ETV - Equity CEFs: An Even Better Opportunity To Own The Eaton Vance Equity CEFs (ETJ And EXG)

2023-04-25 10:19:09 ET

Summary

- In early December of last year, I wrote an article saying that it was the best time to own the Eaton Vance equity CEFs since the COVID-19 pandemic.

- That was a result of distribution cuts declared a month earlier in November, which dropped the Eaton Vance CEFs from as high as 20% premiums to mostly discounts.

- But I also said in that article that bringing down the fund's NAV yields back-to the 7% to 9% sweet spot after the bear market of 2022 would mean better NAV growth and performance in 2023.

- And that's exactly what has happened as virtually all of the Eaton Vance equity CEFs are top one-third performers of the 100 or so largest and most popular equity CEFs I follow.

- However virtually all CEFs have been losing valuation over the past year which has only accelerated with the Fed reigning in liquidity. This tends to hit smaller cap securities like CEFs of $2 billion or less, but compared to most CEFs out there, the Eaton Vance funds are a steal right now.

On Dec. 9 of last year, I wrote this article:

Equity CEFs: Best Opportunity To Own The Eaton Vance CEFs All Year

... and I would suggest first reading that to get an understanding of where we are today.

Since that article, valuations for the vast majority of CEFs have moved even further down as the regional bank crisis in early March pretty much wiped out any valuation gains made by CEFs in January and February. Yes, the Fed has made available billions in liquidity for the banking system but virtually none of that is finding its way into CEFs.

And as a result, what we see today is the widest average discount valuation in CEFs since the early fallout from the COVID-19 pandemic in March of 2020. That's how bad it has gotten and if you own CEFs, you probably have seen that valuation compression in your funds at some point over the last year.

