QQQ - Equity CEFs: Best Opportunity To Own The Eaton Vance CEFs All Year

Summary

- Eaton Vance offers what may be the most popular equity-based closed-end funds available to income investors. As a result, the funds have been trading at mostly premium-market price valuations for some time.

- But all that momentum changed when on Nov. 1, Eaton Vance cut the distributions for virtually all of their equity CEFs, the first-cuts for many of their funds in years.

- Clearly, last month's distribution cuts has left a sour taste in investors' mouths and there continues to be selling overhead as valuations continue to drop.

- But unlike a lot of other fund families, Eaton Vance has bitten-the-bullet and now has all of their fund's NAV yields down to the 7% to 9% sweet spot range.

- So unless there's a strong market recovery in 2023, many funds are going to see continued NAV erosion while the Eaton Vance equity CEFs should be just fine.

Nobody likes to see distribution cuts in their CEFs, but when it's intended to better align a fund's future distributions with its expected income, then what may be taken as a short-term negative will end up being a long-term positive as pressure is taken off the NAV.

I prefer fund sponsors that are proactive and are willing to get ahead of what still might be coming in 2023 rather than fund sponsors who roll the dice and hope that their funds will be able to cover their 12% or higher NAV yields.

I have found that 7% to 9% NAV yields are the sweet spot for most equity CEFs which allows the fund to cover the yield while also giving the opportunity of NAV growth too. The problem with 12% or higher NAV yields is that if a fund can't reasonably be expected to cover their distributions, and each distribution shortfall just means that much less NAV to derive the next distribution.

This can create a spiral down in NAV erosion, and if a fund sponsor refuses to adjust the fund's distribution when needed, like during a bear market, then all it means is that there will need to be a much larger cut in the future and an inevitable market price collapse down the road.

This was the basis of many articles I wrote about the PIMCO Global StocksPlus & Income fund ( PGP ) , $6.98 current market price , from 2015 to 2017 when the fund got as high as a 106% market price premium due to PIMCO maintaining the fund's $0.1834/share monthly distribution for far too long.

I said in many articles over the years that it was only a matter of time before PIMCO would have to cut PGP's distribution and that finally happened on October 3rd of 2016.

I wrote this article, Equity CEFs: The Sum Of All Insanities - Part II , the day after. At the time, PGP was priced at $20.43 . Today, after four distribution cuts later, PGP is at $6.98 and is now at a discount.

That is an extreme example of what can happen when a fund sponsor refuses to adjust a fund's distribution while shareholders assume everything is fine, even while its NAV erodes and the market price premium skyrockets.

CEF NAV Distribution Policies

Today, many CEFs are set up automatically to adjust their distributions based on an annual NAV distribution policy that can adjust every year, every quarter and in some cases, every month now.

Some funds use a 6% NAV distribution policy, some use 8% to 10% NAV distribution policies, largely dependent on how aggressive the fund's income and appreciation strategy is, and one fund sponsor, Cornerstone, goes to the extreme and sets a 21% NAV distribution policy each year even though they admit, that has nothing to do with the actual yield of the funds to expect.

Personally though, I would much rather own funds from a CEF sponsor like Eaton Vance, which doesn't use NAV distribution policies but instead uses a managed distribution approach that doesn't necessarily have to change their funds distributions at certain times but will adjust based on what they project the funds should comfortably be able to cover while maintaining their NAVs.

So here's how all of the 12 Eaton Vance equity CEFs look YTD as of December 8th, 2022, sorted by their total return NAV performance.

Note: Green in the YTD NAV Total Return column means the fund's NAV is beating the S&P 500, -16.5% YTD, while those in red are trailing the S&P 500

{kind=link}

The far-right column in yellow shows all of the fund's NAV yields since the distribution cuts and as you can see, all of the funds are now in the 7% to 9% sweet spot range.

Note: Funds in light blue above use an option income strategy while the 3 Eaton Vance funds in orange use a leveraged income strategy.

I should also mention that two of the Eaton Vance equity CEF funds, the Tax-Managed Buy/Write Strategy fund ( EXD ) , $9.85 current market price , and the Enhanced Equity Income fund ( EOI ) , $16.48 current market price , did NOT have a distribution cut on November 1st.

Here's the Nov. 1 distribution declaration from Eaton Vance for all of their CEFs, fixed-income and equity:

Which Eaton Vance CEFs Are Now Most Attractive

If you believe, like I do, that Eaton Vance offers the best lineup of equity CEFs for the long run, you can now buy many of them at discounts instead of double-digit premiums.

