ETRN - Equitrans Midstream: Mountain Valley Pipeline Already Priced Into The Stock

2023-08-22 21:48:19 ET

Summary

- The completion of the long-delayed MVP presents a significant opportunity for ETRN, but there are potential risks and cost overruns associated with the project.

- Equitrans' stock already reflects the anticipated benefits of the Mountain Valley Pipeline coming online.

- Given the run in ETRN stock, I'd remain on the sidelines.

While the Mountain Valley Pipeline coming online should be a huge boost to Equitrans Midstream ( ETRN ) moving forward, the benefits already look priced into the stock.

Company Profile

ETRN is an Appalachia-focused midstream company that operates in three segments: gathering, transmission and water. Former parent EQT ( EQT ) is its largest customer, representing over 60% of its revenue in 2022.

In its gathering segment, the firm provides firm and interruptible services. It has three primary gathering systems. Its largest is a ~690 mile high pressure system in Pennsylvania and West Virginia that serves EQT. Its ~280 mile Eureka & Hornet system supports dry gas development in Ohio and wet gas development in West Virginia. Its Ohio Utica system, meanwhile, is ~210 miles and supports dray gas gathering for Gulfport. It gathering segment represented over 2/3 of its operating revenue in 2022.

ETRN’s transmission segment includes ~940 miles of FERC regulated interstate pipelines, as well as 18 storage pools with 43 BCF of gas storage capacity. About 97% of its firm capacity commitments come are under negotiated rate agreements. The segment represented about 30% of its operating revenue in 2022.

The midstream operator’s water segment, meanwhile, includes 350,000 barrels of above ground storage and over 200 miles of freshwater delivery pipelines. The segment accounted for 4% of its operating revenue in 2022.

Opportunities and Risks

ETRN’s biggest opportunity by far will be the completion of the long-delayed Mountain Valley Pipeline ((MVP)). MVP is a 303-mile, 42-inch diameter natural gas interstate pipeline with 2.0 Bcf per day of capacity that was designed to connect the company’s existing transmission and storage assets to demand markets in the Southeast U.S. The project is being developed as part of a joint venture with a number of utility and power companies, including NextEra Energy ( NEE ), Consolidated Edison ( ED ), AltaGas ([[ATGFF]], [[ALA:CA]]), and RGC Resources ( RGCO ). ETRN has a 45.5% stake in the pipeline.

The project began construction in 2018 but has been hampered throughout the years by lawsuits and regulatory matters. The pipeline received some positive news when the Biden administration approved a permit for the natural gas pipeline to run through a National Forest. This was a big win for the project and would allow the last 20 miles of the pipeline to be completed. Afterwards, though, a judge once again halt the pipeline even after a law changed the jurisdiction of the pipeline, but the Supreme Court lifted the stay and said that construction could resume.

Most recently, the U.S. Pipeline and Hazardous Materials Safety Administration said that MVP needed to undergo a series of safety inspections , as the pipes have been buried without corrosion protection or exposed to the elements for a long time. The inspections could not only lead to further delays, but could result in expensive fixes.

