SSRM - Equinox Gold: Getting Saved By The Gold Price

Summary

- Equinox Gold Corp. was one of the worst-performing gold miners in 2022, sliding 51% for the year after an already disastrous 34% return in 2021.

- This disappointing performance was attributed to a significant miss on production and costs, and following this week's report, output massively missing the downward revised guidance by a mile.

- Fortunately, 2023 is shaping up to be a better year, and the company's liquidity situation could be less messy if Equinox can continue to benefit from a $1,825/oz+ gold price.

- However, with Equinox Gold stock up ~80% from its lows and no longer trading at a deep discount to fair value, I don't see any way to justify paying up for the stock here.

As I've warned in past updates , Equinox Gold Corp. ( EQX ) was a risky name to own as of Q2 2022. It was quite clear inflationary pressures were worse than anticipated, and Equinox is a relatively high-volume and low-grade producer. This meant that EQX would be more sensitive to peers when it came to inflationary pressures. It was also suffering from elevated inflation rates in Brazil (which were above the global average), strength in the Brazilian Real, and nearly one-third of production was coming from Guerrero State, which was a less attractive jurisdiction and where the company had seen issues in the past.

Unfortunately, all these issues impacted Equinox last year, with inflationary pressures being stickier than hoped, and the company reported yet another blockade in September at Los Filos. The result? Higher unit costs and lower production. Adding insult to injury, recoveries were weaker than anticipated at Santa Luz, RDM was impacted by the delayed receipt of permits for a scheduled TSF raise, and while Equinox/Orion have managed to evade a capex blowout at Greenstone, unlike other Ontario construction-stage peers (Magino, Cote), the weaker balance sheet has led to some worries about the company's ability to fund all of its obligations without needing to tap its ATM or do a small equity raise.

Fortunately, the recovery in the gold price over the past two months has helped to alleviate some of these worries. Equinox's equity investments have risen substantially in value (which could be partially or fully monetized), and it is in a position to generate up to $200 million in operating cash flow next year, assuming gold prices can continue their ascent. The result is that any potential funding gap to build Greenstone could be avoided without equity dilution or asset sales, which is one reason the stock has underperformed over the past year. Let's take a closer look at recent developments below:

