EQNR - Equinor Is A Long-Term Winner And Should Trade Much Higher

Summary

- Equinor is a winner in geopolitical tensions. In view of this, the share has not yet moved very much.

- The share has priced in a drop in oil and gas prices. Should this occur, however, the risk of a sharp drop in the share price is low.

- However, if the prices remain permanently higher, the share price should catch up strongly when the market realizes this.

- The stock trades at a long-term average P/E of 13. Currently, it stands at 5.4.

- So I think the risk is low, but the upside is high, with a very good risk/reward ratio.

Investment Thesis

Since the Ukraine war and the almost completed energy separation of Europe from Russia, it seems to be a no-brainer to invest in the gas suppliers of Europe. These include LNG suppliers from the USA, among others, but the most apparent supplier for Europe is Norway and thus Equinor ( EQNR ). I think the market expects too much that oil and natural gas prices will fall sharply next year and the year after. In other words, the market underestimates the EPS outlook for Equinor. Since this is already priced in, there is little downside risk, but if things turn out differently and oil and natural gas prices remain high, the share still has much room to move upwards.

Europe will buy everything at any price

I want to avoid repeating too much here; probably, most of you reading this article know about Europe's overall situation. Just a few remarks. Since I come from Germany and like to be prepared, I have been very busy with energy in the past months. It became clear to me that the biggest problem is not this winter, as last summer, they managed to get the storage relatively full due to flowing Russian gas supplies. Russian gas has been flowing for the longest time, and yet we are now in a situation in Germany where it is said that we will only make it through the winter if we save 20-30% gas.

The challenge will be to fill up the storage again next summer to be prepared for the winter of 2023. And this pattern could repeat itself for years to come. At the moment, LNG terminals are being built, but most likely, there will need to be more supply. Not only do we need more LNG terminals but also more ships . By blowing up the Nord Stream pipelines, Europe has also been deprived of a Plan B. No matter how you look at it, gas remains a scarce commodity, and new supply chains are very inefficient. LNG ships sailing thousands of kilometers is very inefficient compared to pipelines. Russia will probably sell gas to third countries, which will sell to Europe. This was already happening through China and happened throughout the summer with Russian oil . These trades make the deliveries much more inefficient and, therefore, more expensive for Europe.

Eventually, Europe will buy everything possible from reliable and local Norwegian sources. You could say that for Equinor itself, nothing has changed, but around it, there is suddenly much more inefficiency and supply shortage, which drives up the prices from which Equinor benefits. Probably prices will remain permanently increased compared to 2019. At least at the moment, I can't see anything that should push the prices back to such low levels. No LNG ship can compete with Russian pipeline gas, which was also delivered under long-term supply contracts.

Russia's invasion of Ukraine impacted already tight energy markets and has created an energy crisis with high prices affecting people and all sectors of society. Equinor puts its best effort into securing safe and reliable deliveries of energy to Europe, whilst continuing to invest in the energy transition.

Anders Opedal , president and CEO of Equinor ASA

Strong balance sheet and profitability

The first thing I like very much is the enormous safety of investing here. According to Equinor's Q2 report, the net debt ratio is negative 38.6%, meaning they have more cash than debt. Equinor's long-term ratings are AA- and Aa2 from S&P and Moody's, respectively. Profitability also gets an A+ rating in Seeking Alpha's Quant rating.

Valuation

In the following chart, I have added three key figures. Share price, EPS, and forward PE ratio. Here we can see that the share price has increased less than the EPS. This means that the forward PE ratio is lower than in 2021, which probably means that the market does not expect the company to be able to realize the 2022 gas prices in the future.

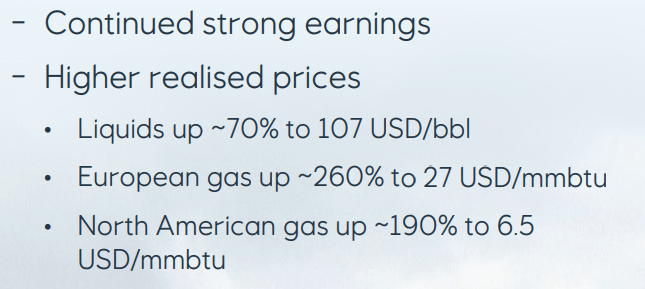

What were the realized prices in the last quarter? We can see that in the following screenshot.

