ELS - Equity LifeStyle Properties: Strategically Positioned In A Dynamic And Growing Market

2023-09-20 08:37:25 ET

Summary

- Equity Lifestyle Properties, Inc. is trading below its fair value despite its strong financial performance and growth opportunities.

- Recent developments, such as strong quarterly results and increased dividends, indicate the company's positive outlook.

- The company is strategically positioned and relevant to changing consumer needs, with a diverse portfolio and a track record of growth.

- Given the company’s discounted price, strategic positioning, and commitment to its shareholders, I rate it a buy.

Investment Analysis

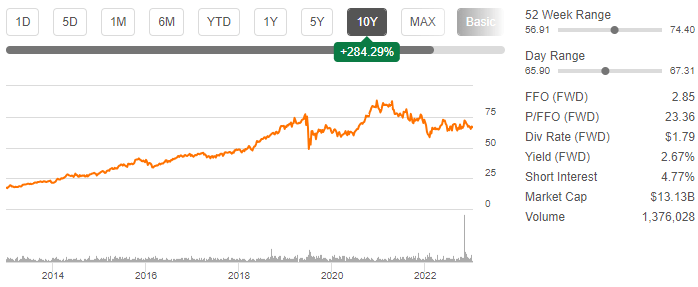

Despite a spectacular share rise of more than 284% over the last decade, Equity LifeStyle Properties, Inc. ( ELS ) is trading below its fair value, according to my model estimates. I believe the company’s strong financial performance, growth opportunities, and initiatives such as acquisitions have fueled the excellent share performance.

{kind=link}

With the company trading below its fair value, I am bullish on it because it is strategically positioned to leverage the market, and its offerings are relevant to the dynamic consumer needs. Further, the company’s recent developments mirror my bullish stance. Additionally, it has delivered to its shareholders over the last decade, as evidenced by its commitment to return capital to shareholders through dividends and an attractive TSR of about 496% compared to the S&P 500 of about 311% in the same period. Given my bullish stance on the company and the excellent returns to its investors, I rate the company a buy.

Current Developments: Reasons To Be Optimistic

In light of recent activity with ELS, I am more upbeat about this stock. First off, the company reported strong MRQ results. On July 17, 2023, ELS announced its financial results for the second quarter, which showed a 7.4% year-over-year increase in revenue, a 13.9% increase in net income, and a 9.1% increase in funds from operations [FFO] per share. The company also increased its full-year sales, net income, and FFO per share projections. These results, in my opinion, show the company’s strong demand for its properties and services, particularly in the property segment, which caters to active retirees and vacationers. I also think the results reflect that the company is well-positioned to provide long-term value for its shareholders and customers, as evidenced by the rising FFO per share and growing dividends.

The second development is that the firm has declared a new dividend . On July 25, 2023, the company announced a quarterly dividend of $0.4475 per share, up 9.4% over the same period in the previous year. On October 13, 2023, dividends will be distributed to stockholders of record as of September 29, 2023. The dividend increase, in my opinion, indicates the company’s confidence in its cash flow generation and commitment to returning capital to its shareholders, which I believe is a compelling reason to be optimistic about the future.

Lastly, in this section is the passing of Samuel Zell , the company’s founder and chairman emeritus, on May 18, 2023. He was an innovative business leader and a trailblazer in the manufactured home sector, growing ELS from a regional player to a national powerhouse with over 420 properties and 165,000 sites. His demise might cause some shareholders to worry about the company’s future because of his positive impact on its development, but I don’t share their concerns. Despite the emotional toll his passing may have on the company and its stakeholders, Zell’s inactivity since 2012 makes it unlikely that his demise will have any practical effect on the company’s strategic direction or performance.

Furthermore, the corporation is committed to honoring his legacy by following his vision of developing exceptional communities for people to enjoy life, which I believe is very promising. Based on this background, the recent advances of this company are highly promising, and they offer me reason to be confident about the company’s future.

Strategic Positioning While Staying Relevant To Dynamic Consumer Needs

Following the company’s strong success in the past, it is critical to assess its ability to replicate similar performance in the future. I believe the company’s future success will be based on its strategic positioning while remaining relevant to changing consumer needs. Below is my assessment of how the company is strategically positioned and how relevant it is to changing consumer preferences.

