ETRN - EQT: Narrowing The Gap

2023-06-19 03:57:34 ET

Summary

- The realized prices are going to improve as EQT's management continues to arrange transportation to stronger pricing markets.

- EQT's management has worked on decreasing operating costs. It is easily the most visible accomplishment.

- Finding transportation depends upon opportunistically purchasing pipeline capacity as it becomes available. This is a slow process.

- The latest acquisition does have some midstream capacity out of the basin. It also conforms to other management requirements.

- This management will likely continue to improve prices and costs, which will lead to increasing profitability as natural gas prices strengthen.

When the current management of EQT Corporation ( EQT ) actually gained control of the company, they found a real mess. There was little to no emphasis on costs and even less emphasis on prices realized (if that was possible). The prior management was happy to report results as long as those results were okay. The problem with that was that the challenges of 2020 laid ahead at the time. Had this management not taken over, there is every chance that the company would have had some challenges that the prior management may not have overcome. Shareholders would likely have been more than disappointed.

Since current management has taken over, there has been a lot of work on costs from the day they walked in the door. But realized prices are taking longer because transportation agreements tend to be long term. So, it is hard to redirect production to more profitable places when there is no immediate way for natural gas to get there. Nonetheless, management is working to get more favorable prices even if "it is at an inch at a time".

