ETV - Equity CEFs: Buy ETB As We Enter The Dumb Stage Of The CEF Sell-Off

2023-10-27 12:36:00 ET

Summary

- This happened in the fall of 2008 during the toxic mortgage crisis and in March 2020 during COVID-19. You see CEF shareholders sell at any price just to get out.

- Though this year has been more of a slow-motion crash in equity CEFs, that's not to say that we won't get a spike down sell-off that could see CEFs briefly hit -25% discounts or more.

- We had a name for when that happened. We'd call it the "dumb stage" of a market sell-off, and it could last one or two days before a recovery.

- We called it that not just because you'd be "dumb" to sell but also because most investors would be too scared to buy as well.

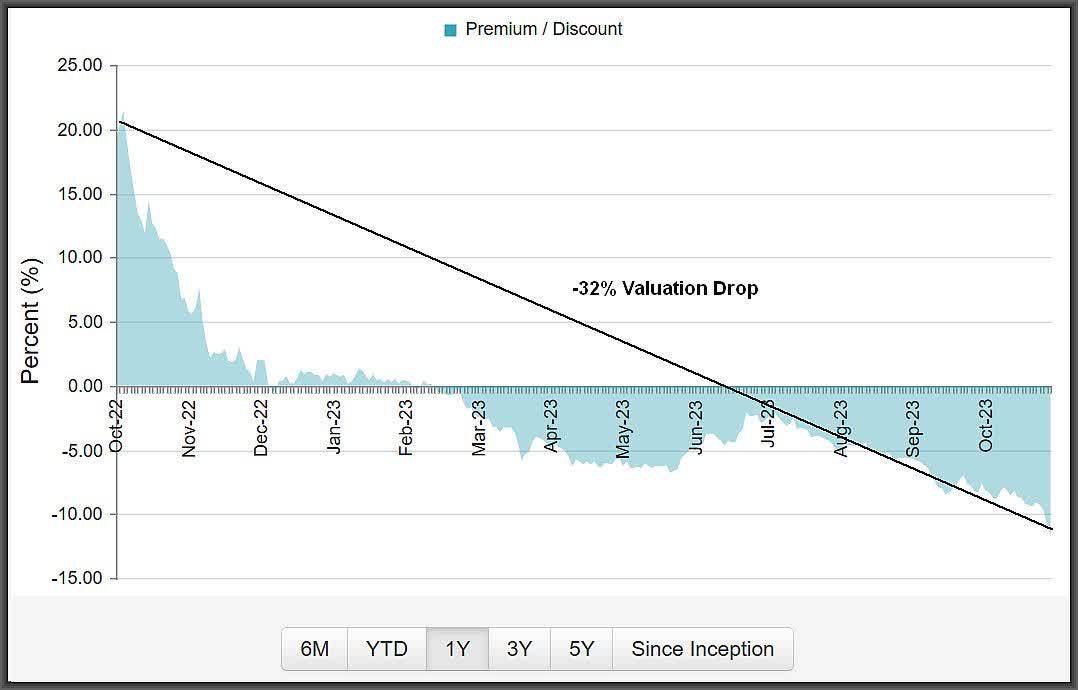

- This is why a fund like the Eaton Vance Tax-Managed Buy-Write Income fund is becoming so attractive after losing -32% of its valuation already.

Are we getting close to the "dumb stage" in this equity CEF sell-off that's frankly been just as bad as the worst days back in 2008 and in March of 2020? Only we haven't seen the climactic whoosh down yet?

Over the past year, we've seen CEF valuation collapses that rival anything that we saw during the financial crisis of 2008 or COVID-19 in 2020, only this year, it has been more spread out over a longer period of time.

For example, take a look at the Eaton Vance Tax-Managed Buy-Write Income fund ( ETB ) , $11.69 real-time market price , 1-Year Premium/Discount chart:

{kind=link}

Now maybe ETB should not have risen to a 20%-plus premium in the first place, though it did handily outperform its benchmark S&P 500 ( SPY ) , $412.55 closing market price , last year when ETB's NAV was down only -12.9% vs SPY's -18.1% , including distributions.

So it seems to me that a fund whose portfolio and income strategy are outperforming its benchmark by that much should not be losing valuation to the tune of a -32% valuation drop over the past year.

