WPC - EPR Properties: Cheapest Amongst Triple Net REITs But Is That Enough?

2023-10-05 12:00:00 ET

Summary

- EPR Properties is an experiential real estate investment trust with a portfolio valued at $6.7 billion.

- The majority of EPR's earnings come from its experiential segment, with theaters being the largest component.

- The REIT shut off its dividend spigot in 2020, but it is back with a bang and looking stronger than ever.

An experiential real estate investment trust. That is how EPR Properties ( EPR ) introduces itself on their website and publications. It fits like a glove when you consider the source of most of EPR's earnings.

Q2-2023 Presentation

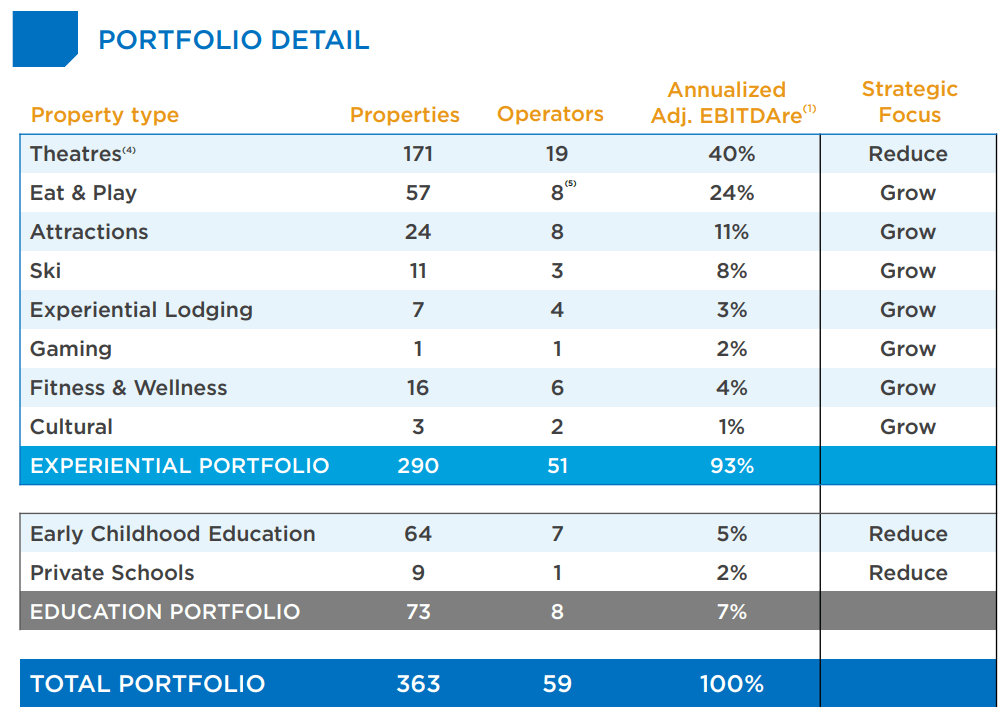

As of the end of Q2-2023, EPR had a portfolio valued at $6.7 billion, with 363 locations spread across 44 states of the United States and two Canadian provinces, Ontario and Quebec. Of the 363 locations, 290 are grouped under the "Experiential" segment for reporting. As we can see below, theatres form the bulk of these.

{kind=link}

The Education segment comprises 64 early childhood center properties and 9 private schools. In terms of occupancy, as of June 30, 2023, the experiential portfolio was 98% leased, whereas the education portfolio was 93% leased. On a combined basis, the occupancy was 97%.