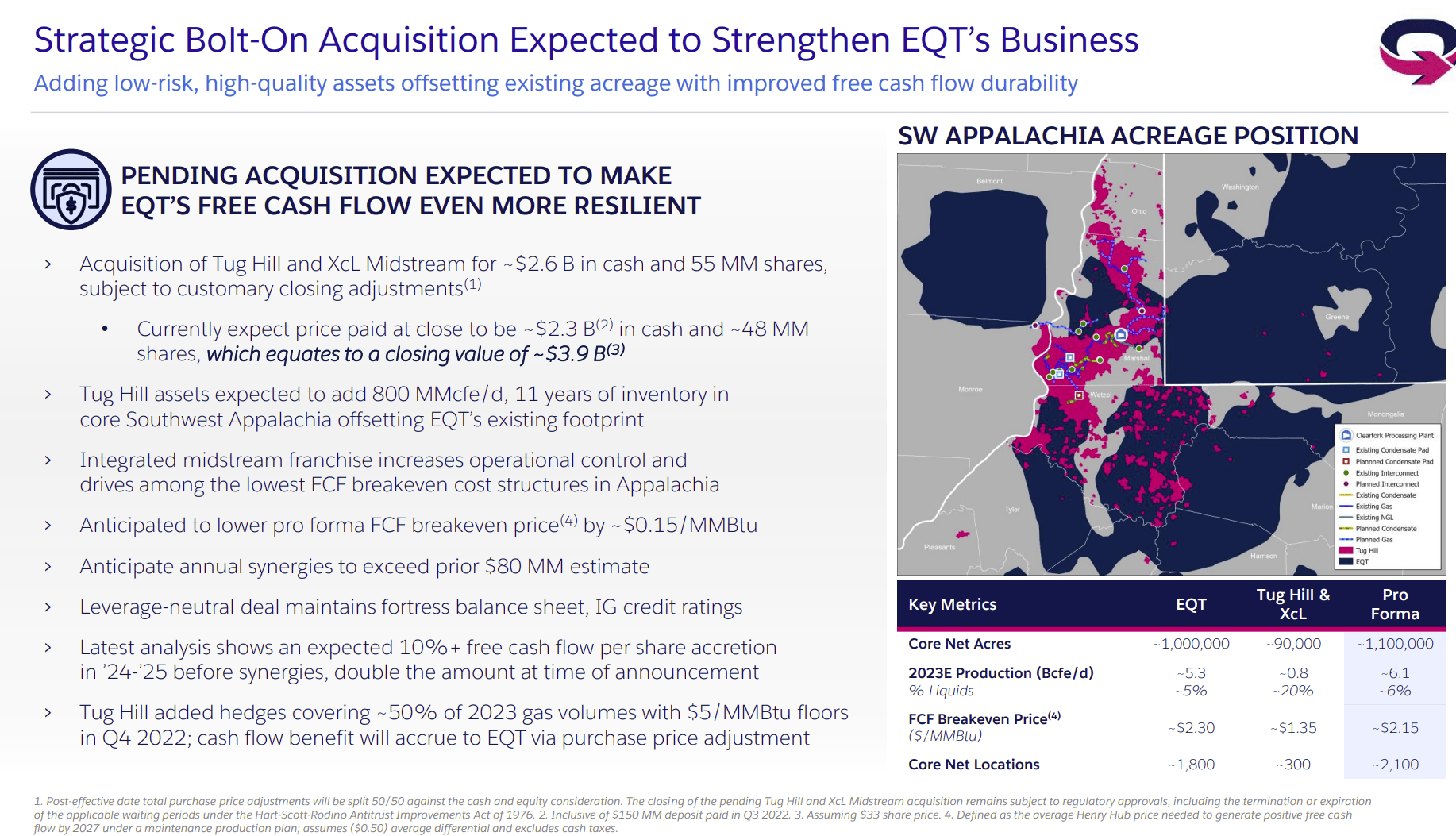

EQT Summary Of Acquisition Benefits (EQT First Quarter 2023, Earnings Conference Call Slides)

{kind=link}

The acquisition clearly has all the usual benefits this management looks for plus one more. There is some midstream capacity that gets at least some of the production out of the basin. When that is combined with the low breakeven point shown above, this acquisition is unusually profitable compared to the operations of EQT.

Furthermore, the more connections out of the basin that management has, the sooner management is likely to get better prices for production. The Marcellus has too much production to sell in basin. Therefore, the production sold in basin goes for a discount. The situation was particularly bad when this management took over. It is slowly getting better through management purchases of capacity as it becomes available and acquisitions like this one that have a little bit of room that management will likely use.

Management formerly had a close relationship with Equitrans Midstream ( ETRN ). However, that midstream company has been bogged down with the Mountain Valley Pipeline challenges for some time. Hence, there will not be any new hookups to better pricing markets any time soon.

Now if Equitrans' management can overcome the current challenges and meet the goals of this management to get that pipeline operating, then EQT management probably gains access to a stronger pricing market than the Marcellus basin. Recently, the latest debt agreement had a provision to get things going again. But given the history here, let us see if that solution holds up where many others failed. Time will tell on this possibility. You can bet that management of EQT is not exactly waiting with bated breath.

