SBNY - Equity CEFs: No Rush On BTO

2023-03-22 13:59:52 ET

Summary

- The John Hancock Financial Opportunities fund (BTO) has had an enviable record over the years as one of the most successful equity CEFs of all time.

- But these last few weeks in the financial sector have showed that no fund is immune from a crisis.

- The bad news for BTO is that the fund focuses in the hard-hit regional bank sector, which has now seen three banks go insolvent while others are wavering.

- However, the good news for BTO is that the portfolio managers have mostly avoided the most troubled regional banks, like Silicon Valley Bank, when you look at their end-of-year portfolio holdings.

- But with BTO at a current +12.9% market price premium while also having the worst NAV performance of all equity CEFs I follow year-to-date, I think there will be a better moment to step up.

The first thing to know about the John Hancock Financial Opportunities Fund ( BTO ) , $29.76 real time market price , -3.7% , is that the fund is second to none among equity CEFs in terms of total return over the years and has had a stellar performance record during both bull and bear periods in the markets.

{kind=link}

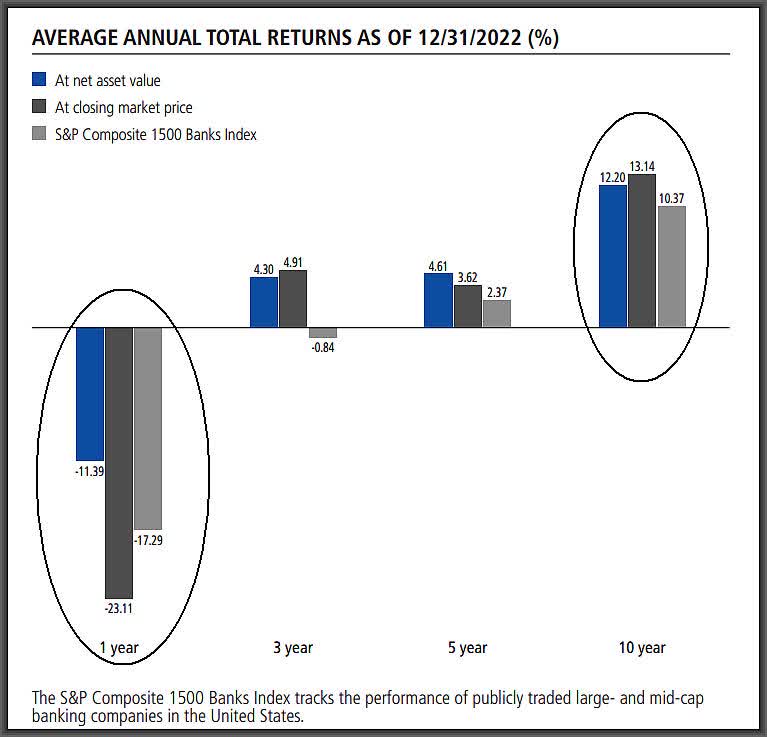

Whether it was during the bear market of 2022 in which BTO's NAV fell only -11.4% (circled above in blue) compared to its benchmark down -17.3% or over a longer 10-year mostly bull market cycle (second circle above) in which BTO's NAV has outperformed an S&P Composite index of 1,500 large and mid-cap banks, +12.2% annualized vs. +10.4% for the index, those are the kind of performance figures you want to see from your fund.

And to boot, BTO's total return market price over that 10-year period was an even better 13.1% annualized (black bar above).

Note: NAV total return performance is the true apples-to-apples comparison with a fund's benchmark whereas MKT total return performance reflects shareholder sentiment towards the fund, often reflecting the greed or fear factor that can result in a significantly higher or lower MKT price and performance

Maybe it's because John Hancock is a financial institution itself but no matter how you slice i, BTO's portfolio managers , have done an incredible job over the years balancing risk and reward in a 16.5% leveraged fund of mostly large-cap to medium-cap sized bank/financial common stocks with roughly 6% of the portfolio in bank preferreds and corporate bonds.

Here is BTO's Fact Sheet as of 12/30/2022:

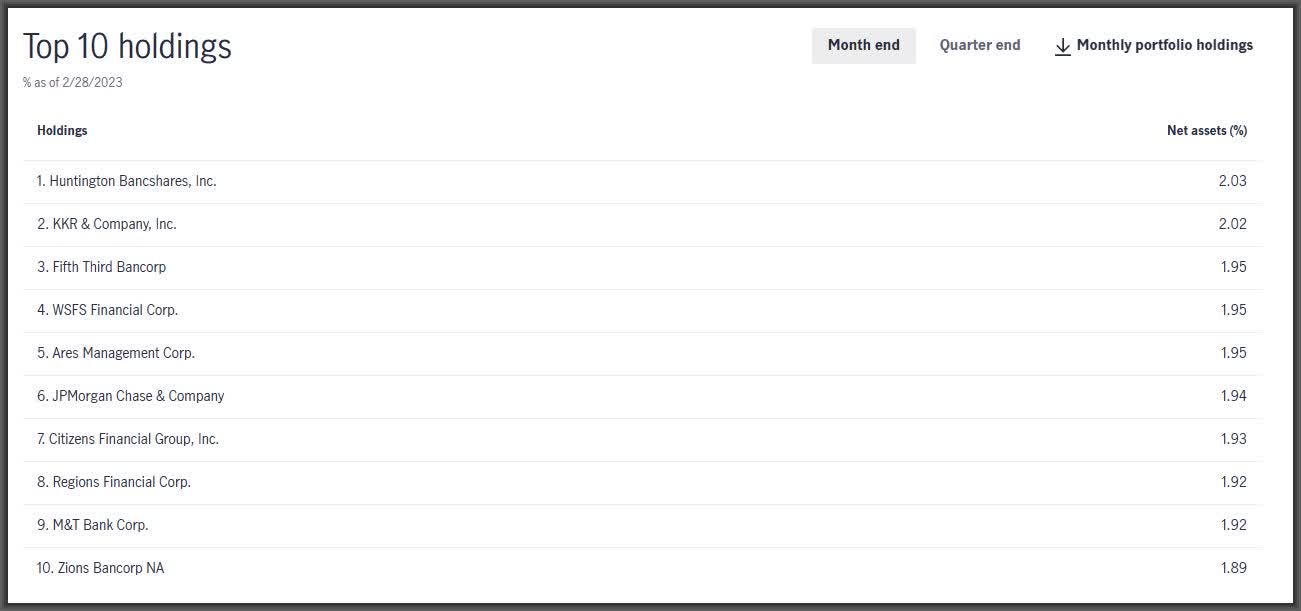

And here's an updated Top 10 Holdings as of 2/28/2023:

{kind=link}

Clearly though, not even BTO was going to come out of this unscathed with 156 bank holdings, mostly in the regional bank space. But just looking at the fund's holdings from its Annual Report as of 12/30/2022, I don't see any of the regional banks that have gone into bankruptcy or receivership this year and not even First Republic Bank ( FRC ), $15.20 real time market price, -3.5% , the latest bank to be teetering, shows up among its holdings, so that gives me a lot of confidence that the portfolio managers were well ahead of this problem even if they didn't know the extent of the fallout that would come to all regional banks.

Note: BTO's latest portfolio holdings are as of 12/30/22 while the latest Top 10 holdings are as of 2/28/2023.

Silicon Valley Bank Debacle

After the 2022 bear market and the Federal Reserve's campaign to raise interest rates from essentially 0% to roughly 5% in the span of a year, the fastest on record, it finally looked like inflation was coming down and the Fed's work was having its designed effect and 2023 would be more about rates being "higher for longer" rather than "how much higher" do we go?

But little did the markets know that there were already cracks in the armor appearing due to that unprecedented rate rise and that not all banks and financial institutions were prepared for it.

The liquidation of Silicon Valley Bank ( SIVB ), Signature Bank ( SBNY ) and Silvergate Capital Corporation ( SI ) over the last few weeks was due to a confluence of factors that, so far, seem to be specific to these certain financial institutions though Wall Street already is trying to figure out how serious this problem could get and who might be next, like with First Republic Bank, which could be up or down 25% or more at any given moment.

Though I don't believe this is anything close to the 2008 financial crisis, which was all about sub-prime mortgages metastasizing in the economy for years before they finally blew up, perception can be reality, and right now, we have a guilty until proven innocent environment in which most all regional banks have fallen significantly and even the larger cap money center banks have come down hard too.

This really all started just a few weeks ago when it was realized that for financial institutions that had an undiversified client base (for example, Silicon Valley Bank was heavily reliant on its venture capital and technology company clientele) and were seeing rapid deposit and cash depletion combined with unrealized losses in their treasury holdings and other lower yield investments, that their debt-to-equity ratio was essentially at insolvency levels. As a result, Silicon Valley Bank tried to raise cash by selling its treasury and mortgage-backed securities (MBS) at a huge loss (while trying to issue debt at the same time) but that only served to spook the markets and depositors alike and thus began the run on the bank.

Now I don't profess to know the banking sector requirements and regulatory rules, like stress tests or capital requirements, very well but when heavily leveraged institutions like banks are losing deposits, are seeing loans like in commercial real estate becoming non-performing and are seeing their large holdings of readily convertible-to-cash like investments go down in value as interest rates went up, you don't have to be a genius to figure out that at some point, the balance tilts toward bankruptcy.

What's surprising is that hardly anybody saw this coming but one who did happens to be a contributor here on Seeking Alpha called CashFlow Hunter, and he wrote this article on Dec. 19 of last year, SIVB: Blow Up Risk , well before the crash in the regional banking sector.

