BIGZ - Equity CEFs: The Best Return Of Capital Funds For 2023 (And A Look At BIGZ CLM And ETW)

Summary

- It was back in November of 2012, yes, over a decade ago, that I wrote my first article discussing the benefits of high Return of Capital (ROC) in equity CEF distributions.

- Back then, I first wrote (link below) about the risks and tax-differences between high ROC in equity based CEFs vs tax-free distributions in municipal bond CEFs.

- I then went-on (also link below) to offer what I considered to be the best Return of Capital equity CEFs to own, even though many of them are no-longer around.

- Why is this relevant again? First, because over the past year, bonds have been just as risky as stocks, and second, because of the bear market last year, many stock-based CEFs are now showing much higher ROC in their distributions, thus competing more with tax-free or tax-advantaged bond CEFs.

- So I thought that this would be a good time to revisit this subject and identify equity CEFs in a high inflationary environment that can not only offer a high distribution yield, but also allow income investors to keep more of that yield.

2022 was a year to forget for the equity and bond markets so what I have been telling my subscribers of CEFs: Income + Opportunity is that if you have a taxable account, you might as well look to make lemonade out of last year's lemons and what better way to do that than to invest in high Return of Capital - ROC - equity CEFs.

That's because Return of Capital in a CEF's distribution is non-taxable in the year received though IRS rules stipulate that you would need to reduce your cost basis by the ROC amount. In essence then, the income is deferred until you sell the fund. But until then, ROC can be just as tax-advantaged to tax-loathing investors as tax-free interest payments are from municipal bonds.

And since virtually all CEFs lost NAV last year, some significantly, you might as well look for CEFs that can get you 8% to 10% tax-deferred yields, much higher than even municipal bond CEF yields, since not all CEFs can offer high Return of Capital in their distributions even if they lost -20% or more of their NAVs last year.

Below, I will tell you the best Return of Capital equity CEFs to choose from since, depending on their income strategy, not all CEFs are even capable of generating much ROC even in a bear market, due to high dividend and interest income or due to realized gains they still need to work off. And of the CEFs that do typically include ROC in their distributions (mostly option-income funds), there are fund sponsors who actually try to maximize Return of Capital so that shareholders can keep more of what they earn.

But let's first talk about Return of Capital since even after a decade, many investors still consider ROC to be a red flag warning and will avoid funds that include it in their distributions. And for some funds, that is true, since you generally don't want to see Return of Capital in leveraged CEF distributions, but for 2022, that was almost inescapable.

CEFs, ETFs And ROC

CEFs are probably the most misunderstood asset class in the markets and thus can offer unique advantages if you know the differences between CEFs, ETFs and mutual funds. Trust me, the vast majority of investors do not so it's to your advantage if you do.

Most investors would consider CEFs to be nothing more than high-yielding ETFs and are generally clueless about the premium and discount feature that only CEFs offer. But that's not what this article is about since this article is going to highlight another overlooked difference between CEFs and ETFs, and that's the makeup of their distributions and yields.

Most income seeking investors are familiar with ETFs and mutual funds that offer a current yield based on actual dividends and interest generated by the fund. Typically, those accumulated distributions are paid out (quarterly or monthly) and are taxable in that year received. And if the fund is actively managed, it also may include a year-end capital gain distribution too.

But for most CEFs, distribution levels are based on expectations of income and/or gains, and there's often a difference in what is paid out vs. the actual income and realized gains (if any) in any given year. And if there's any shortfall of what is expected, like what happened en masse last year, the balance of the distribution can typically be classified as Return of Capital .

This is a bit oversimplified since accounting rules may limit the amount of ROC that can be taken during the year if there is carryover income or gains but the bottom line is that distributions from CEFs can be broken down into either income (from portfolio dividends and interest) or realized net gains (long or short term) and anything that is not considered income or realized net gains can ultimately be used as Return of Capital .

