ELS - Equity LifeStyle: Favorable Demographics And A Premium Multiple Leave Shares Fairly Valued

2024-01-01 02:03:57 ET

Summary

- Equity LifeStyle Properties has outperformed many real estate stocks, with its unique business model and asset mix.

- The company's manufactured home unit has seen strong rental growth and high occupancy rates, driven by favorable demographic tailwinds.

- Equity LifeStyle has a strong balance sheet and is positioned for future growth with planned unit expansions and manageable debt maturities.

- Shares do reflect much of these positives, and at 23.5x forward FFO, I view ELS as fairly valued.

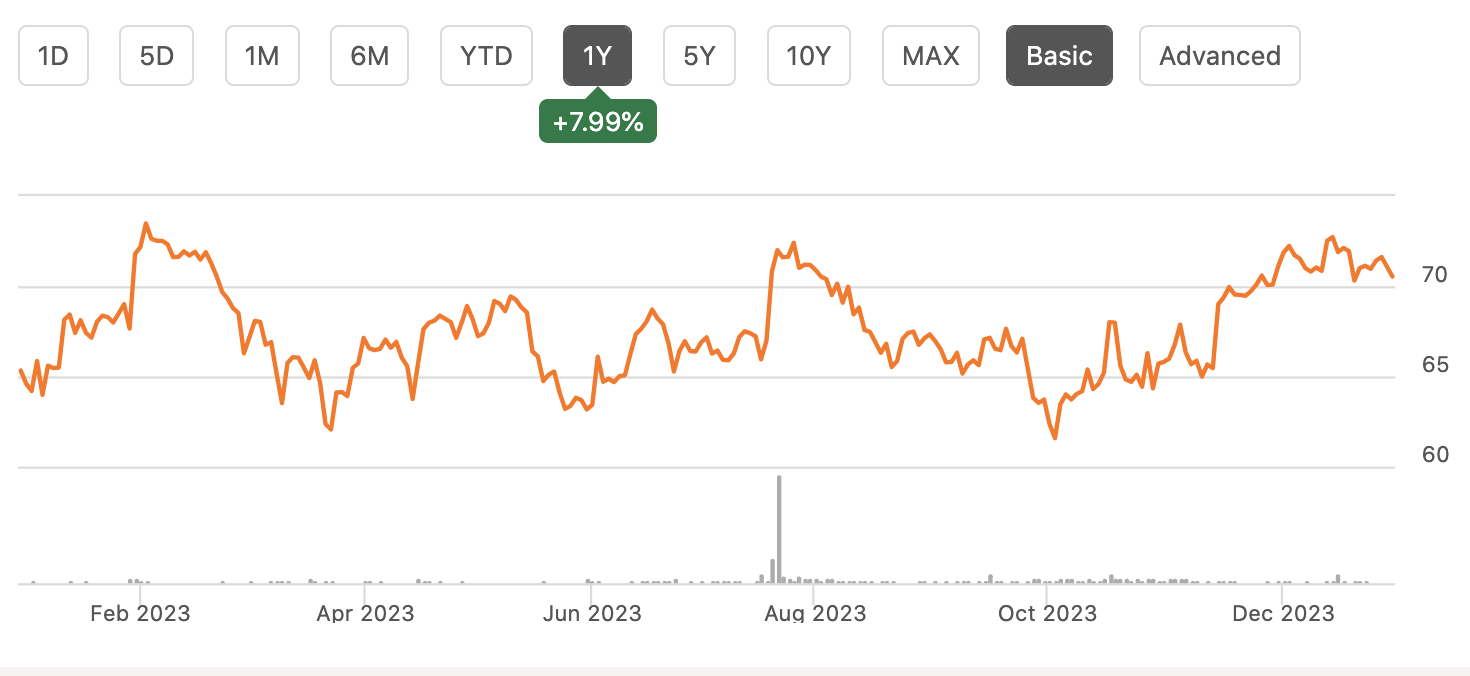

Shares of Equity LifeStyle Properties ( ELS ) have lagged the broader market this year, gaining just 8%, but they have outperformed many real estate stocks with most apartment REITs, for instance, posting losses. With its unique business model and asset mix, ELS has significantly outperformed the national rent slowdown in 2023. While shares are relatively expensive, I view them as attractive given likely rental growth in 2024 and the scope for margin expansion.

