DLR - Equinix: One For The Watchlist

2023-09-19 17:37:38 ET

Summary

- Equinix is a dominant player in the data center industry, and will benefit from the rapid pace of digital transformation.

- We touch upon a few favorable facets of this story.

- Even though we like this story, we are not too enthused with the current valuation and technical backdrop.

Why Equinix Should Be On Your Watchlist

Digital transformation is snowballing by the day (reportedly growing at 8x the pace of the broader economy according to IDC), and data-center REITs such as Equinix, Inc. ( EQIX ) can serve as a decent proxy to ride this wave, given how central they will be in the housing and support of digital information. To get a sense of the rapid pace of digitization, one may consider perusing the latest Global Interconnection Index (GXI) report which states that in less than two years, 90% of all Fortune 500 companies will be selling and consuming digital services.

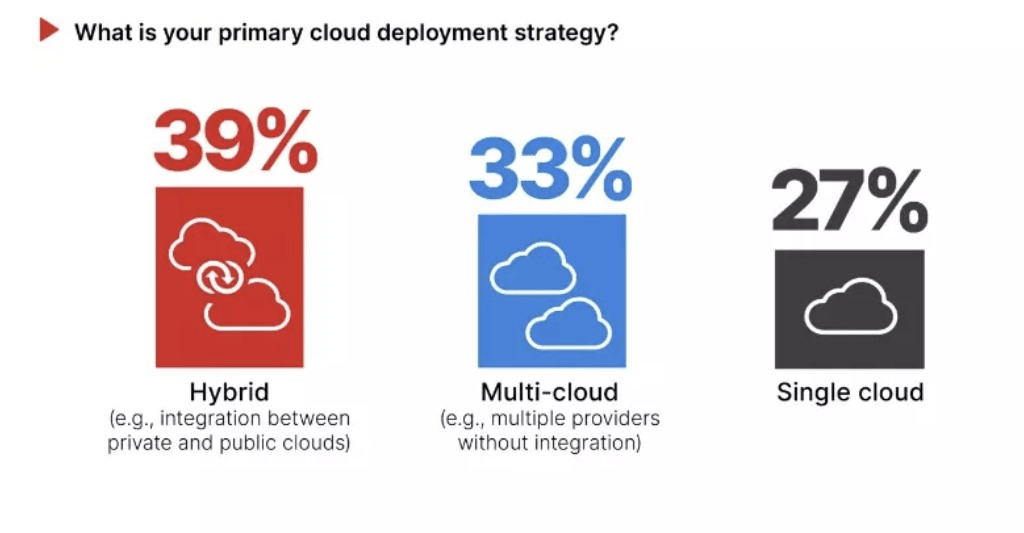

If the pace of digital transformation remains resilient (it is likely to account for 55% of all Information and Communication Technology Investment by the end of next year), it effectively means that you will see a greater chunk of enterprises distributing their applications across multi-clouds or a mix of private and public clouds. Just to ensure business continuity, we’ve already seen close to three-fourths of enterprises already pursuing a hybrid-cloud or multi-cloud strategy, and something like Equinix’s platform which spreads its tentacles across three broad geographic regions (AMER, APAC, and EMEA) and 70 metros will attract a lot of dollars. For context, note that since 2018, Equinix’s customers that have resorted to single-metro deployment has only grown by 3%, whereas those demanding deployment across multi-metros has grown by 46%! As things stand, close to 67% of EQIX’s recurring revenues come from customers deployed in all three regions.

{kind=link}

This ongoing thrust of higher digital transformation coupled with the need for growing AI training demands, will certainly also put pressure on the nature of CAPEX and acquisitions that EQIX will have to indulge in, going forward. EQIX plans to add around 30,000 retail cabinets by the end of next year, but in the new paradigm, clients' power and cooling requirements on a per-unit basis will likely be more demanding (could be over 2x what the previous IBX data centers could provide), and EQIX will have to adapt accordingly. For instance, EQIX management did touch upon their intention to embrace liquid cooling technology with not just their existing capacity, but for their future designs as well. All in all, the CAPEX threshold could likely step up (management pegged it at around $3bn p.a through FY27).

Needless to say, in order to successfully fulfill these growth and capacity ambitions, incumbents in this space will need to have a robust balance sheet, with solid coverage levels, and that’s where EQIX has an edge over its public peers such as Digital Realty Trust ( DLR ). Equinix’s net leverage ratio of 3.6x is substantially lower than DLR’s figure of 6.8x, and the former also does a far better job in generating ample EBITDA to cover its interest bill ( 9.2x ). The other key differentiator is that EQIX only pays out 43% of its AFFO as dividends, compared to 78% for Digital Realty, providing some context on the quantum of funds that gets reinvested back into the business to fulfil its growth objectives.

