EQGPF - EQB: Caution Advised Despite Strong Growth

2023-08-09 18:03:39 ET

Summary

- At the current share price, Equitable Bank is now a hold given the macroeconomic backdrop and recent increase in share price.

- The Canadian macroeconomic environment, characterized by rising interest rates and record-high household debt, poses potential risks for EQB and other banks in the market.

- Monitoring the nonperforming asset rate and the bank's asset quality becomes essential as the Canadian economy faces headwinds related to debt burden and rising interest rates.

- While the bank's low-efficiency ratio is an appealing aspect to investors, expanding its physical presence and services may impact efficiency and net interest margin.

All financial figures are in unless otherwise stated.

All financial data is from Capital IQ unless otherwise stated.

Price Target: $75.00

Investment Thesis

EQB Inc. ( EQB:CA ) has seen tremendous growth in its share price and their operating results over the past 3 years. In my opinion, the recent share price increase now reflects an accurate valuation of EQB Inc. when considering the economic backdrop Canadians are facing and the contraction in pricing multiples relative to the 'Big 6'.

Introduction

Below, I provide a brief description of EQB's lines of business as they will be mentioned throughout various sections of the article. EQB operates under two lines of business:

- Personal Banking (Loans Under Management: ~$32 billion)

- EQ Bank: A leading digital bank and the first bank hosted in the cloud.

- Residential Lending: Lending in the uninsured mortgage market.

- Wealth Decumulation: Reverse mortgages and insurance lending.

- Consumer Lending: Lending solutions other than mortgages.

- Payment-as-a-Service: Developing a PaaS business.

- Commercial Banking (Loans Under Management ~$28 billion)

- Business Enterprise Solutions: Commercial real estate solutions for small businesses.

- Commercial Finance Group: Partners with large institutions and mortgage investment corporations to finance large commercial mortgage transactions across Canada.

- Multi-unit Insured: Orgination of multi-unit insured loans under the Canada Mortgage Bond program.

- Specialized Finance: Offers secured financing solutions to special lenders in order to finance their growth.

- Equipment Leasing: Provides commercial vehicle and equipment leasing services to small businesses across Canada.

- Credit Union: Concentra Bank which is the largest provider of wholesale banking solutions and partnerships for the majority of credit unions outside of Quebec.

- Concentra Trust: A subsidiary of Concentra Bank which is the 7th largest trust company in Canada which provides solutions to corporations, indigenous trusts, and personal trusts.

Together with the acquisition of Concentra Bank, Equitable Bank is the 7th largest Canadian Bank behind the 'Big 6' and has framed itself as 'Canada's Challenger Bank' with roughly $108 billion AUM & AUA. They serve more than 543,000 customers in Canada and have been ranked the number 1 bank in Canada by Forbes for two years in a row.

