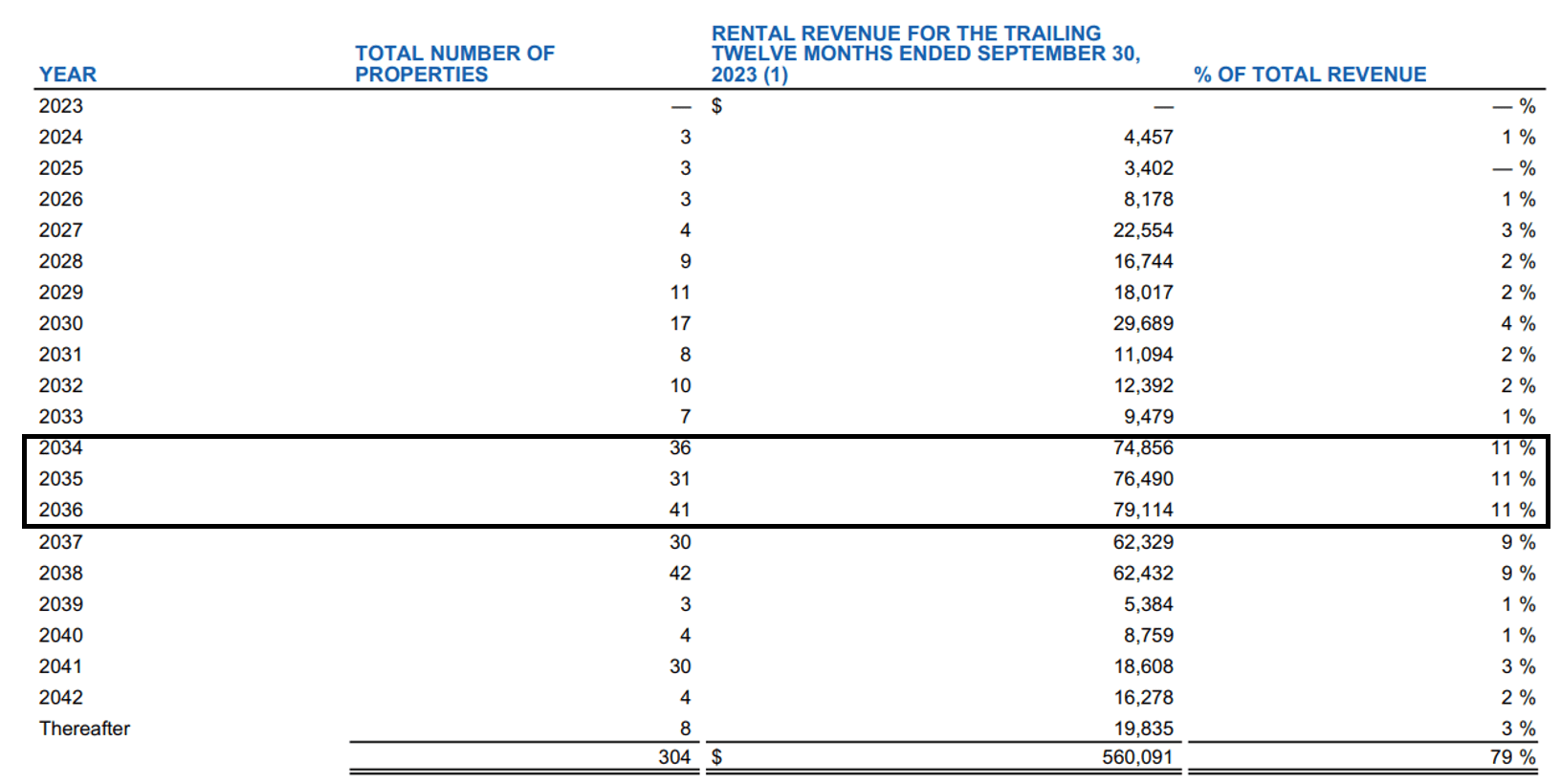

During their Q3 presentation, EPR's management provided valuable insights into their lease expirations. The majority of their properties are scheduled to have their leases expire in roughly ten years, and the management is proactively addressing this reality.

For income investors, this should provide a sense of reassurance, knowing that there's an entire decade before most of the revenue segment needs to be renegotiated.