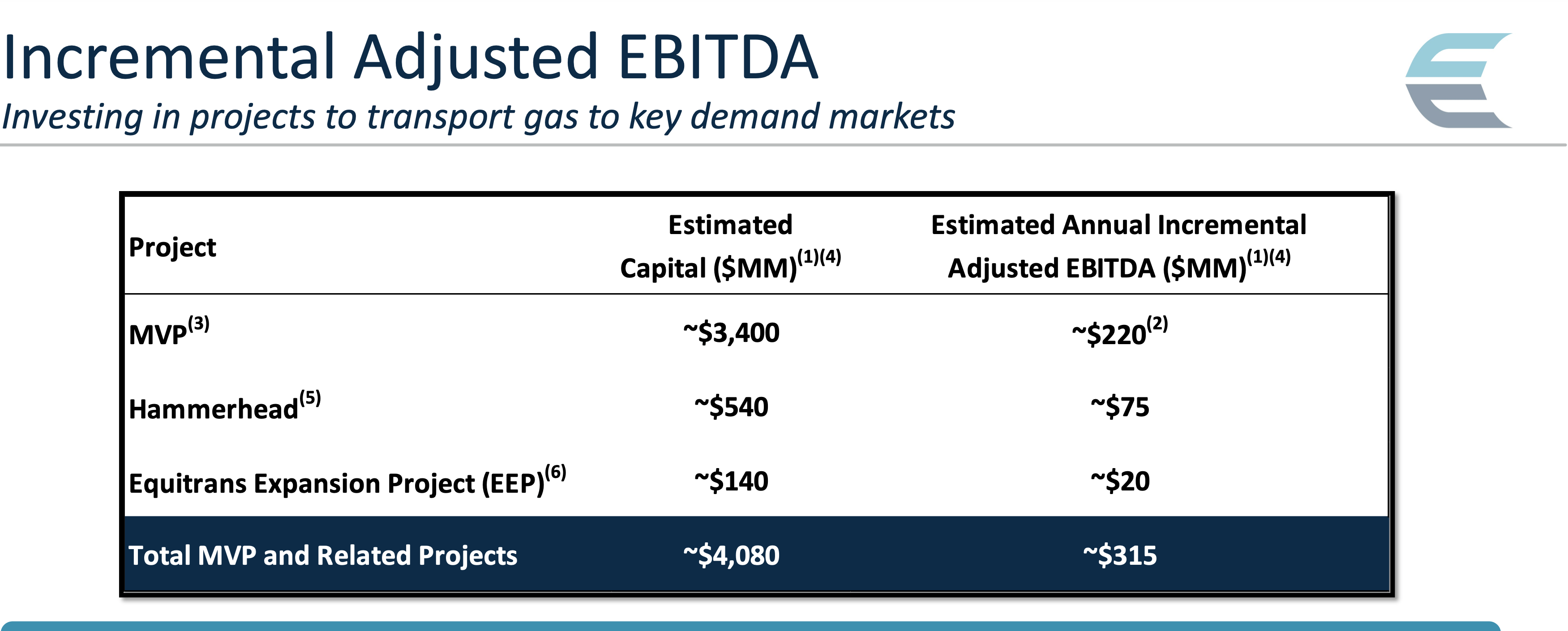

That said, there is finally a light at the end of the tunnel of this $6.6 billion project coming finally online. The company is targeting a completion date by the end of 2023, although there is still some potential for delay with the safety inspections. The project is now massively overbudget given the delays and its overall economic return won’t be great as a result. However, the pipeline should add about $315 million in EBITDA to the company, which includes $220 million from MVP itself and then another $75 million from its already built Hammerhead gathering pipeline, where it will get 1.2 Bcf/d of firm commitment from EQT once MVP is in service. It also expects to get $20 million from its Equitrans expansion project.

{kind=link}

ETRN is expected to generate just a tad over $1 billion in EBITDA this year, so the additional EBITDA as a result of MVP coming online will be a big boost. Now there is still a question of timing, which remains a risk, and EQT was pegging more of mid-2024 timeframe for the pipeline coming online, versus the end of 2023 target from ETRN. There also remains the question of any additional costs that arise from the aforementioned safety inspections and potential fixes that will be needed.

Discussing MVP on its Q2 earnings call , CEO Thomas Karam said:

“It has been a remarkable couple months for MVP. We saw congressional leadership from both sides of the aisle, together with the administration, work in a bipartisan way to enact the Fiscal Responsibility Act of 2023 on June 3. This legislation includes Section 324, which ratifies and approves all permits and authorizations necessary for the construction and initial operation of MVP. Importantly, the legislation also divests any court of jurisdiction to review agency actions on approvals necessary for MVP construction and initial operation and grants exclusive jurisdiction for claims against the legislation to the U.S. Court of Appeals for the District of Columbia. On June 28, after MVP received all required permits, FERC authorized all construction activities to resume. After only days of active construction, the U.S. Court of Appeals for the Fourth Circuit issued stay orders on 2 of the project's federal authorizations, again halting forward construction. On July 14, we filed an emergency application with the United States Supreme Court seeking to vacate the stays and requesting a summary ruling on the extent of the Fourth Circuit's jurisdiction. On July 27, the Supreme Court vacated the stays, and our previously filed motions to dismiss the underlying cases are pending with the Fourth Circuit. We have now resumed forward construction and are still targeting completion by year-end at a total project cost of approximately $6.6 billion. Despite all the twists and turns, we are grateful for the timely ruling by the Supreme Court and to be, once again, focused on construction.”

MVP coming online should also set up ETRN for its next round of growth projects that connect to MVP. The company originally had plans for a number of demand-pull related projects off of MVP, including its Southgate project, as well as power plant connections and other potential shoot-offs. Appalachian E&Ps have been starting to deal with pipeline constraints to get gas out of the Marcellus and Utica basins, so MVP will be a big boost to that. There should be other potential expansion and tie-in projects down the road.

Outside of MVP, ETRN has other growth projects, including its Ohio Valley Connector Expansion project, a $160 million project to add 350 million cubic feet per day of deliverability on its Ohio Valley Connector pipeline, which provides access to the Mid-Continent and Gulf Coast markets. It also continues to build out its water infrastructure.

When looking at risks outside of more MVP delays or cost overruns, the price of natural gas is one potential risk. However, since it operates in a low cost basin that is pipelined constrained with long-term contracts, nat gas prices shouldn’t have too much impact on the company’s operations. The company also carries a lot of debt, stemming in large part from the delays and overbuild costs associated with MVP.

Valuation

ETRN stock currently trades at about 10.7x the 2023 EBITDA consensus of $1.04 billion, and 8.3x the '24 consensus of $1.34 billion.

The stock yields 6.1% based off its current distribution. The company reduced its quarterly dividend from 45 cents to 15 cents back in 2020. It has an FCF yield of about 14%.

ETRN is one of the more expensive midstream operators based on 2023 numbers, but its valuation moves to the lower side once MVP comes online.

{kind=link}

Conclusion

MVP coming online should be a huge boost to ETRN moving forward. However, the stock has generated strong gains this year, reflecting the impact of the pipeline coming in service next year. At the same time, the company is overleveraged, when most midstream companies have worked on improving their balance sheets for several years. There is also the possibility of more cost over-runs related to the mandated safety inspections for MVP.

Given this, while ETRN has been a strong performer this year, I think it is best to stay more neutral on the name as present.

For further details see:

Equitrans Midstream: Mountain Valley Pipeline Already Priced Into The Stock