{kind=link}

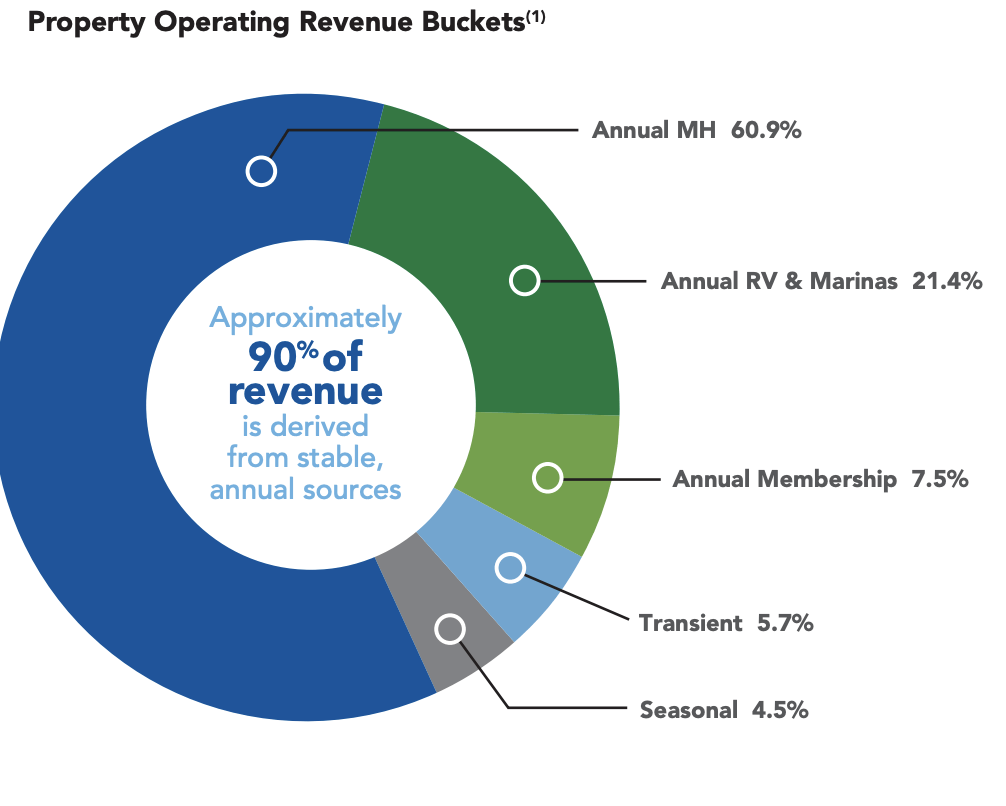

Equity LifeStyle owns 450 properties of manufactured home ((MH)) communities, RV resorts, campgrounds, and marinas. While the company operates in 35 states, 34% of its locations are in Florida, 11% in California, and 10% in Arizona. It has 75,000 MH sites while its 225 RV resorts have 90,000 sites with 35,000 annual leases, the remainder are seasonal, transient or membership. Equity's 23 marinas have 6,900 boat slips. From a revenue perspective, its MH unit is the primary driver, and annual leases account for about 90% of its business with just 10% seasonal/transient.