{kind=link}

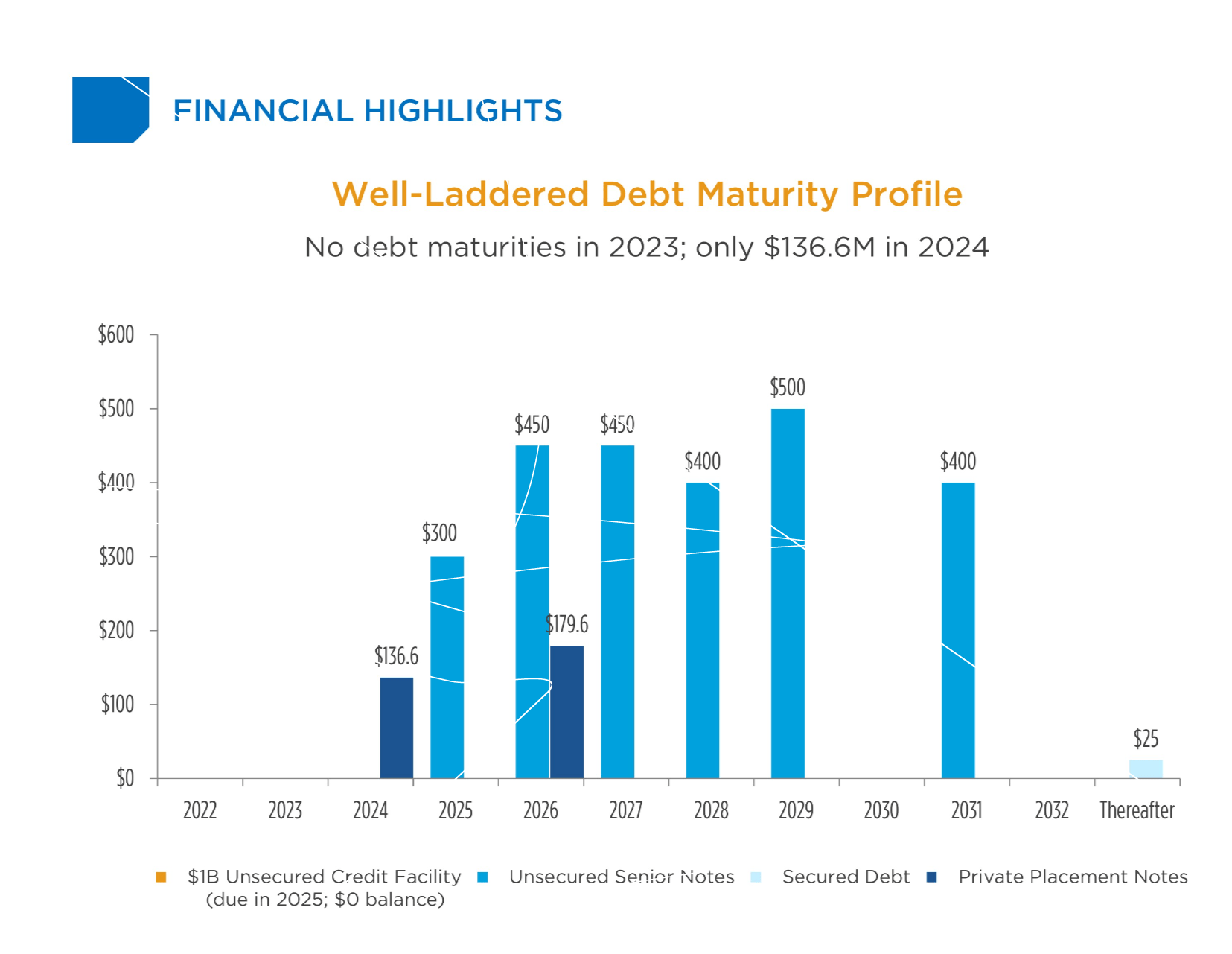

Furthermore, EPR's debt maturity schedule is positioned relatively far into the future and evenly spread out, as shown in the chart below. It's always wise to evaluate a company's debt maturity profile, particularly when you intend to maintain your position for an extended period.

This is important because as these maturities approach the 12-month mark, they become near-term debt on the balance sheet (in most cases), which can influence the overall market perception and, consequently, our return on the investment.