Q2-2023 Presentation

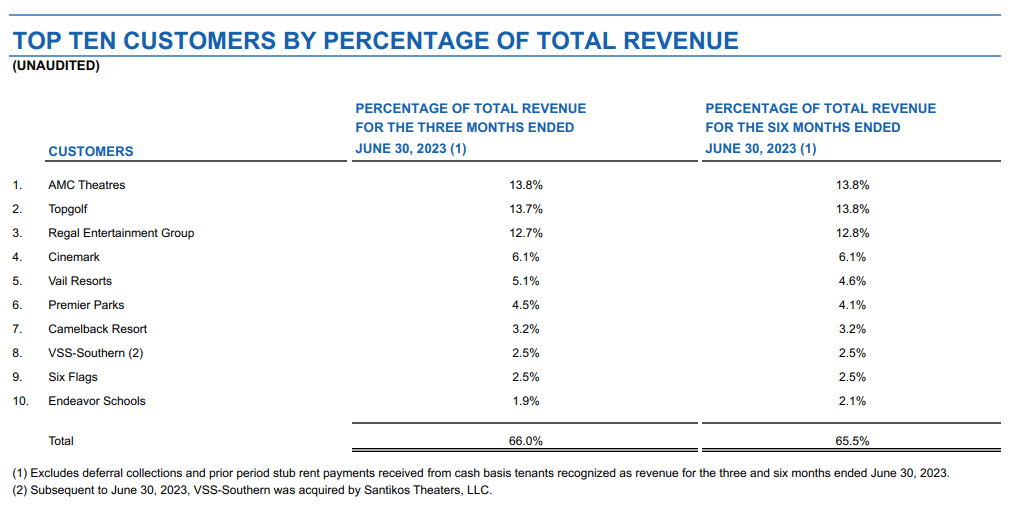

Based on its portfolio composition, it is no surprise that its top 10 tenant list is comprised almost entirely of entertainment providers, several of them well-known.

{kind=link}

AMC Entertainment Holdings, Inc. ( AMC ), Topgolf and Regal Entertainment Group, contribute the bulk revenue in this group. The lattermost of this trio filed for Chapter 11 bankruptcy in September 2022. Regal stopped paying rent for a brief period, but recommenced in the following month. In June 2023, EPR and Regal entered into a new master lease agreement for 41 of the 57 properties that Regal leased. Those that were not covered by the master lease were surrendered to EPR. Our protagonist already put to use 5 of the 16 surrendered properties and has plans for the balance 11.

The Company has entered into management agreements whereby Cinemark will manage four and Phoenix Theatres will manage one of the surrendered properties. The Company plans to sell the remaining 11 surrendered properties and deploy the proceeds to acquire non-theatre experiential properties.

Source: 10-Q .

VSS-Southern, another name in the top 10 list was acquired by Santikos Theaters at the beginning of Q3. VSS-Southern paid in full the deferred rent owing to EPR, which will be recognized in Q3. There were no structural changes to lease terms due to the change of hands.

Collectively, EPR's tenants had a 2.0x rent coverage for the trailing twelve months ended March 31, 2023. Theatres were the big drag with rent coverage barely averaging 1.3X.

Q2-2023 Presentation

Almost all of EPR's properties cater to single-tenants and are structured as triple-net leases. This means, that the tenant is responsible for the operating and ongoing maintenance expenses, with the landlord only covering the major structural repairs that are capital in nature. The REIT does have a few multi-tenant properties, where the triple-net provisions are not in place. In these cases, the tenants each pay their pro rata share of common area maintenance expenses.

It is rare that a triple net REIT finds itself in a predicament where it has to stop paying dividends. However, being a landlord that primarily caters to the entertainment industry, EPR did just that for several months during the pandemic. Its tenants were not essential services and were subject to shutdown, drying up the REITs cash flow for dividends. The REIT had just raised its monthly payout from 37.50 cents to 38.25 cents in March 2020 and stopped it completely from May 2020 to July 2021. The dividend has still not been restored to its former glory, and the REIT now pays 27.50 cents/month. At the current price of $40.60, EPR currently yields around 8.1%.

The dividend cut is in the rearview now. EPR had its credit ratings drop below investment grade as the credit rating agencies weighed in on the fallout post COVID-19. By the middle of 2022, all of them basically acknowledged that EPR had navigated the turmoil with aplomb and handed them back their IG numbers.