{kind=link}

Let's compare that with current prices. Oil has fallen to 85 USD per barrel. The European Union's natural gas import price for September 2022 was 59.10 USD/MMBtu. However, it recently fell sharply and was at 27 USD/MMBtu a few days ago . Overall, since Equinor's last quarterly report, the price has been significantly above USD 27/MMBtu at times. North American gas is down to $5.70 per MMBtu. So, the company could realize lower prices for oil and gas in North America but higher prices for European gas in the next quarter.

Of course, it is difficult to say how prices will develop in the long term. I assume that we will remain at elevated prices for a few more years and, due to the tight supply, will probably be permanently well above the average prices of 2010 - 2019. A realized price for Europe of $27 is pure money printing for Equinor, and even if prices fall, it would not be a disaster.

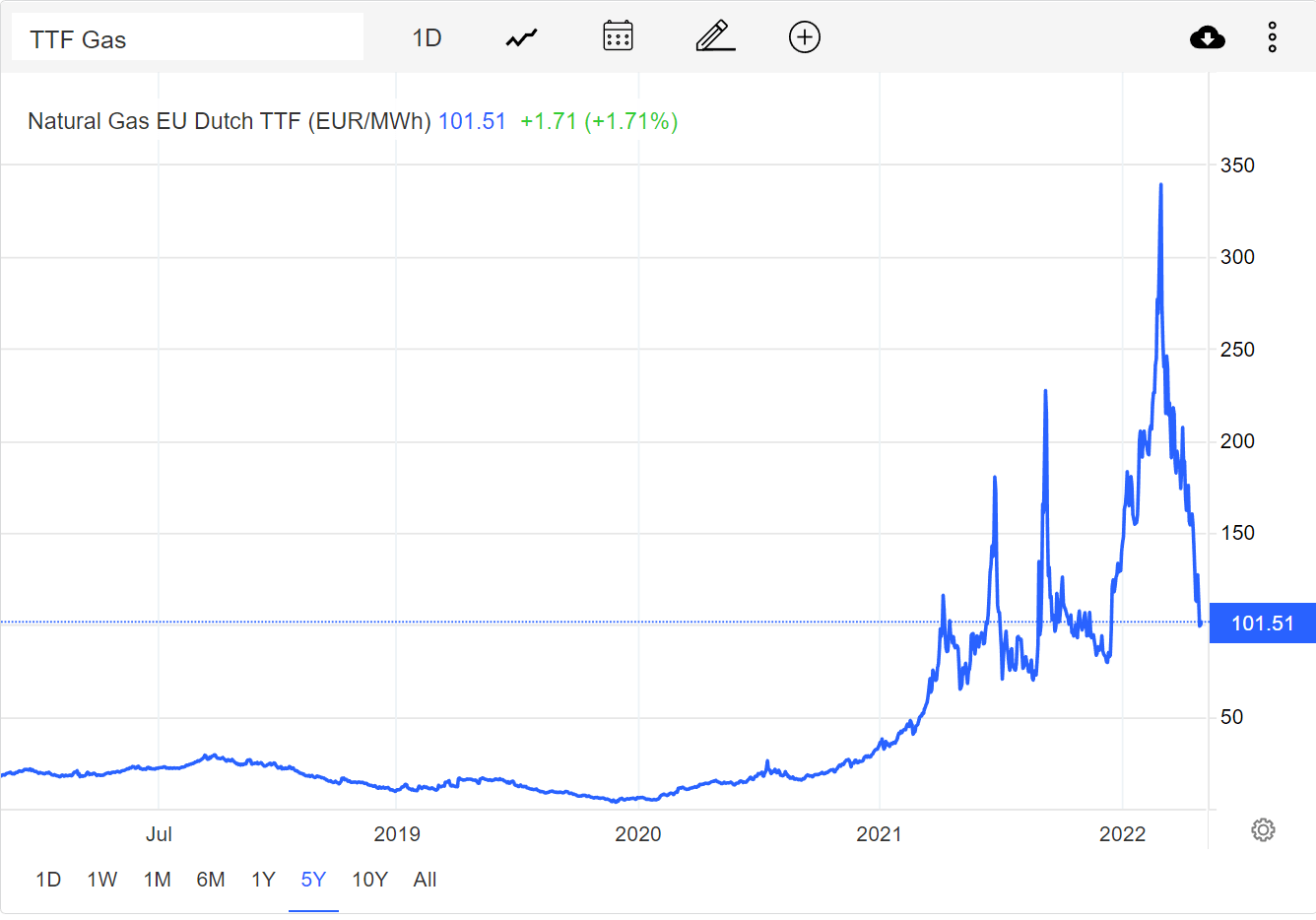

Please look at this 5-year chart (which uses a different unit of measure than $/MMBtu, so the numbers are different, but the ratios are the same). Right now, a big thing is being made of the fact that gas prices have fallen sharply recently, but in the long-term chart, you can see how expensive natural gas still is. In October 2019, the price was 22 euros/MWh, and now five times as much.