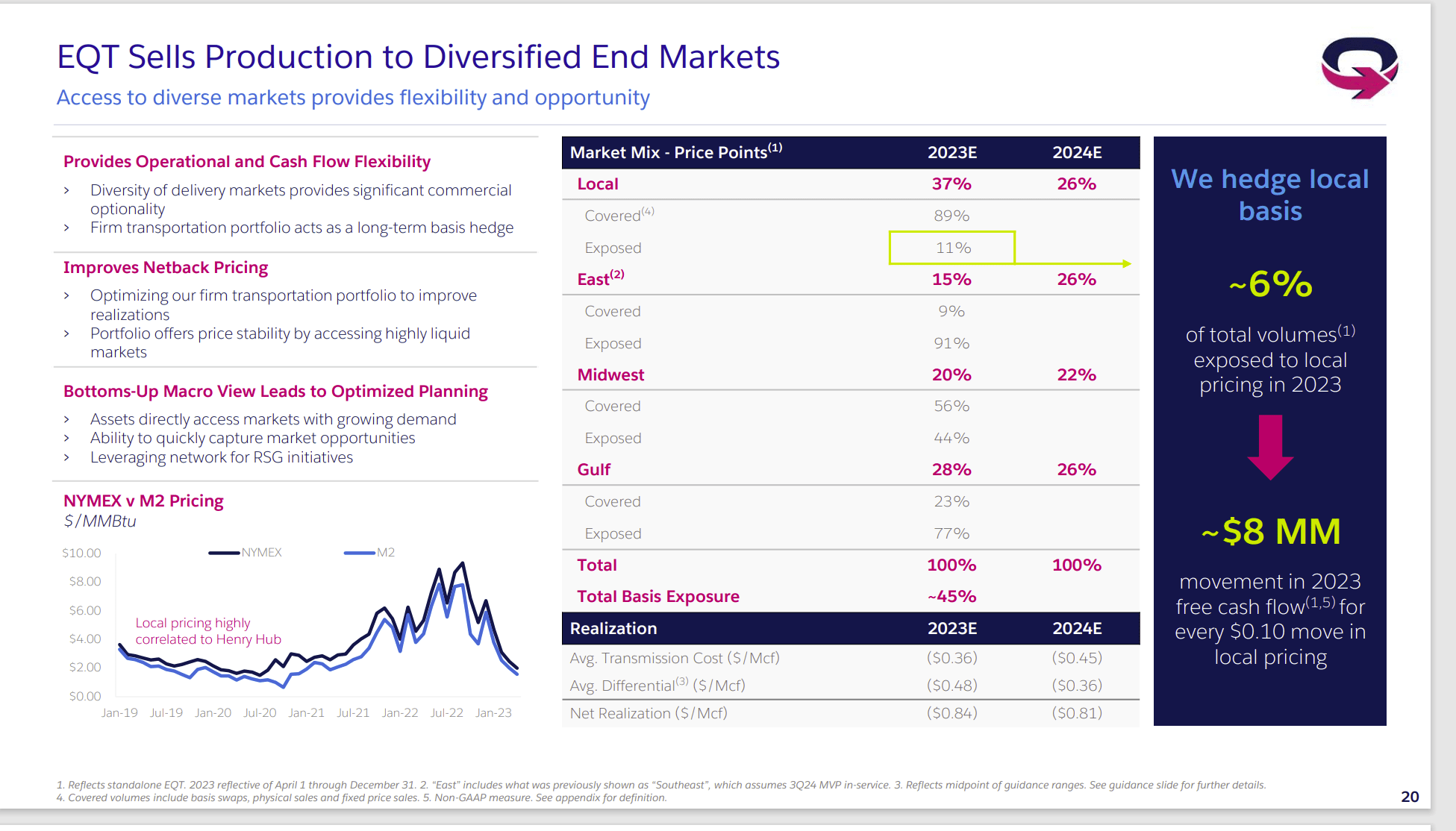

EQT Potential Sales Markets And Current Sales Destinations (EQT First Quarter 2023 Earnings Conference Call Slides)

{kind=link}

Now, there is an assumption in the above slide about the Mountain Valley Pipeline beginning operations late next year. However, even with that, a substantial amount of production is still exposed to the weak pricing of the basin.

Management is going to continue working on that, and there is more export capacity coming online for North America that should lead to stronger prices in general in the future as North America joins the stronger world natural gas pricing market.

Shareholders should expect that net realization to improve over time as management gets more and more production out of the basin. This will continue to be an incremental improvement situation for some time to come. Unless new pipelines are built to better areas, it takes a fair amount of time (as in years) for this type of improvement to happen.

