EQIX - Equinix Is Expensive But Worth It

2024-01-09 18:38:18 ET

Summary

- Equinix, Inc. is a leading data center provider with 204 hubs across 5 continents and has experienced significant growth over the past couple of decades.

- The company has advantages such as superior property level operating margins, a phenomenal cost of capital, and a significantly higher profit margin at the REIT level.

- Despite trading at a high multiple, Equinix is positioned to outgrow its peers due to its operational strength and cross connection ecosystem.

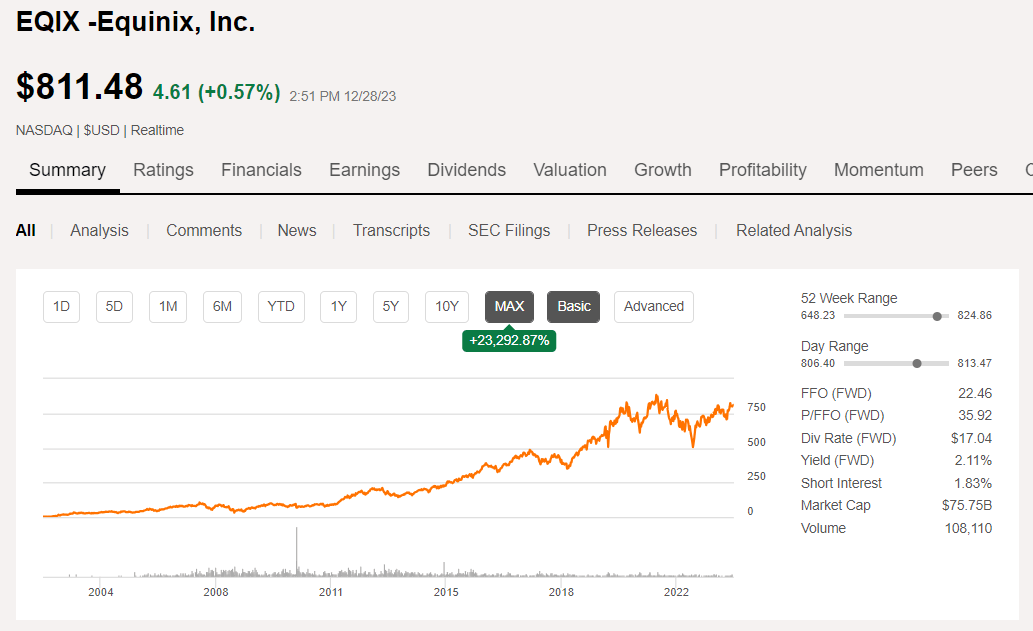

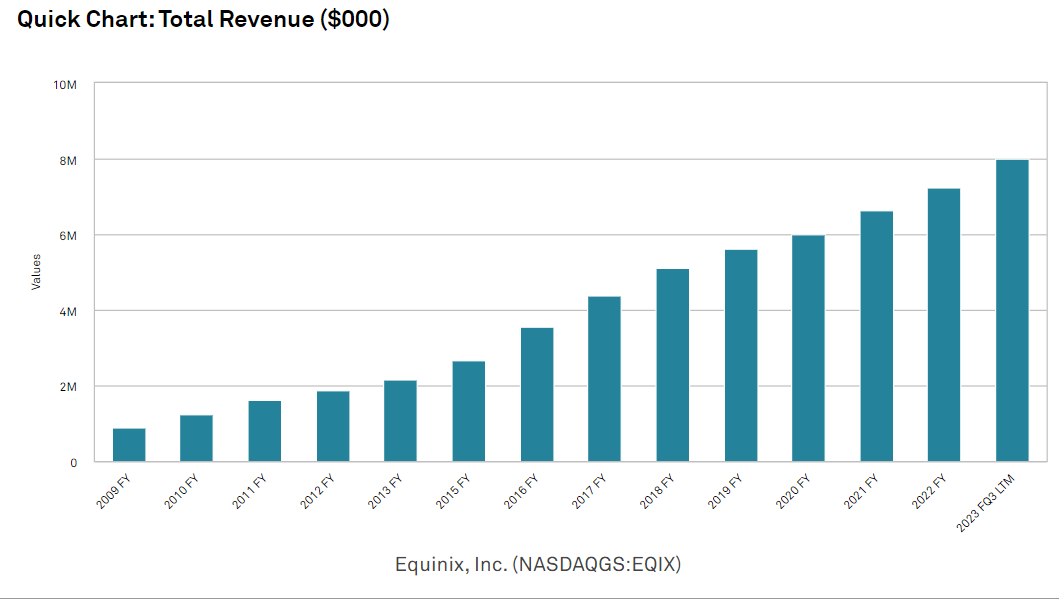

Equinix, Inc. ( EQIX ) is the world’s leading data center provider, with 204 hubs across 5 continents. Its facilities house 1800 network service providers, with cross connections between them. It has been rapidly growing fundamentally and has been a clear winner, up 23,292.87% over the past couple decades.