{kind=link}

And even with 2019 prices, Equinor has made a lot of money. The stock trades only about 50% more expensive now than at the beginning of 2019, but free cash flow has multiplied. That means the stock trades much cheaper on a P/E or price/free cash flow basis. Probably because the market assumes earnings will return to much lower levels. But given the simply too little supply available, it is extremely unlikely that natural gas prices will return to 2019 levels soon. And even if there is more supply, the competition for Equinor is no longer cheap Russian pipeline gas but more expensive LNG from further away. And there is competition for these ships between Europe and Asia, since LNG is flexible, whereas pipelines are not.

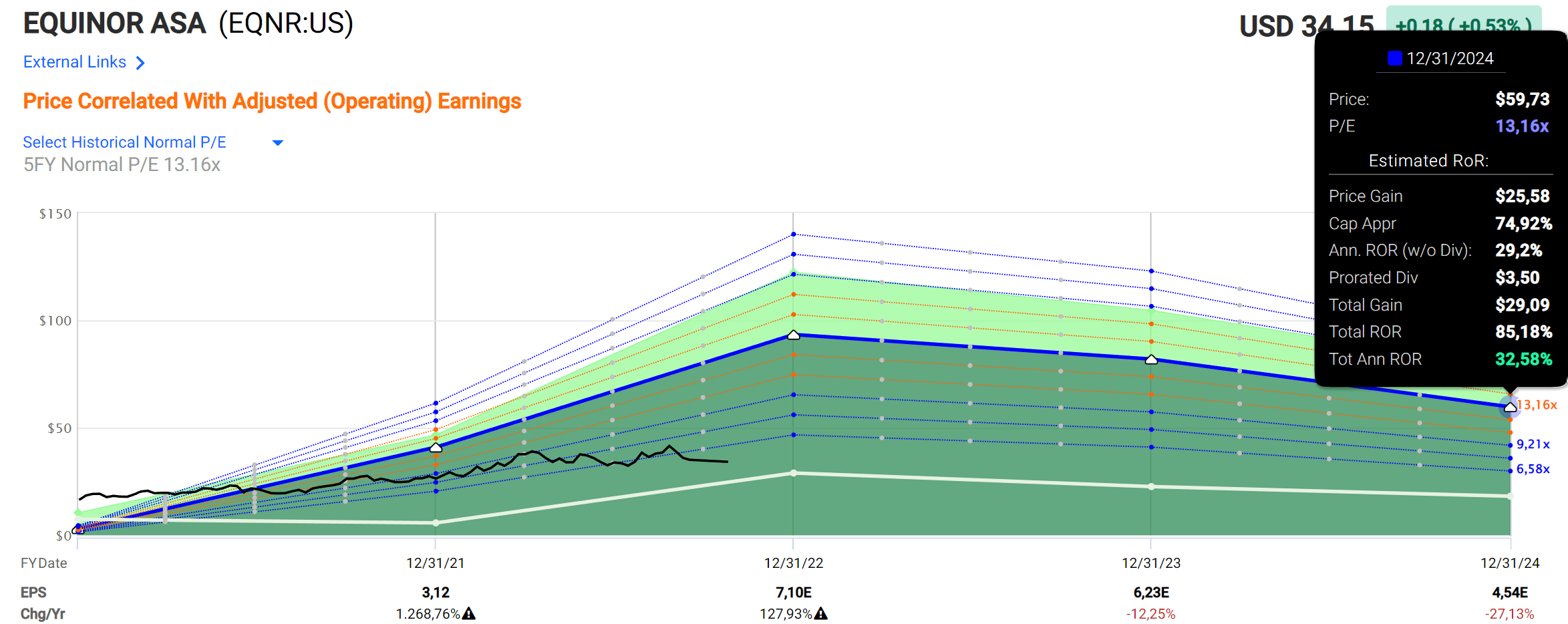

According to fastgraphs, the stock trades at a long-term average P/E of 13. Currently, it stands at 5.4

Even with declining EPS in 2023 and 2024, the stock would still be a tremendously good investment, according to fastgraphs, if it returns to its long-term P/E average.

