ETRN - Equitrans Midstream: A Possible Finish In Sight For Their MVP Project

Summary

- Equitrans Midstream faced continued setbacks during 2022 trying to finish their MVP project.

- Thankfully, there is a possible finish in sight during 2023 with management expecting permits could be forthcoming reasonably soon.

- It remains to be seen whether this eventuates, although at least it seems their dividends will keep flowing.

- As such, there are no visible warning signs of an impending dividend cut.

- Given their resulting high near-10% dividend yield, I believe that maintaining my strong buy rating is appropriate.

Introduction

When last discussing Equitrans Midstream ( ETRN ) and the continued setbacks faced by their Mountain Valley Pipeline project, hereon referred to as their MVP project, my previous article discussed how investors were able to count on the dividends to keep flowing, despite the failure of a bill in the United States Senate. Thankfully, there finally appears to be a possible finish in sight for their MVP project that could come online during 2023 but even without being finished, investors can still grab a high near-10% dividend yield that remains safe.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

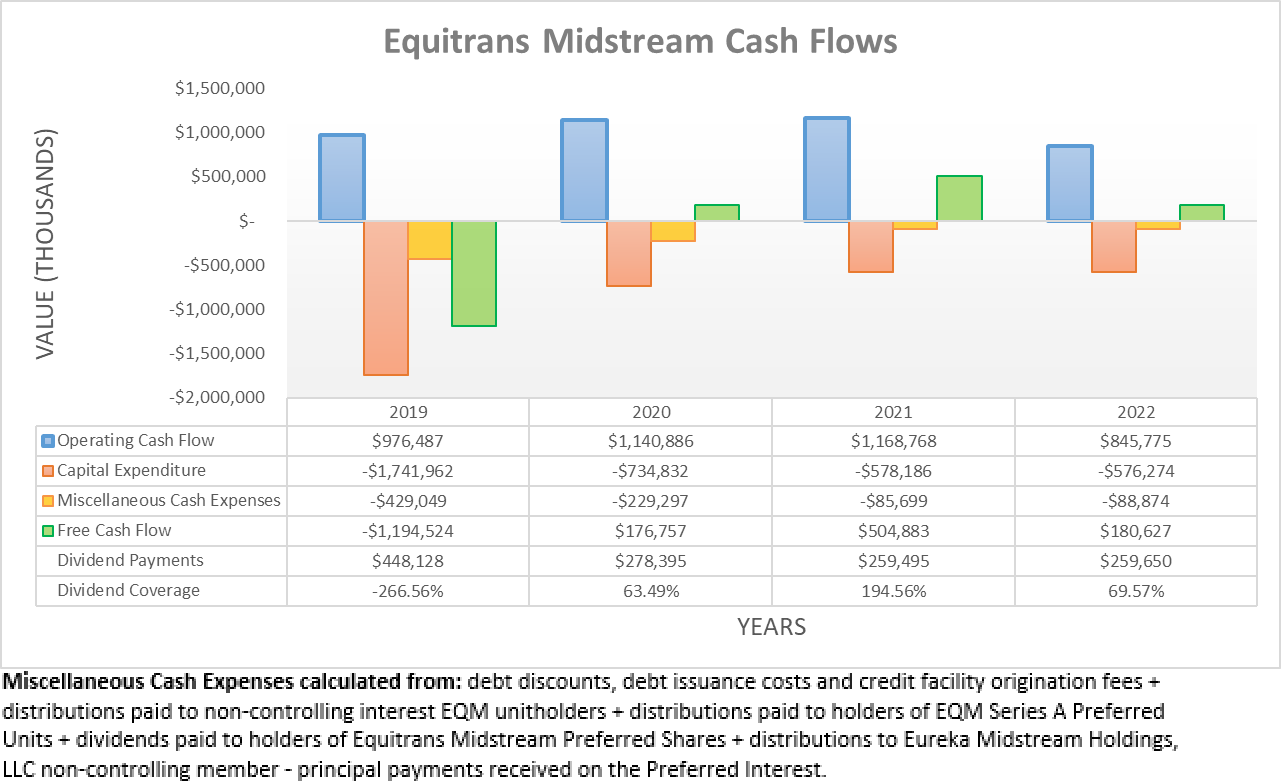

Following a weak start to 2022 during the first half, this disappointingly continued into the second half with their operating cash flow ending the year at $845.8m and thus down a significant near-28% year-on-year versus their previous result of $1.169b during 2021. As a result, they only generated $180.6m of free cash flow during 2022, which fell short of funding their accompanying dividend payments of $259.7m, thereby resulting in very weak coverage of 69.57%.