Note: Net gains equals realized gains minus realized losses over a given year

Now that may sound like Return of Capital really is just returning your principal back to you but it's actually much more complicated than that and I, and others like Eaton Vance , have put out articles and white papers over the years trying to explain why Return of Capital doesn't necessarily have to be a bad thing and can actually be a good thing if non-taxable (or tax-deferred) income is your objective.

In fact, managing a fund to try and maximize ROC by generating losses in all market environments, i.e. during up markets (by closing out options) or during down markets (by taking stock losses), doesn't necessarily mean that the fund has to sacrifice NAV performance to achieve that goal. In fact, during difficult or down-market periods, equity CEFs that use a high option-write strategy, like from Eaton Vance , can generally solidly outperform their benchmarks even while offering high ROC in their distributions.

I first tried to address the Return of Capital conundrum in this article from January of 2011, CEFs & Return Of Capital: Is It As Bad As It Sounds? and if you go to the link, there is also the highlights of a white paper from Eaton Vance explaining how many of their option-income CEFs try to maximize ROC by taking realized losses in both bull and bear markets.

More recently, Eaton Vance put out this document titled Return of Capital Distributions Demystified , explaining how ROC is more of a tax-concept rather than an economic concept.

Nonetheless, to many income investors, ROC is akin to just having your principal handed back to you and is something to be avoided.

But that would be very shortsighted so let's see if we can't turn some of those skeptics around.

The Best Return Of Capital CEFs From 2012

Here are the articles I wrote back in 2012. The first, titled Equity CEFs: The Best Return Of Capital Funds , came out on Nov. 5, 2012, and talked mostly about the yield comparison between municipal bond CEFs and high Return of Capital equity CEFs.

The second article, titled Equity CEFs: The Best Return Of Capital Funds, Part II , was released the next day on Nov. 6, 2012, and identified the high ROC equity CEFs that I recommended.

As it turns out, three of the funds highlighted in the article are no longer around and either matured, like the Nuveen Dow 30 Enhanced Premium and Income fund (DPO) or were merged into other funds, like the Cohen & Steers Global Income Builder (INB) and the Nuveen Equity Advantage Premium fund (JLA).

But two of the funds, the Eaton Vance Tax-Managed Buy/Write Opportunities fund ( ETV ), $13.12 current market price , and the Eaton Vance Tax-Managed Global Diversified Equity Income fund ( EXG ), $7.96 current market price , are still around so let's see take a look at those.