BTW, I listen to a popular podcast calle d All-In , whi ch has 328,000 subscribers on YouTube , and they actually singled out CashFlow Hunter on their latest episode last weekend as the only person who predicted this to happen!

Back To BTO

In any event, to see the damage that has been suffered in the financial sector as a result, here are the YTD performances of the SPDR Financial Select ETF ( XLF ) , the SPDR S&P Regional Banking ETF ( KRE ) and for the John Hancock Financial Opportunities fund ( BTO ) :

And though the losses for XLF are not really that material and in fact, most feel as if the beneficiaries of the regional bank fallout will be the large money-center banks like JPMorgan ( JPM ), Bank of America ( BAC ), Citigroup ( C ), Wells Fargo ( WFC ), the NAV losses (i.e. portfolio depreciation) are quite a bit more serious for KRE and BTO.

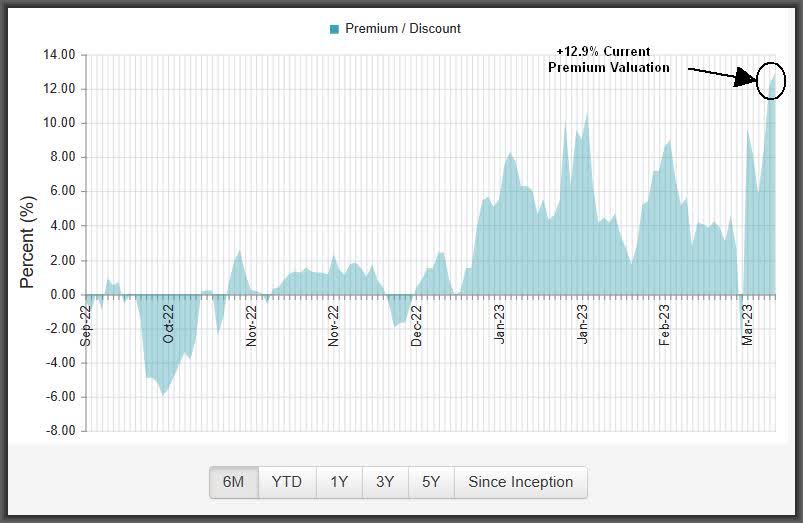

But it's when you look at the Market Price total return, you can see how BTO's market price has actually held up much better than its NAV, down only -7.3% YTD as of the close on Tuesday, March 21.

And this is why BTO's premium has actually risen quite a bit even as its NAV and MKT price have come down. Here's a six-month Premium/Discount chart for BTO:

{kind=link}

Give BTO Time

On Friday, March 10, when the regional bank crisis really began, I wrote to my subscribers, Should You Be Buying BTO Here? (subscription required) when BTO fell -7.5% from $32.45 to $30.02, including BTO's $0.65/share distribution that also happened that day .

I even put in a low bid of $29.95 on that day, which just missed getting executed, though I did end up buying a small number of shares in ensuing days when BTO fell as low as $26.11 intraday.

I sold those shares yesterday over $31, not because I don't want to be a long-term holder of BTO but because it appears this regional bank crisis may not be over yet.

Part of the problem is that a "run on deposits" could happen at any time to any regional bank based on speculative or real news and this is why a regional bank coalition wants to see deposits insured up to much higher limits for the next two years instead of the current $250,000 per account.

Treasury Secretary Janet Yellen seems to be amenable to that but only if needed. So in essence, we would have to see the crisis get worse before that happens.

The other problem that has yet to be truly known or priced in is the exposure banks have to loans that may not be performing or that may still go bust. The Federal Reserve announced the other day that banks could borrow against full maturity value of their treasuries and other liquid government securities that were underwater due to low yields, so they wouldn't have to sell them at a loss like Silicon Valley Bank did.

But what can they do about commercial loans or other debt out there that may not be performing? Other than lowering rates or going back to Quantitative Easing (QE) , I don't know if there is much they can do about that in the short run.

Already we've seen Columbia Property Trust, a large office landlord controlled by PIMCO, default on $1.7 billion in loans tied to seven buildings across the country and it seems to me that with tens of thousands of job cuts already announced and many of those that do have jobs working remotely, this problem is not going away.

With the Federal Reserve set to either raise rates again today or possibly keep rates where they are, that doesn't mean their battle to bring down inflation to their 2% target is over, even if it means costing more jobs and a recession.

I don't agree with it and maybe Jerome Powell will soften his tone at today's Q&A after the rate decision, but in many ways the seeds have already been planted and we're already seeing the first dominos to fall in the regional bank space.

BTO will probably always be over-weighted in the regional bank sector along with its stable of large-cap money center banks and that means increased risk and volatility for the time being.

There will come a time to buy BTO, and maybe at a sharp discount, but give it some time as the worst may not be over yet.

For further details see:

Equity CEFs: No Rush On BTO