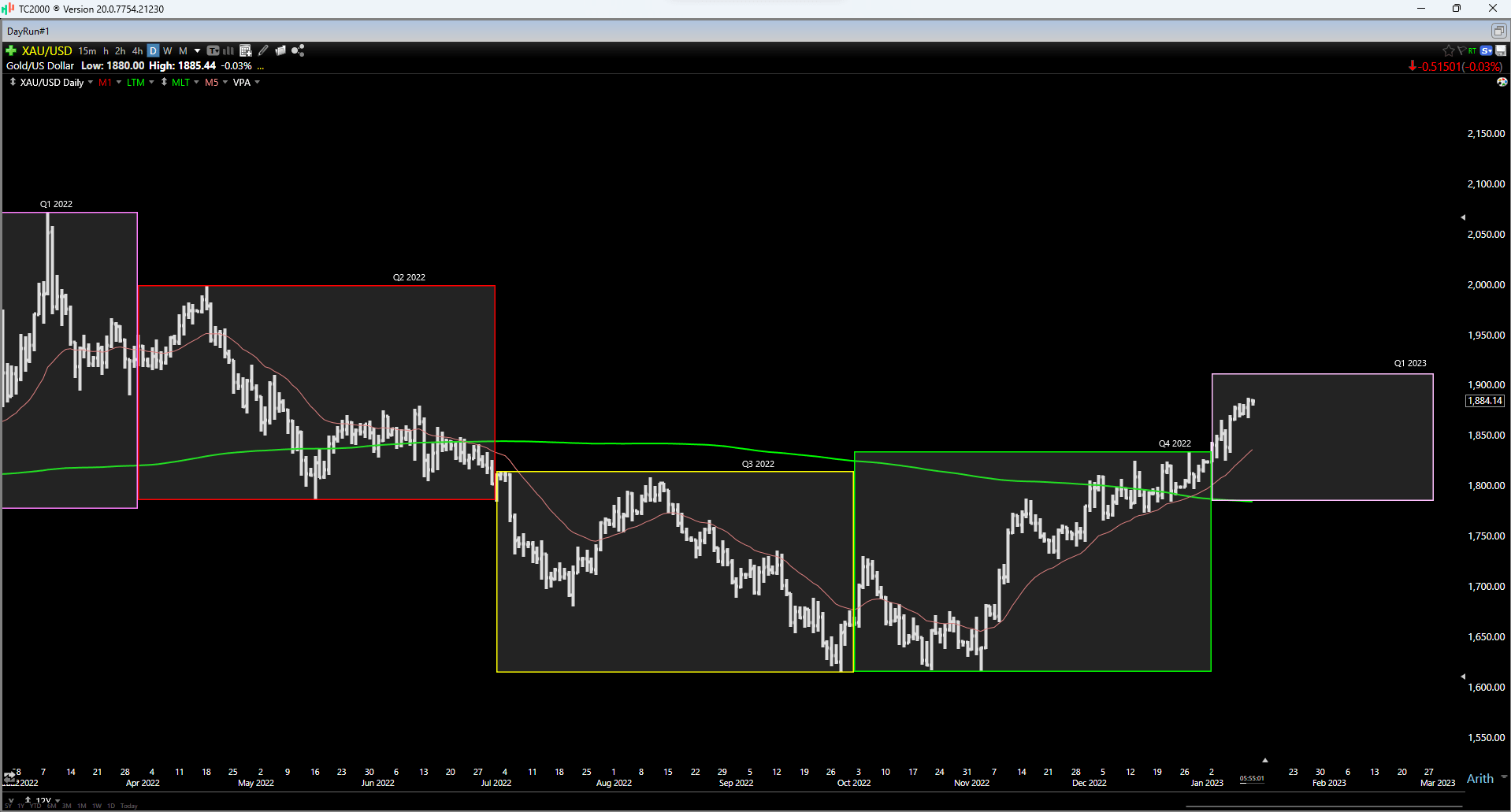

Gold Futures Price (TC2000.com)