In fact, even with a mostly upmarket over the past year, ETB's NAV has more than kept up with the S&P 500 at NAV:

In essence, what ETB, and in fact all of these uber-defensive option-income CEFs do, is smooth out returns such that you don't capture all of the upside, i.e., shown above when the markets were rallying and hitting their highs in June and July and when the S&P 500 (in orange) sped ahead of ETB.

But when the markets are weak, ETB's NAV starts to outperform the S&P 500. Thus, ETB's NAV has a far lower beta than the S&P 500, and in fact, is one of the most defensive option-income CEFs you can buy, selling index options against 96% of its portfolio value. What does that mean?

First off, it means that ETB's NAV will continue to outperform the S&P 500 in a down market environment, and we can see that just from those market highs since the end of July to today:

That's over a 300-basis point improvement over three months and yet ETB's market price has dropped another -13.3% despite that NAV outperformance.

How is that justified? That means that if this market sell-off continues, ETB's NAV will just continue to outperform the S&P 500.

How do I know that ETB, and in fact, many of the Eaton Vance uber-defensive option-income CEFs like ( ETV ) , ( ETW ) and ( ETJ ), will be survivors in case we go into a more serious downtrend or bear market?

Because Eaton Vance is the only fund sponsor that, because of the volume of options they write, are able to write (sell) options every few days rather than once a month, which is what all other fund sponsors have to use, both CEFs and ETFs.

Why is that an advantage? Because there will always be fresh options being put on (and in the case of ETJ, fresh Put options) whereas the downside protection of a monthly option can be used up quickly if the markets drop quickly.

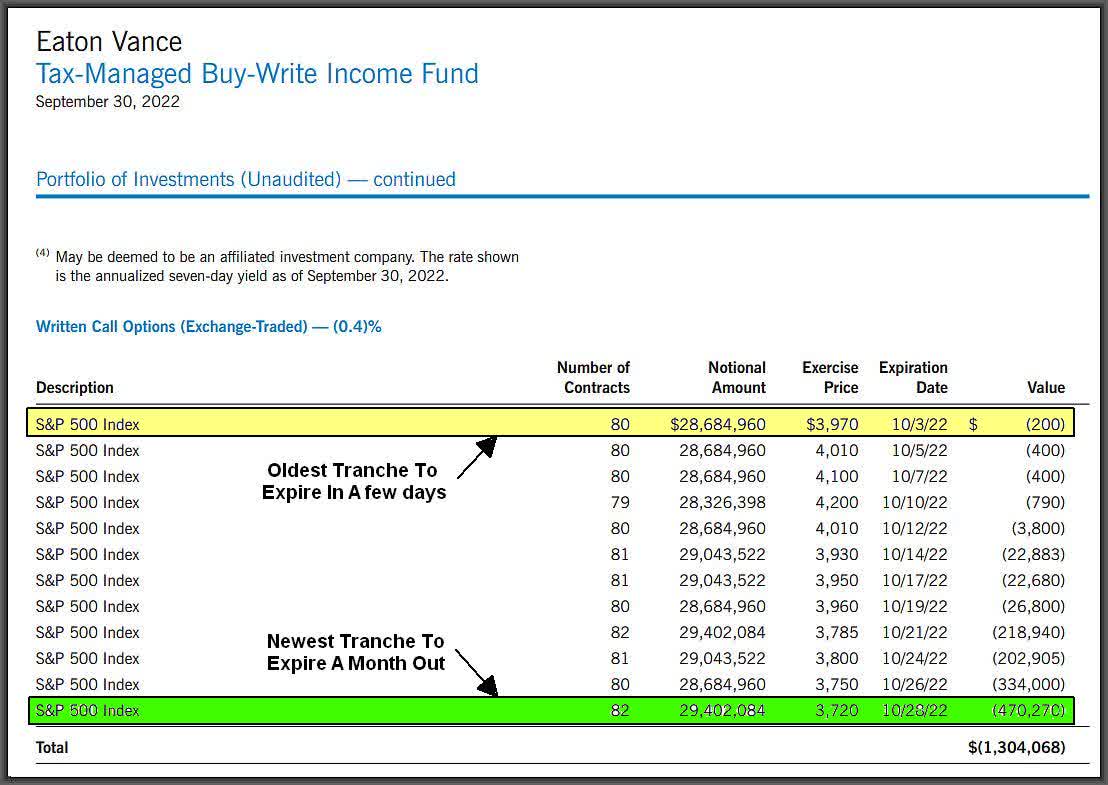

Let's use ETB's option sleeve from 9/30/22 as an example, since it's not unlike what we are experiencing this year in the September to October time frame as well.

