UMH - Equity LifeStyle Properties: A Recession-Resistant Dividend Growth Rockstar

Summary

- ELS is the premier mobile home & RV park REIT on the public market.

- ELS's primarily older/retiree tenant base give it extraordinary recession-resilience, as retiree income largely comes from the secure source of Social Security.

- The REIT has an excellent dividend growth track record that looks poised to continue for the foreseeable future.

- I compare ELS to its two primary mobile home REIT peers to show why ELS is the cream of the crop.

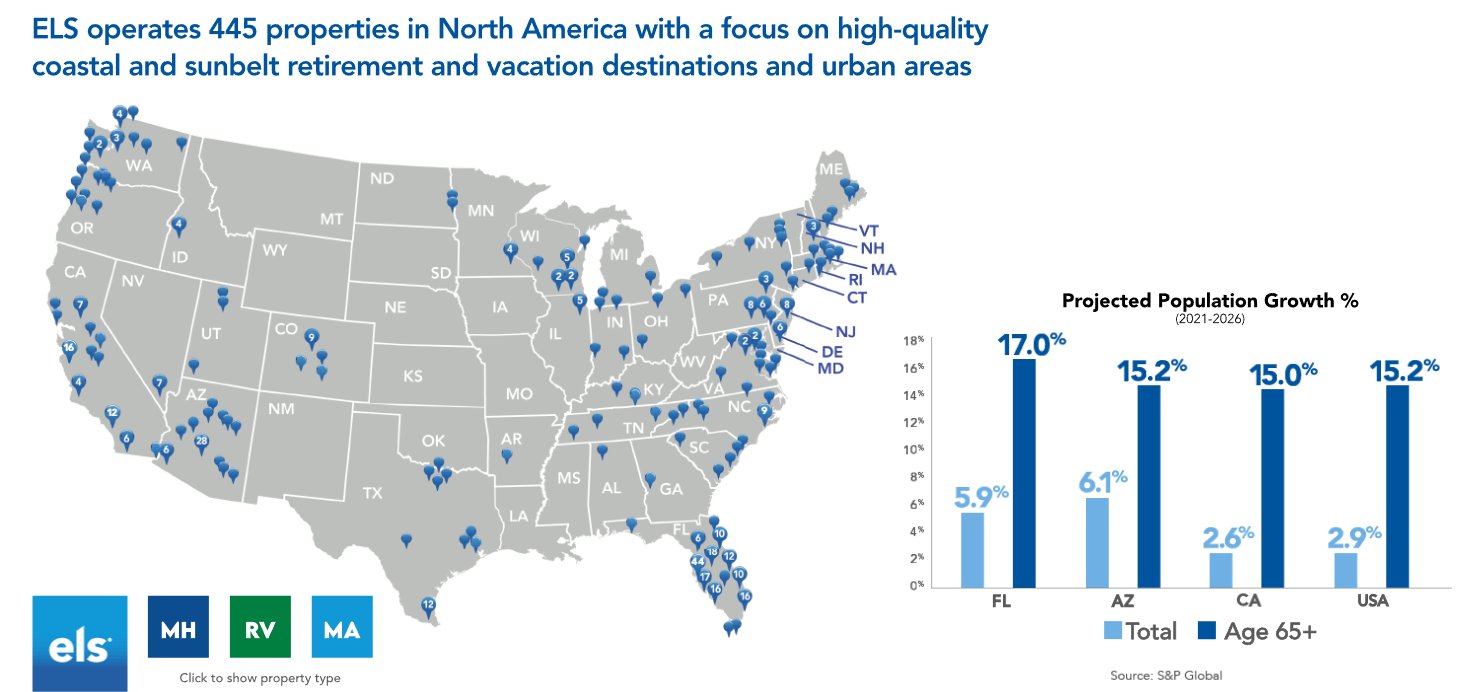

Equity LifeStyle Properties ( ELS ) is a real estate investment trust ("REIT") that owns and operates a portfolio of 445 properties including mobile home communities, RV parks, and marinas across the United States. Despite the inclusion of RV parks and marinas, it's important to note that 89% of ELS's revenue derives from annual leases or contracts.