Q2-2023 Presentation

Q2-2023

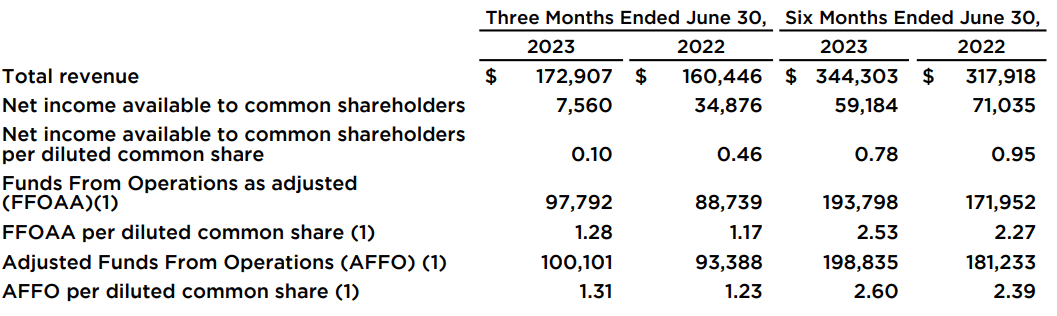

$7.3 million of previously deferred rent was received in Q2 and EPR recognized it as revenue as the proceeds were from cash-based tenants. That, along with the accretive impact of acquisitions and developments after Q2-2022, contractual rent increases, and higher percentage rent from one of the ski properties, resulted in the close to 8% increase in the year-over-year revenue.

{kind=link}

The FFO and AFFO increased by a similar percentage though the amounts per share were down due to a higher share count.

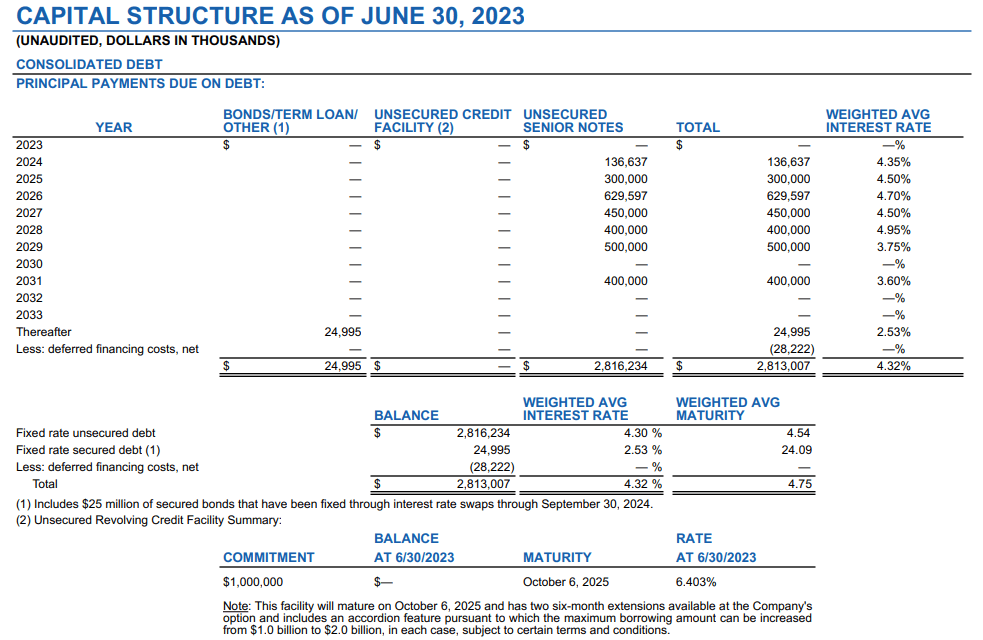

EPR does not have any debt maturing for the remainder of 2023, with around 5% maturing in 2024.