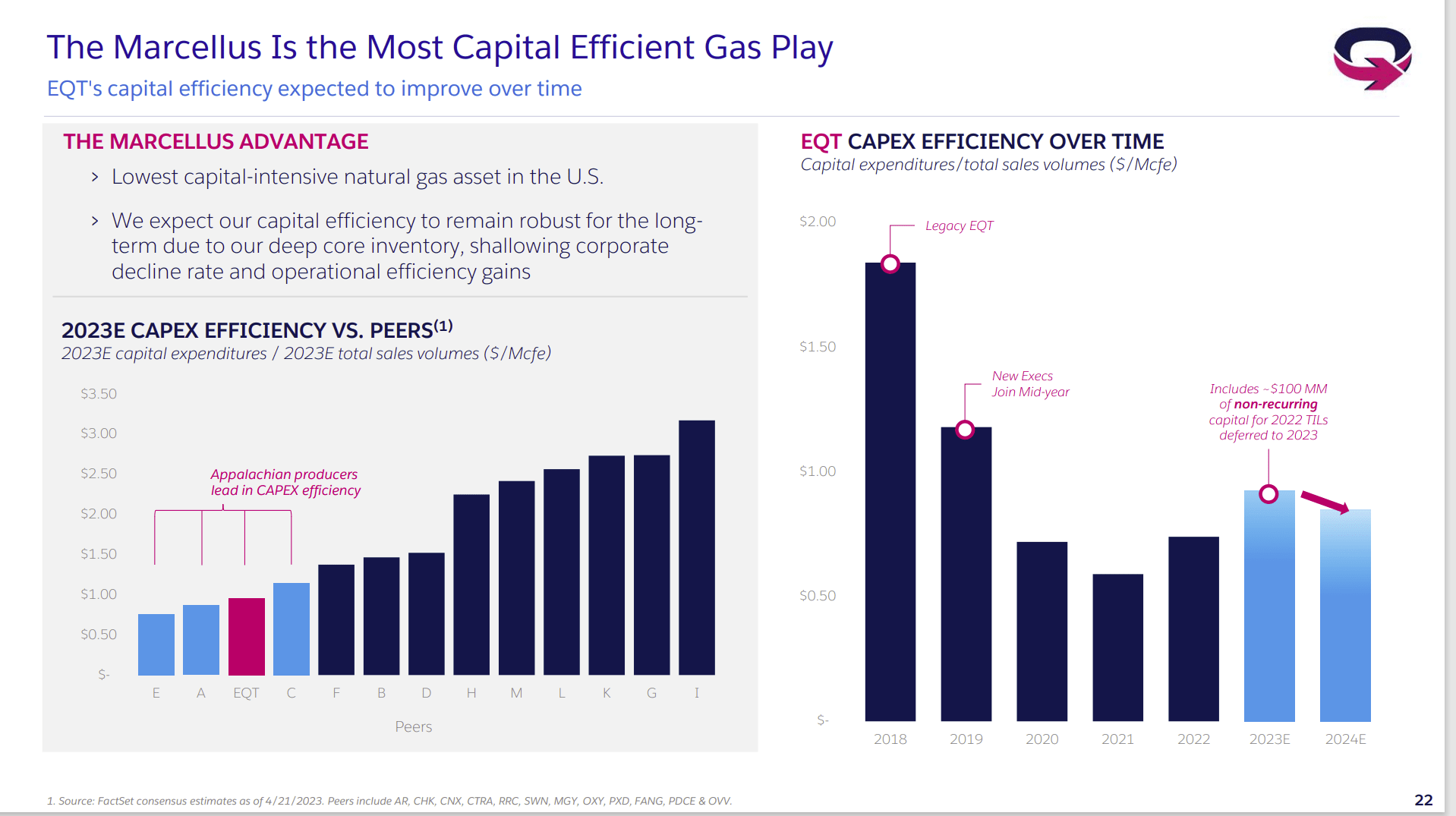

EQT Capital Efficiency History And Competitor Comparison (EQT First Quarter 2023, Earnings Conference Call Slides)

{kind=link}

Right now, prices are fairly weak in North America for a number of reasons. But the Marcellus has some of the best costs in North America. Therefore, production is unlikely to decline because production here adds cash flow under a wide variety of industry conditions (including some substantial weak pricing conditions).

Investors need to realize that the decision to drill and produce natural gas differs from the corporate breakeven. A profitable natural gas well will spread corporate costs over more production to actually lower the corporate breakeven and aid profitability even when commodity prices are weak.

Since Marcellus basin costs are among the lowest in the industry, this basin will not be cutting production in the current environment. Such an action as cutting production now would decrease cash flow for most producers.

It would appear instead that the basin acting as the "swing production" is the Haynesville where costs are quite a bit higher. There may be other dry gas production that gets shut-in as well because the production cost is simply too high.

This management and Antero Resources ( AR ) management have noted that overall natural gas production appears to be headed down. Therefore, both are viewing the future as having stronger natural gas pricing. This has been mentioned in the conference calls and the last few quarterly reports (one way or another). Now, should that change, then both managements would likely have new priorities. Right now, neither appears to be worried about an extended period of weak natural gas prices.

The Future

The current management has accomplished a lot since taking over EQT. The company is now investment grade, which lowers the cost of debt. Management has also whipped operations into shape.

There is now an emphasis on cost reduction to keep up with the periodic technology improvements that sweep the industry. The Marcellus was one of the last basins to show operating improvements for a while. But that currently appears to have changed towards faster improvements. The pace can change at any time, and cost improvements could certainly end tomorrow. But it appears that the Marcellus operators will improve costs considerably over the next few years even as North America increases the ability to export natural gas.

That makes this company an investment consideration for those that can handle the volatility of natural gas. This management did well with the last company they sold. They appear to be on track to treating shareholders well with this company also.

The company is now in a position to build free cash flow considerably. That will likely result in a rapidly rising dividend and share repurchases. While this is considered a variable distribution entity because of the reliance on commodity prices, this entity could have some rather generous future distributions when compared to the current share price. Those who are not retiring right away may want to consider this issue for that reason.

This issue is not for those that cannot accept the pricing volatility that goes with the oil and gas business. This is also a business that has unusually low visibility.

On the other hand, this is one of the best management in the business. That alone could make the purchase of this stock quite a bargain.

For further details see:

EQT: Narrowing The Gap