For the sake of this article, I will compare ELS to its two closest REIT peers in the manufactured home space:

ELS is not quite as large as SUI with its $12.7 billion market cap. Compared to SUI's $16.2 billion in undepreciated real estate assets, ELS has a mere $7.3 billion in undepreciated real estate assets.

Overview of Equity LifeStyle

ELS owns a high-quality portfolio of mostly mobile home and RV properties across the US, with a small allocation to marinas that are overwhelmingly located on the coast of Florida.

{kind=link}

Rather than targeting mobile home communities broadly, ELS mainly focuses on communities in popular retirement destinations that are either age-restricted to 55+ or are mostly occupied by older people. This has its pros and its cons.

On the one hand, resident turnover is very low, and the vast majority of leases/contracts are annual or longer, making cash flows very stable. Moreover, the population of older Americans is growing faster than the overall population, as around 10,000 baby boomers will turn 65 every day through 2030.

On the other hand, rent rates typically don't rise much faster than cost of living adjustments for Social Security and other pension benefits. Thus, in years like 2021 and 2022 when most residential rents are soaring by double-digit percentages, ELS's mid-single-digit rent growth looks piddly in comparison.

Then again, in the 20 years from 2001 to 2021, ELS's average NOI growth nearly doubled the CPI during that time. So, in more "normal" times, ELS's portfolio actually beats inflation.

For the most part, ELS owns the land while the tenants own the improvements or assets sitting on the land, including mobile homes, RVs, or boats (in the case of marina slips). Most of these properties are located in relatively close proximity to some body of water, whether it be a river, lake, or the ocean.

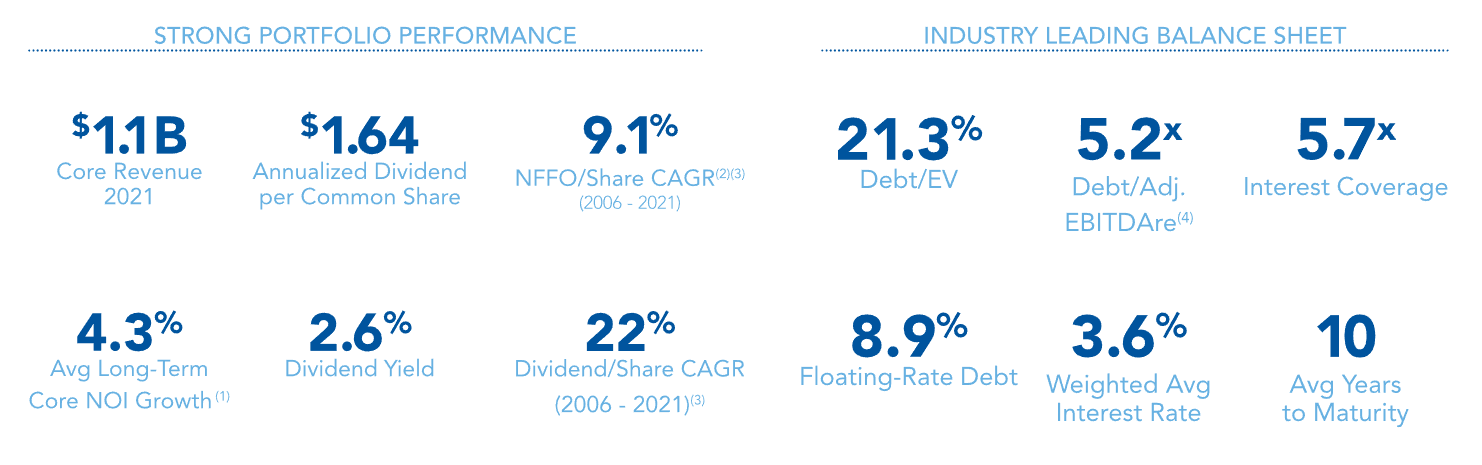

One of the strongest aspects of ELS is the company's balance sheet and financial management (more on the latter below). ELS enjoys an investment grade balance sheet with relatively low debt, little floating-rate exposure, and a long average maturity.