{kind=link}

And there is a possibility that EPS will not even drop that much. This estimate assumes that oil and natural gas prices will fall sharply again in the long term. The estimated EPS for 2024 are 37% lower than in 2022. If the realized oil prices in the last quarter were $107 per barrel, they should 2024 be $67. Natural gas prices should then be about $17/MMBtu. Of course, this calculation is not exact since it excludes, e.g., CapEx. But approximately, the consideration should be accurate. There is no other reason why EPS should drop so much.

Will we see a sharp drop in oil and gas prices, or will they remain elevated for years to come? I suspect the second. However, it seems to me that the share price has priced in the possibility of a sharp drop in commodity prices. Conversely, if this happens, there is little risk that the share price will crash sharply. However, if the prices remain permanently higher, the share price should catch up strongly when the market realizes this. I suspect, in this case, there will be a permanent re-rating of the stock, and it will probably trade around its long-term average P/E.

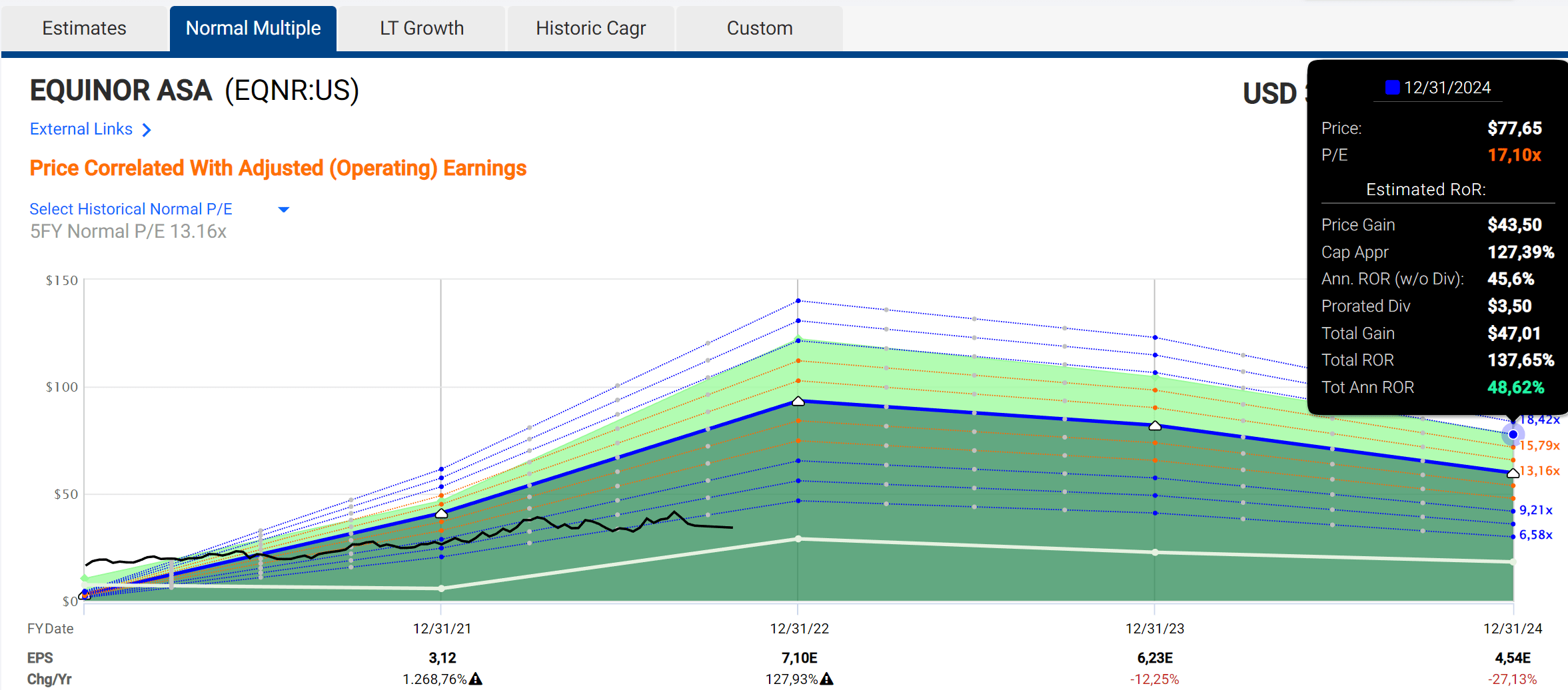

Or put another way, if 2024 EPS were $6 instead of the expected $4.54 and the stock were to trade at its long-term average P/E of 13, the stock price would be $6 x 13 = $78. Then this fastgraph would be the expected return.

{kind=link}

Equinor is more than just a European gas supplier

The company does much more than pump natural gas. I have already mentioned oil, and here Equinor is a significant producer with 870k b/d in Q2. This means that the company's profits will also depend on oil prices. Here, too, I see a tight market for the next few years. If I also go into detail about the developments in the oil market, the article will be too overloaded. For this, there are many good other articles on Seeking Alpha.

Furthermore, Equinor owns gas fields not only around Norway but also in many international countries . However, the Norwegian assets are the most important and bring in 7 times as much revenue as the international fields.

In addition, the company is also producing more and more electricity from wind energy and has described this area as an essential growth driver. The company mainly uses floating offshore wind farms, which are initially more expensive to build but deliver more energy in the long term.

We plan to reach an installed net capacity of 12-16 GW by 2030. Two-thirds of this capacity will be within offshore wind.

{kind=link}

The company also invests in smaller companies through " Equinor Ventures ." One example is the Dutch company Elestor, which develops flow batteries for grid-scale energy storage. In addition, Equinor is also involved in Co2 storage and is part of several hydrogen projects .