Earnings transcripts and filings

Given the demand for data center services, this is also one of those businesses that can implement a healthy dose of price increases, without fretting over losing too many clients. Around five years back, net pricing effects were only around 3% or so, but these days it is 2x as much (on the Q2 call, management described pricing as “ very firm ”), yet the net churn rate for EQIX, as a function of their monthly recurring revenue has been rather minuscule at less than 2.5% (In Q2 it was 2.3% and by the end of the year, it is expected to drop to 2%).

Analyst Day Presentation

Closing Thoughts - Why Equinix Stock Isn’t A Buy At This Point

Whilst the Equinix story looks tantalizing on paper, we don’t believe the stock warrants a BUY rating at this juncture. Here are a few reasons why we are less bullish.

Given how well-placed data center REITs look to exploit the tailwinds from a burgeoning digital and AI wave, it’s perfectly reasonable to expect a premium multiple, but do consider that EQIX is currently priced at an exorbitant forward price to FFO multiple of over 35x, which translates to 3x the median multiple of the entire REIT sector. We are not sure that can be justified.

Besides, even compared to the other major listed player in this space- (Digital Realty), EQIX’s forward multiple translates to a massive 81% premium, with DLR trading at only 19x. One could perhaps make allowances for this massive variance if EQIX's medium-term growth runway was drastically different from DLR, but consensus estimates show that EQIX will generate FFO CAGR growth of less than 9.5% through FY25, which is not even 200bps more than what DLR is poised to deliver across the same period ( 7.6% ).