Whilst not necessarily ideal, thankfully there were moving parts that skewed this comparison in favor of 2021. The first of which is the $195.8m impact during the fourth quarter of 2022 pertaining to the EQT cash option . This saw their large customer, EQT ( EQT ) elect to forego part of a gathering fee relief payment to Equitrans Midstream that would have otherwise been applicable, as a result of their delayed MVP project. If this one-off impact was added back into their results, it would have seen their full-year operating cash flow at $1.042b and thus down a less significant circa 11% year-on-year.

{kind=link}

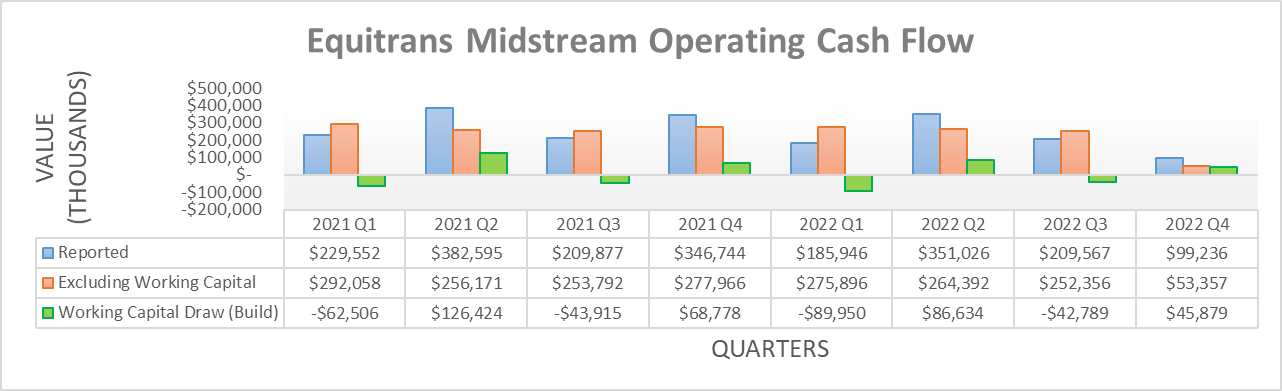

When viewing their operating cash flow on a quarterly basis, it uncovers another moving part that skewed the comparison in favor of 2021. Namely, their working capital movements that vary each quarter, sometimes boosting their reported results with draws, whilst other times they are a hindrance with builds. If aggregating their various draws and builds during 2022, it nets out to an immaterial build of $0.2m. Although in the case of 2021, it sees a material draw of $88.8m that materially boosted their reported results. If excluded, their underlying operating cash flow during 2021 was actually $1.08b and thus similar to their equivalent result of $1.042b during 2022, excluding their one-off EQT cash option impact. Despite being disappointing on the surface, this means that 2022 was not actually too bad of a year beneath the surface, which bodes well heading into 2023 that could see their MVP project finally come online, as per the commentary from management included below.

"…we expect to receive all of the required permits and approvals over the next few months. This timing will allow for mobilization of construction crews in the summer of 2023, which will position us to bring MVP into service in 2023. However, as we all know, we expect project opponents to yet again challenge these [duly] issued permits. As such, we believe the agencies are focused on issuing permits that will exceed all legal standards as well as address points previously raised by the Fourth Circuit."

- Equitrans Midstream Q4 2022 Conference Call.

