ETRN - Equitrans Midstream: This 7.31%-Yielder Is Worth Considering Today

2023-05-31 12:20:59 ET

Summary

- Equitrans Midstream Corporation is a natural gas-focused midstream company operating in the Marcellus and Utica Shale plays.

- Equitrans Midstream enjoys remarkably stable cash flows due to its contract-based business model.

- The company is well-positioned for growth and should be helped by a provision in the debt ceiling deal.

- The company's debt load remains somewhat higher than we really like to see.

- ETRN boasts a 7.31% yield at the current price, and it appears to be able to sustain it.

Equitrans Midstream Corporation ( ETRN ) is a midstream corporation that primarily transports natural gas throughout the Appalachian region, which is at least partly due to its link with EQT Corporation ( EQT ). In fact, Equitrans Midstream Corporation was formed via a merger between the former EQT Midstream Partners and Rice Midstream Partners, which were two master limited partnerships that were formed to build out the infrastructure needed to develop the Marcellus and Utica Shale plays to their full potential.

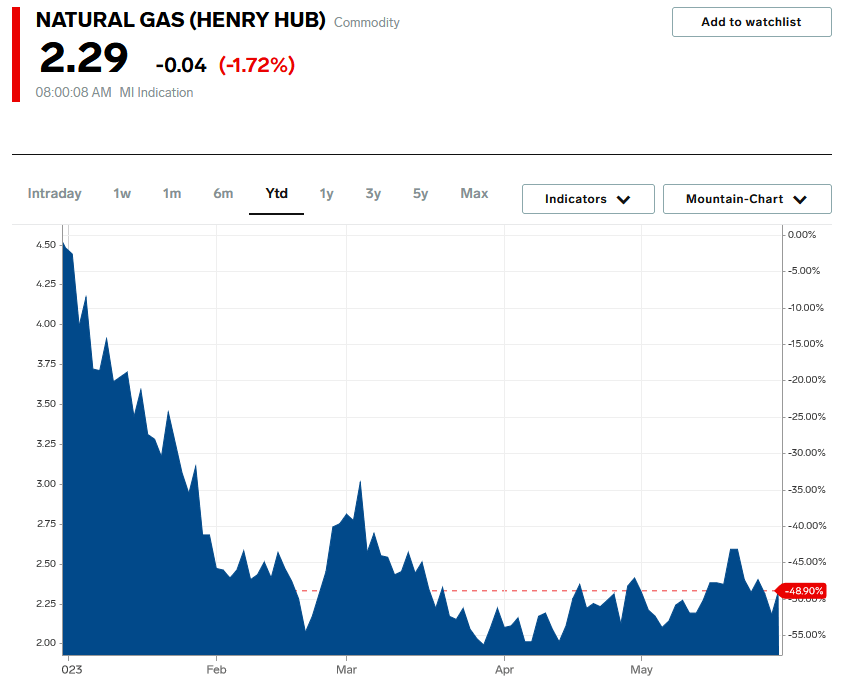

As I have explained in many previous articles, natural gas midstream operations are generally a very good place to be right now because the demand for natural gas is likely to grow over the coming years. This is partly due to its use as a supplementary fuel for renewable sources of energy that are incapable of providing the "always-on" reliability that we expect from a modern electric grid. However, natural gas has certainly not performed very well this year, as a warm winter and the Freeport LNG export terminal outage have caused a tremendous oversupply of the substance to build in the market. I discussed this in a blog post earlier this month. This oversupply has naturally caused the price of natural gas to plummet, with the price of the compound at Henry Hub down 48.90% year-to-date:

{kind=link}

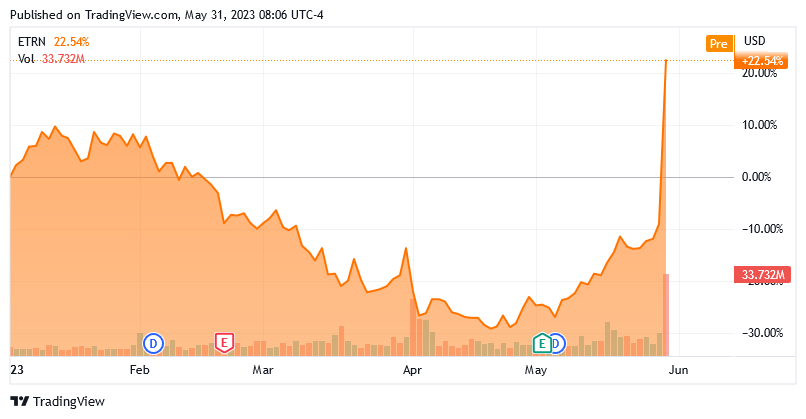

However, this has not had a significant impact on Equitrans Midstream's financial performance due to the business model that the company employs. This did not stop the stock from losing ground in the market, though, but it has since more than regained its losses as it shot up about 40% yesterday:

{kind=link}

This does not mean that the opportunity has been lost, though, as the stock still yields a very impressive 7.31% at the current price. The company also has some strong growth potential going forward, as rising demand for natural gas will likely spur development in the Marcellus Shale and boost demand for the company's services. Let us investigate this opportunity.

About Equitrans Midstream

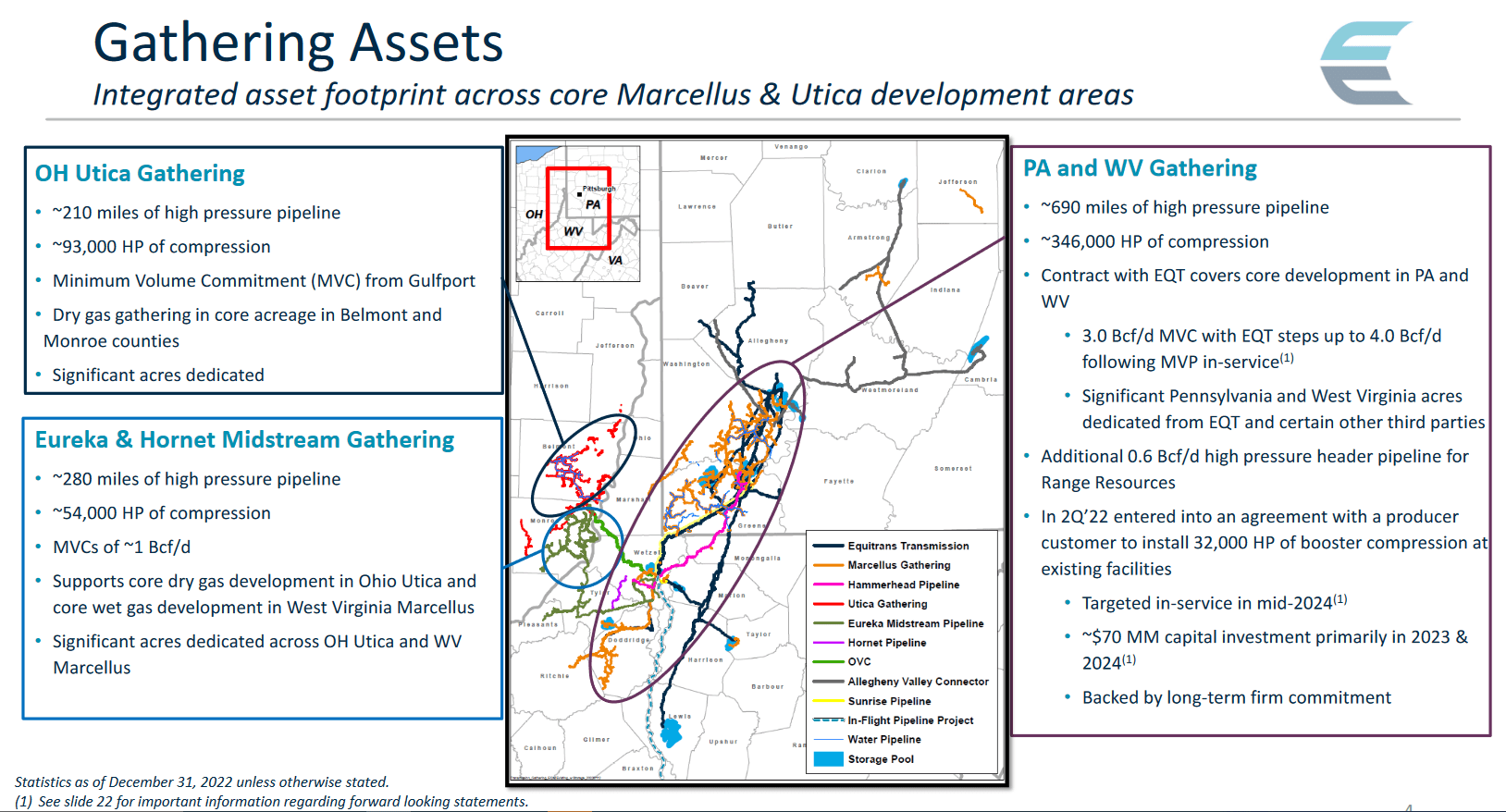

As stated in the introduction, Equitrans Midstream Corporation is a natural gas-focused midstream company that operates primarily in the natural gas-rich Marcellus and Utica Basins:

{kind=link}

As we can see, the company has a substantial gathering pipeline infrastructure that stretches across much of Southwest Pennsylvania, Southeast Ohio, and the northern half of West Virginia. This is one of the richest natural gas regions in the world, which positions the company quite well to exploit any forward growth in natural gas demand.

It is important to note though that these are not the traditional long-haul pipelines that we typically associate with a midstream company. A gathering pipeline is a relatively short pipeline that grabs produced resources at the wellhead where they are removed from the ground and transports them to the first stop on their journey to the end-user. This initial destination is usually a much larger long-haul pipeline or a processing plant. In the first quarter of the year, the company's gathering pipeline infrastructure had an operating cash income of $104.294 million against the company-wide total of $215.244 million. Thus, this business accounts for approximately 48.45% of the company's total income.

Obviously, the gathering pipeline business is not Equitrans Midstream's only source of revenue or income since it only accounts for slightly less than half of the company's business. The company does, in fact, own some of the larger long-haul pipelines that we usually associate with midstream companies. These mostly just cover the Appalachian Region, though, much like the company's gathering pipeline infrastructure:

Equitrans Midstream

In total, Equitrans Midstream's long-haul pipelines extend a total of 940 miles and are capable of carrying approximately 4.4 billion cubic feet of natural gas per day. As such, the company's infrastructure is clearly much smaller than MPLX LP ( MPLX ), which also has substantial midstream infrastructure in the region. However, Equitrans Midstream's long-haul infrastructure is mostly intended to serve as trunklines through the region that collect the natural gas from all of the gathering pipelines into one place for easy transport