{kind=link}

Less than 10% of debt is maturing over the next three years, and only 18% of debt matures through 2026, far lower than the REIT industry average of 43%.

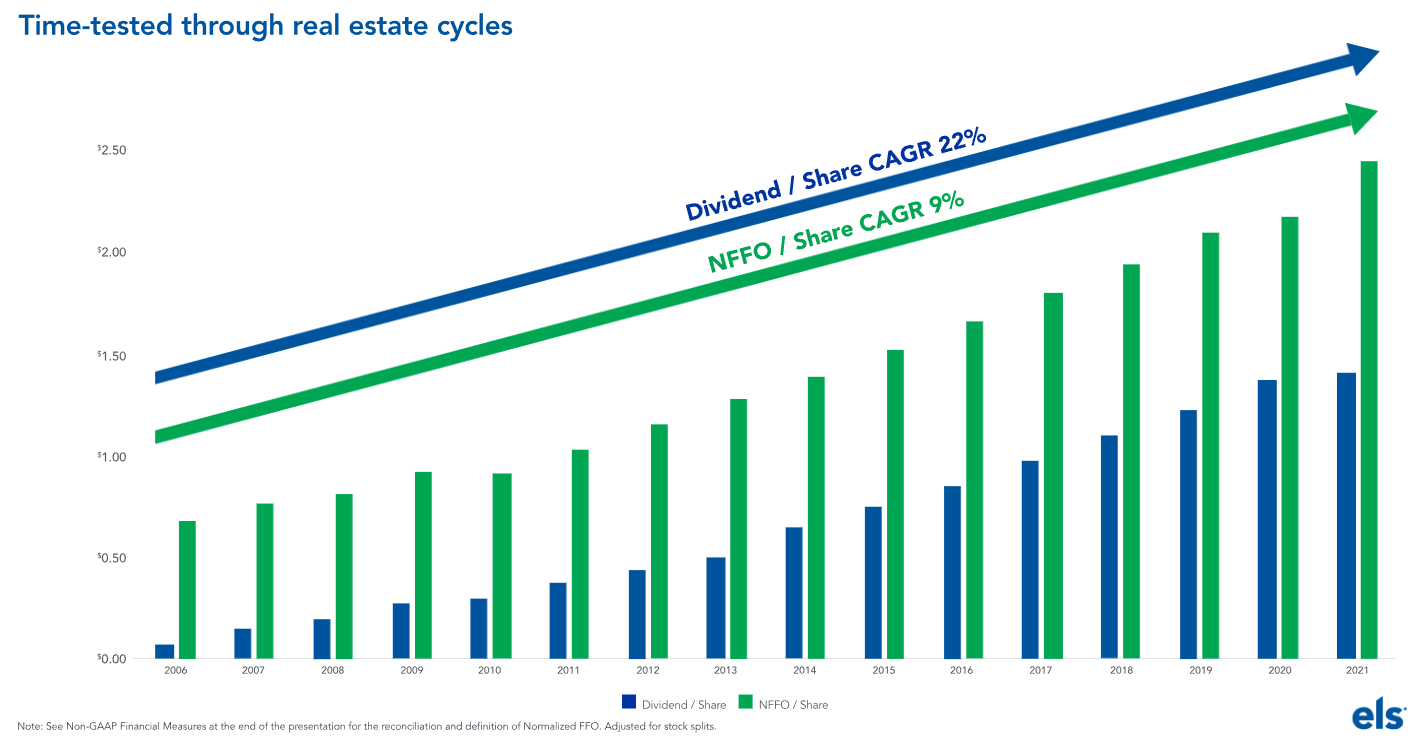

Notice also in the above image that ELS has grown its dividend at a compound annual growth rate of 22% in the 15 years from 2006 to 2021. That is a phenomenal growth rate, but it should be noted that much of this came from an expanding payout ratio, as normalized FFO per share growth only averaged 9% during that time.