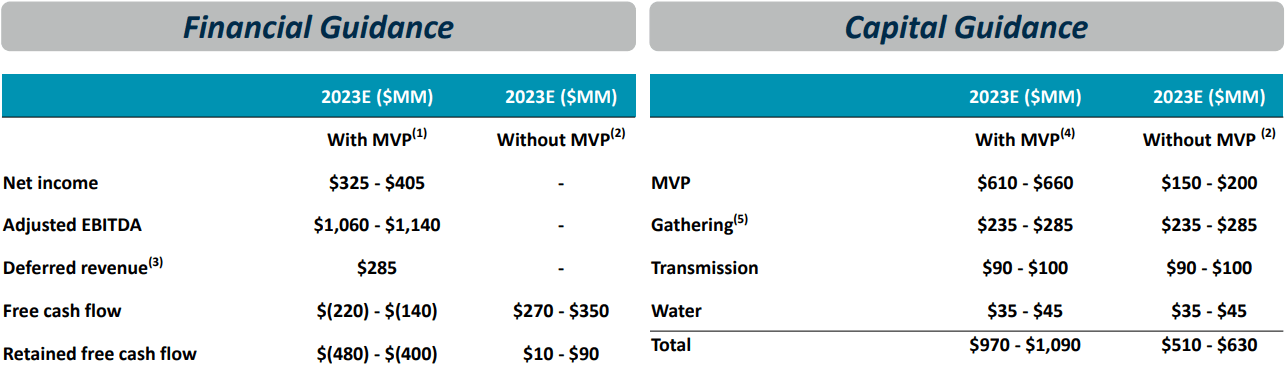

After suffering continued setbacks during recent years, as discussed within my previous analysis, it seems an end might finally be in sight with management seeing the possibility for their MVP project to finally come online during 2023. That said, nothing is finalized and thus they have issued two separate sets of guidance for the year ahead, one with their MVP project being finished and one without.

Equitrans Midstream Fourth Quarter Of 2022 Results Announcement

{kind=link}

Assuming their MVP project comes online, their guidance for 2023 forecasts adjusted EBITDA of $1.1b at the midpoint, which would represent a slight increase year-on-year versus their result of $1.071b during 2022, as per their fourth quarter of 2022 results announcement . Whilst this may seem underwhelming given it includes their new flagship project, it should be remembered that any earnings contributions are weighted towards the end of the year with most of the benefit not evident until 2024. More so, it was disappointing they did not provide any adjusted EBITDA forecast assuming their MVP project does not come online because if anything, I would have thought this to be the easier of the two forecasts for management to provide.

Regardless, their guidance for 2023 still includes forecasts for free cash flow for both paths, along with retained free cash flow, which pertains to how much is left after their dividend payments. Whilst they did not cover their dividend payments during 2022, this may not be repeated again during 2023. If they receive the permits to finish their MVP project, the resulting higher capital expenditure will outpace their operating cash flow, thereby seeing them forecast negative free cash flow of between $140m and $220m and thus by extension, negative retained free cash flow of between $400m and $480m. On the other hand, if their MVP project remains on the back burner, they are forecasting free cash flow of between $270m and $350m of which between $10m and $90m should be retained.

Ultimately only time will tell, although it is positive for the safety of their dividends to see adequate coverage during 2023, absent of the additional capital expenditure to finish their MVP project. That said, until we know which of these two paths will eventuate, it leaves their dividend coverage looking uncertain. Importantly, there was no discussion surrounding their dividends during their previously linked fourth quarter of 2022 conference call, which in my opinion is another good sign because this implies they are effectively on autopilot and thus, not likely to be cut.

