SUI - Equity LifeStyle And Sun Communities: Similar But One Is A Buy

2023-07-07 00:52:42 ET

Summary

- Equity LifeStyle Properties and Sun Communities are similar lifestyle-oriented REITs that have generally traded in-line with one another.

- In recent periods, however, the performance gap between the two has diverged more notably.

- While each have their strengths, the overall portfolio metrics and the sector outlook remain largely the same.

- Given the recent disparity in trading multiples, investors may find it best to allocate scarce investment dollars to just one of these two competitors.

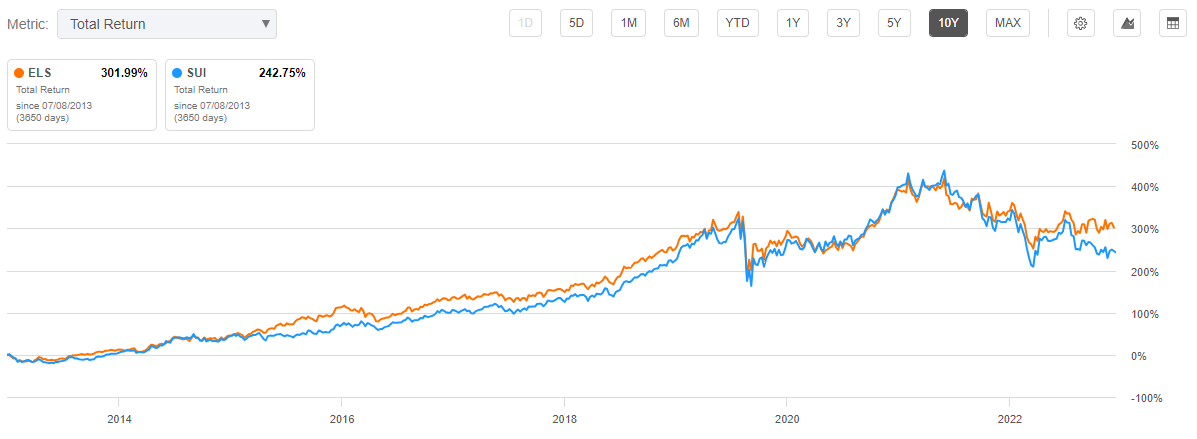

Equity LifeStyle Properties ( ELS ) generally trades in-line with their larger sized peer, Sun Communities ( SUI ). But the performance in total returns has diverged more notably in recent periods.

Seeking Alpha - 10-YR Returns Of ELS Compared To SUI

{kind=link}

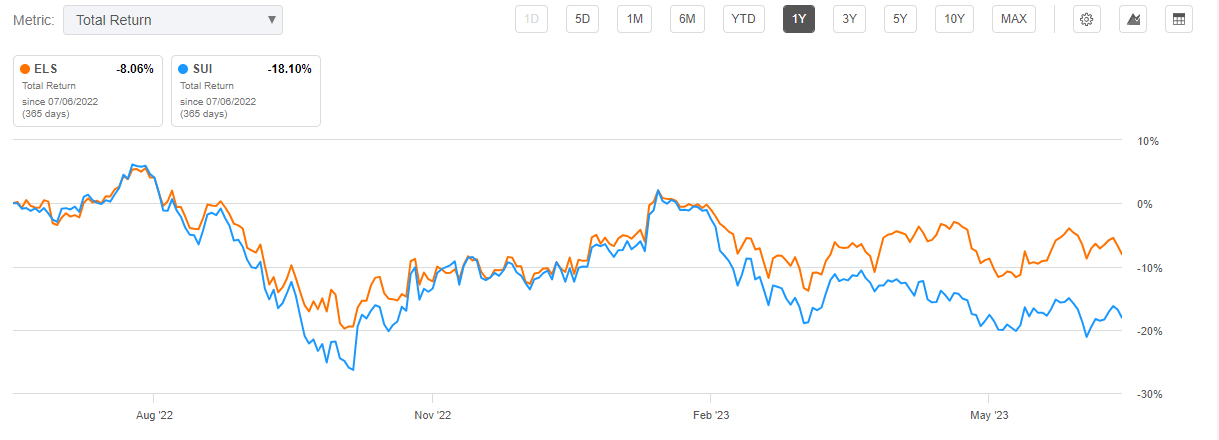

Over the past year, ELS’ losses are less prominent than SUI, who is down nearly 20% during this timeframe. ELS shares are even in the positive on a YTD basis. This compares to a 6% decline by their counterpart.

Seeking Alpha - 1-YR Returns Of ELS Compared To SUI

{kind=link}

The recent outperformance has predictably brought about a wider spread in trading multiples. Before allocating further dollars to ELS, investors may want to consider whether the current premium is justified.

Similar Property Level Performance

ELS and SUI both reported results that came in ahead of expectations. SUI, however, produced stronger growth rates at the property level. ELS grew same-property net operating income (“NOI”) by 5.7% following estimates of 5.0% at the high end of their range. SUI outpaced these results with 6.7% growth and a 230 basis point beat over expectations.