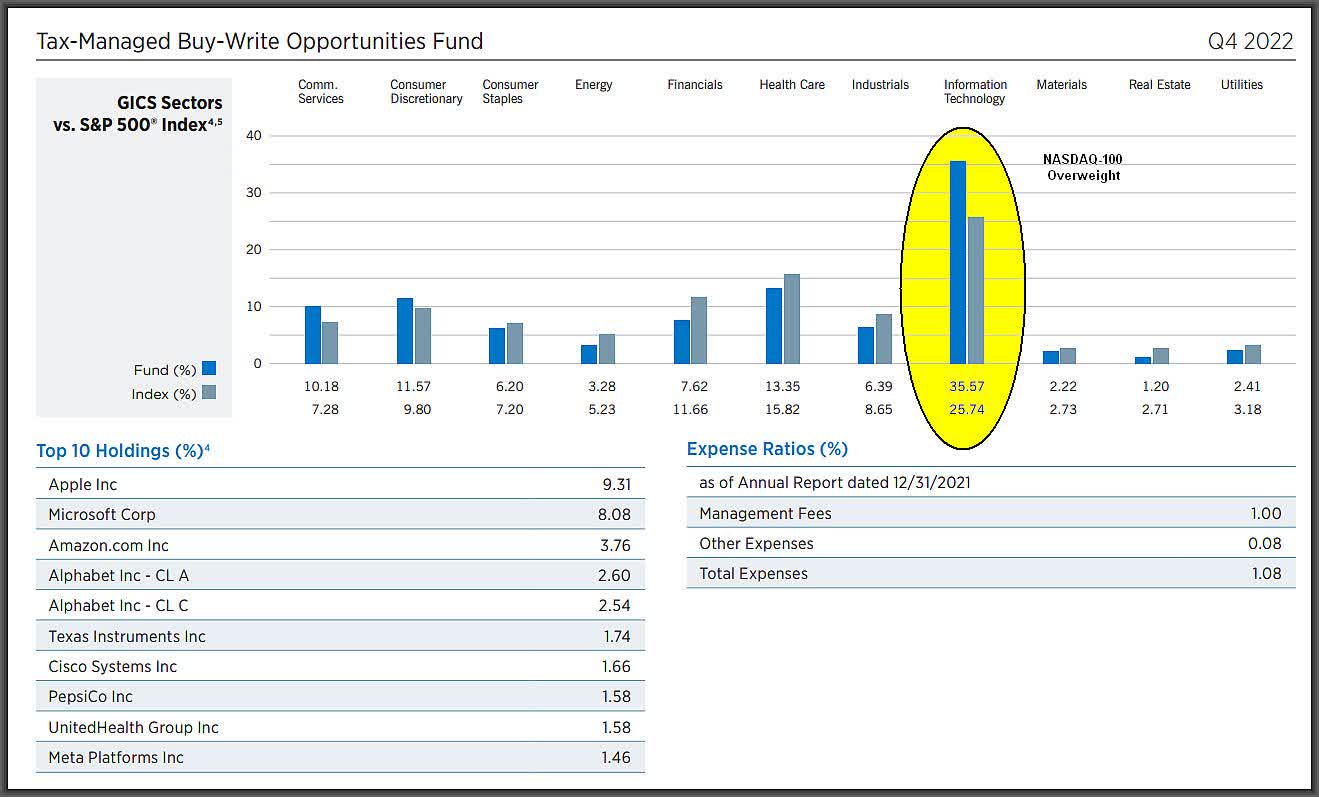

ETV is one of the most popular option-income funds in the CEF universe and sells (writes) S&P 500 and Nasdaq-100 index options against a very high 95% of the notional value of its all-US stock portfolio.

This makes ETV very defensive and last year during the bear market, ETV's NAV was down -16.9% vs. -18.2% for the S&P 500 ( SPY ), $409.83 current market price and -32.5% for the Nasdaq-100 ( QQQ ), $303.59 current market price .

That may not seem like a huge outperformance compared to the S&P 500 but you also have to take into account that the Eaton Vance option-income CEFs tend to overweight the mega-cap technology stocks (see top 10 Holdings as of 12/31/2022 below) so ETV's benchmark would also be the NASDAQ-100, which was down -32.5% last year.

{kind=link}

So if you compare the Total Return NAV performance of the three, which is the true apples-to-apples comparison, ETV stands up very well in what was mostly a bull market period since November of 2012:

This assumes reinvestment of all distributions and dividends for all three funds, which for ETV, was $0.1108/month during virtually the entire 10+ year period before Eaton Vance cut the distributions of pretty much all of their equity CEFs last November.