{kind=link}

Recent Results

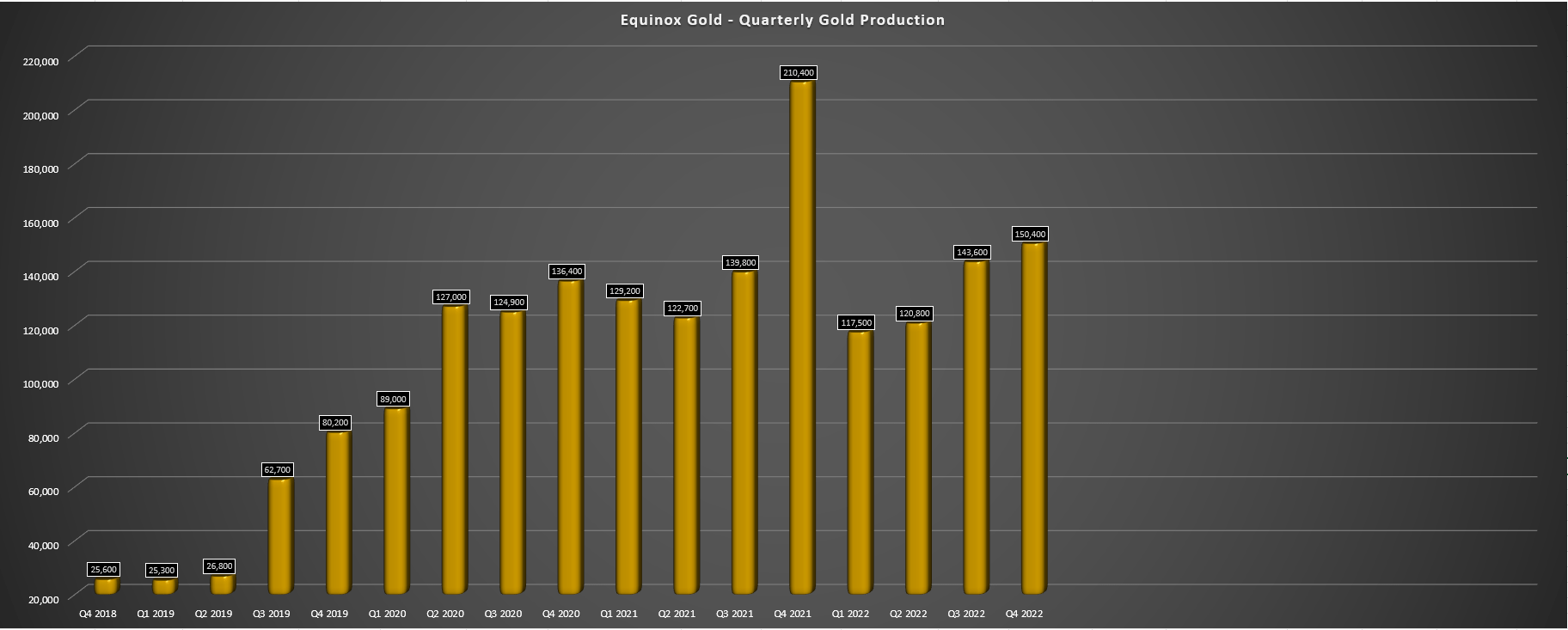

Equinox Gold reported another disappointing quarter in Q4 (~150,400 ounces), with quarterly production coming in well below last year's levels (Q4 2021: ~210,400 ounces), leading to a massive vs. already downward revised FY2022 guidance. While this was partially related to two divestments that included Mercedes and Pilar, it was undoubtedly a challenging year for Equinox, with Santa Luz significantly underperforming expectations, a negative surprise at RDM, and another hiccup at Los Filos due to a temporary blockade. Ultimately, this led to an ~8% miss vs. the guidance mid-point (~582,000 ounces) and a sharp decline in production year-over-year. The result is that FY2022 all-in-sustaining costs [AISC] should come in above the previous outlook of $1,605/oz at closer to $1,615/oz, a ~57% rise from FY2020 levels.

In the company's Q3 results, Equinox noted that "costs were likely to exceed the upper end of AISC guidance of $1,530/oz by approximately 5%".