{kind=link}

Dividend growth averaged "only" 11% over the past five years, and as the payout ratio slowly rises, that growth will eventually have to slow to the same level of growth as FFO per share.

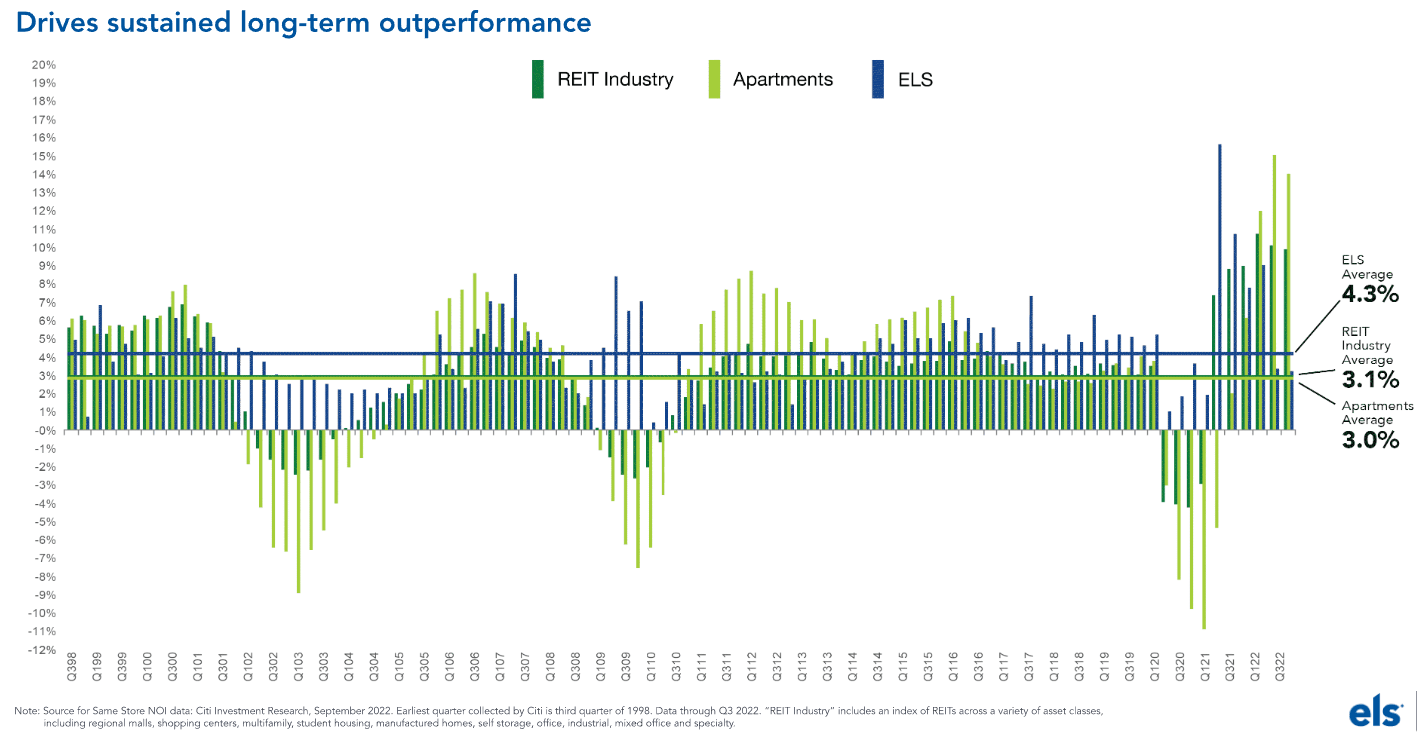

One of the most attractive aspects of ELS is its resilience in the face of recessions. Look closely at the chart below, which shows ELS's same-property NOI growth compared to apartments and the REIT industry more broadly quarter by quarter.