{kind=link}

While it clearly would have been better to buy in 2003, that is not a decision that is available today. Thus, this article will discuss the merits of buying EQIX today at around $811 per share.

The Buy Thesis

EQIX trades at a fairly high multiple of 24X forward adjusted funds from operations, or AFFO, but this is rather cheap relative to EQIX's recent history. It is also cheap relative to what we see as the forward growth rate. EQIX is positioned to outgrow peers due to the following advantages:

- Superior property level operating margins

- Phenomenal cost of capital

- Significantly higher profit margin at REIT level

- Operating superiority stemming from

- Cross connect ecosystems

- Global presence facilitating single source provider

- Ease of setup

- Customizability of setup

- Speed of deployment.

We will discuss these in greater depth below and then follow with analysis of valuation, adjustments we would make to reported AFFO, and risks to investment in EQIX.

Property level operating margins

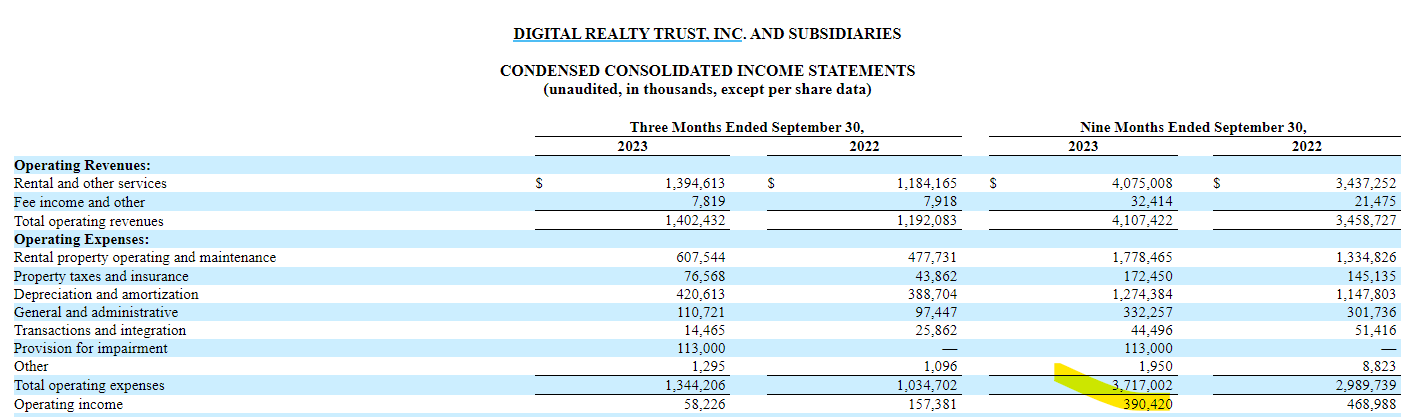

EQIX’s largest competitor is Digital Realty ( DLR ), which has a $5.476B annual revenue run rate. Below is the latest DLR 10-Q , which shows an operating margin of 9.5%.

{kind=link}

Equinix has a similar scale with $8.1B in annualized revenues, but its margin is significantly higher, coming in at 18%.

{kind=link}

Despite having higher AFFO and higher revenues, EQIX actually has less assets on the balance sheet than DLR. Thus, the margin difference is not an advantage of scale, rather it seems to be superior operations.

The higher property level operating margin is compounded at the real estate investment trust, or REIT, level by EQIX’s phenomenal cost of capital.

Lowest cost of capital available

As you know, there are 2 components to cost of capital for a REIT; Equity capital and debt capital.

At a forward AFFO multiple of 24X, EQIX’s cost of equity capital is just over 4% (100 divided by 24).

While it is beneficial to the REIT to have a cheap equity cost of capital, I don’t see that as necessarily beneficial to shareholders because it mathematically means a high earnings multiple (AFFO in this case).

The real benefit to shareholders comes from a REIT having access to cheap debt capital, and in this category EQIX is unmatched. Having studied the REIT universe for the last 12 years, I don’t think I have ever encountered a REIT with such a large amount of debt this cheap.