Seeking Alpha

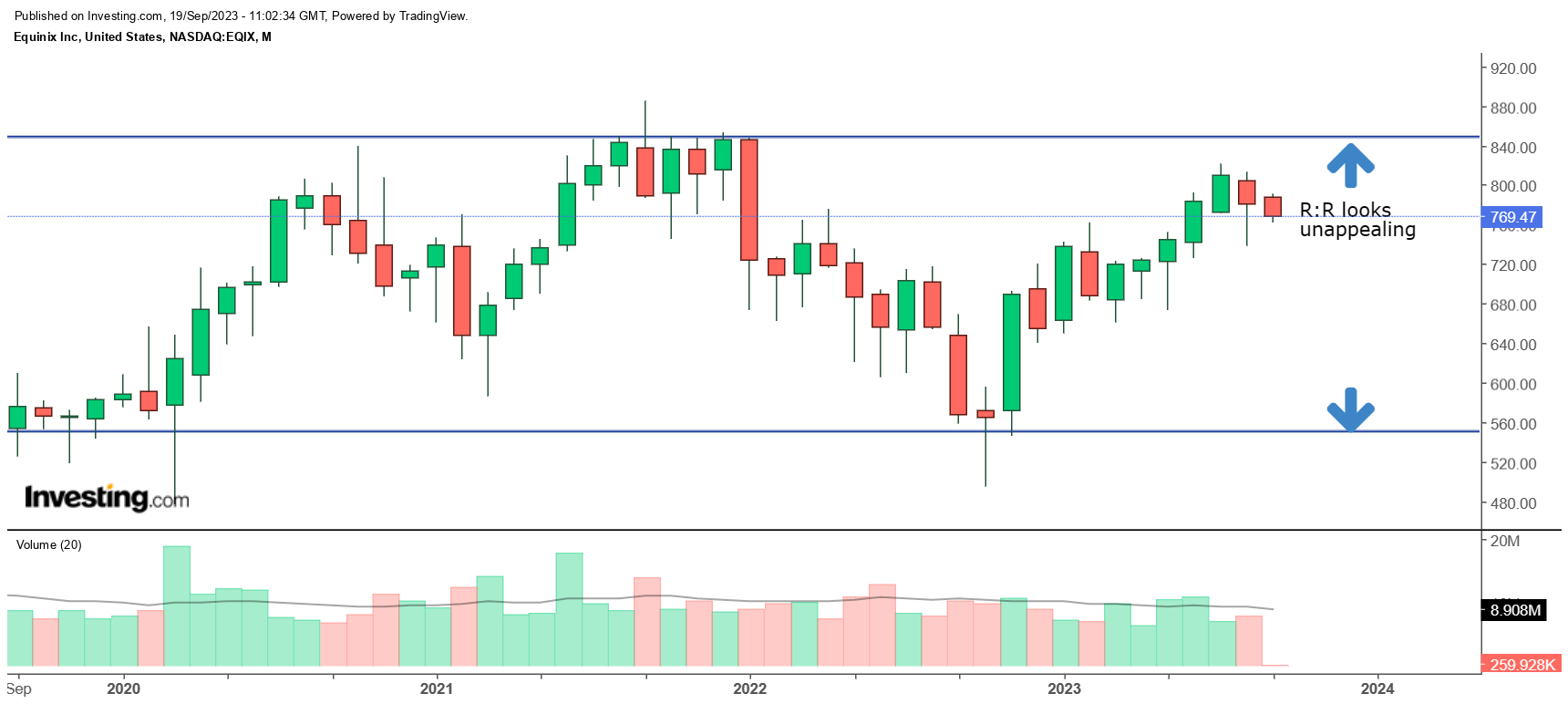

Then, if we review EQIX's stock price imprints over the last four years, we can see that it tends to chop around within an approximate range of $550-$850. Now after a pretty strong uptrend since November 2022, the stock looks ripe for a pullback or a bout of consolidation, rather than persist with yet another unidimensional uptrend. Regardless, even if one wants to dismiss the prospect of a pause, and use the range levels as pivot points, an entry at current levels would translate to a pretty underwhelming reward to risk of less than 0.4x.

{kind=link}

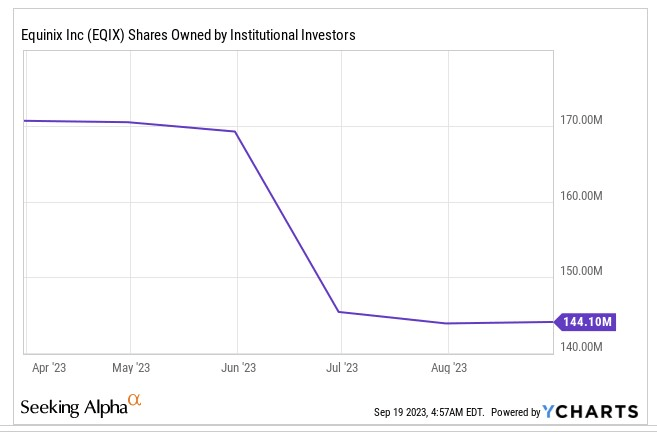

The lack of bullish sentiment is further validated in the positioning of notable stakeholders. Firstly, consider that the smart money who is typically responsible for large moves in a stock, have actually been trimming their stakes in Equinix in Q3. The total net shares owned by this cohort is down by -15% in recent months.

{kind=link}

There’s also something to be said about the ferocity of insider selling witnessed last month, and this, after a month (July) where there were no insider trades at all.