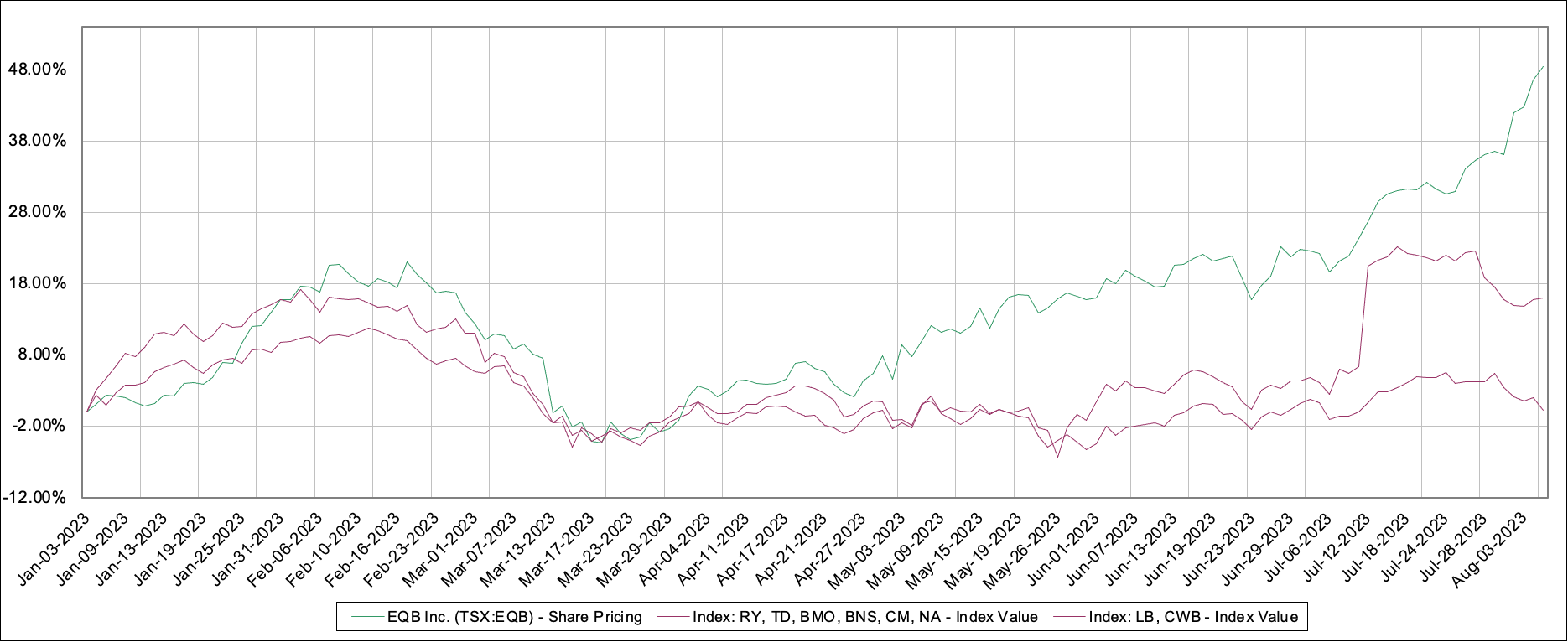

Share Price Increase & Relative Valuation

Note: For the purposes of my relative valuation, I have created two market cap-weighted indices:

- Index 1: RY, TD, BMO, BNS, CIBC, and National Bank

- Index 2: LB and CWB

EQB has properties that fit into both indices but generally lines up more with index 2 given the size of the companies in index 1. Any note of indices can have the reader refer to the above.

Throughout the year, index 1 (Big 6) delivered a modest return of 0.29%, index 2 (LB and CWB) achieved 16%, while EQB outpaced them all with an impressive 47% return, highlighting its superior performance.

The first half of 2023 has been exceptionally successful for EQB, leading to an upward revision of their guidance. Despite the recent banking crisis in the United States taking a small toll, EQB's share price has demonstrated resilience. In 2023, EQB achieved remarkable financial metrics, including a 17.5% return on equity (ROE), a significant 7.5% increase in book value per share, a remarkable 27% surge in diluted earnings per share (EPS), and a substantial 26% increase in their dividend payout. These figures underscore EQB's strong growth and investor-friendly approach.

{kind=link}

EQB's performance across all business lines has firmly established it as a premier Canadian bank. However, its smaller size has historically led to a size premium embedded in the P/B multiple. A detailed analysis of this crucial metric reveals intriguing insights.

Over the past five years (Jan 1, 2018 - Jan 1, 2023), Index 1 has traded at an average P/B of 1.62x, while EQB's average P/B during the same period was 1.09x, representing a substantial 49% discount to Index 1. However, in 2023, this premium has narrowed to an average of 37% and currently stands at approximately 7%.

EQB's recent growth has significantly closed this premium, leading to a notable convergence. As EQB's size does not match that of the banks in Index 1, the recent surge in share price appears to be more momentum-driven than fundamentally-based. In 2023, EQB's average P/B has been 1.02x, implying a share price of $68.68 at those levels. This convergence is evident during the recent run-up in share price after the Q2 results were reported.

Historical P/B Multiples (Capital IQ)

{kind=link}

Despite EQB's impressive growth and attractive returns for existing shareholders, potential new investors should carefully consider the recent surge in share price. The Canadian banking industry operates as an oligopoly with stringent regulations and high barriers to entry. The Big 6 banks collectively hold around 93% of all Canadian assets, a share that has remained relatively stable over the past decade.

While EQB's growth has been remarkable, it may not be sufficient to propel the bank into the ranks of Canada's top banks just yet. The established players in the industry have a dominant position, and breaking into this elite category requires consistent and substantial growth over an extended period.

Therefore, while EQB has demonstrated noteworthy performance, it's essential to acknowledge the competitive landscape and potential challenges the bank may face in reaching the level of the Big 6 banks in Canada.

ROE Breakdown

Return on Equity is one of the key indicators of value being generated by a bank. As such, it's important to break down the ROE into components so we can better understand where the return is coming from. For this analysis, I use the 5-step Dupont Analysis Model which uses the following:

-

Tax Burden = Net Income/Pre-Tax Income = 0.75

- Asset Turnover = Revenue/Average Total Assets = 0.011

- Financial Leverage Ratio = Average Total Assets/Average Equity = 19.72

- Interest Burden = Pre-Tax Income/Operating Income = 0.62

- Operating Margin = Operating Income/Revenue = 0.88

ROE = (0.75*0.011*19.72*0.62*0.88)*2 = ~17.3%

The difference in ROE here is due to rounding errors and minor differences between the reported ROE and adjusted ROE.

From the above numbers we see that EQB retains roughly 75% of earnings after paying income taxes, EQB is able to generate around $0.01 of revenue for every $1 in assets, they have a financial leverage of 19.72x, an interest burden of 62%, and an operating margin of 88%.

If EQB is able to increase their tax burden (the amount they retain after paying taxes), their asset turnover (the revenue generated for every $1 in assets), their financial leverage ratio (the amount of assets they have relative to equity), their interest rate burden (the extent to which interest expense impacts profits), or their operating margin (% of operating profit for every $1 in revenue) they will be able to increase their ROE. The first, fourth, and fifth terms multiplied together give the net profit margin. A key indicator in the bank's ability to generate a profit.