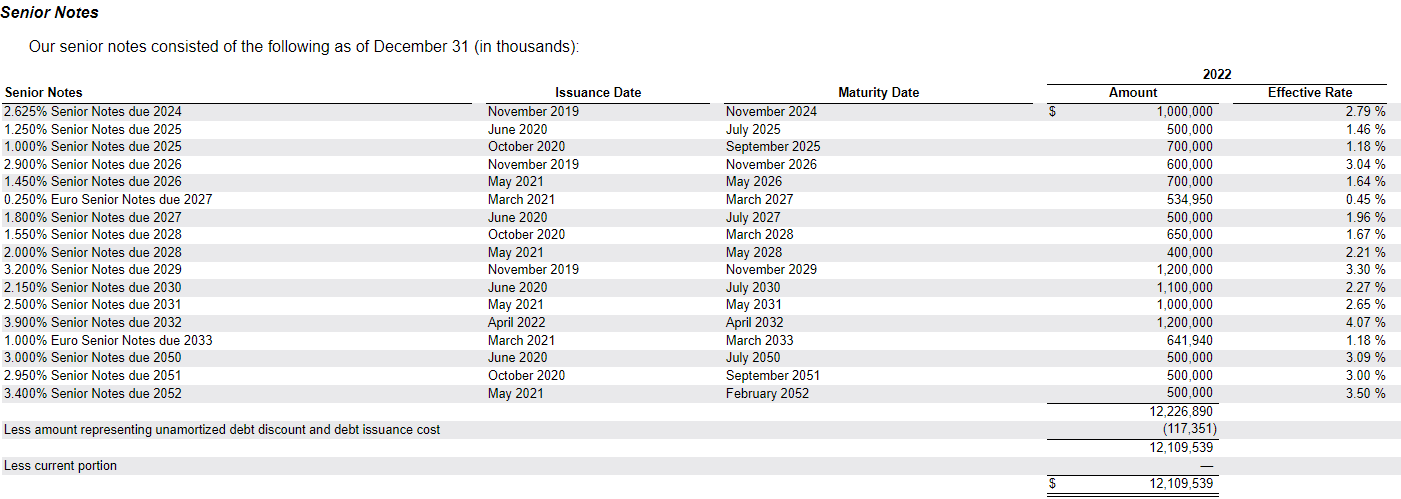

Here are EQIX’s senior notes.

{kind=link}

- The weighted average cost is 2.25%

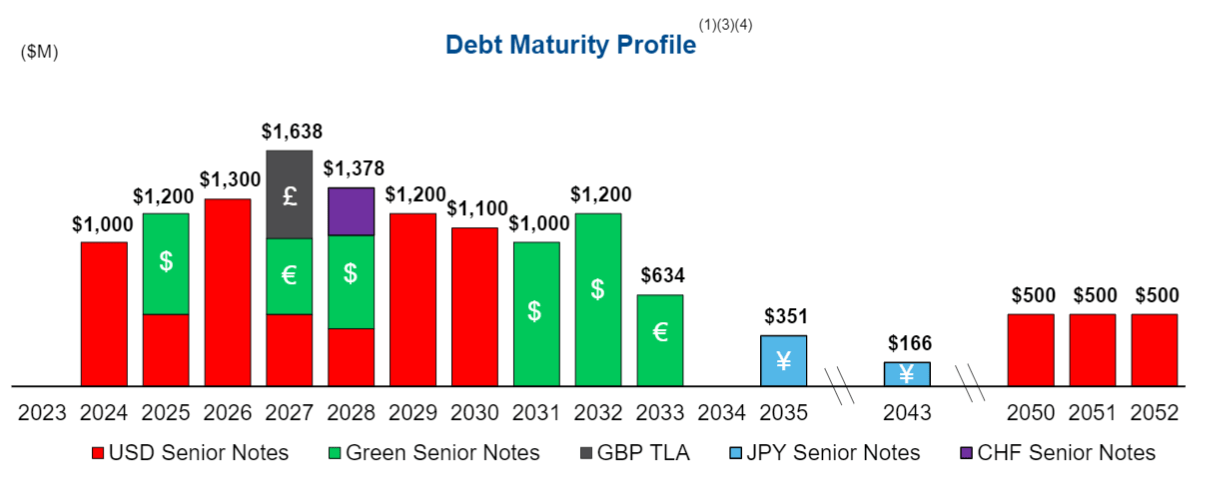

- The maturity schedule is well laddered going out to 2052.