{kind=link}

Looking ahead, it's noteworthy that the market is valuing EPR in a way that presents attractive prospects for investors. The free cash flow ((FCF)) yield, which stands at nearly 11% based on FY2023 projections, indicates a potentially compelling investment opportunity. Furthermore, when we focus on the exact FY2023 expectations, we see EPR trading at an enticing dividend yield of almost 8%.

In simpler terms, this means that for each dollar you invest in EPR, you can potentially expect to receive an 8% return in the form of dividends and still have the opportunity for further gains with an 11% FCF yield. These numbers suggest that EPR might be a favorable choice for income-focused investors.

Stock Info

The market foresees a slight uptick in the dividend yield by 2025. However, EPS and FCF per share are expected to double in the same year, suggesting substantial growth potential.

Stock Info

In short, EPR's well-thought-out strategies, strong financial foundation, and attractive yields make the prospect of investing in this company a smart move for those who prioritize income. By carefully aligning their business decisions, maintaining robust financial health, and offering appealing returns, EPR presents a compelling opportunity for income-oriented investors looking to generate steady returns over time.

Valuation

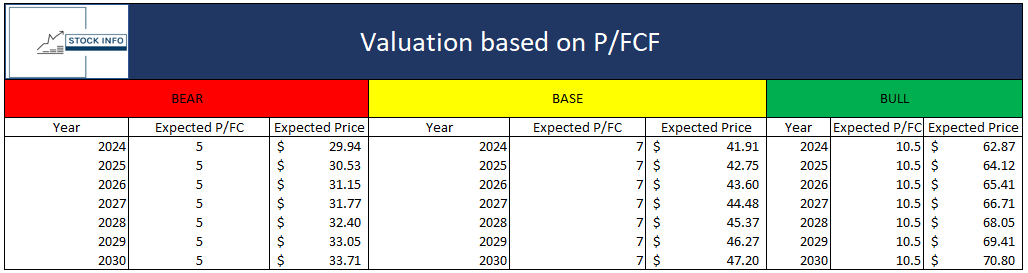

Now, let's assess the value of EPR's stock price by modeling it based on P/FCF ratios. We've considered various scenarios with different P/FCF ratios. EPR is trading at a P/FCF of approximately seven at the time of writing. In our base case, we assume this ratio will remain constant. EPR's stock trades a bit lower than the rest of its sector , so in a bullish case, we assume a P/FCF of around 10.5, which is closer to the sector median. Conversely, in a bear case, we consider a P/FCF of 5.

While we believe FCF is a powerful metric, when looking at REITs such as EPR, it is also essential to look at the P/FFO. If you are unfamiliar with FFO (Funds From Operations), it's a good metric to use for REITs as it doesn't take into account property depreciation but instead adds it back into the net income on the income statement.

EPR currently trades with a P/FFO ((FWD)) at 8.48 against a sector median of 11.03. This only underscores that EPR is underpriced to the rest of the sector at its current price. In the chart below, you can see the current FFO per share for EPR and some other REITs.

In our model, we've incorporated a conservative annual FCF growth rate of 2% and started with a price of $41. EPR actually has a 5-year FCF CAGR of 38%. However, 2018 was a year where they only made $88M, and is a historically low number for the company.

Overall, their FCF swings from year to year, which is difficult to predict, hence the conservative assumption. The results of these assumptions are detailed below.

The most significant takeaway from our model is that if EPR's P/FCF were to align more closely with the sector median, the stock price could reach around $63 by 2024. This represents a remarkable 50% increase from its current price of approximately $40. However, if the stock continues trading at its current valuation, it is reasonably priced.

If EPR's stock valuation moves in line with the sector, there's substantial upside potential. But if it remains as it is, it's currently priced relatively.

{kind=link}

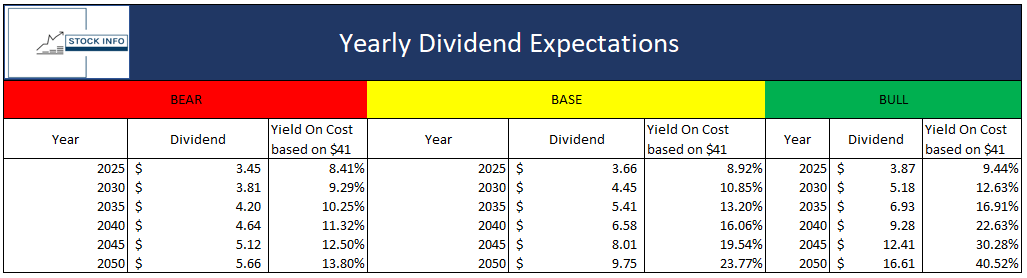

We've also applied a similar modeling approach to their dividend yield. We assumed a 2% growth in the base case, with 1% and 4% dividend increases for the bear and bull cases, respectively.

