ETB - Equity CEFs: Initiating ETB With A Strong Buy

Summary

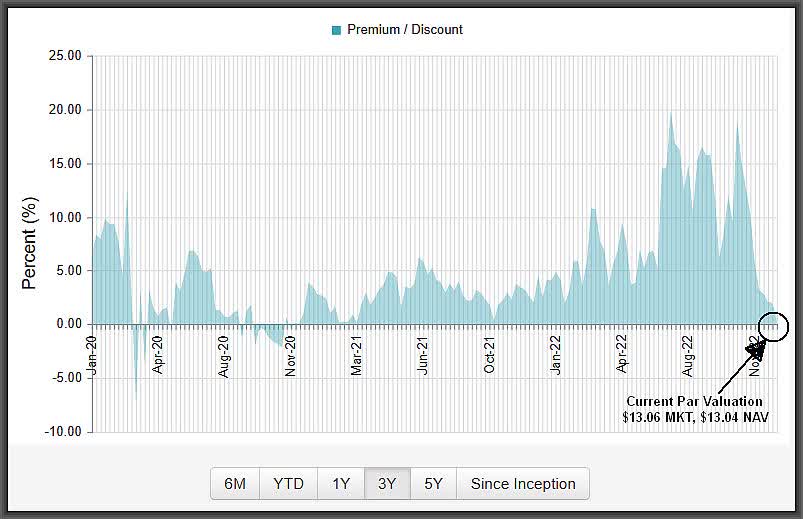

- I've avoided the Eaton Vance Tax-Managed Buy-Write Income Fund for years as it rose to a higher-and-higher premium which reached 20%-plus as recently as October.

- ETB is one of Eaton Vance's smaller equity CEFs at only $382 million in assets, so it will trade with more volatility at market price.

- ETB is one of the more value stock-focused funds among Eaton Vance's option funds so is better protected in case the Nasdaq-100 underperforms again.

- This helped ETB's NAV hold up much better at NAV than the more growth-focused Eaton Vance option funds and was down only -12.9% last year.

- That's much better than all of Eaton Vance's other option funds and much better than the S&P 500 down -18.2%. With ETB's valuation now down to about par value along with all of the Eaton Vance equity CEFs due to a distribution cut in November, I believe now is the time to buy ETB.

I've waited for years for the Eaton Vance Tax-Managed Buy-Write Income Fund ( ETB ) , $13.06 current market price , to come down in valuation from its perpetual premium and that has finally happened.

Here's ETB's three-year Premium/Discount graph:

{kind=link}

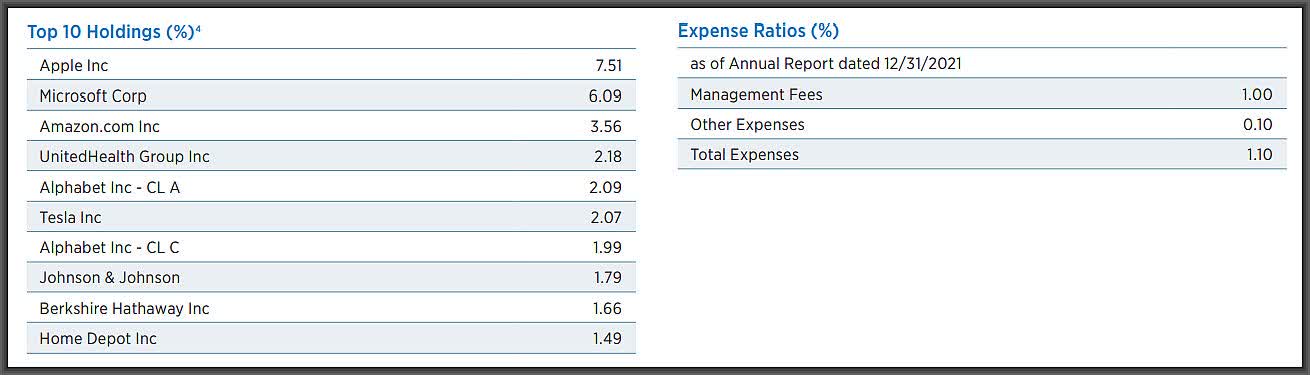

Though like many of the other Eaton Vance option-income CEFs which have the large-cap technology names among their top holdings, ETB is actually more value stock focused than any of them.

Combine that with an option-write strategy on the S&P 500 index covering a relatively high 95% of the notional value of ETB's all-US stock holdings, and that explains ETB's NAV outperformance last year.

Here's ETB's Top 10 holdings as of 9/30/22 and relatively low expense ratio considering ETB's 8.6% current market yield paid monthly:

{kind=link}

So why has ETB come down so much at market price, down -16.6% in 2022, when its NAV was holding up the best of all the Eaton Vance option funds last year, down only -12.9% ?