Barcharts

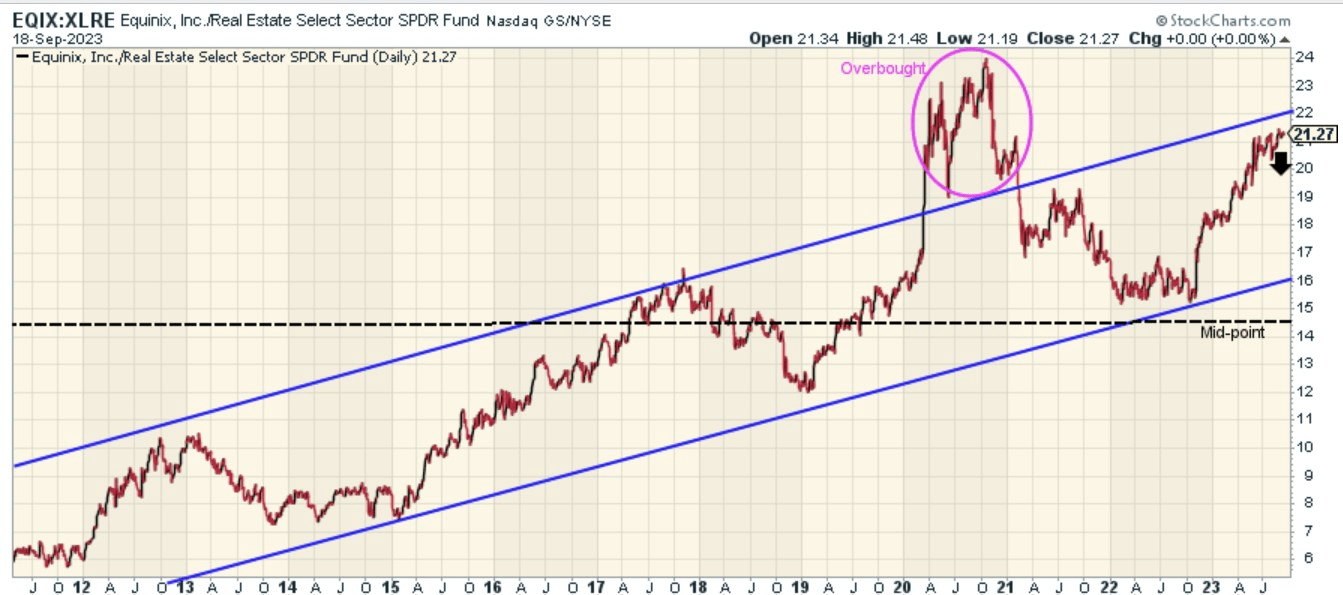

Then, would EQIX appeal as a rotational play for real-estate-focused investors? Well, the chart below suggests that is unlikely to happen as EQIX's relative strength as a function of the popular XLRE ETF is currently not only well past the mid-point of its long-term range, it is also near the upper rail of an ascending channel trend that has largely played out well since 2012.

{kind=link}

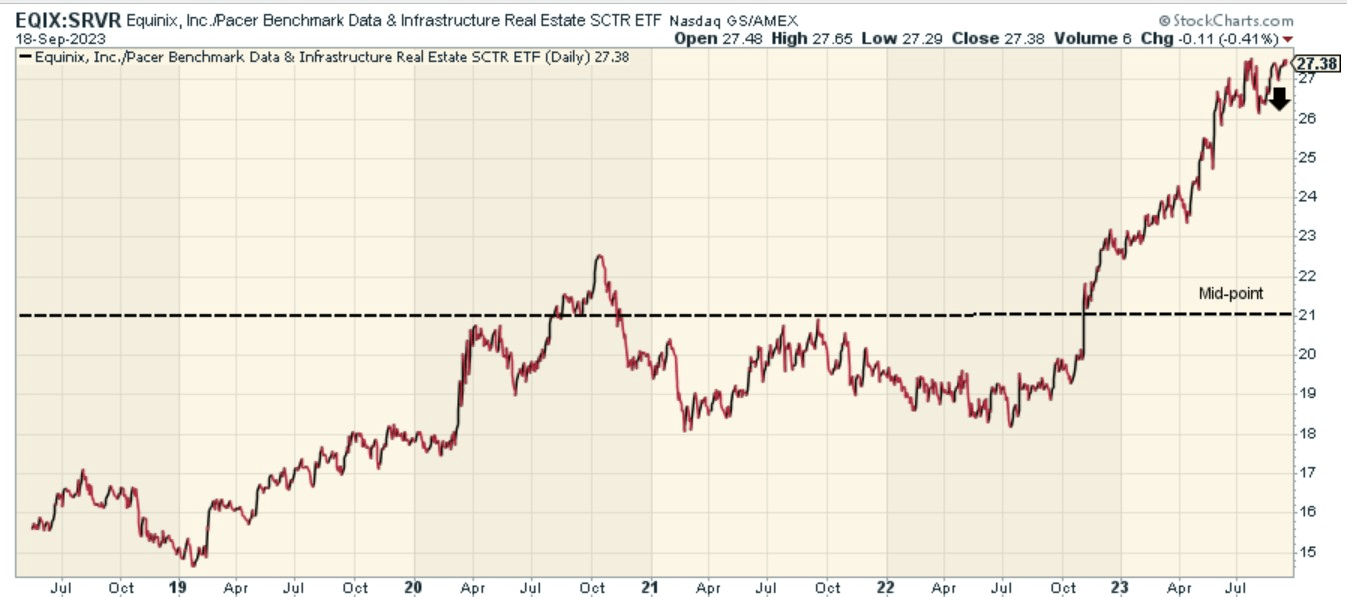

Well, if you happen to be more nuanced, and only want to focus on EQIX’s closest peers from the data center and infra space, we could look at EQIX’s positioning versus its peers from the Pacer Benchmark Data & Infrastructure Real Estate ETF. Here, EQIX’s overbought nature is only more obvious, dampening the allure of a long position.

{kind=link}

For further details see:

Equinix: One For The Watchlist