{kind=link}

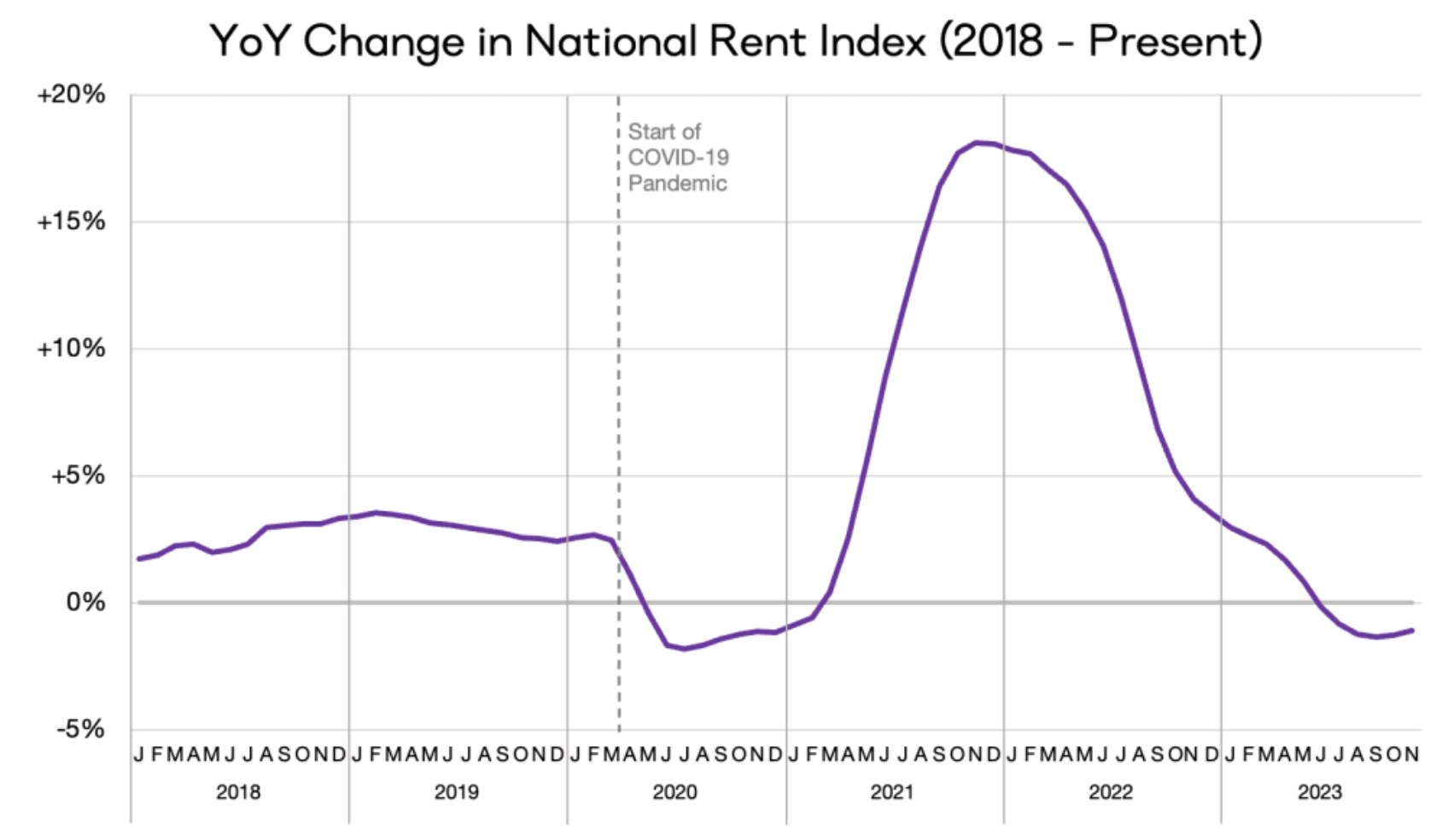

This helps to provide strong revenue visibility. Now, 2023 has been a difficult year for many landlords. After extraordinary rental inflation in 2021 and 2022, rents have not only normalized, but according to Apartment List , rents are declining year over year. We have seen household formations normalize, and there has been a surge in apartment supply, helping to meet the increased demand post-COVID. Rents remain high on an absolute level, but the rate of change has decelerated markedly.