First, here is ETB's third quarter 2022 po rtfolio data that I will be using for this analysis:

{kind=link}

Note: The market low from last year was on Oct. 14, 2022:

So what are we looking at here? ETB is one of the smaller Eaton Vance option-income CEFs so this should be easier to explain.

What you're looking at is ETB's option sleeve looking out a month from 9/30/22. The farthest out option tranche (one month approximately) is the most recent ones put on and they are the 82 contracts sold for approximately ($470,270) and due to expire on 10/28/22.

Since we know September was a mostly down month, along with October last year, you can see how the oldest contract tranche, the 80 at the top of the list due to expire on 10/3/22 are essentially worthless.

That's good for the fund because they also were sold for roughly $470,000 too but have been worn down in value over the month of September as the markets struggled.

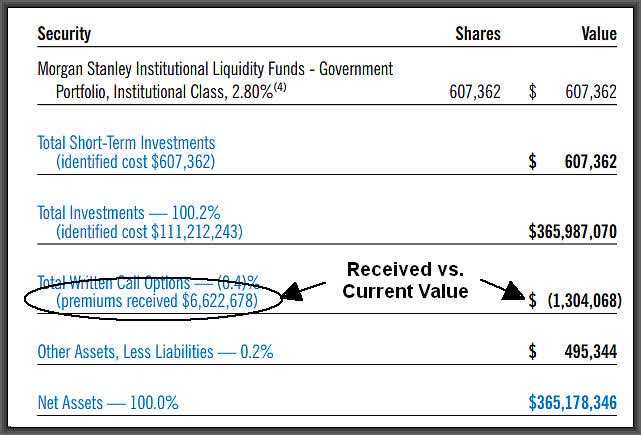

So collectively during this mostly negative September of last year, here's what ETB's total asset/debits looked like as of 9/30/22:

{kind=link}

So, if you took all of the written call options on the S&P 500 that ETB had sold and were still outstanding (see tranche list above), they would have totaled ($6,622,678) of option premium received but were only worth ($1,304,068) at the end of September.

That's well over a $5 million unrealized gain that would become realized as each option expired. And since we know there are 29,374,715 shares of ETB outstanding, ETB's monthly distribution of $0.0932/share would amount to $2,737,723 .

Note: ETB's market yield is a generous 9.6% for any current buyer, which is a windfall over its 8.5% NAV yield.

So in a flat to down market, ETB can easily cover its distribution nut and even realize gains too. Of course, that would be offset against ETB's portfolio of stocks that would probably be going down at the same time, but that's part of the overall strategy of these uber-high option-writing CEFs to offer tax-advantaged distributions while smoothing out returns.

Conclusion

This is why I say that ETB, and a host of other uber-defensive option-income CEFs, should not be losing valuation in a difficult market environment, but should actually be gaining valuation for holding up better at NAV than their benchmarks.

But as we know, just because funds like ETB can outperform at NAV, doesn't mean emotional shareholders won't continue to sell down these funds at market prices to lower-and-lower valuations.

And that's exactly what has been happening over the past year in this slow-motion train wreck. I actually started warning investors to lighten up on equity CEFs back in March when the regional banking crisis first hit since it was clear to me that less liquid securities like CEFs would suffer compounded valuation declines as institutional investors liquidated to reduce debt, and then more recently, individual shareholders finally threw in the towel when they couldn't the pain any longer.

I can't say for sure if this is the worst of the valuation declines in CEFs and we could still see that dreaded spike down if the markets finally break, but that would represent an even better opportunity to be buying equity CEFs like ETB, and I'm already starting to do just that.

For further details see:

Equity CEFs: Buy ETB As We Enter The Dumb Stage Of The CEF Sell-Off