Y Charts

It really has to do with the distribution cuts in November for most of the Eaton Vance equity CEFs, including ETB, which triggered waves of selling in the funds all the way up to year-end with tax-loss selling and when most of the funds closed near their 52-week lows.

But that's short sighted in my opinion since this makes the Eaton Vance option-CEFs in a much better position to ride out any further market turmoil in 2023 compared to some other fund families which did not cut their funds distributions last year but should have.

Virtually all equity CEFs saw their NAV yields go up dramatically last year as their NAVs eroded in the bear market. But once you start getting to 10% to 12% NAV yields, that makes it a lot harder to cover those yields and maintain NAV.

Eaton Vance is one of the more pro-active CEF fund managers and so on November 1st , when many of their funds, including ETB, were over the 10% + NAV yield red-zone during the market lows in early to mid October, distribution cuts were declared for most of their funds to get them down to the more sweet-spot 7% to 9% NAV yields.

That included ETB's cut from $0.108/share per month to $0.0932/share, which you can see below:

The irony in all this is that with the market price drops since the distribution cuts, the current market yields for most of the Eaton Vance equity CEFs aren't that much different than before the cuts when many of the funds traded at premiums.

For example, ETB's market yield on Oct. 31 of last year, just before the declaration cuts, was 8.2% ( $1.296 annualized distribution divided by $15.83 market price on 10/31/22).

Today, with the lower distribution of $1.1184 annualized ( $0.0932 X 12) divided by ETB's current market price of $13.06 , that equates to an even higher 8.6% current market yield for anyone buying today!

As a result, I believe this is one of the most opportunistic times to buy ETB in years. ETB has the most growth AND value all US-stock portfolio of all the Eaton Vance option CEFs while utilizing a very defensive option-write strategy on the S&P 500.

And with a current market yield that is higher now than before the distribution cut, making it much easier for ETB to cover its current 8.6% NAV yield, all the stars are aligning for a much better 2023 for ETB.

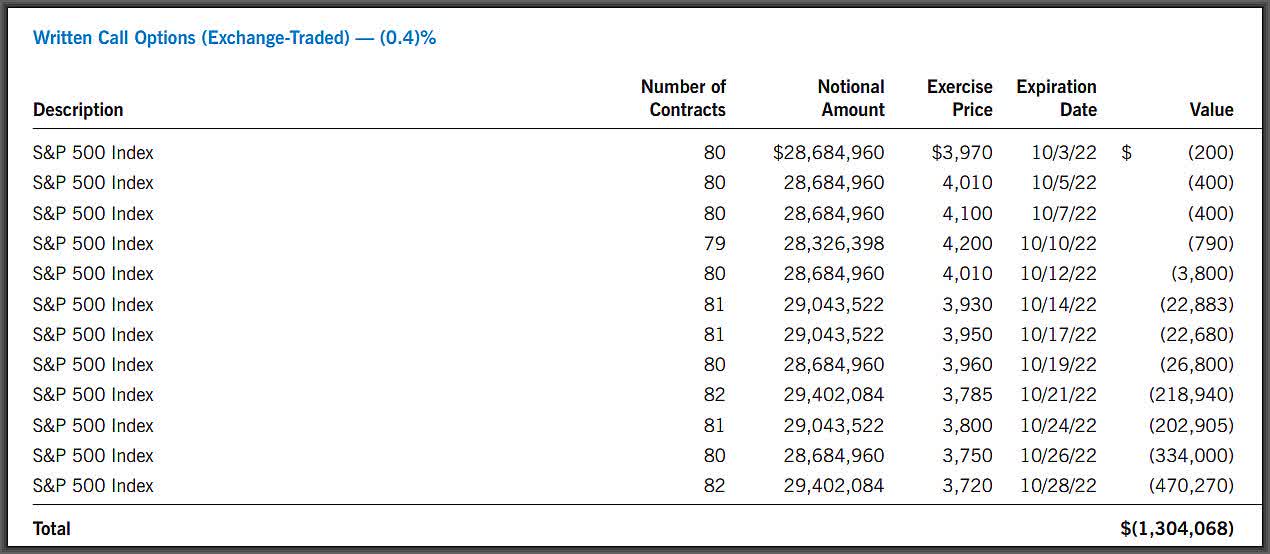

Finally, I've mentioned that Eaton Vance is the only fund sponsor of option-income CEFs that is able to secure a counterparty that provides option placements every few days rather than every month.

This is a huge advantage to the Eaton Vance option CEFs to have rolling option expirations every few days since this largely gets around the problem that most option-income funds have, both CEFs and ETFs, when their monthly options expire at inopportune times.

Here's a typical option sleeve for ETB at the end of the third quarter showing the multiple expiration placements covering the month of October:

{kind=link}

If you have any questions on what this is showing, just ask.

Note: Prices may have changed since I started this article earlier this morning

For further details see:

Equity CEFs: Initiating ETB With A Strong Buy