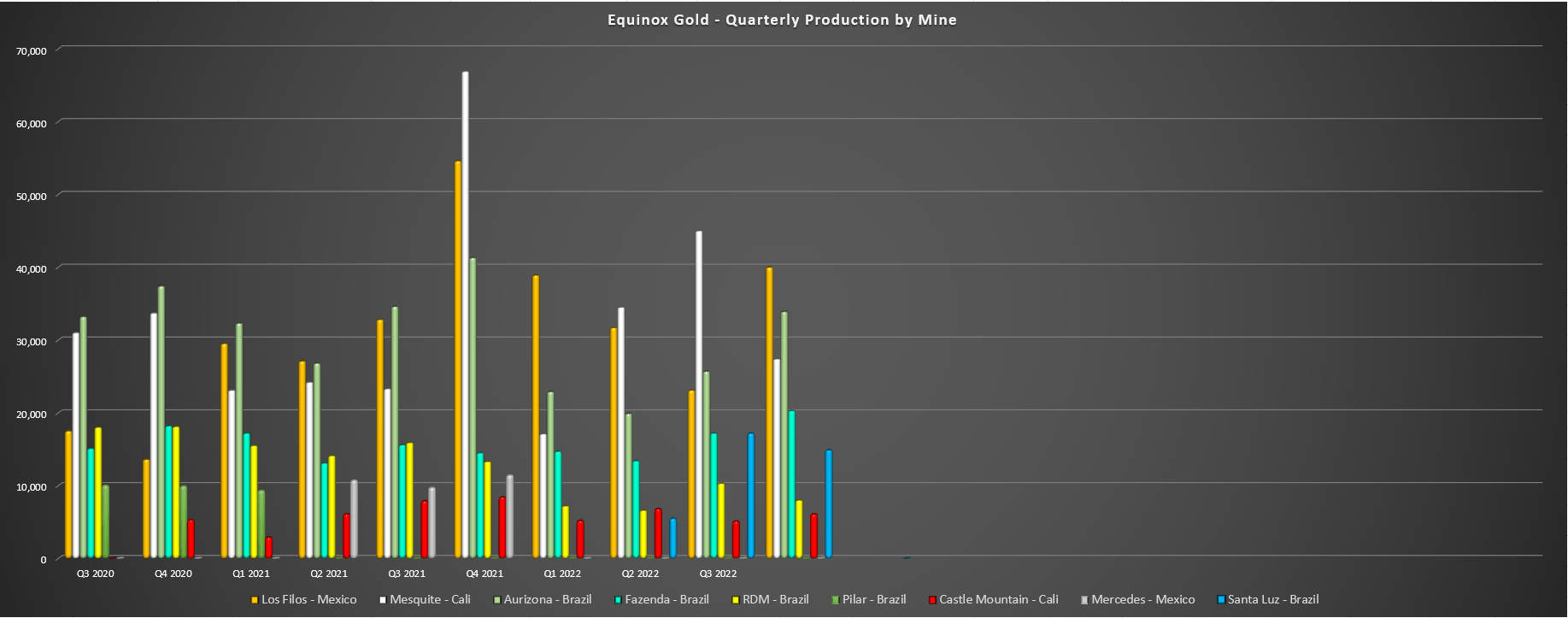

Equinox Gold - Quarterly Gold Production (Company Filings, Author's Chart) Equinox Gold - Quarterly Production by Mine (Company Filings, Author's Chart)

{kind=link}

{kind=link}

Fortunately, there were some bright spots, including that its injury frequency rate dropped substantially, and it ended the year with $700 million in liquidity ($800 million with ATM) after selling part of its position in Solaris ( SLSSF ). Plus, it achieved commercial production at Santa Luz even if performance was well below expectations. Meanwhile, from a development standpoint, the company has commenced permitting for Castle Mountain Phase 2, and its Greenstone Project in Ontario continues to make solid progress (65% complete) and remains on budget. Lastly, it received permits for three portal locations for an exploration ramp ahead of underground development at its Aurizona Mine. These positive developments should provide a significant lift in production later this decade, with Greenstone first on deck in mid-2024.