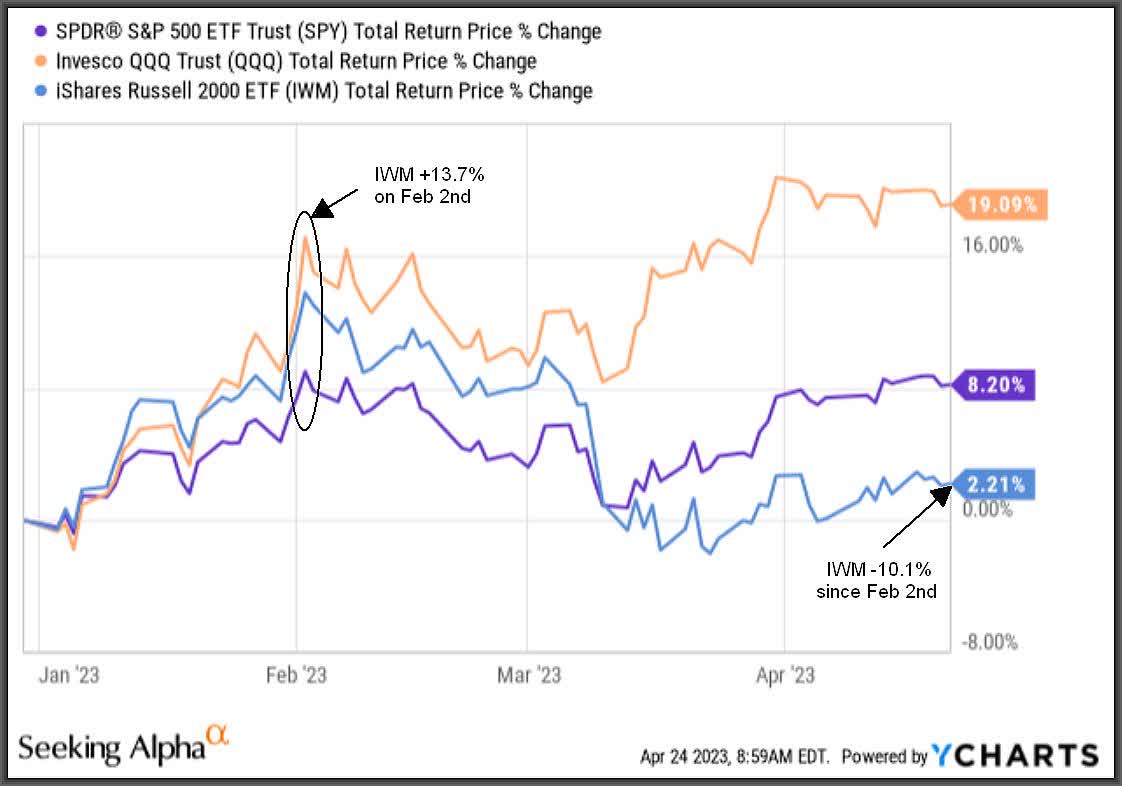

Part of the reason is that small-cap securities and stocks, i.e. less than $2 billion in market cap, have severely lagged in performance compared to the larger cap stocks which make-up most of the major market indexes like the S&P 500 ( SPY ) , $412.63 current market price , which is up +8.3% YTD and the Nasdaq-100 ( QQQ ) , $315.95 current market price , up +18.8% YTD.

You can see this when you compare YTD returns with the Russell 2000 Small Cap Index ETF ( IWM ) , $177.44 current market price , which was up +13.7% YTD by February 2nd, but has since dropped -10.1% to only a +2.2% gain today.

{kind=link}

Y-Charts

Now do most equity CEFs own small cap securities? Absolutely not, and the Eaton Vance equity CEFs own mostly large cap stocks from the S&P 500 and Nasdaq-100. But what's important to understand is that it's the size of the fund at less than $2 billion in market cap that is hurting liquidity and buy interest.

So if you believe, like I do, that the opportunities in equity CEFs haven't been this attractive in years but you also want to look at equity CEFs that have a measure of protection in case the markets tumble back down, then we're on the same page.

The Eaton Vance Equity CEFs Are Back On Top

Let me first show you the YTD NAV performances of the top one-third of the 100 largest and most popular equity CEFs I follow through last Friday.

As of 4/21/2023:

{kind=link}

Capital Income Management LLC

Note: Funds shown in light blue in the first four columns use an option-income strategy while funds in orange use a leveraged-income strategy. Funds in purple means an 'other' income strategy

Here you can see that only about 20 funds (shown in green above) are beating the S&P 500 ( SPY ) at total return NAV, which means that an additional two-thirds of the funds I follow would extend below the funds shown above in red.

That just goes to show you how dominant the major market averages have been this year as big money has gravitated to the safety and liquidity of the largest index ETFs and large cap stocks.

But let me highlight the nine Eaton Vance equity CEFs that populate the top one-third of the 100 equity CEFs I follow, since no other fund family comes close to having this many of their funds near the top in NAV performance:

{kind=link}

Capital Income Management

Now keep in mind, these are NAV total returns and NOT market price total returns, which are more reflective of investor sentiment and the low liquidity. NAV returns are the actual portfolio total returns i.e. NAV performance, whereas MKT price total return (column to right of NAV Tot Ret above) tend to reflect more of the greed and fear in the markets and are often contrarian indicators when they get extreme.

So if MKT price performance is based on investor sentiment, emotions and liquidity, you can see how shareholders could get this wrong and that's what I believe has happened to the Eaton Vance equity CEFs as their NAV's outperform while their market prices struggle.