{kind=link}

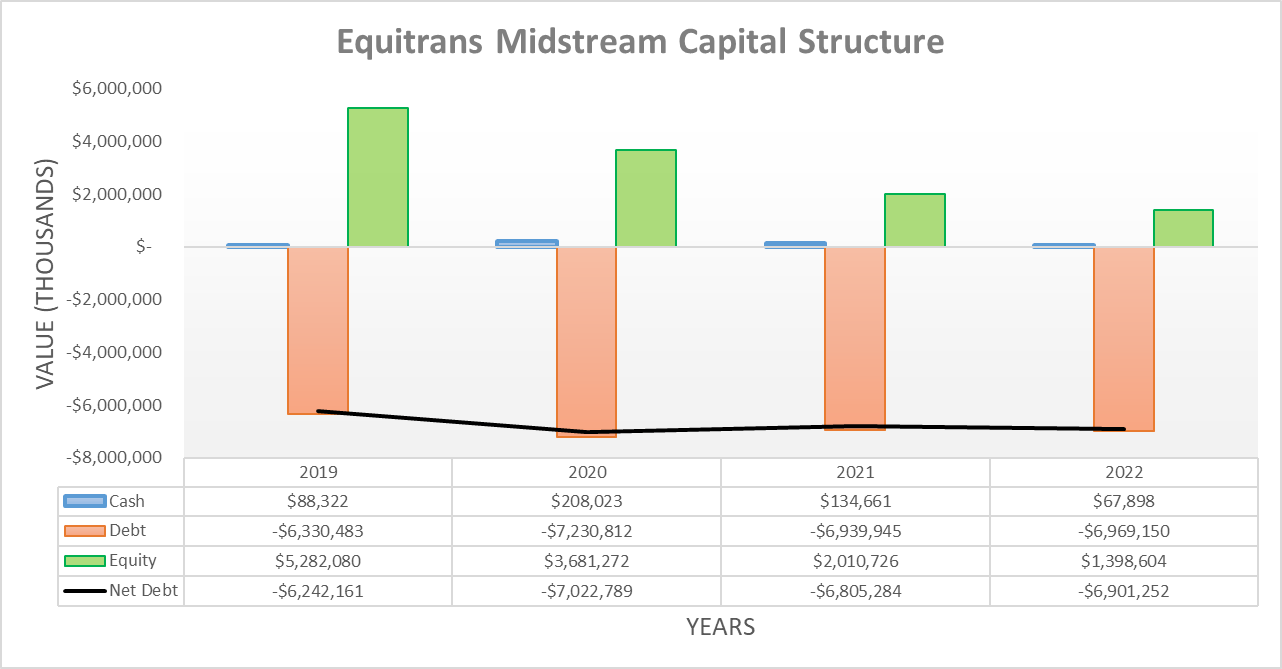

Since conducting the previous analysis, the second half of 2022 saw their net debt increase slightly higher to $6.901b at the end of the year versus its previous level of $6.734b following the second quarter. This $167m increase solely stems from the aforementioned $195.8m impact of the EQT cash option during the fourth quarter and thus, it is not necessarily a sign of a structural problem.

Going forwards into 2023, the direction their net debt takes will obviously depend upon whether their MVP project is finished or endures further delays. In light of their aforementioned guidance, the former path should see their net debt expand somewhere around $400m to $480m given their forecast for negative retained free cash flow. Meanwhile, the latter path should see their net debt decrease slightly by circa $10m to $90m, given their concurrent forecast for positive retained free cash flow.

Whilst only time will tell how 2023 unfolds, at least their financial position should be broadly stable even without their MVP project coming online. Even though finishing their MVP project would see their net debt increase, the accompanying boost to their earnings starting during 2024 should counteract this increase. When this outlook is combined with their net debt only increasing slightly since conducting the previous analysis, it would be redundant to reassess their leverage, debt serviceability or liquidity in detail, especially as their outlook for 2023 was the primary focus of this follow-up analysis.