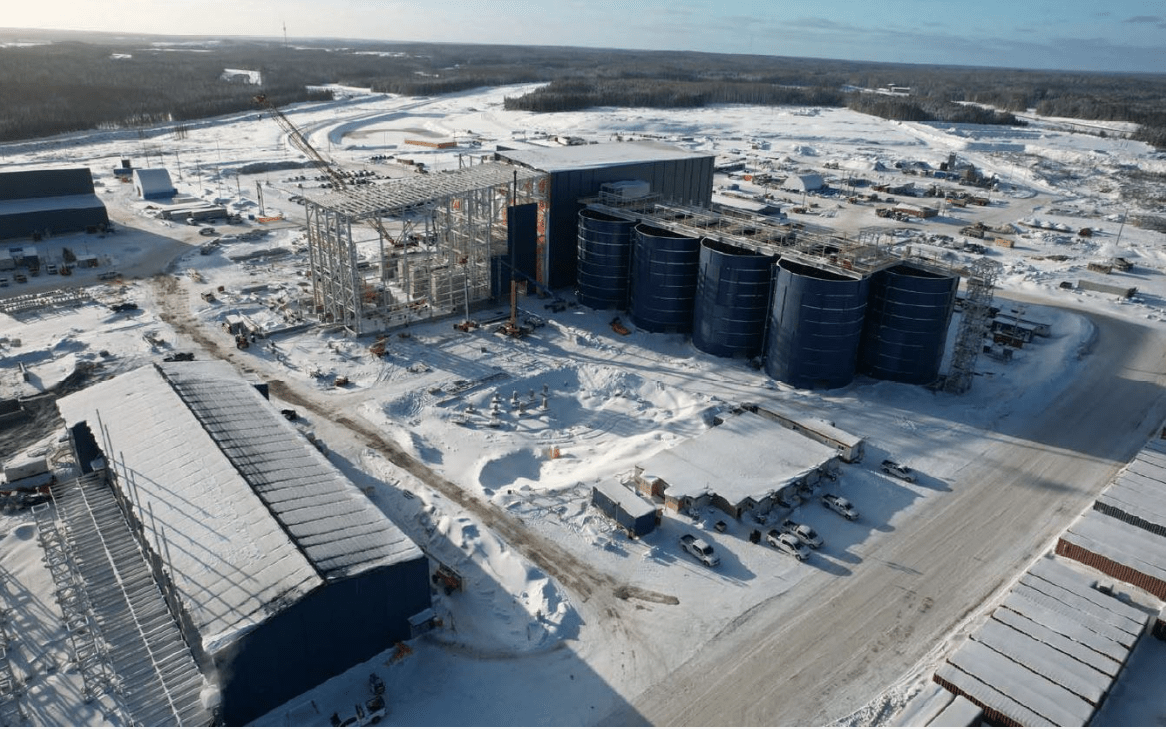

Greenstone Construction Progress (Company Website)

{kind=link}

However, the most significant development for Equinox has been the recovery in the gold price, with Equinox taking the defensive measure to put an At-The-Market equity program in place to sell up to $100 million in shares if its liquidity situation were to worsen . Fortunately, the ~$250/oz increase in the gold price over the past two months, and the company's proceeds from partial shares in Solaris, have alleviated concerns of a potential funding gap, combined with the fact that the Greenstone construction team continues to do an incredible job keeping this massive ~27,000 tonnes per day gold project on budget and schedule. So, while there's no guarantee that Equinox will be able to navigate the next 18 months without share dilution (Greenstone's first pour), I am cautiously optimistic.

Greenstone Progress

Digging into the most recent company update, Greenstone's construction is 56% complete, earthworks are 73% complete, the process plant is 41% complete, and the tailings facility is 47% complete. Given that tailings are one area where we saw a capex blowout from another Ontario-based gold producer (Magino), it's encouraging to see that this is nearly half complete, and also nice to see that procurement is nearing completion as well. This solid progress and ability to stay on budget and schedule suggest that there's a possibility the company might deliver successfully on budget, alleviating worries about the need to dilute shareholders to ensure it can fund Greenstone.

It's worth noting that Equinox noted in its Q3 Conference Call that its least favored options in terms of raising capital would be selling shares of its own stock at these prices or parting with an asset. That said, this certainly worked out very nicely for Iamgold ( IAG ) in terms of padding its funding gap, with the stock being the top performer over the past 12 months among its peer group and sentiment improving sector-wide, suggesting Equinox might be able to get a decent price for one of its less "core" assets like Fazenda and or RDM.

Greenstone Progress (Company Presentation)

{kind=link}

For those unfamiliar, Greenstone is a transformative asset for Equinox. It is expected to produce upwards of ~250,000 attributable ounces per annum for its first six years at all-in-sustaining costs below $700/oz. This will significantly increase production, lifting Equinox's annual production above 825,000 ounces, assuming it maintains its current portfolio. Meanwhile, this would provide a nice boost to its margin profile and also a major upgrade to its jurisdictional profile. The result is that we could see multiple expansion for Equinox once Greenstone is in commercial production, and this would be helped further by a non-core asset, with this helping to let go of a higher-cost asset and its relatively high concentration to Brazil.

Valuation & Technical Picture

Based on ~356 million shares and a share price of US$4.10, Equinox Gold trades at a market cap of ~$1.46 billion, which is a dirt-cheap valuation for a company with ambitions to become a 900,000-ounce producer. However, it is important to note that there are no guarantees that the company can achieve this without share dilution if the gold price declines below $1,750/oz, meaning that the share figure could end up (resulting in a higher market cap at the same share price of US$4.10). In addition, Equinox is a higher-cost producer and will remain a higher-cost producer even once Greenstone is online, with a few high-cost operations (Castle Mountain, Los Filos, RDM) that have seen unit costs worsen after two years of inflationary pressures.