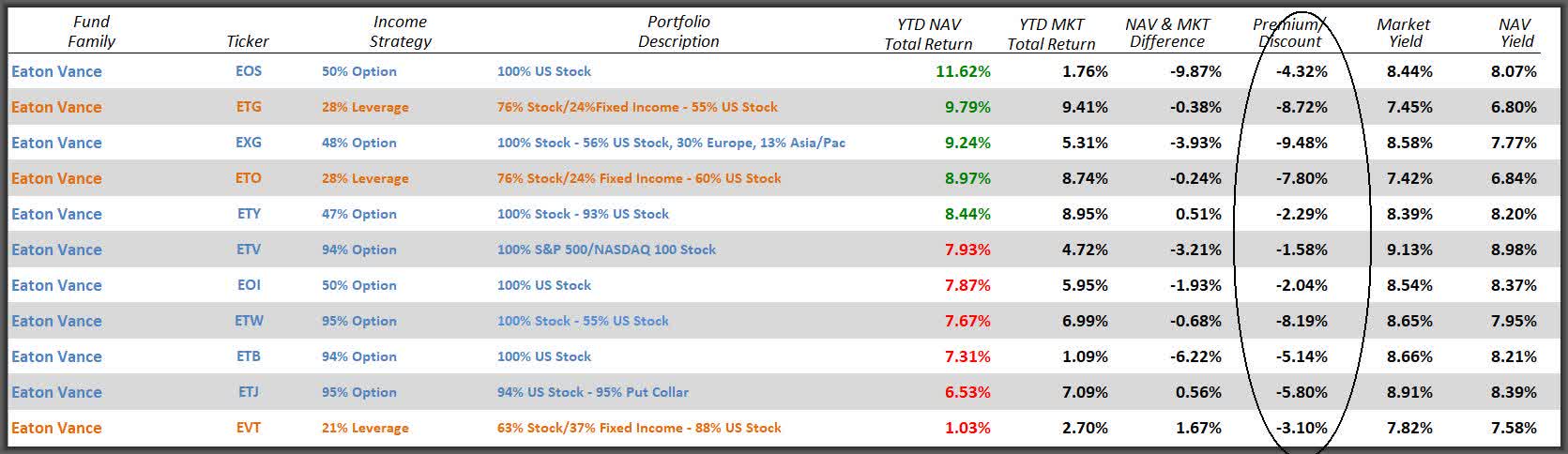

Focusing now on the Eaton Vance equity CEFs, here are their statistics for all of funds as of 4/21/2023:

{kind=link}

Capital Income Managment LLC

Note: List above has one less fund than list below as (EXD) was merged into the Eaton Vance Tax-Managed Buy-Write Opportunities fund ( ETV ) on April 14th

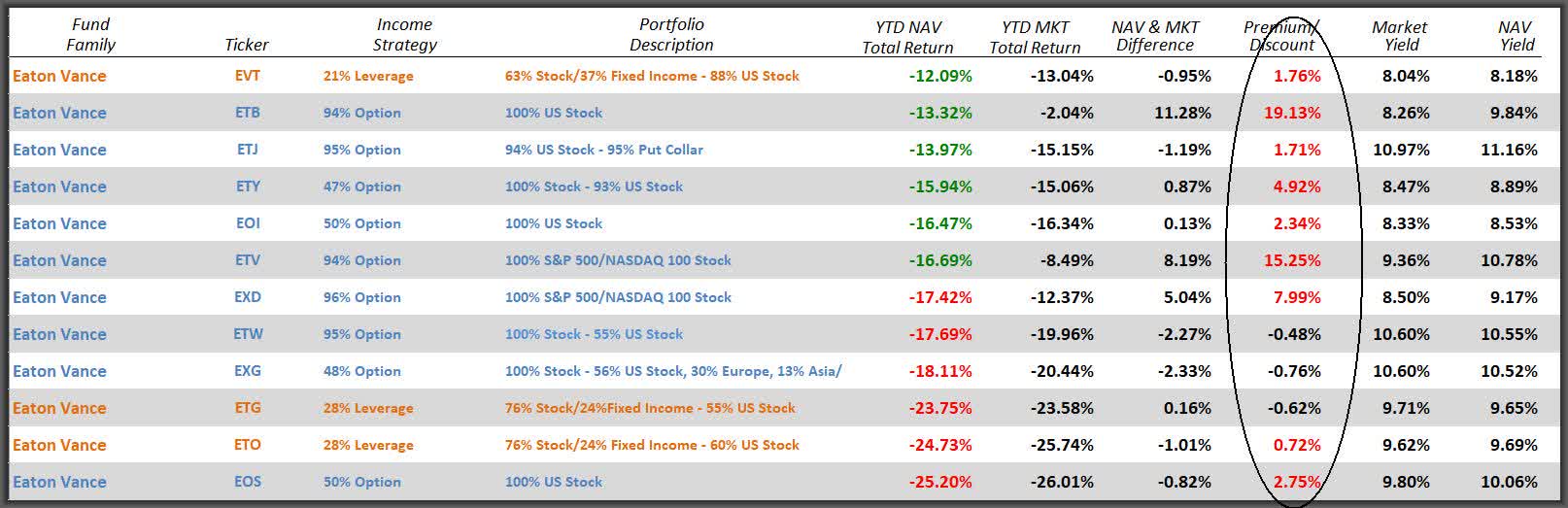

And to see the valuation collapse since then, here are the same funds (including EXD) from my last Equity CEF Performance update on October 28th, just before the distribution cut declarations on November 1st.

As of 10/28/2022:

{kind=link}

Capital Income Managment LLC

Here you can see in the circled Premium/Discount columns above how many of the Eaton Vance equity CEFs were at premiums at the end of October and how are at discounts today. Try all of them.