Perhaps it is less relevant than the weighted average, but they have $534 million of debt due in 2027 at 0.25%!

How does Equinix get such a low cost of debt?

Well, there are 3 reasons:

- Low overall leverage at 20% debt to capital supports a BBB stable outlook credit rating.

- Equinix’s global presence facilitates Euro denominated notes which tend to be cheaper.

- Equinix has a green reputation with regard to energy sourcing.

Whether one cares about green policies or not is irrelevant to the thesis. I am referring to the financial impact of EQIX checking the green boxes.

On December 20 th , 2023 EQIX announced the allocation of $4.9B of Green Bonds. The capital from Green Bonds is extremely cheap, but has to be allocated exclusively to approved projects. EQIX is able to meet those qualifications, so it gets the extremely cheap debt. Green notes are a significant portion of EQIX’s capital structure.

{kind=link}

Cheap debt results in higher AFFO margins.

EQIX’s AFFO annualized run rate is $3.06B against $8.1B of revenue. That is an AFFO margin of about 38%.

In comparison, DLR has an AFFO annualized run rate of $1.75B against $5.476B revenues for an AFFO margin of about 32%.

(Note that the reason AFFO margins are higher than operating margins is largely because of depreciation and amortization. We will delve deeper into the intricacies of AFFO accounting later in this article.)

Better operations and a cheaper cost of capital are causing Equinix to outperform with higher margins.

Evidence that EQIX operations are superior

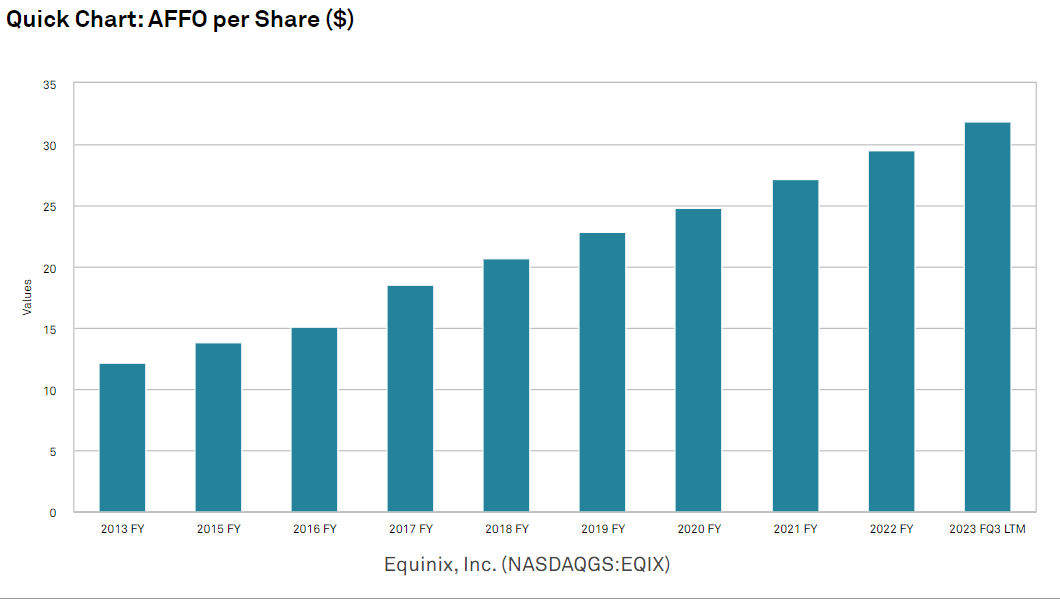

Beyond the margin data, EQIX’s history is evidence of its operational strength. AFFO per share has grown like clockwork.

{kind=link}

The Wall Street Analyst consensus is calling for continued AFFO growth through 2026 and probably beyond, that is just how far the consensus numbers go.

{kind=link}

I believe the operational strength is a result of multiple factors, with some of the bigger ones being:

- Cross connection ecosystems

- Global presence facilitating single source provider

- Ease of setup

- Customizability of setup

- Speed of deployment.

When an enterprise, Internet service provider or other data center customer has data needs, they usually need a solution right away. Speed and accuracy of deployment is a big deal.

Equinix is set up to provide what is termed IaaS, or Infrastructure as a Service. A customer can go up to Equinix’s website and select where they want to be based, how much capacity they need, and with whom they want to cross connect.

With high end data centers across all the major global data hubs, Equinix can be a one-stop solution, allowing its customers to meet all data center needs in one place regardless of where they are located.