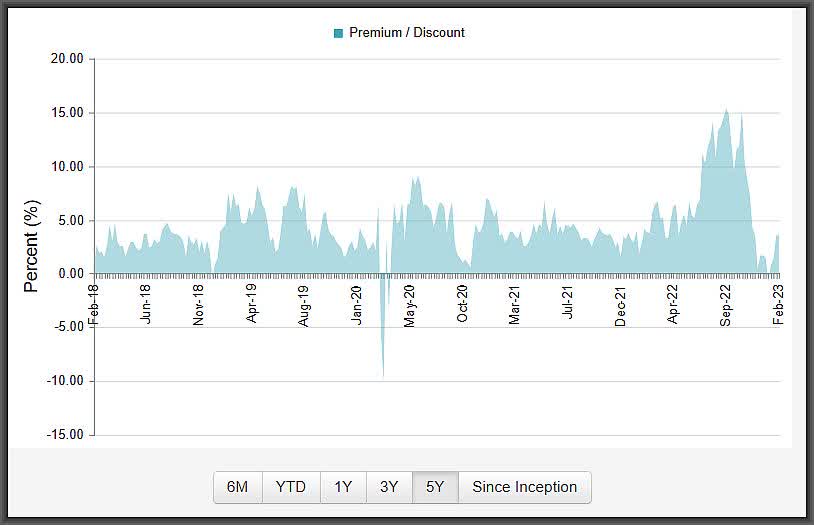

What I'm not going to show is ETV's MKT price total return performance compared to SPY and QQQ since it shows ETV way ahead of SPY, which I'm not sure is correct. But this is one of the problems with trying to calculate DRIP reinvestment performance with CEFs since whether the fund is at a premium or a discount can mean the difference between whether reinvestment will be at the NAV price or MKT price. Most calculations will use the MKT price exclusively but when a fund goes to a premium, often times the NAV should be used.

And ETV has been at a premium a lot over the past five years:

{kind=link}

In any event, one thing is for sure. Any DRIP reinvestment calculation that you can get from a variety of financial websites will not take into account the added benefit of Return of Capital in those calculations, which could mean a significantly higher after-tax return.

As a result, ETV has been one of the most successful option-income CEFs since its inception in June of 2005, especially when you consider that much of ETV's roughly 10% average annualized MKT price yield was tax-deferred if you held onto ETV over the years.

The other equity CEF in the 2012 article, the Eaton Vance Tax-Managed Global Diversified Equity Income fund ( EXG ) is a global stock option-income CEF that also has shown mostly Return of Capital in its distributions over the years too but hasn't had the NAV or MKT price performance compared to an all-US stock portfolio like ETV.

Still, I own a lot of EXG but indirectly, I own even more of ETV since I also own the ultimate Return of Capital fund, the Eaton Vance Tax-Managed Buy/Write Strategy fund ( EXD ), $9.83 current market price , which is merging into ETV.

EXD has been offering almost 100% ROC in its distributions for years (see Estimated Sources Of Distributions below) simply because it started out as a municipal bond CEF in 2010 that also wrote equity index options. That didn't work very well for almost a decade before Eaton Vance changed EXD into an ETV clone in 2019. But it is still working off those losses and as of 12/31/21, the fund still had (-$32,000,000) in realized losses which, for a $92,000,000 total assets fund, is very high.

That will be a nice present for ETV when EXD finally merges into its much larger parent fund sometime in the next few months.

The Best Return Of Capital Equity CEFs For 2023

Return of Capital is going to be found in most of the option-income CEFs, particularly after last year, and no fund sponsor tries to maximize tax-deferred income more than Eaton Vance .

Option-writing CEFs are designed to "s ell future appreciation potential for income today." In other words, they tend to lag in bull markets but hold up better in down markets, thus smoothing out returns by reducing volatility.

The Return of Capital component is really just a bonus for taxable accounts so for those who can use it, an 8% to 10% market yield in a CEF, can suddenly turn into a 12% to 13% tax-equivalent yield, depending on your tax-bracket.