Now again, this is not just happening to Eaton Vance but between the strong NAV gains this year and the weak market prices due to the distribution cuts and the general lack of liquidity in CEFs, the Eaton Vance funds have seen one of the more dramatic valuation drops.

For example, the Eaton Vance Tax-Managed Buy/Write Income fund ( ETB ) , $12.87 current market price , has gone from a +19.1% premium as of late October to a -5.1% discount today. But does that seem fair simply because of a distribution cut that made it easier to cover its NAV distribution and grow its NAV?

If I graph ETB's NAV total return performance against the S&P 500 ( SPY ) , over that roughly six-month time frame from Oct. 28, ETB's NAV, i.e. portfolio appreciation, is beating SPY by almost 100 bps:

Note: Total Return NAV includes all monthly distributions for ETB and two dividends for SPY since October 28th amounting to $3.2876/share

So can we agree that the Eaton Vance distribution cuts were not necessarily a reg flag at all and may have contributed to their strong NAV performance since then? And ETB isn't even close to the best NAV performer of the Eaton Vance equity CEFs! That honor goes to the Eaton Vance Enhanced Equity Income II fund ( EOS ) , $16.32 current market price , which is up +11.4% at NAV this year even though its MKT price total return is only up +1.6% YTD.

Yes, EOS had a difficult 2022 just like all technology stock focused funds did, but once again, shareholders kept EOS at a premium market price valuation when it was at the bottom of the Eaton Vance list for NAV performance as of 10/28/22, but now is at the top of the list YTD and at a -4.3% discount. To me, that's just another example of a contrarian indicator, when you should be doing just the opposite of what the herd is doing.

And here's the final endorsement for the Eaton Vance equity CEFs. Due to the market price drops since the cuts 6-months ago, investors can get virtually the same market yield today than what the funds offered before the cuts were made.

Conclusion

In my experience with Closed-End funds, follow the NAV and eventually you'll find where the market price goes . Though virtually all CEFs, bond and equity, have seen valuation compression over the last year, not unlike what we saw during COVID-19 in 2020 and even the financial crisis of 2008; the question is, is it enough and if so, where are the best opportunities now?

I believe, based on NAV performances this year, reasonable NAV yields to cover and a variety of popular option-income and leveraged-income funds to choose from, nothing comes close to the opportunities I see in the Eaton Vance equity CEFs.

Because if you want to stick with funds that have portfolios that include the largest-cap stocks from the S&P 500 and Nasdaq-100 indexes as well as from international markets, mostly Europe, then that's what all the Eaton Vance CEFs include.

Which funds look the most attractive? That depends on where you think the markets are headed from here. The markets have been in a tight trading range this month and that is good news for the option-write funds but frankly, Eaton Vance has CEFs, ( ETO ) , ( ETG ) and ( EVT ) for a bull market as well as funds that are designed for a flat to even down market, i.e. option-write funds.

The best value opportunity among the Eaton Vance equity CEFs is probably the Eaton Vance Tax-Managed Global Diversified Equity Income fund ( EXG ) , $7.78 current market price.

EXG is a very large option-income fund that sells index options against roughly 50% of the notional value of its all-stock fund, mostly in the large cap S&P 500 and European stock names. Year to date, EXG's NAV is up an impressive +9.2% while its market price drop to $7.78 means you can buy EXG at a wide -9.2% discount.

If you're more concerned about a difficult market environment, then Eaton Vance has three funds, ( ETW ) , ( ETV ) and ( ETB ) that utilize an option strategy that writes index options against a very high 96% of the portfolio value of each fund.

And one option-income fund, the Eaton Vance Risk Managed Diversified Equity Income fund ( ETJ ) , $7.84 current market price , goes one step further and buys Put options against 96% of its portfolio value as well, making ETJ one of the most defensive funds you can buy.

In fact, ETJ was the only CEF I followed back in 2008 that was actually positive at market price during the financial crisis:

Let me repeat. Follow a fund's NAV and eventually you will find where a fund's market price goes.

And so far this year, the Eaton Vance equity CEFs are doing just fine at NAV and thus, I believe it is only a matter of time before their market prices catch up.

For further details see:

Equity CEFs: An Even Better Opportunity To Own The Eaton Vance Equity CEFs (ETJ And EXG)