{kind=link}

Equity LifeStyle has been able to largely buck this trend. In fact, MH rental growth was still running at 6.9% in October, with a 94.9% occupancy as of 10/31. Manufactured homes have not seen the surge of construction like apartments have, which has helped to insulate them to supply pressures. Manufactured homes are also relatively inexpensive, making them an attractive "trade-down" play, particularly for elderly customers. The average manufactured home costs about $127,000, and the majority buy with cash, reducing interest rate sensitivity.

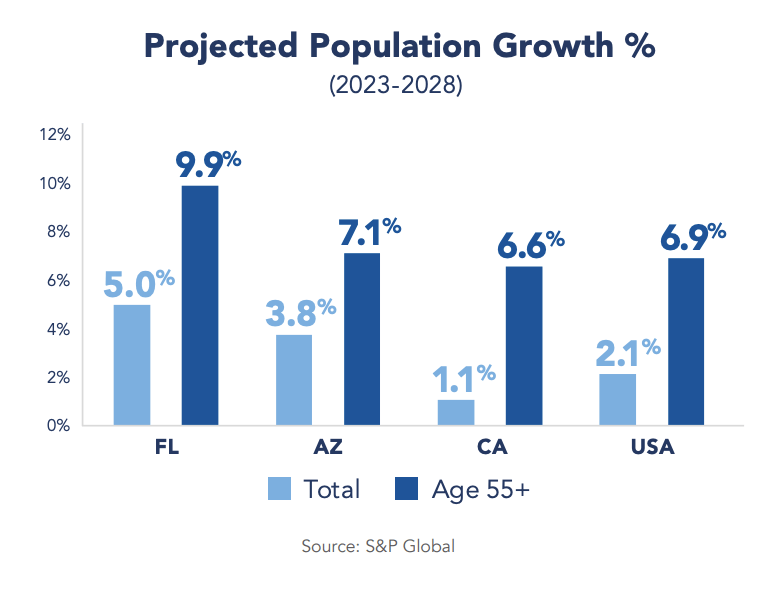

Equity LifeStyle owns the land on which the manufactured home sits, and the owner will pay rent for the land parcel. Aside from its relatively low cost, ELS has very favorable demographic tailwinds. 70% of its communities are either officially 55+ or have 55+ year-old average residents. In its key states, this population is growing strongly, creating ongoing demand in a tightly-supplied niche market.