These ease of set-up features likely help EQIX lease up data centers faster and keep them leased, but the bread and butter of EQIX is its cross connection ecosystem. To understand why this is so valuable, let me first dig into the competitive landscape as it relates to new supply.

Positive Network Externalities and how they counter new supply

The physical data center is fairly generic. Lots of companies can and do build data centers.

SDX central predicts that :

“between 2022 and 2026 [ ] the number of operational hyperscale data centers is set to jump by 50%.”

The hyperscale cloud companies like Microsoft (MSFT) and Google (GOOGL) are increasingly building their own data centers. There is very little that is special about the physical structure.

Data centers are often used as bulk commodity infrastructure where the entire facility will be leased to a large tenant. In these cases, the tenant is interested in the raw power of it.

- Energy availability

- Number of cabinets

- Other capacity factors.

The lease rates on this sort of commodity data centers are often fairly low, and are kept low by the fact that the tenant can simply build their own. If the landlord tried to jack up rent, Microsoft simply leaves and constructs a new data center. It is a simple matter of whether the rent or the upfront capital is a better financial choice.

Thus, new supply will perpetually threaten commodity data centers. Historically, Digital Realty has struggled to maintain lease rates because its tenants hold the power to just build their own data centers. I don’t really like the commodity data center business model. I think it will consistently be fairly low margin upon stabilization.

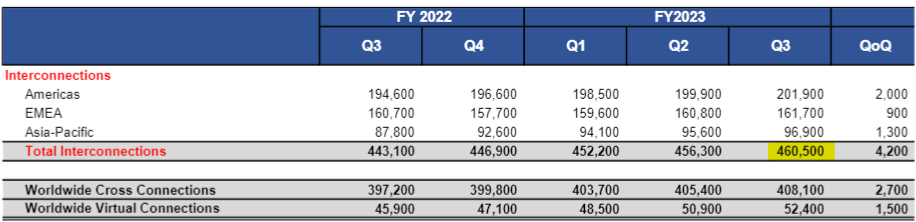

Equinix is different, as its data centers are focused on cross connections.

{kind=link}

Cross connects allow tenants to connect to one another directly such that they can have near 0 latency. This makes the data center more valuable than the raw equipment.

Leasing a newly built data center, you just get equipment. Leasing a EQIX data center provides access to cross connect with essentially any major company. It flips the power dynamics in Equinix’s favor and makes them highly resistant to new supply.

The cross connection ecosystem becomes a positive network externality making the EQIX data center more valuable to a new tenant the more existing tenants there are. This makes tenants stickier and allows EQIX to charge higher rent in addition to collecting revenues on the cross connections themselves.

Due to superior operations and its cross connection ecosystem, I think EQIX is positioned to continue its growth trajectory. With that in mind, let’s take a look at its valuation.

Valuation

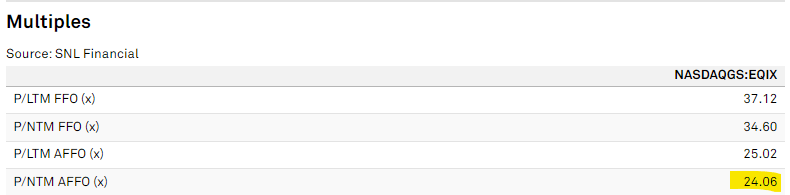

EQIX trades at 24.06X forward estimate AFFO.

{kind=link}

DLR trades at 21.5X forward AFFO.

I think the premium of 3.5 turns of AFFO is well worth it given the vast difference in quality. So, on a relative basis, EQIX is the clear choice among the data center REITs. Thus, the choice for me is between investing in EQIX or simply not investing in pure-play data center REITs, as they are the only 2.

It is a matter of discerning whether it is worth paying the high multiple to get Equinix’s growth.

In looking into the accounting, I think Equinix’s true multiple is actually a fair bit higher than the reported AFFO multiple. There are some add-backs in AFFO that, while common, are not ideal.

