GUT - Equity CEFs: So DPG Cuts But GUT Won't Have To?

2023-07-31 17:35:53 ET

Summary

- It's been a rough year for utility stocks and utility focused CEFs as interest rates have moved up making their high dividend yields less attractive.

- So despite a bull market in just about everything this year, the SPDR Utility ETF (XLU) is actually down -3.5% YTD and -6.6% over the last year.

- Now utilities can mean a lot more than just generating, storing or transmitting electricity, particularly if you throw in infrastructure stocks like pipelines, natural gas, water, alternative energy, etc.

- But generally, electric utilities make up the bulk of XLU and even utility focused CEFs like the Gabelli Utility Trust (GUT) and the Duff & Phelps Utility & Infrastructure fund (DPG), which I will be using in this article for a valuation comparison.

- As many CEF investors know, GUT trades at the highest market price premium in CEF history, currently at a market price +114% over its NAV. DPG, on the other hand, dropped from a +15% premium to current -12.5% discount after cutting its distribution -40% on June 15. The only problem is that GUT should have been the one to cut.

Distribution cuts in CEFs are probably the most damaging news for a fund's market price even if it's more of a knee-jerk reaction that ultimately helps the fund down the road by better aligning the fund's distribution with its actual income.

Which is why for a CEF's NAV, a distribution cut is probably the best news the fund can receive, even if shareholders don't see it that way. But since a distribution cut takes pressure off the NAV, that makes it more likely that the fund can grow its NAV even after distributions.

And if you can grow your NAV, then it just makes each future distribution that much easier to cover too since the fund's portfolio dividends, interest and appreciation potential can also grow.

On the other hand, if you have too high of an NAV yield, it makes the likelihood of NAV erosion that much more likely and eventually, that will result in a distribution cut.

And here's the situation we find ourselves in with the Gabelli Utility Trust ( GUT ) , $7.03 current market price , and the Duff & Phelps Utility & Infrastructure fund ( DPG ) , $10.01 current market price, resulting in probably the most flagrant valuation difference I have ever seen for two funds that are very alike in so many ways.

How similar? Well, if you go by NAV total return performance, which is the actual portfolio performance of each fund including all distributions, you would be hard pressed to tell them apart.

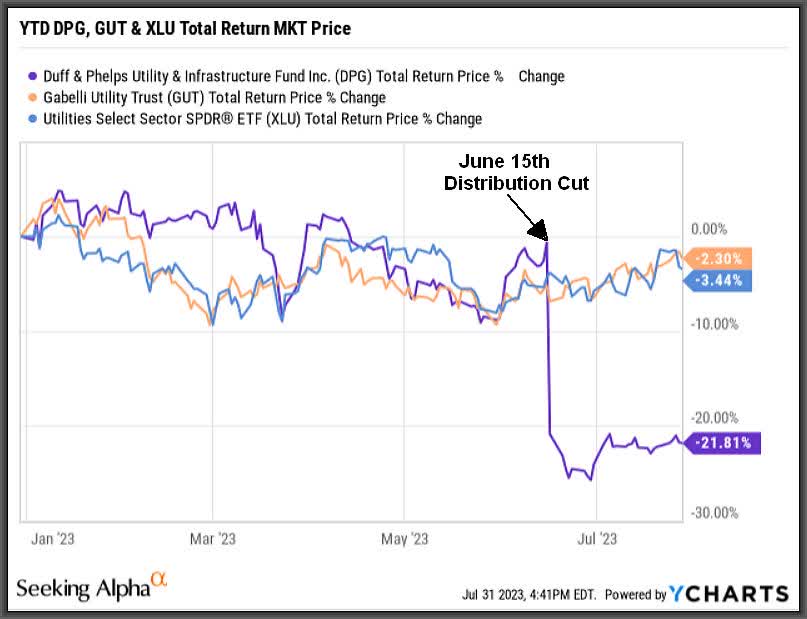

Here's a year-to-date total return NAV of DPG and GUT along with XLU for comparison:

And here's a three-year NAV total return comparison:

As you can see, very similar performances, even with XLU. In fact, both DPG's and GUT's NAVs are actually outperforming XLU over these two time frames.