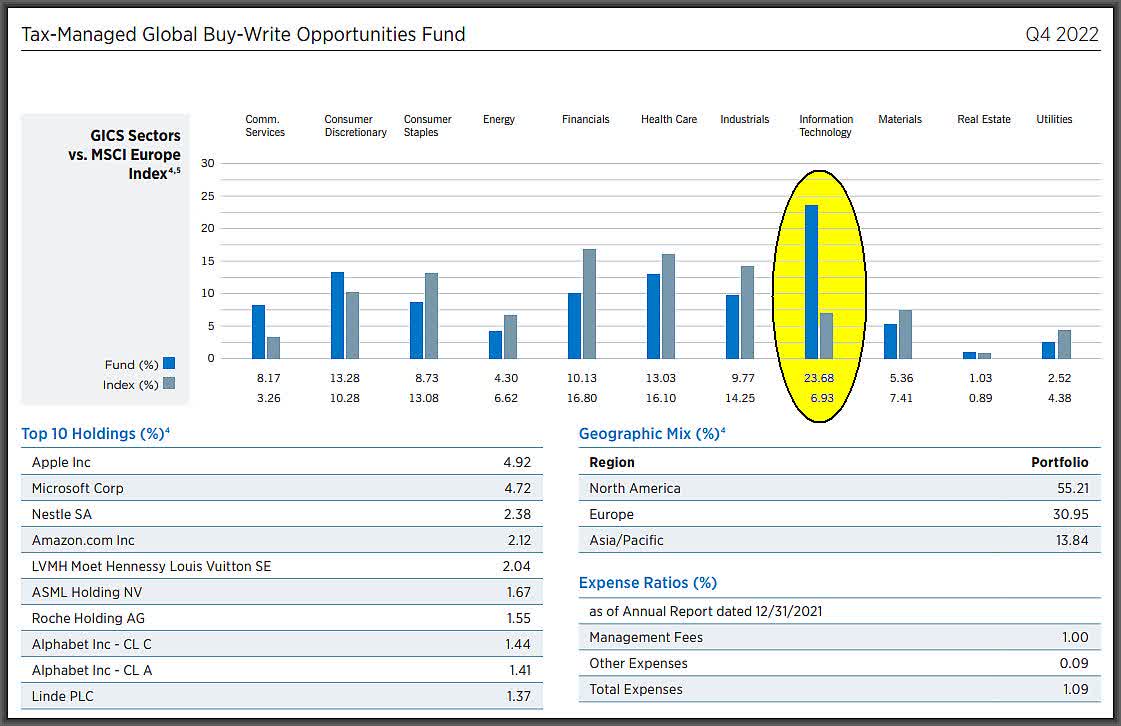

With that in mind, my first pick for the best Return of Capital equity CEF for 2023 is going to be the Eaton Vance Tax-Managed Global Buy/Write Opportunities fund ( ETW ), $8.10 current market price .

ETW has a lot in common with ETV, selling out-of-the-money index options against a very high 95% of the notional value of its portfolio. The difference is that ETW includes a global large cap stock portfolio that is also heavily over-weighted information technology compared to its benchmark indexes:

{kind=link}

Ironically, ETW did not include a high Return of Capital in its distributions last year, only 9% . In fact, ETW's distributions in fiscal year 2022 were mostly long and short-term net capital gains.