Shareholders get rewarded too

For years, the company has regularly launched new buyback programs that give the share price a nice little boost. In 2022, about $6B has been budgeted for this.

The regular dividend is currently $0.20€ per quarter. However, there was an additional payout of another $0.50€ in the last quarter. This additional payment is also planned to be made in Q3. Thus, the total dividend for 2022 is already at least $0.7 + $0.7 + 2x $0.2 (normal quarterly dividend) = $1.8. Based on the current share price, this yield is over 5%.

Risks

Energy prices fluctuate significantly and depend on factors outside of the company's control.

- How is the global economy and, therefore, the energy demand?

- How much are other countries producing?

- How quickly are Europe and the world turning away from oil and gas?

- What is OPEC+ doing?

Equinor's revenues have been fluctuating in the past, and that will continue. Another risk is that future wind farms may not be needed in this form if better power generation methods are found. Possible options are fusion reactors or solar will become much more efficient. Recently, for example, I wrote about NuScale , which is building small nuclear reactors that are supposed to be much safer than traditional nuclear power plants. It has yet to be determined what the future energy mix will look like.

Another risk is an escalation of the conflict between the West and Russia. In this case, Equinor would be one of the most critical energy suppliers for Europe, and pipelines and LNG terminals would be perfect targets. This is a risk that applies to almost every company. In such an escalation, any industry will suffer massive disruptions. Equinor's specific risks here are that there could be isolated attacks on assets without an actual hot war, as happened recently with the Nord Stream pipeline.

Conclusion

Overall, it is such a good investment because it seems to be priced in that commodity prices, and thus, EPS will fall sharply. However, if this does not happen and the market realizes it, the stock has a lot of upside. And even if it does, you still have a good investment in a very safe company whose products are in high demand and which rewards its shareholders.

Overall, analysts believe that we will need oil and gas for several decades to come. The energy turnaround is happening slower than some green parties would like. At the same time, the company invests in new areas, and the shareholder gets rewarded too. Overall, I am confident this investment will generate very good returns for shareholders.

Editor's Note : This article was submitted as part of Seeking Alpha's Top Ex-US Stock Pick competition, which runs through November 7. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

Equinor Is A Long-Term Winner And Should Trade Much Higher