{kind=link}

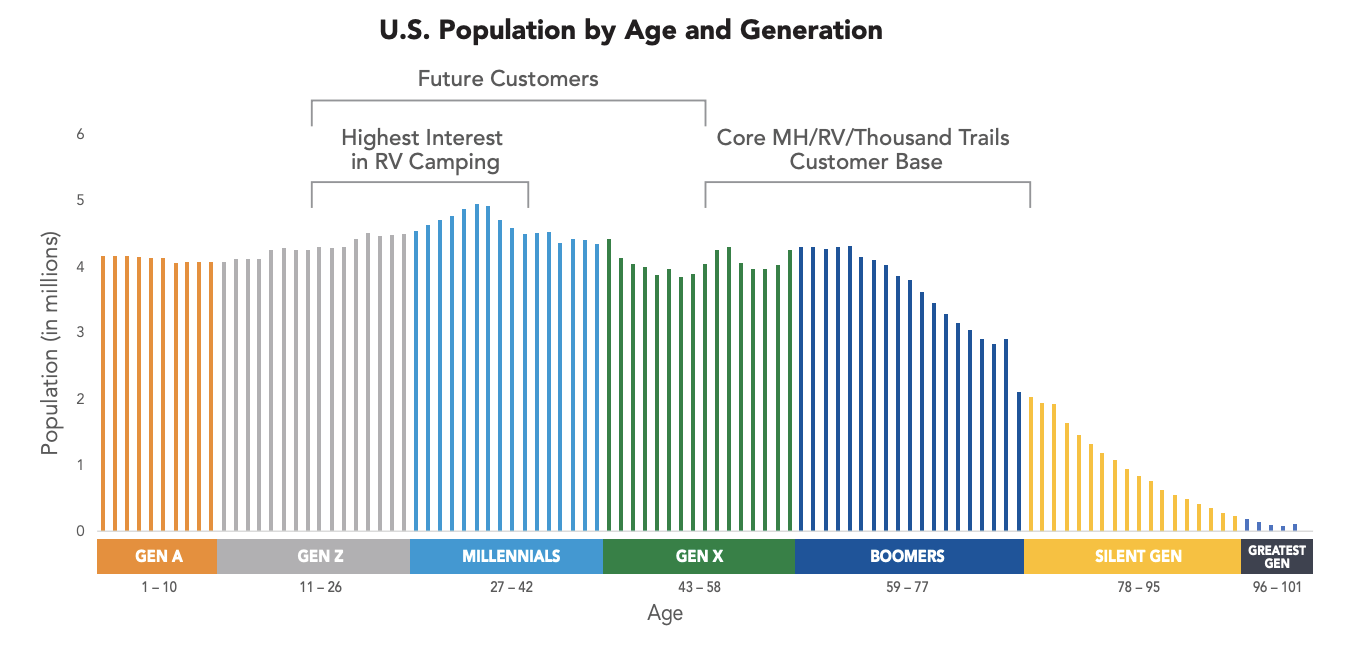

It is well known that the country is aging and that boomers are increasingly retiring. As you can see below, the larger boomer cohorts are just now entering their late 50s. As these Americans continue to retire, the pool of people who tend to like ELS's product will continue to rise, which should provide ample demand to support rent growth.

{kind=link}

Additionally, the millennial generation is our largest, and these are in their prime RV/camping years. Interestingly, RV and marina rent is 3.6% above last year. While this is positive, annual base rents are up a stronger 8.6%. In other words, we are seeing a downtick in the smaller seasonal/transient segments. In 2021-2022, we saw a surge in travel, with RV sales also surging as people began moving on from COVID restrictions. With this activity now returning to more normalized levels, we are seeing a downturn in seasonal activity. While this has slowed growth, the fact RV/marina rents are still rising is a testament to the fact that annual leases are the core of Equity's business.

These strengths are evident in the company's financial results. In the company's third quarter , normalized funds from operations ((FFO)) were $0.71 per share, up 2% from last year. Core revenues rose by 5% to $336 million. While the strong rental growth is driving top-line gains, the bottom-line conversion has been somewhat soft. This is because property operating expenses rose by 5.1% with utilities and payroll up 1.2%. They account for nearly half of the expenses. Repair and maintenance were up 8%, due to higher storm clean-up costs. Insurance expenses rose by 10% while property taxes rose by 12%. Higher insurance costs have plagued the real estate sector, and they are likely to remain elevated. As home price appreciation has slowed, we should see property taxes decelerate next year, helping the company to retake margin.

I have been particularly encouraged to see that rental income is running faster in Q4 than in full-year 2023, according to the latest guidance, which speaks to the fact that rental activity remains strong. Revenue tailwinds are not yet fading.

{kind=link}

Even more than Q4 2023, I am encouraged by preliminary 2024 actions, which are most relevant to future share price movements. The company sent rent increases in October to half of its MH residents, with an average increase of 5.4%. RV annual rates are up 7% on 95% of its sites. This is somewhat slower than 2023's pace, but it remains quite high, significantly outpacing apartment rents and overall inflation. With wage costs muted and property taxes likely to slow, we should see net operating income rise in keeping with revenue.