According to our model, if the stock maintains its $41 price, the dividend yield is projected to reach 8.92% by 2025. This aligns closely with the market's expected yield of 8.13%, as discussed earlier. Furthermore, our model suggests that with a 2% dividend growth in the base case, EPR could pay nearly $10 per share by 2050.

This particularly appeals to young investors aiming to build a robust retirement portfolio, as it provides an attractive long-term income potential.

{kind=link}

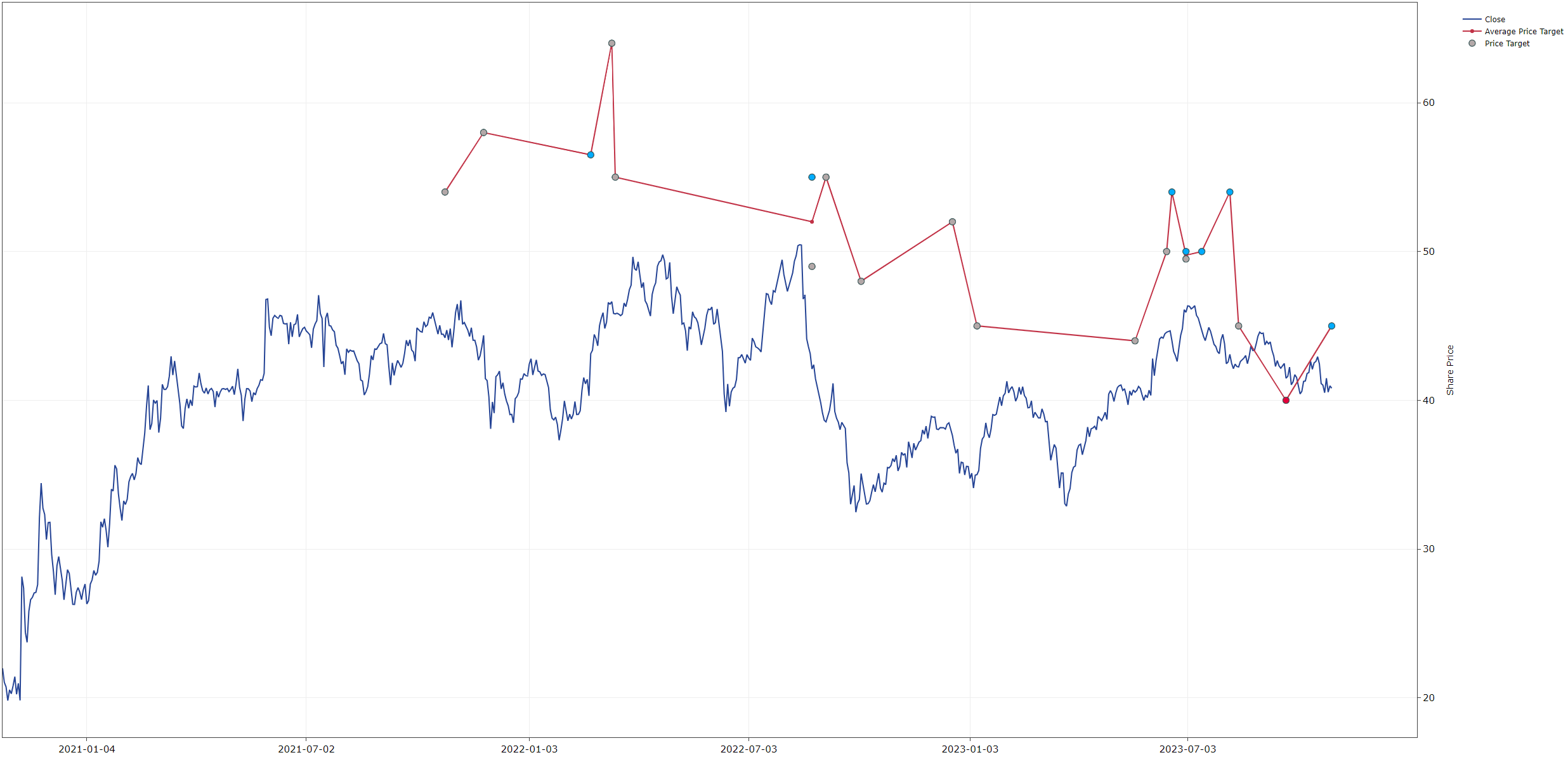

If we examine the graph below, it becomes evident that the average target price, as projected by analysts covering EPR for the next 12 months, hovers at approximately $45. This implies a potential upside of roughly 10% from the current stock price as of the time this analysis was conducted.

In practical terms, this suggests that market experts and analysts anticipate a modest increase in the stock's value over the coming year, making it an intriguing consideration for investors looking to benefit from a reasonable short-term gain.

{kind=link}

Our models and price targets suggest a small upside to EPR's stock price in the near term, which also has the potential to provide an excellent dividend yield in the future. We believe EPR is more than a solid choice to include in your dividend portfolio due to its attractive pricing and potential dividend yield.