NIMS & The Efficiency Ratio

EQB's net interest rate margin (NIMS), which represents the difference between the interest earned on assets and interest paid on liabilities, has demonstrated positive growth. In Q2 of 2023, EQB achieved a NIMS of 1.99%, and over the past 6 months, it has averaged 1.97%.

This upward trend in NIMS can be attributed to the Canadian government's decision to raise interest rates, which has positively impacted the bank's ability to generate income from their asset portfolio. Notably, comparing quarter-to-quarter NIMS across different banks can be misleading due to the varying fiscal year periods employed by each bank. However, when considering the year-to-date performance, EQB's NIMS stands out, surpassing many other banks, except for CWB and BNS.

EQB's ability to maintain a higher NIM relative to its peers underscores its strong position within the industry, and the upward trajectory of NIMS bodes well for the bank's income generation potential moving forward.

The efficiency ratio is a critical measure to see which bank is operating at the best rate. Defined as:

- Efficiency Ratio = Non-Interest Expenses/Revenue

Another reason why EQB is in favor with investors is because of how low their efficiency ratio is:

| Bank |

| FY2022 |

| Q2 2023 |

| RBC |

| 52.3% |

| 58.8% |

| TD |

| 52.8% |

| 53.4% |

| BMO |

| 55.8% |

| 60.2% |

| BNS |

| 52.8% |

| 57.5% |

| CIBC |

| 56.4% |

| 56% |

| NA |

| 52.6% |

| 52.6% |

| EQB |

| 41.6% |

| 42.8% |

| CWB |

| 51.5% |

| 55.3% |

| LB |

| 66.5% |

| 69.7% |

| Average (Excluding EQB) |

| 55.1% |

| 57.9% |

I believe that EQB has achieved its low-efficiency ratio primarily by operating solely through digital banking, which has proven to be a successful low-cost model for the bank. This strategy has allowed them to maintain an excellent efficiency ratio while keeping their operating costs competitive.

However, for EQB to effectively compete with the largest banks and be priced similarly to the Big 6, they may need to consider adopting the traditional banking model, which could result in an increase in their efficiency ratio. This increase in efficiency ratio may be an inevitable consequence of expanding their physical presence and offering a broader range of services.

Furthermore, as EQB aims to compete on a larger scale, they might face trade-offs that could potentially lead to a slight decrease in their net interest margin.

Given these considerations, I rate EQB as a hold. While their successful low-cost digital banking model has served them well, further growth and competition with larger banks may require strategic decisions that could impact their efficiency and net interest margin.

Canadian Macroeconomic Environment & Debt

The combination of inflation, depleted pandemic savings, and rising interest rates has made Canada the most indebted country in the G7, with household debt reaching 187% of disposable income in 2022 . As of the first quarter of 2023, Canadian consumer debt has hit an estimated all-time high of $2.32 trillion, representing a 5.6% increase from the previous year. The impact of rising interest rates on this record-high debt level is yet to be fully realized, especially with mortgage interest payments now 70% higher than a year ago.

Given these challenges, the focus is on Canadian banks, including EQB. In particular, EQB reported that nonperforming assets constituted 0.44% of their total assets, making it the second-worst among the largest nine banks. This nonperforming asset rate has been gradually increasing, raising concerns about potential risks in the bank's loan portfolio. As the Canadian economy faces headwinds related to the debt burden and rising interest rates, monitoring the banks' asset quality and ability to manage credit risks becomes critical for investors.

| Quarter |

| Rate |

| Q2 2022 |

| 0.172% |

| Q3 2022 |

| 0.219% |

| Q4 2022 |

| 0.272% |

| Q1 2023 |

| 0.304% |

| Q2 2023 |

| 0.438% |

The nonperforming asset rate for EQB is currently at 0.44%, which is reminiscent of levels last seen in Q1 2019 when it reached 0.473%. However, during the height of the COVID pandemic in Q2 2020, this rate peaked at 0.525%. Considering the current economic challenges, including higher interest rates, increased living costs, and mortgage renewals, it is likely that this rate will continue to rise and more importantly, persist as this environment is different than the 'short' lived pandemic.

As an alternative lender, EQB may face more significant impacts from negative shocks in the market compared to traditional banks. While the bank has experienced remarkable growth, these potential risks should be carefully considered by new investors. The bank's ability to manage credit risks and navigate the changing economic landscape will be crucial in determining its future performance.

Conclusion

In conclusion, EQB's exceptional growth and performance have positioned it as a leading Canadian bank. However, careful consideration should be given to the current valuation, competitive landscape, and potential risks amid the evolving macroeconomic environment. Investors should closely monitor EQB's ability to manage credit risks and adapt its business model to sustain its growth trajectory in the dynamic banking industry.

For further details see:

EQB: Caution Advised Despite Strong Growth