Here's a two-month Premium/Discount chart that shows how the EV funds were largely at premiums of up to 16% or more at the end of October but have now largely moved down to discounts since the distribution cut declaration on Nov. 1:

Picking which Eaton Vance CEFs offer the best opportunities now depends largely on whether you believe 2023 will be a continuation of the bear market or if we see a rebound in the equity markets.

If you believe 2023 will still be a tough year though not as bad as 2022, my first pick would be the Eaton Vance Tax-Managed Global Buy-Write Opportunity fund ( ETW ) , $8.02 current market price.

ETW is a very defensive option-income CEF that sells index options against a very high 96% of the fund's large cap global stock portfolio. That brings in an immense amount of option premium income while offsetting downside exposure in the portfolio.

So why was ETW one of the funds that cut its distribution? What you need to understand about the Eaton Vance equity CEFs is that for years, most of the funds over-weighted the mega-cap technology names like Apple ( OTC:APPL ) , Microsoft ( MSFT ) , Amazon ( AMZN ) , Alphabet ( GOOGL ) , Tesla ( TSLA ) , etc. so even though ETW's NAV is beating the S&P 500 YTD (see table above), this large exposure to the tech heavy Nasdaq-100 ( QQQ ) , down -28.3% YTD, has certainly been a drag, not only on ETW, but on many of the Eaton Vance funds this year.