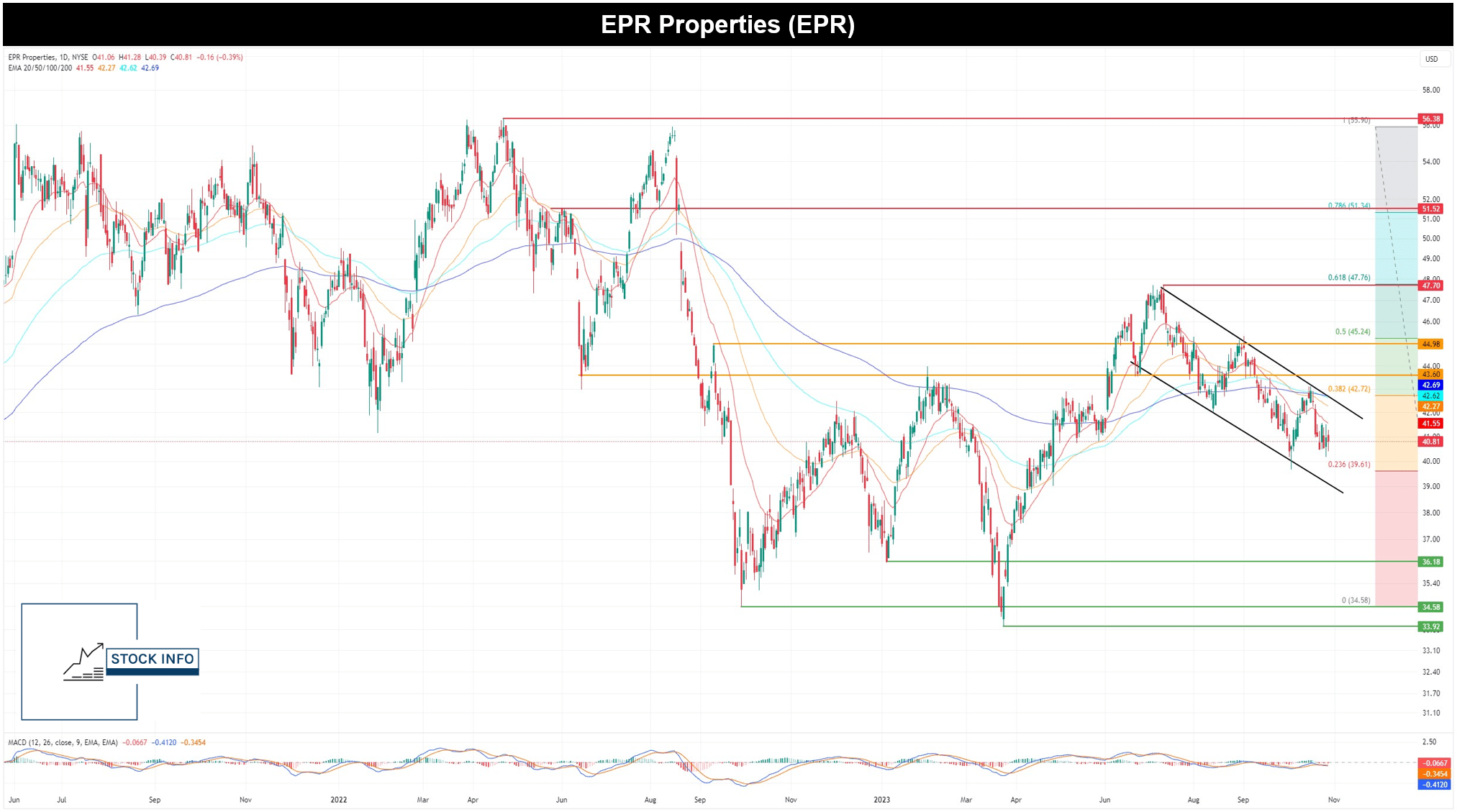

Technical Analysis

After delving into EPR's financials and projecting its potential stock price and dividend growth, the logical next step is to analyze the stock's technical aspects.

To begin with, it's worth noting that the stock has been trading within a downward channel for several months, much like many other assets in the market since the peak in late July. Recently, the stock reached a low point of around $39.60, coincidentally aligning with the 0.236 Fibonacci level. This convergence could present an attractive entry point for those considering establishing a position in EPR.

The channel's boundaries have been respected over the past few months, making it a significant trend to monitor. A breakout from this channel would be viewed as a highly bullish signal.

For a solidly bullish sentiment to emerge, the stock must breach the 20, 50, 100, and 200 Exponential Moving Averages (EMAs). It's important to note that while these EMAs may not have been consistently significant resistance points in the past, breaking through all of them can still be a formidable task.

While the EMAs may act as potential resistance levels, our analysis suggests that the initial key area of resistance is between $42.70 and $43.60. Further upward, there are resistance levels at $44.98 and $47.70, but these may be somewhat distant objectives to reach.

{kind=link}

Generating Extra Income on Top of Your 8%+ Yield

Suppose we expect EPR to trade within the range of $39.60 to $43.60 in the near term. In that case, you can generate extra income if you already hold a position in EPR by employing a short-strangle strategy.

For instance, let's assume you don't mind acquiring 100 shares of EPR at around $35. In this scenario, you can write a cash-secured put option with an expiration date of April 19, 2024, and collect a premium of $0.65 per share.

It's crucial to remember that this commitment exposes you to the possibility of purchasing the shares for $3,500 if the option is exercised.

Additionally, you can complement this by writing a covered call with a strike price representing a level at which you'd be willing to sell 100 shares of EPR, say $50. If you select the same expiration date as the cash-secured put, this option will provide you approximately $0.60 per share.