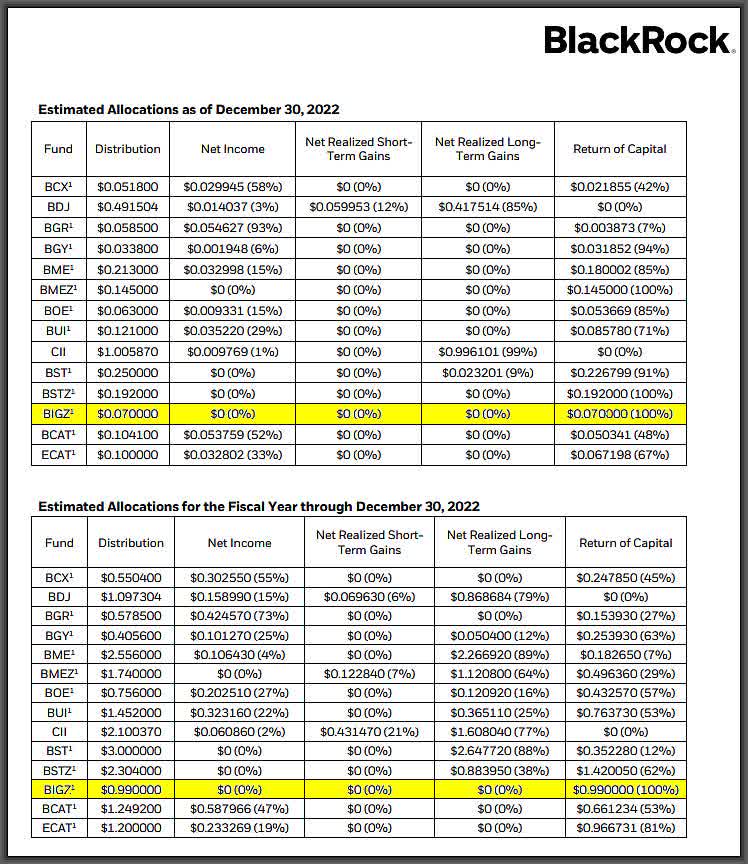

You can see this in the Estimated Sources Of Distributions for December for all of the Eaton Vance equity CEFs, which for most of the funds, was the end of their fiscal year in 2022. Just scroll down to ETW on page 4 below:

But as we enter the new year, the Return of Capital in ETW's January distribution jumped from a total of 9% for all of 2022 to 90% in January and I think that high ROC will continue for the year even though ETW's NAV was down only -15.6% in 2022, also well ahead of the S&P 500 and NASDAQ-100, which ETW writes Call options against as well as a few international indices:

I should point out that virtually all of the Eaton Vance equity CEFs are now showing a high Return of Capital in their distributions based on the January Estimated Sources of Distributions release just the other day, and that is why I pretty much own all of the Eaton Vance equity CEFs across the board.

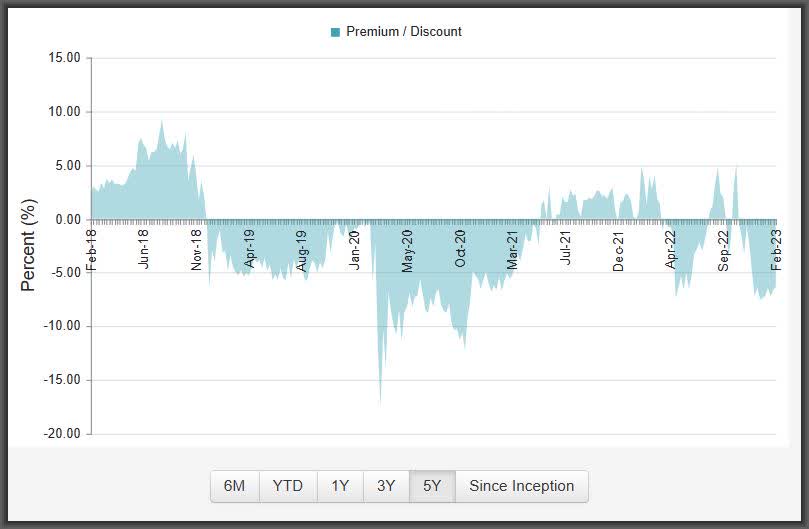

But what attracts me to ETW in particular, is that it now trades at a -6.7% discount, which is towards the low end of its one-year, three-year and five-year valuation range:

{kind=link}

The best market environment for these high % option-write funds will be a flattish market in which no clear up or down trend is established.

But for my next Best Return of Capital equity CEF for 2023, this fund will excel, even as an option-income fund, if small cap technology stocks continue their rebound.

When you think of the BlackRock Innovation & Growth fund ( BIGZ ), $7.56 current market price , you can almost think of Cathie Wood's ARK Innovation ETF ( ARKK ), $42.98 current market price , which lost almost 2/3 of its value, or -67% , in 2022.

But because BIGZ is an option-income fund, its NAV held up much better in 2022, down 'only' -42.1% vs. -67% for ARKK:

Still nothing to write home about since the small to mid-cap innovation and technology stocks that ARKK and BIGZ invested in were probably the worst performing sector in 2022.