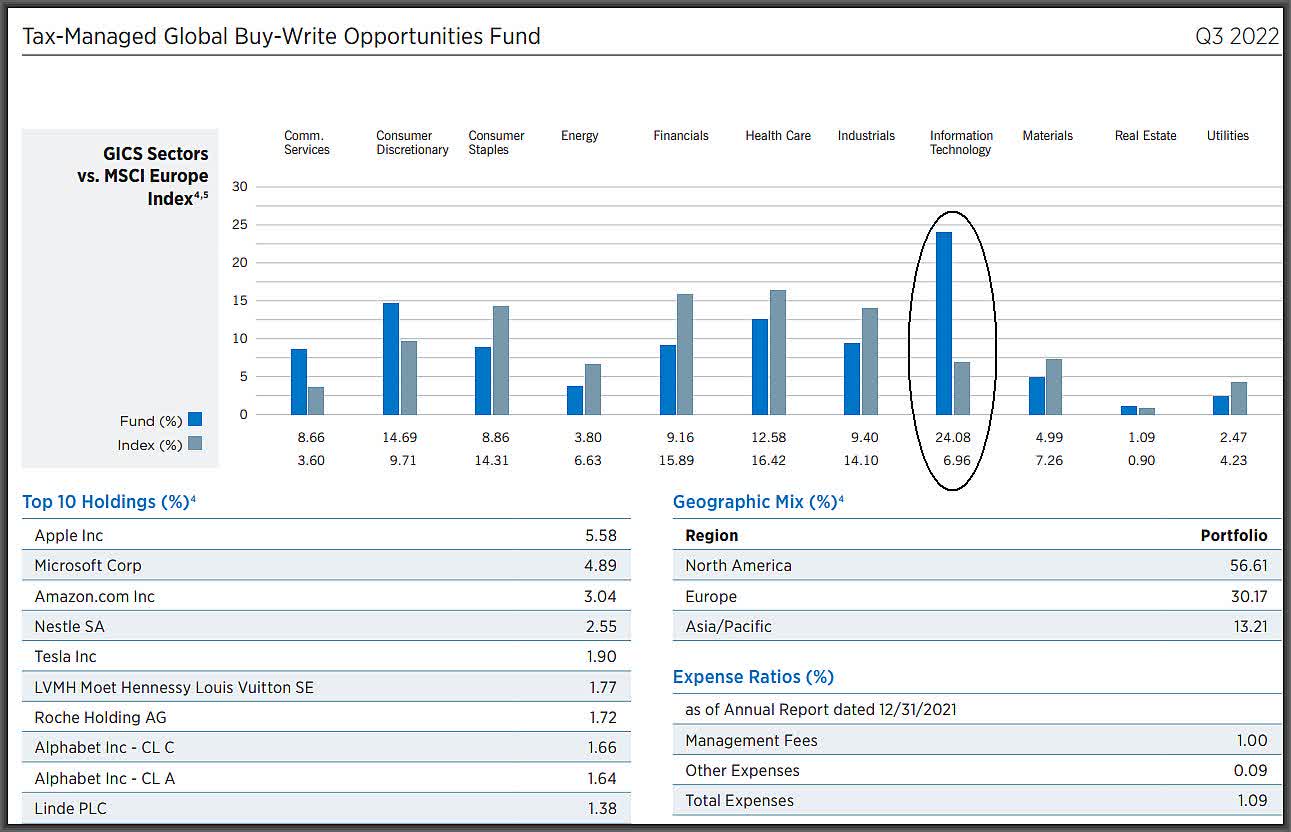

For example, here is ETW's sector breakdown as of 9/30/22 and you can see how much higher the percentage ETW carries in the Information Technology sector (circled), i.e. 24% , than the index allocates, i.e. 7% .

You can also see that in its top 10 holdings:

{kind=link}

But even with this high technology exposure, ETW's very defensive option write strategy means that the fund has largely offset the bear market in technology stocks this year, with its NAV down only -13.9% YTD.

So with the distribution cut from $0.0727/share to $0.0582/share per month declared on Nov. 1, ETW's NAV yield went from 10.1% down to a current 8.1% . That's extremely conservative considering how defensive ETW is so with the fund now at a -7% discount, ETW is a strong Buy here at $8.00 .

And if information technology happens to rebound in 2023, all the better for ETW.

Eaton Vance's Leveraged Equity CEFs

What's nice about the Eaton Vance lineup of equity CEFs is that they offer extremely defensive option income CEFs, like ETW, for a flat to volatile market environment and they offer very aggressive, leveraged equity based CEFs for a bull market.

So if you believe 2023 will see a rebound in the markets, Eaton Vance's three leveraged equity CEFs, the Eaton Vance Tax-Advantaged Global Dividend Income fund ( ETG ) , $15.76 current market price, the Eaton Vance Tax-Advantaged Global Dividend Opportunity fund ( ETO ) , $21.59 current market price and the Eaton Vance Tax-Advantaged Dividend Income fund ( EVT ) , $23.97 current market price, offer some of the best long-term returns of all equity CEFs.

You know how you can tell which leveraged equity CEFs have been managed in the shareholder's interest and are the best ones to hold onto? Their NAVs are close to or even higher today, even after all those monthly distributions, than when they came public.

The vast majority of CEFs can't say that but for the leveraged equity CEFs from Eaton Vance, which came public in 2003 and 2004 with $19.10 inception NAV values, EVT now has a $24.48 NAV, ETO has a $23.41 NAV and ETG has a current $17.04 NAV.

And if you go to the YTD table above, you'll see that EVT is leading all of the Eaton Vance equity CEFS in NAV performance, down just -9.4% YTD. That's because EVT offers a more value stock focused portfolio and doesn't overweight the tech sector.

So which of the Eaton Vance leveraged CEFs offer the best upside in a strong market rebound in 2023? There's little doubt that both the Tax-Advantaged Global Dividend Income fund ( ETG ) and the Tax-Advantaged Global Dividend Opportunity fund ( ETO ) , would be the big winners at NAV and MKT price if we see a market rebound next year, particularly if the beaten down technology mega-cap stocks recover.

Though both funds have underperformed the S&P 500 so far this year, with ETG's NAV down -19.5% YTD and ETO's down -20.5% (see above), that's because like many of the Eaton Vance option-income CEFs, they have a high information technology sector exposure and the leverage has just contributed to that downside.

But to offset the volatility that leverage brings and to add income, all three of the Eaton Vance leveraged CEFs also include roughly 12% to 15% exposure in preferred securities and corporate bonds. ETO and ETG also have significant exposure to global stocks, roughly 30% of which is represented in large-cap European stocks.

Here is ETO's latest Fact Sheet , which would not be that much different than ETG's, only that ETO is a much smaller fund than ETG:

Conclusion

Nobody knows what 2023 will bring, but for income investors who want a more conservative approach from their CEF fund sponsors heading into the new year. I believe Eaton Vance should be at the top of their list now whether they want a defensive or offensive income strategy.

Add to that the fact that many of the Eaton Vance funds are now at discounts of up to -7% due to the distribution cuts, and that just makes the Eaton Vance funds that much more attractive.

Or, on the other hand, you can roll the dice and buy equity CEFs at up to 55% market price premiums that haven't cut their distributions yet even with NAVs down up to -40% on the year. All I can say is good luck with those funds.

For further details see:

Equity CEFs: Best Opportunity To Own The Eaton Vance CEFs All Year