to a processing facility. It is not really intended to transport resources all across the nation like the pipelines operated by its larger peers. The fact that Equitrans Midstream's infrastructure is smaller than some of its peers does not prevent it from making money, however. Indeed, its long-haul pipelines earned an operating income of $98.922 million during the first quarter of 2023 so they are of comparable profitability to the company's gathering operations.

Despite the differences between them, Equitrans Midstream's gathering pipeline business and its long-haul transmission pipeline business have a similar business model. Basically, the company enters into long-term contracts with its customers. Under these contracts, the company provides transportation for the customer's natural gas and the customer compensates Equitrans Midstream based on the volume of natural gas that is transported, not on its value. This provides a company with a great deal of insulation against fluctuations in resource prices, which is important today given the weakness in natural gas prices that we discussed earlier in this article. In addition to this, the contracts that the company has with its customers include minimum volume commitments that specify a certain quantity of resources that must be sent through the company's infrastructure or paid for anyway. This provides some protection against revenue and cash flow declines that might accompany production cuts. As it is typical for upstream producers to cut production when resource prices decline, this provides Equitrans Midstream with further protection against the inherent volatility of commodity prices.

We can see the overall stability that the contract-based business model provides to the company by looking at its operating cash flow over time. Here are the company's figures from each of the past eleven twelve-month periods:

{kind=link}

This general stability is something that we should be able to appreciate as income investors. This is because it provides a great deal of support for the dividend that the company pays out. After all, it is much easier for management to feel confident paying out a significant portion of the company's cash flow to the shareholders if it knows with some certainty that it will have a similar amount of money available next quarter or next year. The overall stability through any economic environment also reduces the risk that a company will reduce its dividend during challenging economic conditions, although admittedly midstream companies have still cut their payouts in the past due to market hostility despite their cash flows remaining relatively stable.