Now DPG's NAV tends to be a bit more volatile, shown with the sharper up and down spikes in the graphs because it uses a higher leverage percentage than GUT and it also has a more concentrated portfolio with only 41 holdings whereas GUT has more than 200 holdings disbursed over more sectors and even countries.

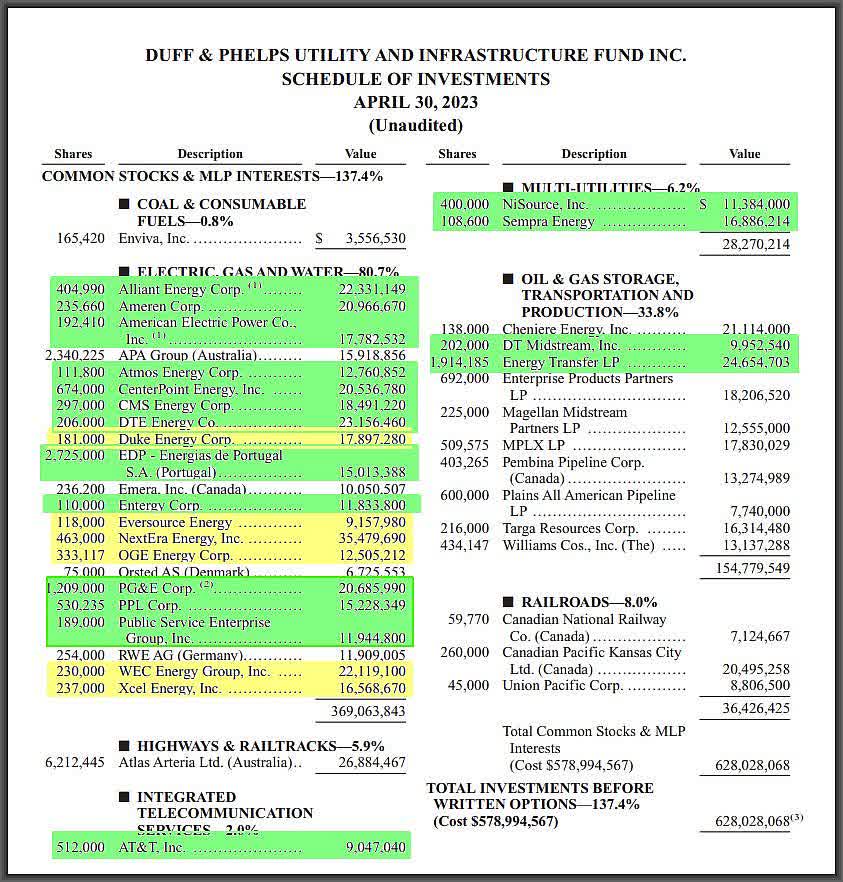

Nevertheless, electric, gas and water utilities are by far the largest sector exposure in both funds and here are the portfolio holdings of DPG showing a color-coded overlap with GUT's holdings as of April 30, 2023:

{kind=link}

Duff & Phelps

Note: Yellow denotes top 10 holdings overlap in both funds while green denotes general portfolio overlap.

Based on the valuations of the current holdings of both funds, I calculate that 88.2% of the value of DPG's holdings are also held by GUT, though those holdings only constitute 34.6% of GUT's total holdings. Still, that's a big overlap and explains why the fund's NAV performances have closely matched each other.

So does it make any sense whatsoever that if the NAV's of these funds will pretty much move together with or without the distribution cut, that the valuations and MKT price performances should be at such polar opposite extremes now?