By combining these two options, you'd collect a total premium of $1.25 per share, equivalent to $125. This premium would supplement any dividends you receive while holding your stock. If you are able to do this about three times a year, it would bring in $3.75 per share a year. This represents an additional 9.15% yield per share, which is great for your portfolio.

It's important to note that holding these options contracts until expiration is not ideal. We recommend rolling them when they're about 3-5 weeks from expiration, to avoid assignment. Alternatively, you can roll the options if their gains have reached 50% or more and you feel confident adjusting the strike prices.

Furthermore, you can tailor the strategy to your preferences. For example, if you are bullish on the stock, you may opt for a cash-secured put with a strike price close to the current stock price and a covered call with a more distant strike. Ultimately, your strategy should align with your analysis and risk tolerance.

Conclusion

EPR Properties stands out in real estate investments with a unique portfolio encompassing theaters, amusement parks, recreational facilities, and educational institutions. We've assessed their historical financial performance and addressed concerns related to their reliance on AMC theaters, finding they've positioned themselves well to adapt to evolving industry dynamics.

Financially, EPR boasts a robust top-line margin and a healthy net income margin, though it face challenges in managing interest costs and equity levels. Despite some balance sheet concerns, they've grown earnings and cash retention.

EPR offers potential for income-focused investors with an attractive free cash flow yield and dividend yield. Our models suggest a modest stock price upside and solid income potential.

In technical analysis, EPR has been trading within a downward channel, with an attractive entry point near $39.60. Breaking through the Exponential Moving Averages (EMAs) and critical resistance levels between $42.70 and $43.60 is essential to turn bullish.

Overall, EPR presents an intriguing investment opportunity, offering diversification, income, and potential growth, with a solid foundation to navigate market changes. We rate this stock a buy.

For further details see:

EPR: 8% Yield For Your Retirement