AFFO intricacies

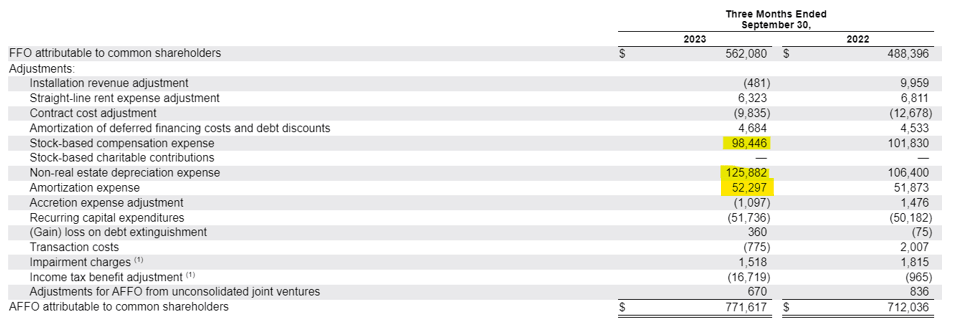

Shown below is EQIX’s reconciliation of FFO to AFFO.

{kind=link}

There are 3 lines items in here that I think need adjustment to get to true earnings.

- Stock based compensation, or SBC, is a real expense. EQIX is a tech company and it is vey common for tech companies to have high stock comp, but the dilutive cost is functionally the same to shareholders as if it was cash compensation. AFFO should be lower by $98.4 million.

- Non-real estate depreciation expense: The real estate of a data center is durable and will last quite a long time. It makes sense to add back real estate depreciation. Non-real estate tends to actually lose value. Equipment, vehicles, solar panels, and other such things significantly degrade over time and will need to be replaced. The accounting speed of depreciation tends to be faster than the actual depreciation, so not all of this is a real expense, but I would estimate roughly half of it is. AFFO should be lower by $60 million.

- Amortization expense is deducted from AFFO because it is a cash expense and AFFO is meant to reflect cash flows. However, cash being used to paydown debt or other amortizing instruments is not a real expense because it also reduces liabilities. This should be added back to AFFO to get to true earnings. +$53 million to AFFO.

Putting these together, I would calculate true earnings at roughly $666.2 million. That is 86% of AFFO.

Adjusting the multiple to true earnings, EQIX is trading at 28X true earnings.

That might not be all that expensive compared to its fellow Nasdaq stocks, but it is a fairly expensive REIT given that the REIT index is around 15X.

Cheap relative to its own history

Equinix has traded down about 4% in the last 2 years.

{kind=link}

During this time, AFFO has grown significantly.

Higher AFFO and a slightly lower price means the multiple is significantly lower than it was 2 years ago.

This pause in market price presents a cheaper than usual multiple at which to buy EQIX. It can be quite difficult to get in to high quality stocks like EQIX that consistently trade at high multiples, so this pause in its market price might represent a relatively favorable entry point.

Valuation relative to growth

EQIX, according to consensus estimates, is consistently growing at 8% to 15%. I think the consensus numbers are largely right in the near term and that is roughly appropriate growth relative to the 28X true earnings multiple.

I think the factor that makes EQIX a buy rather than fair value is that most companies growing at that pace can only do it for maybe 5 years.

I believe Equinix’s growth has a much longer runway which will allow it to outgrow what is implied by the multiple. As such, I think EQIX is trading below fair value and has the potential to deliver a strong total return to shareholders who buy at the current price.

Risks to thesis

Allow me to open with a risk factor that I actually do NOT think is a concern and then follow with the areas in which I am more concerned.

Pull forward of revenues

In many companies, the AI boom has pulled forward some revenues. The concern would be that AI players overspent on infrastructure needed to build their platforms such that future capex might be lower. I think that is the case for many input products of AI, but it does appear to be the case for EQIX. Its revenue has been steady state.

{kind=link}

That is about as consistent as growth gets, so it does not appear as though revenues were pulled forward. Instead, I think it will be a smoother and more consistent demand driver.

Geopolitical tensions

So far, EQIX’s global presence has unequivocally benefitted its operations. The Internet has largely been open across national barriers. EQIX specializes in providing that global interconnection, so it would be disproportionately hurt if countries started to put up digital barriers to international connections.

I have no way of estimating the probability of such an outcome, but I think shareholders should keep an eye on geopolitical tensions, particularly as it relates to the digital realm.

ETF drag down

The Nasdaq had a monstrous 2023 with extreme gains. In my opinion it has become significantly overvalued and is due for a pullback. As a constituent of the Nasdaq, Equinix is in many of the same ETFs, which suggest a significant selloff in the sector could have some impact on the market price of EQIX.

Wrapping it up

Equinix, Inc. represents the pinnacle of data center operations, making it our top pick in the sector. While its multiple is somewhat high, I think the long runway of growth will quickly overcome the initially expensive price.

For further details see:

Equinix Is Expensive, But Worth It