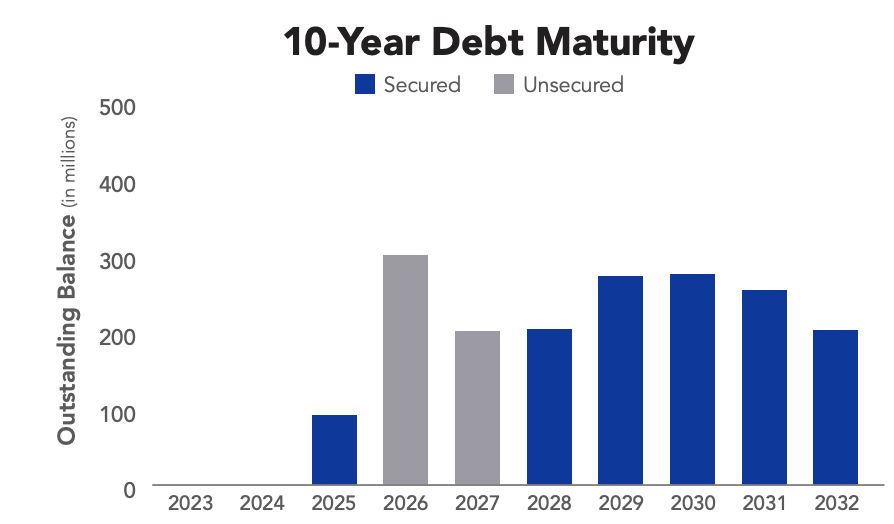

Beyond these favorable business dynamics, Equity LifeStyle has a strong balance sheet. It carries 5.3x leverage, and its debt load is well-structured. 89% of debt is due after 2026 with no 2024 maturities, allowing it to ride through this period of elevated rates. Interest expense of $33.4 million in Q3 was up from $29.8 million, but we should not see material further increases until 2025, at the earliest. Overall, ELS's debt has a 3.7% average rate with a 9-year average maturity, with manageable maturities across the next decade.

{kind=link}

ELS is moderately expanding its unit count with 1,000 expansion sites planned in each of the next two years, modelled at an 8-10% stabilized yield. The company has $90 million in recurring capex needs and about $140 million in discretionary capex. ELS has a 1.6x dividend coverage ratio, leaving it with about $200 million of retained cash flow, meaning it can essentially self-fund all of its capex needs, rather than rely on debt markets.

Shares have a 2.5% dividend yield and a 4% FFO yield. Historically, the company has grown its dividends more quickly than FFO as it has worked down its high coverage ratio. I view 1.5-1.7x coverage as a strong level to ensure sustainable dividends and flexibility to engage in growth capex. As such, I would expect dividend growth to more closely track FFO growth going forward to keep coverage near current levels.

{kind=link}

Equity LifeStyle has managed through this rental market downturn incredibly well, thanks to its niche market and favorable demographic tailwinds. Now, shares trade at a premium valuation as a result. I am looking for the company to generate about $2.95-$3.05 in 2024 FFO, giving it a 23.5x forward multiple. For comparison, Mid-America Apartment ( MAA ) trades at less than 15x.

The tailwinds that have boosted results in 2023 are likely to continue in 2024, as evidenced by announced rent increases. Beyond 2024, the aging population and high cost of traditional housing are likely to be tailwinds for the company's results for several years. In other words, ELS trades at a premium, but that premium is justified. With about 1% annual unit growth, and 4-5% rent growth given these factors, ELS is positioned for 5-7% FFO growth, or slightly higher if it can recapture some lost 2023 operating margins. With a starting yield of 2.5% and dividend growth in that 5-7% range, ELS can provide ~8% returns for investors.

I view this as broadly fair value, making shares a hold. Investors can collect a secure and solidly growing dividend. However, with its premium nature already in its multiple, ELS is unlikely to generate a 15+% return for investors over the next year, absent a further drop in interest rates. There is also no pressing need to sell, given this return potential, particularly if an investor has a large unrealized gain. If we saw a 5-10% pullback, I would begin adding to a position, but at ~$70, I view shares as a solid hold.

For further details see:

Equity LifeStyle: Favorable Demographics And A Premium Multiple Leave Shares Fairly Valued