{kind=link}

Absolutely not. Anyone who thinks that GUT is a safer fund to own than DPG now should realize that after cutting its distribution -40% on June 15th from $0.35/share per quarter to $0.21/share per quarter, DPG now has a dramatically lower 7.3% NAV yield to cover, down from 13% .

What this means is that DPG will have a far easier time to actually grow its NAV back than GUT. And the end result will be far better NAV performance going forward. How do I know this will happen? Because GUT is currently saddled with an 18.3% NAV yield it can't cover, which is causing its NAV to slowly collapse.

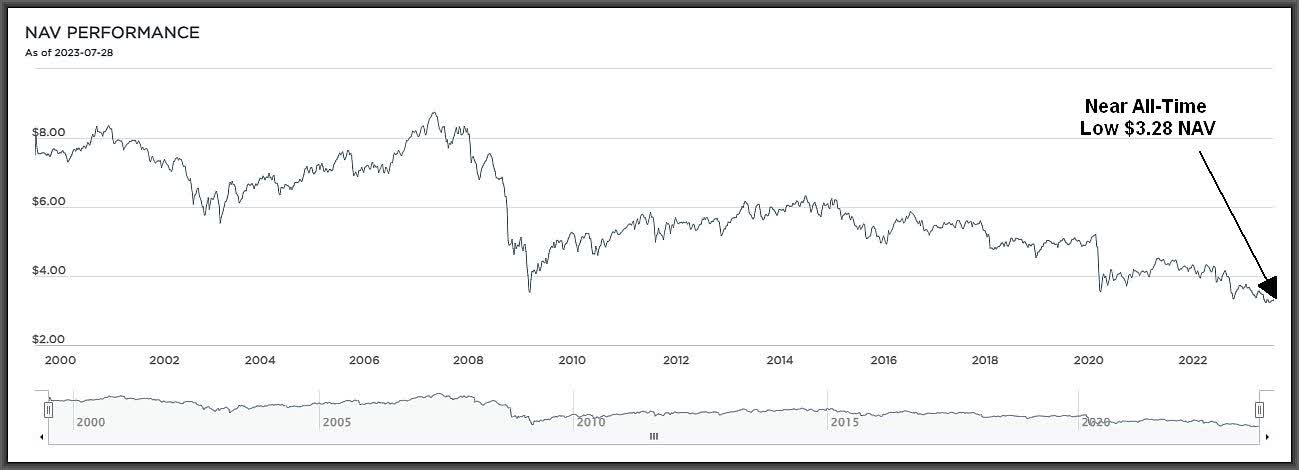

And it's getting worse. In fact, I doubt even if the utility sector turned around today, that GUT will be able to stop its NAV deterioration. Because even with Rights Offerings over the years that GAMCO offered to existing shareholders at significant price premiums to GUT's NAV to try and support the NAV, all you got to do is look at GUT's NAV history over the last 23 years and see that GUT's current NAV of $3.28 is just off an all-time low.

{kind=link}

GAMCO

It really makes you wonder who in their right mind would hold onto a fund, let alone buy a fund, at $7 when its liquidation value is only $3.28 . Because if the utility sector is considered a safe haven sector to invest in, which I guess is why PGP can attain the highest market price premium in CEF history, then why wouldn't you want to own a fund like DPG whose board of directors have already made the hard decision to cut the distribution and with the fund now trading at a -12.5% discount as a result?

Seems a lot safer to me! And with DPG's price drop to $10.00 , even with the distribution cut, DPG's market yield is now NO different than GUT's 8.5% current yield.

I have no skin in the game on GUT, but on a price and valuation basis, there is no way this extreme valuation difference should continue.

And if you think DPG may just be a poorly managed fund (even though Duff & Phelps also manages another utility fu nd ( DNP ) tha t trades at a +20% premium), then here's how both DPG's & GUT's NAVs have performed since the distribution cut on June 15:

So far, so good.

For further details see:

Equity CEFs: So DPG Cuts, But GUT Won't Have To?