Growth Projects

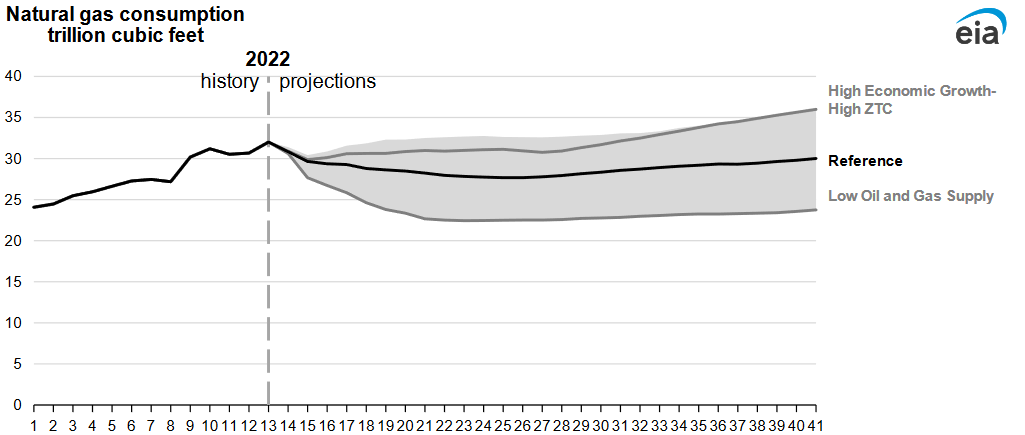

Naturally, as investors, we are interested in more than just mere stability. We like to see a company that we are invested in grow and prosper with the passage of time. Fortunately, Equitrans Midstream is well-positioned to accomplish that due to the fact that the demand for natural gas is expected to increase over the coming years. This comes from the fact that natural gas is critical to the energy transition as solar and wind power are unreliable and cannot sustain the "always-on" capability that most people expect from a modern energy grid. In the 2022 World Energy Outlook , the International Energy Agency projects that the global demand for natural gas will grow to 4.357 billion cubic meters equivalent by 2050, up from 4.213 billion cubic meters equivalent today. The U.S. Energy Information Administration likewise projects that domestic natural gas consumption will increase under most scenarios:

{kind=link}

Clearly, natural gas demand is not going anywhere except in the most pessimistic scenarios as both sources agree on that. The United States is expected to become a more significant supplier of this demand going forward than it has been in the past due to the enormous undeveloped reserves domestically compared to aging and declining reserves in areas such as the North Sea and parts of the Middle East. Thus, we can expect to see domestic production increase in order to feed the growing world demand.

One of the unfortunate problems with natural gas midstream infrastructure is that there is only a limited quantity of resources that a given pipeline can handle. In order to generate growth, the company will need to increase the volume of resources that it carries due to its volume-based business model. Thus, it will need to construct new infrastructure in order to expand its capacity to handle more resources. This is exactly what the company intends to do over the next few years.

One of the company's most significant growth projects is the Mountain Valley Pipeline, which is a 300-mile natural gas pipeline that runs from northwestern West Virginia to southern Virginia:

Equitrans Midstream

The pipeline is intended to meet the growing demand for natural gas in Virginia and North Carolina, as both states are in the process of switching from coal to natural gas for power generation. There has long been opposition to this pipeline from various environmental groups, which has been a drag on the company's stock price as there were some doubts that this ambitious and expensive project will ever be completed.

These doubts have been somewhat alleviated though as the recent debt ceiling deal contains a provision to get approval for the completion of this pipeline from the U.S. Army Corps of Engineers. While there are certainly politicians that oppose the construction of this pipeline on ideological grounds, the inclusion of this provision was a necessary compromise as the debt ceiling deal itself does not cut spending as much as some Congressmen want. The fact that this particular pipeline will be fast-tracked is the major reason why Equitrans Midstream's stock jumped yesterday as this is a substantial project for the company that should prove to stimulate its growth in the near term.

Financial Considerations

It is always important to investigate the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. That is usually accomplished by issuing new debt and using the proceeds to repay the existing debt. That process can cause a company's interest expenses to increase following the rollover in certain market conditions. As interest rates are currently at the highest levels that we have seen since 2007, this is an especially major concern today. In addition to interest-rate risk, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes a company's cash flow to decline could push it into financial distress if it has too much debt. While midstream companies like Equitrans Midstream typically have remarkably stable cash flows over time, we should still not ignore this risk.