{kind=link}

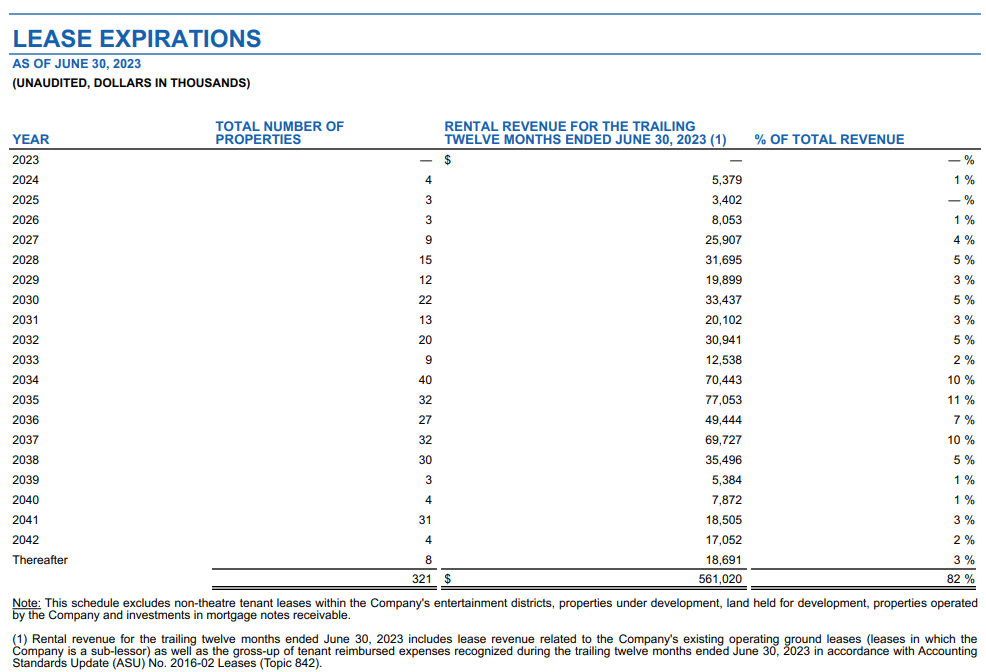

The debt remained unchanged in 2023 and as a result so did the weighted average interest rate of 4.32%. It has more than enough liquidity on hand at June 30, with around $100 million in cash and the $1 billion available from its revolving credit facility. EPR is also well positioned in terms of lease expirations, with no meaningful activity happening in any single year for a decade out.

{kind=link}

Verdict

The bull case for EPR comes down to the ultra-low valuations (8X FFO), alongside a solid investment-grade balance sheet. The debt maturities are one of the better ones we have seen as well and the REIT did not romance at all with floating rates. This bull case has been relatively weakened as EPR has really outperformed its triple net peers recently. So when you run against,

1) Spirit Realty Capital Corp ( SRC )-9X FFO.

2) NNN REIT Inc. ( NNN )-11X FFO.

3) WP Carey ( WPC )-10X FFO.

4) Realty Income ( O )-12X FFO.

5) Essential Properties Realty Trust Inc. ( EPRT )-12X FFO,

you still find EPR attractive, just perhaps, not as much as you did at the beginning of 2023.

Also let's face it. None of those have the same tenant profile with AMC right at the top and with such a heavy weighting. The counterpoint here is that AMC is its very likely bankruptcy, is not such a big deal. Most of AMC's theatres leased from EPR are above average in terms of revenue generation and quality. Even in a bankruptcy, AMC would be forced to honor those terms, or at worst, get them amended just slightly. Overall we think EPR is attractive here, but we would not call it a table-pounding buy, simply because of what else is on offer.

The Preferreds

EPS had three preferreds outstanding, two of which are convertible.

- EPR-C 5.75% Series C Cumulative Convertible Preferred Shares ( EPR.PR.C ).

- EPR-E 9.00% Series E Cumulative Convertible Preferred Shares ( EPR.PR.E ).

- EPR-G 5.75% Series G Cumulative Redeemable Preferred Shares ( EPR.PR.G ).

The EPR.PR.G is the simplest to evaluate with an 8% yield on the current price. It has a solid yield but for its rating (BB-Fitch), we don't think it is particularly enticing. We are getting in that range with IG level debt today and this is a bit weak on a relative basis.

EPR.PR.C offers even less (7.83%) but it is convertible into common shares at your option. So is EPR.PR.E.

As of December 31, 2022, our Series C preferred shares are convertible, at each of the holder's options, into our common shares at a conversion rate of 0.4192 common shares per $25.00 liquidation preference, which is equivalent to a conversion price of approximately $59.64 per common share (subject to adjustment in certain events). Additionally, as of December 31, 2022, our Series E preferred shares are convertible, at each of the holder's options, into our common shares at a conversion rate of 0.4826 common shares per $25.00 liquidation preference, which is equivalent to a conversion price of approximately $51.80 per common share (subject to adjustment in certain events).

Source: EPR 10-K .

At present the 8.9% yield on EPR.PR.E remains the most attractive in the entire EPR suite on a relative basis. It also offers substantial upside in case the former glory days come back.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

EPR Properties: Cheapest Amongst Triple Net REITs, But Is That Enough?