SUI's gains were attributable to strength across their portfolio. For instance, manufactured housing ("MH") NOI grew 5% YOY due to a 6.4% increase in revenues, attributable in part to a 280 increase in MH revenue producing sites. The strength in their MH units was complemented by NOI strength in RVs and their Marinas, which grew 4.4% and 15.1%, respectively.

SUI’s higher NOI growth rate was also in spite of their unfavorable expense burden. Their same-property operating expenses grew 8.2% compared to an increase of 7.4% reported by ELS. The disparity here was largely attributable to real estate taxes, which provided a significant tailwind to ELS in the form of a 1.8% YOY decrease during the period. SUI, on the flip side, incurred a 9.9% increase.

Exposure To Rising Insurance Premiums

ELS did take a larger hit on their annual insurance renewal. While it was known the premiums would be up, given the more challenging market, the ultimate increase was surprising. For the year, their premium increased 58% or $0.01/share above what had been anticipated.

This, then, negatively trickled into their full year expectations for same-property NOI. At the midpoint, growth is expected at 5.1% compared to their previously stated 5.5%. On a more positive note, the expectation for funds from operations (“FFO”) was maintained at a midpoint of $2.84/share.

SUI had previously guided for a +$18M increase in property-related insurance costs. But there were discussions of a potential opportunity to readjust their exposure in the current year. While not yet baked into SUI’s full year guidance, I expect SUI to be better positioned than ELS on this line item.

Both companies have significant exposure to Florida, which is a net positive in many respects. But one fact of life of doing business in the state is the tropical storms and hurricanes. Operations were impacted last year by Hurricane Ian for both. And insurance premiums adjusted accordingly. For ELS, the risks will likely remain greater due to their more concentrated exposure.

Impact On Transient Business And Opportunities Elsewhere

ELS also has a large footprint in California, which is another state that is disproportionately affected by negative weather trends. A stormy start to the year placed a strain on ELS’ full year guidance for their transient business. In Q1, same-property transient revenues were down 14.9% due to lower occupancy levels as a result of fewer sites available for their transient stays.

Same-property transient revenues were also down for SUI, but to a lesser extent of 3.2%. SUI also is benefitting from a healthy conversion rate of their transient stays into annual signings. The conversions are important since they increase the stability of reoccurring cash flows. It also results in a significant markup in revenue per site following conversion. Looking ahead, SUI has about 15K sites in North America as candidates for conversion. This figures to be a significant driver of internal growth.

For ELS, their opportunity lies in expanding their Thousand Trails Camping (“TTC”) membership, their annual subscription program. Since 2017, their member count has grown by over 20%. And in Q1, the company sold about 4,500 camping passes and initiated 5,700 RV dealer activations. Continued growth can reduce the volatility associated with their transient sites and can provide a continuing stream of enduring cash flows. For example, an average of 27% of their members have been with the program for 20 years, according to their company presentation .

May 2023 ELS Investor Presentation - Snapshot Of Growth Rate In ELS' Annual Subscription Program

Is ELS Stock A Better Buy Than SUI Stock?

For prospective investors, choosing between ELS or SUI could easily be seen as a tossup. Both operate in the lifestyle business in overlapping footprints, particularly in Florida. And the industry outlook remains favorable.

According to SUI’s most recent investor presentation , there are just 1.7M RV campsites in the U.S. against 11.2M households that own a RV. This is a supply makeup that is unlikely to change anytime soon, given the logistical and regulatory challenges in developing new stock. Persistent demand for affordable vacationing through all stages of the business cycle also create a moat around the business model.

In addition to favorable industry fundamentals, the two companies also tout similar portfolio metrics, with occupancy levels in the mid-90% range and similar growth rates in NOI. SUI has turned out stronger same-property results in recent periods, despite greater operating expenses. In addition, SUI is less exposed to property casualty losses and associated premium risk due to their greater geographic diversification.

For income investors, ELS provides a more attractive case for dividend growth. At present, they’re growing their dividend at a five-year compound rate nearly double that of SUI. With a yield of less than 3%, however, this may not mean much in the current rate environment. But over time, continued growth can contribute to significant total returns for long-term investors.

Investors in ELS thus far have benefitted from outperformance. But current spreads in respective trading multiples indicates SUI is due for a catch up. Currently, ELS commands a forward multiple of 23.4x. This compares to SUI’s 18.0x. One can point to stronger expected FFO growth as one justification for the premium.

In 2023, ELS is expecting 4.1% growth in FFO at the midpoint. SUI, on the other hand, is projecting a decline of $0.03/share. This is offset, however, by strength at the property level. Guidance here was revised slightly upwards to growth of 5.5% at the midpoint compared to 5.4% previously. For their part, ELS reduced guidance by 40 basis points to growth of 5.1%.

Taken together, SUI is performing stronger at the property level, while ELS has the edge in overall expenses. Given the similarities elsewhere, I don’t believe this warrants a five-turn spread in trading multiples. Prior to 2020, SUI traded at about a three-turn discount to ELS.

For investors looking to deploy scarce capital dollars into this REIT subsector, I believe SUI presents the better upside opportunity. ELS has its strengths and faces a positive outlook, but I believe a pause is warranted, given their current share price outperformance despite largely similar operating performance to their counterpart.

For further details see:

Equity LifeStyle And Sun Communities: Similar, But One Is A Buy