One ratio that we can use to judge a company's ability to carry its debt is the leverage ratio, which is also known as the net debt-to-adjusted EBITDA ratio. This ratio tells us how many years it would take a company to completely pay off its debt if it were to devote all of its pre-tax cash flow to that task. As of March 31, 2023, Equitrans Midstream had a net debt of $6.877 billion. It had an adjusted EBITDA of $299.6 million during the first quarter, which works out to $1.1984 billion annualized. This gives the company a leverage ratio of 5.74x, which is higher than we really want to see. As I have pointed out numerous times in the past, Wall Street analysts generally consider anything below 5.0x to be acceptable. However, most midstream companies have been strengthening their balance sheets significantly since the pandemic as part of an effort to reduce or eliminate their dependence on the capital markets as a source of capital. As such, many of the best companies in the industry now have a ratio under 4.0x. Equitrans Midstream, therefore, looks incredibly heavily leveraged compared to its peers, which could pose a very real risk to investors. I will admit that I doubt that the company will have trouble carrying its leverage, but it is still important to be aware of this risk.

ETRN Dividend Analysis

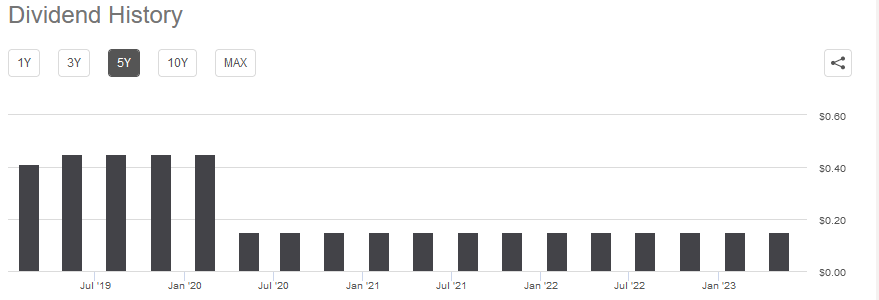

One of the biggest reasons why we invest in midstream companies is the incredibly high yield that these firms typically possess. This comes from the fact that they have fairly low growth and by extension fairly low multiples assigned to them by the market. As a result, they pay out most of their cash flows to the investors in order to provide a return that is competitive with more rapidly-growing companies. Equitrans Midstream is certainly no exception to this rule as the company's 7.31% yield is quite a bit higher than most things in the market. Unfortunately, Equitrans Midstream's dividend history leaves something to be desired, as the company slashed its dividend when the pandemic hit and has yet to restore it:

{kind=link}

This is disappointing, but the company is hardly alone in this respect. After all, there were a number of midstream companies that cut their dividends in response to the collapse in energy prices that accompanied the pandemic. These cuts came despite the fact that cash flows across the sector did not decline, which is due to the business model that was discussed earlier. The biggest reason for these cuts is that the market became very hostile to anything related to the fossil fuel industry and it was prudent to simply reduce debt and strengthen balance sheets to the point where none of these companies have to care what the market thinks. This is still the case today, although it would be nice to see Equitrans Midstream increase its dividend like peers such as Energy Transfer LP ( ET ) have done.

With that said, anyone buying the stock today will receive the current distribution at the current yield. As such, a new investor does not have to worry about the company's past. The most important thing today is the company's ability to maintain its dividend going forward.

The usual way that we judge a company's ability to pay its dividends is by looking at its free cash flow. The free cash flow is the amount of money that was generated by the company's ordinary operations and is left over after it pays all of its bills and makes all necessary capital expenditures. This is therefore the money that can be used for things such as reducing debt, buying back stock, or paying a dividend. In the first quarter of 2023, Equitrans Midstream reported a free cash flow of $94.221 million but the dividends only cost it $64.964 million quarterly. This gives the company a 1.45x coverage ratio, which is quite reasonable. The dividend should prove to be quite sustainable going forward so we should not need to worry about a cut in the future.

Conclusion

In conclusion, Equitrans Midstream Corporation continues to look like a pretty good way to play the strong market for natural gas and earn an income while doing it. The huge jump in the share price yesterday reduced the yield, but it still has a very acceptable one that appears to be sustainable. The biggest risk here is the company's debt load. Hopefully, it will be able to use some of its excess free cash flow to pay this down and strengthen the balance sheet. Overall, Equitrans Midstream Corporation is certainly worth considering today.

For further details see:

Equitrans Midstream: This 7.31%-Yielder Is Worth Considering Today