Equinox Gold Operations (Company Website)

{kind=link}

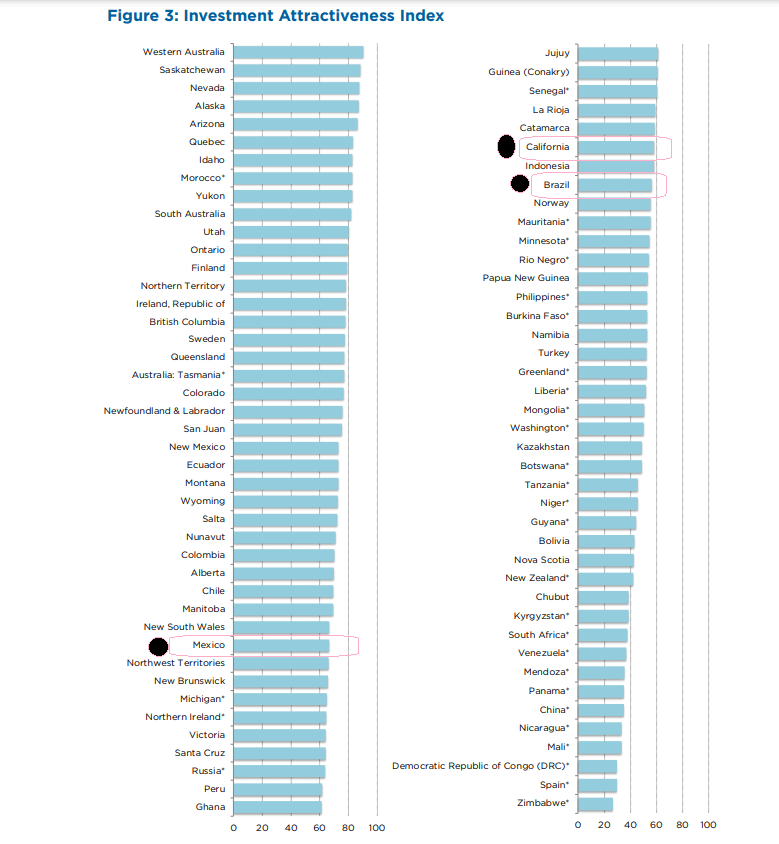

In addition, the company has a less attractive jurisdictional profile than many of its intermediate peers, with a significant portion of annual production tied to Brazil, Guerrero State, and California. Obviously, adding Greenstone will help from a margin and jurisdictional standpoint, but this won't change the fact that over 65% of future production will come from these three jurisdictions. Given these negative attributes, I believe a fair multiple for the stock is 0.90x P/NAV vs. other names like SSR Mining ( SSRM ) that can justify a multiple closer to 1.0x P/NAV with lower costs & a higher proportion of production from Tier-1 jurisdictions (Nevada, Saskatchewan). Using this multiple (0.90x P/NAV), I see a fair value for Equinox of ~$1.73 billion or US$4.85 per share.

Fraser Mining Institute - Investment Attractiveness Index Mining Jurisdictions (Fraser Mining Institute, Author's Drawings)

{kind=link}

Typically, I prefer a minimum 40% discount to fair value to justify buying small-cap producers, and in the case of a relatively weak balance sheet, one could argue that a 45% discount would be more applicable. However, even if we were to apply a 40% discount to fair value to figure out a low-risk buy zone for the stock, Equinox would still need to decline below US$2.95 to become interesting from a valuation standpoint. Obviously, this doesn't mean the stock has to decline to these levels, and a rising gold price will lift all boats. However, I prefer only to stick my neck out if a substantial margin of safety is baked in, and I don't see that being even remotely the case here at US$4.10 per share.