ELS's same-property NOI growth simply does not turn negative during recessions. It slows down but does not decline.

{kind=link}

That is largely a result of the age restriction aspect of the portfolio. Since many of ELS's residents are retirees, their income mostly comes from Social Security, which does not falter during recessions. ELS is basically collecting rent checks from Uncle Sam through the intermediary of their retiree tenants.

Another aspect of ELS that I like is the long-tenured and seasoned management team. The CEO, CFO, and COO have worked at ELS for an average of 29 years (each having been there either 28 or 29 years).

Comparison To Peers

I want to make the case that ELS is the best-in-class mobile home REIT. Actually, one other peer has performed slightly better than ELS on a total return basis, as we'll get to below, but ELS has the best financial management of the three.

First, notice the extreme (and I mean extreme ) disparity in the level of equity dilution over the past decade between ELS and its two mobile home peers:

ELS's portfolio has expanded during that time, as have its profits. But this expansion was funded mostly through other means than equity issuance - namely, capital recycling, judicious use of debt, retained cash, and low-cost in-house development.

That said, SUI's portfolio has expanded far faster than ELS's, funded largely through equity issuance.

Since 2010, SUI has grown its portfolio size by around 5x.

(To be fair, SUI does not make much more use of debt than ELS in order to engage in this portfolio expansion. Compared to ELS's Q3 net debt to EBITDA multiple of 5.2x, SUI's net leverage ratio sits at 5.7x.)

Portfolio expansion is all well and good as long as it is accretive to the bottom line on a per-share basis. But as ELS demonstrates, it is possible to grow one's portfolio of assets at a much slower rate while also matching or exceeding a peer's FFO per share growth.

From 2011 to 2021, SUI's core FFO per share increased 108% from $3.13 to $6.51.

Meanwhile, during that same period from 2011 to 2021, ELS's normalized FFO per share (not exactly apples to apples with core FFO but directionally accurate) increased around 150% from around $1 to $2.53.

What about total returns?

ELS is in the "Equity"-branded family of real estate investment companies founded by Sam Zell. For the most part, Zell's real estate investments have performed extraordinarily well, and ELS is no exception.

That said, SUI's total returns have been slightly better than those of ELS over the past decade, with both REITs lapping their much smaller rival UMH.

But where ELS really shines, especially for dividend growth investors like me, is in the pace of dividend increases the REIT has given shareholders. ELS's dividend growth over the past decade completely obliterates its peers:

This dividend growth needs to be kept in mind when comparing the dividend yields of each mobile home REIT:

- ELS: 2.56%

- SUI: 2.49%

- UMH: 5.01%

Not only does ELS have the slightly higher yield than SUI, it also has the better dividend growth track record.

ELS has turned in 17 consecutive years of dividend growth, while SUI's record of increases only spans five consecutive years.

Admittedly, though, SUI does have the advantage in terms of payout ratio. Year-to-date in 2022, ELS's payout ratio based on normalized FFO has been 59%, while SUI's core FFO payout ratio has been 44%, potentially setting the REIT up for some higher dividend increases in the years to come.

Bottom Line

There's a lot to like about ELS. Admittedly, the REIT is pricey at around 24x NFFO, as of this writing. But even that high multiple is lower than its average valuation in the territory of 30x.

Meanwhile, 2023 should be a great year for ELS as elevated Social Security cost of living adjustments allow the REIT to raise rents at a higher rate than the last few years. ELS does benefit from inflation, only the benefit is a bit more lagging than it is for other residential REITs.

And, as shown above, even if the US economy dips into recession, it likely won't portend negative same-property NOI for the REIT, as ELS has an excellent track record of growing right through recessions.

The low starting dividend yield will be unappealing for investors looking for high current income, but for those with long time horizons or primarily interested in total returns, ELS looks like a great buy right now.

For further details see:

Equity LifeStyle Properties: A Recession-Resistant, Dividend Growth Rockstar