So be glad if you didn't own BIGZ last year or when it went public in March of 2021 at $20/share vs. $7.77 today, since you too would have probably been selling BIGZ for the tax-loss last year too.

But as they say in life and investing, timing is everything and I thus made BIGZ my Aggressive CEF Pick for 2023 in early January, not just because I thought technology stocks would see a rebound to begin the year but also because I knew BIGZ's distributions would be 100% Return of Capital for some time to come:

{kind=link}

So let's see, would you rather own Cathie Wood's ARKK fund, which trades at NAV and has NO yield, or would you rather own BIGZ at a breathtaking -20.6% market price discount to NAV (thank you tax-loss sellers), while offering a 10.8% current yield, ALL of which is ROC?

But if you think BIGZ's 10.8% current yield is unrealistic, just remember that BIGZ's -20.6% MKT price discount means that it's a windfall yield to any current buyer since BIGZ only has to cover its much more attainable 8.6% NAV yield.

And because BIGZ uses an individual stock option writing strategy along with a reduced $0.07/share monthly distribution from an inception $0.10/share , that 8.6% NAV yield is extremely achievable.

So let's wrap this up. A current buyer of BIGZ gets a 10.8% market yield paid monthly of which 100% is going to be tax-deferred income for 2023 as long as you hold onto BIGZ. And that doesn't include any appreciation for BIGZ if we continue to see a technology rebound this year.

And though ARKK has jumped way ahead of BIGZ so far this year, mostly due to BIGZ not really owning large cap technology stocks like Tesla ( TSLA ), which is ARKK's largest holding and has jumped +58.5% YTD, BIGZ is still beating ARKK over a 1-year time frame even as its market price discount dropped to -20.6% :

So maybe you should start thinking of BIGZ as more of a tax-deferred, high-yielding, massively discounted and lower-volatility version of an ARK fund. And that sounds like a good risk/reward to me.

Finally, for my last Best Return of Capital fund for 2023, the Cornerstone Strategic Value fund ( CLM ), $8.41 current market price , is an ultra-high yielding equity CEF which is currently offering a 17.5% market yield, virtually all of which is tax-deferred Return of Capital .

Now the Cornerstone funds CLM and the Cornerstone Total Return fund ( CRF ), $8.06 current market price , have always had a high percentage of Return of Capital in their distributions since each year, Cornerstone sets an unrealistically high 21% NAV yield (set at the end of each October for the upcoming year), which the funds generally can't cover (though they did in 2021).

As a result, CLM (and CRF) typically lose NAV each year even during up market years (except for 2021), and that is the definition of destructive Return of Capital . But before you write off CLM and CRF because of destructive Return of Capital , just remember every equity CEF that lost NAV last year, which was virtually every equity and bond CEF, had destructive Return of Capital, and most were a lot worse than the Cornerstone funds.

So destructive ROC was inescapable in 2022, but that's why you look for CEFs now that will be able to offer 90% or more ROC in their distributions for 2023 since as I said earlier, you might as well look for a silver lining.

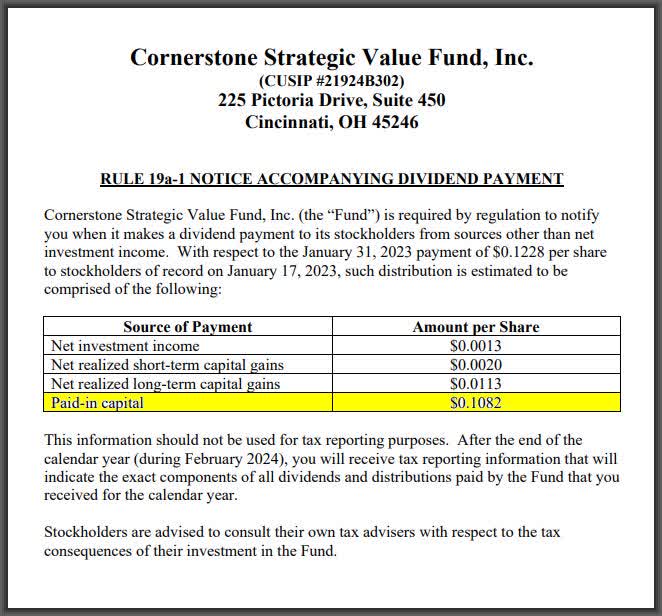

Here's Cornerstone's 19a-1 breakdown of the January distribution for CLM:

{kind=link}

So of CLM's January distribution of 0.1228/share , $0.1082 was Return of Capital (or paid-in capital as described above) or 88% .

This is really just a continuation of the high ROC that was in CLM's (and CRF's) distributions from last year, which were generally around 90% too, but CLM's market price was down a whopping -33.2% last year, much worse than its -15.5% total return NAV performance, which beat the S&P 500.

I didn't start buying CLM until the Rights Offerings for both CLM and CRF were over in June of last year, so my cost basis is lower than the current market price. Thus, I plan on holding onto CLM (and CRF) at least through 2023 since I've had over a half-year of extremely high distributions from both funds that will be mostly ROC. And I foresee that continuing through 2023 at least.

Note: The Cornerstone funds don't use options to help generate income like option-income CEFs do, so they will be more likely to lock in capital gains when opportunities arise. This could affect their ROC percentages in the future but probably not for 2023

The bottom line is that if you're looking for inflation busting income, nothing comes close to the Cornerstone funds as long as their 17.5% current yield distributions are comprised mostly of Return of Capital .

Now, CLM doesn't come cheap at a +20.5% market price premium, but you have to consider the positive offsets, which in years past has pushed CLM up to as high as a 60% market price premium.

The first positive offset are the Rights Offerings that Cornerstone undertakes for both CLM and CRF, usually every year if they can, that actually pads the NAV since the 1-for-3 share offerings to current shareholders are done at a premium to the current NAV.

Last year, that premium was 12% over NAV, which most shareholders are happy to pay if and when the fund's market price is at an even higher premium. What this means is that yes, 21% NAV yields each are going to be difficult to cover each year but the Rights Offerings go a long way to offset that pressure on the NAV.

The second offset, and by far the most important, is that you can reinvest those incredibly high distributions at NAV no matter what the market price premium is.

Think about that for a second. If CLM is at a +20.5% premium but you can reinvest 21% of your total shares each year at the current value of the fund, i.e. at the much lower NAV, how much of that +20.5% premium should be discounted? Quite a bit I would guess.

And finally, plug in that Return of Capital to those distributions for a tax-equivalent yield and you could be looking at something north of + 20% depending on when you bought the fund. And if that ain't an inflation buster, I don't know what is.

Conclusion

Do you own a taxable account? Are you more interested in your after-tax income rather than just the high-yield that many CEFs (equity and bond) offer? If so, then you might as well take advantage of the 2022 bear market and look for funds that can offer a high Return of Capital in their distributions for the foreseeable future.

Because if you think high yielding bond CEFs that lost -25% or more of their NAVs in 2022 are now attractive, just remember, virtually all of their distributions are dividend and interest, which means they are taxable.

And since most bond CEFs don't usually take realized losses in their positions, that's not going to help generate Return of Capital either.

This is a major advantage of equity CEFs over bond CEFs for taxable accounts and yet, most income investors have no clue. In fact, most would probably think that even highly leveraged bond CEFs are somehow safer than most option-income equity CEFs. They aren't and they can't even make their distributions any more tax beneficial to shareholders.

In conclusion for my Best Return of Capital funds for 2023, ETW is the most conservative and defensive, BIGZ offers the most appreciation potential, while CLM offers the highest yields.

All of them, however, should give you very attractive distributions that are around 90% or more tax-deferred for the foreseeable future.

For further details see:

Equity CEFs: The Best Return Of Capital Funds For 2023 (And A Look At BIGZ, CLM And ETW)