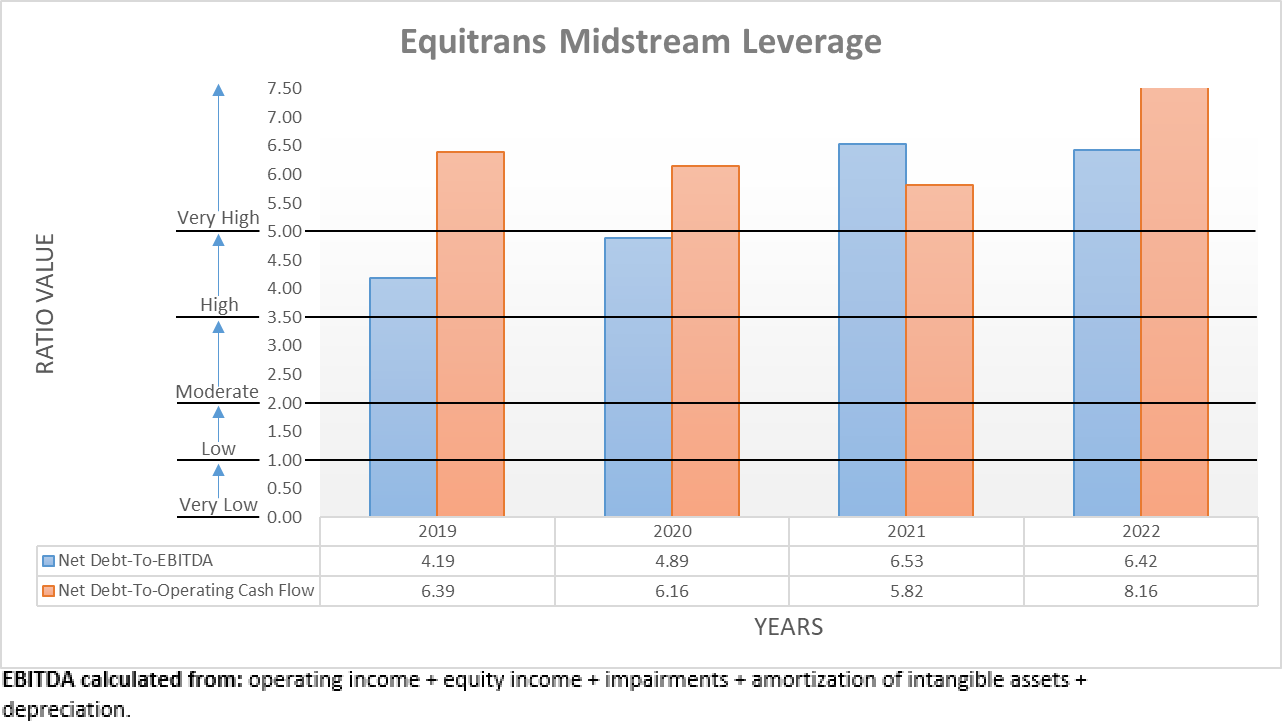

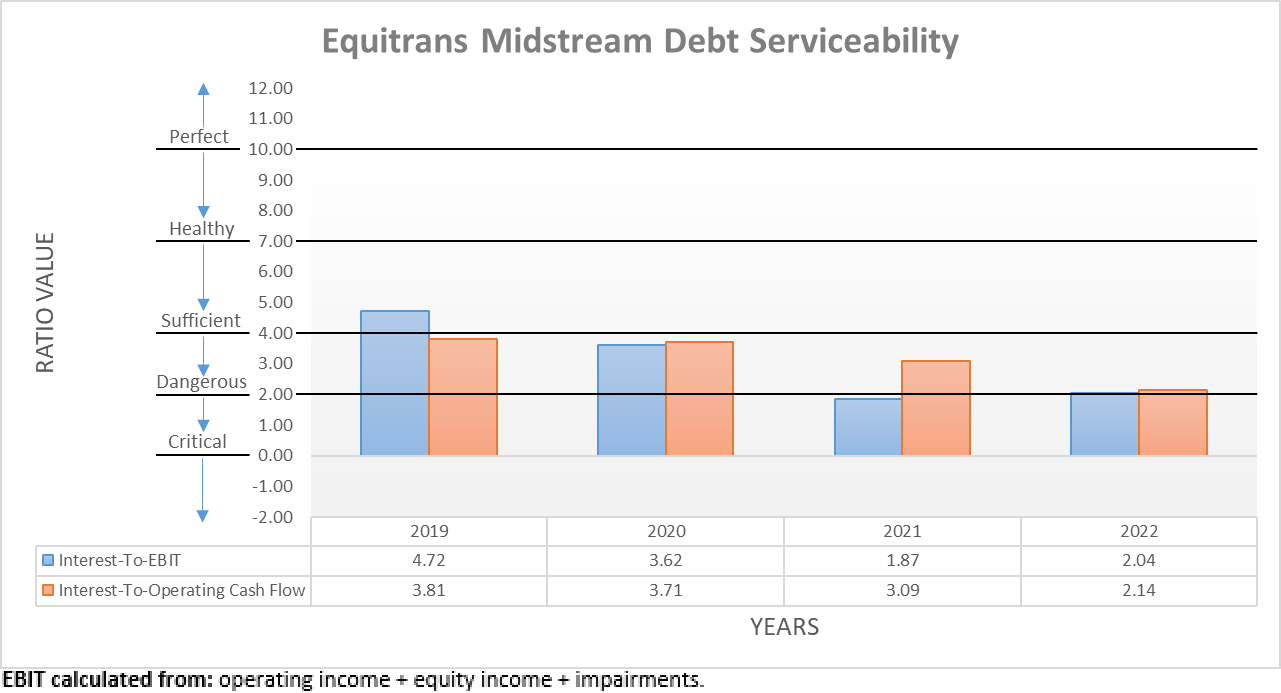

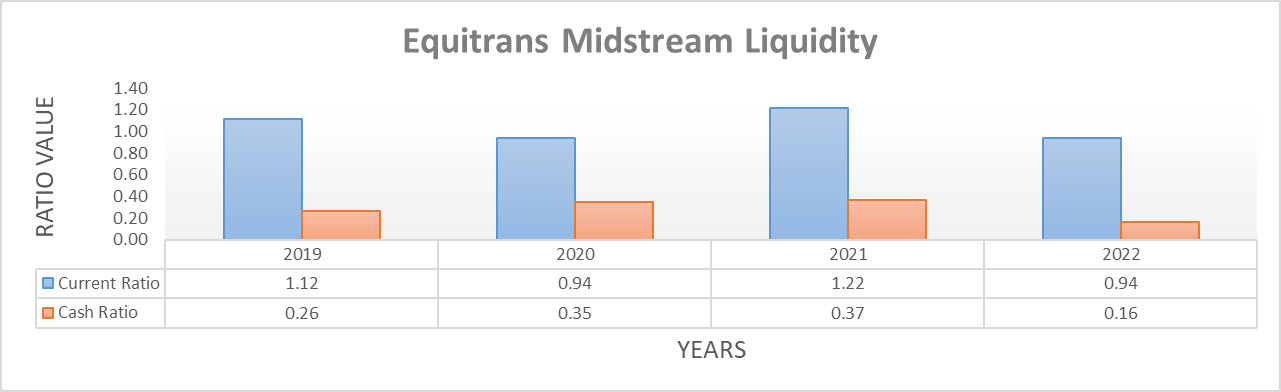

The three relevant graphs are still included below to provide context for any new readers, which shows their leverage remains very high with their net debt-to-EBITDA of 6.42 and net debt-to-operating cash flow of 8.16 both above the applicable threshold of 5.01. Whilst this is not necessarily ideal, at least their debt serviceability remains sufficient with interest coverage of 2.04 and 2.14 when compared against their EBIT and operating cash flow, respectively. Meanwhile, their liquidity remains strong with a current ratio of 0.94 and more importantly, an accompanying cash ratio of 0.16.

{kind=link}

{kind=link}

{kind=link}

Conclusion

If 2023 finally sees their MVP project finished, it should change the narrative away from its continued setbacks, which should facilitate a higher share price via reducing uncertainties, not to mention via boosting their financial performance. Even if delayed once again, the signs point to their dividends being sustained and given their high yield that is now almost near-10% following this recent sell-off, I still believe this yield alone makes maintaining my strong buy rating appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from Equitrans Midstream's SEC filings , all calculated figures were performed by the author.

For further details see:

Equitrans Midstream: A Possible Finish In Sight For Their MVP Project