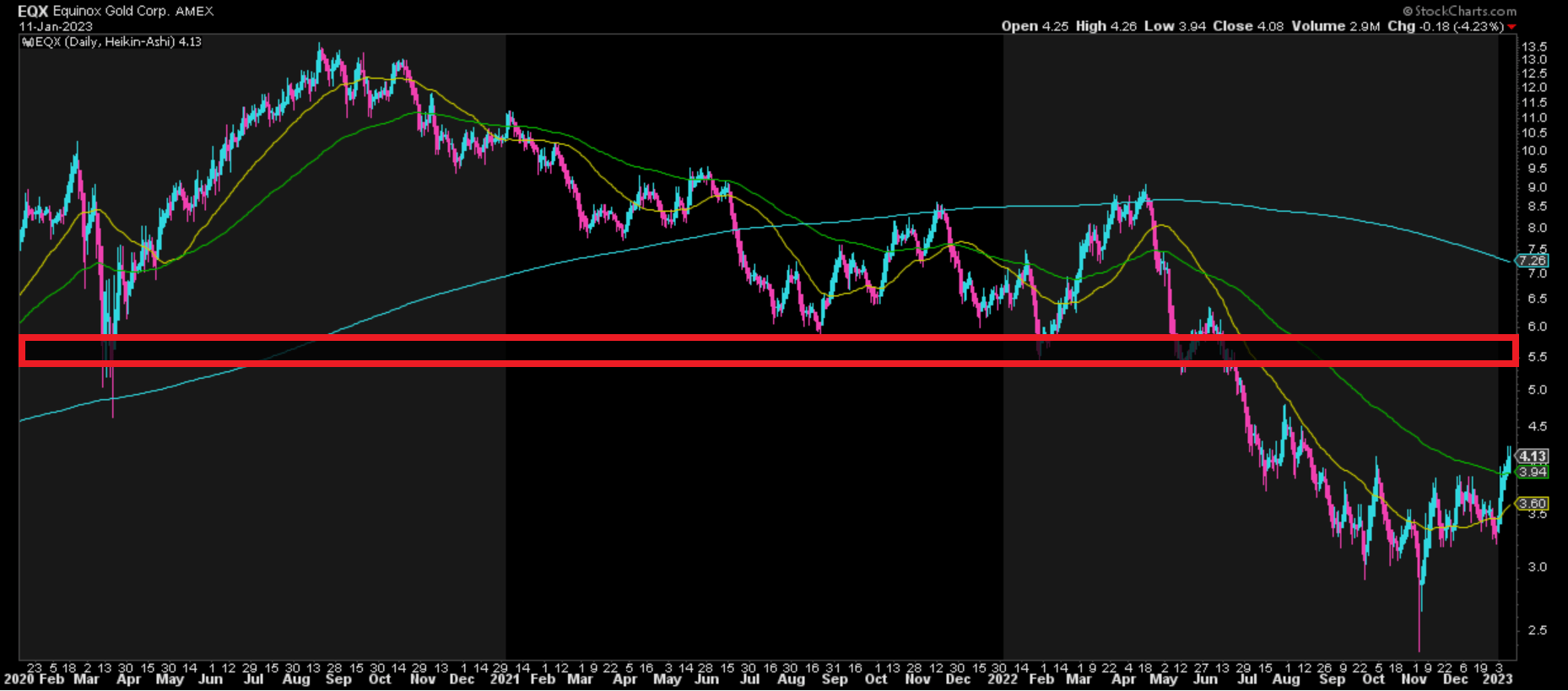

Finally, if we look at the technical picture, we can see that EQX has risen more than 75% off its recent lows, and it rarely pays to chase a sector laggard after a move of this magnitude. Besides, this sharp rally has now left the stock at the mid-point of its expected support/resistance range, with strong resistance at US$5.75 - US$5.90 and no strong support until US$2.35 - US$2.50. Using the high end of support and the low end of resistance, this translates to a reward/risk ratio of 1.03 to 1.0, which is well below the 5.0 to 1.0 reward/risk ratio I require for starting new positions. To summarize, I do not see this as a low-risk buy point, and I don't see any way to justify paying up for the stock above US$4.15.

EQX Daily Chart (StockCharts.com)

{kind=link}

Summary

There is enormous value in being a contrarian in the market, especially in a sector as volatile as the gold space. However, the key is to ensure a significant margin of safety and to buy amid a bloodbath, not rush in after an 80% rally following a recent panic low.

In the case of Equinox Gold Corp., there is no disputing that this is a contrarian bet after an ~80% decline from its highs. However, I'm less interested in chasing EQX here, with it sitting well above support and with two unfilled gaps below. That said, barring a collapse in the gold price, I think the low at $2.35 will mark a multi-year low for Equinox Gold Corp. stock. Therefore, I see Equinox Gold Corp. stock as a Speculative Buy below $2.95, and I would consider starting a new position in the stock if we can see a retracement over the coming months.

For further details see:

Equinox Gold: Getting Saved By The Gold Price