Quality: ELS is dedicated to giving its consumers, who are primarily active retirees and vacationers , first-rate real estate services and experiences. It owns and manages more than 450 properties in 32 states and Canada, including RV resorts, campsites, and marinas for manufactured homes. Regarding ELS’s properties , cleanliness, security, and convenience are always top priorities. In addition to traditional marketing strategies, the company uses data analytics , customer relationship management, and online booking to increase consumer satisfaction and loyalty.

Diversification: ELS has a wide variety of properties to meet the needs of a wide variety of customers. The housing options provided by the company range from single-family homes to cottages, cabins, park models, and RV parking. Activities such as fishing, boating, golfing, hiking, bicycling, and skiing are just some of the vacation options available to you at ELS. Florida, California, Arizona, Texas, Colorado, and British Columbia are just a few of the states and provinces where you may find ELS homes, all of which are among the most popular places to live and visit. This diversity allows the company to meet diverse consumer needs and command a wider market reach both physically and by-product offering; in my view, this is a competitive advantage and a key growth lever.

Growth: The company has a strong track record of organic and acquisition-based growth. Over the last decade, ELS has consistently grown its sales, net income, FFO, and dividends. It has also increased its portfolio by acquiring new properties to supplement those already owned. It added 23 properties to its portfolio in 2021 alone, including 10 RV resorts and campgrounds, ten marinas , and one manufactured home community . The company also aims to boost occupancy and rental prices by recruiting new consumers and retaining current ones, which bodes well for the company’s future success.

Given this background, I have confidence in the company’s future performance because I believe its high-quality product delivery, diversity, and expansion initiatives will lead to increased earnings from a larger client base and higher customer retention rates.

I believe the company’s products are relevant to consumers since they meet the growing demand for flexible housing and lifestyle. I believe ELS’s clientele like the sense of community, convenience, and coziness that the company’s facilities offer. Customers should appreciate the wide range of amenities and entertainment options provided by ELS’s properties, making its products and services relevant. Its diverse services are attractive to retirees and seasonal residents from the baby boomer generation as well as to young professionals and vacationers from other generations.

Generally, I find ELS strategically positioned and relevant in the dynamic market, which will serve as a major growth lever in the long run. In simple terms, this aspect serves as the backbone of the company’s future growth. According to IBIS World , the manufactured home business will increase at a 7.1% annualized rate from 2023 to 2028, while the RV Park and campground industry will grow at a 3.8% annualized rate during the same period. These trends suggest that ELS’s solutions have significant market potential and client appeal, lending credence to my bullish assertion of the company.

Valuation

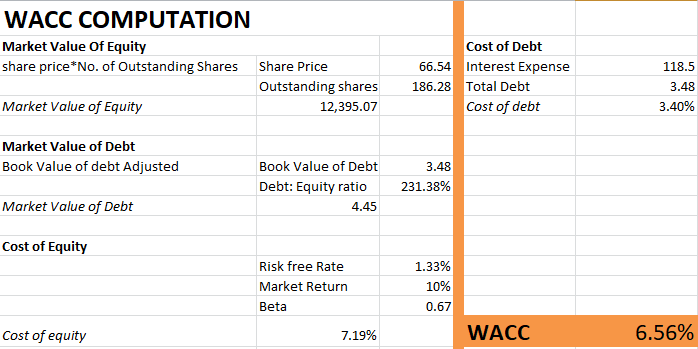

I utilized a DCF model to assess the fair value of ELS because it reflects the underlying fundamental drivers of a firm, such as the WACC. In my model, I estimated a 15% annual growth rate, which is quite conservative given the average annual growth rate of 16.7% during the last five years, and a 5% terminal growth rate, which is slightly greater than the US’s 3.67% inflation rate over the last five years. For the discount rate, I used the company’s WACC, which I arrived at using the formula WACC = E / (E + D) * Re + D / (E + D) * Rd * (1 - T), where;

E=market value of equity

D=market value of debt

Re=cost of equity

Rd=cost of debt

T=effective tax rate

Below is the WACC based on this formula.

{kind=link}

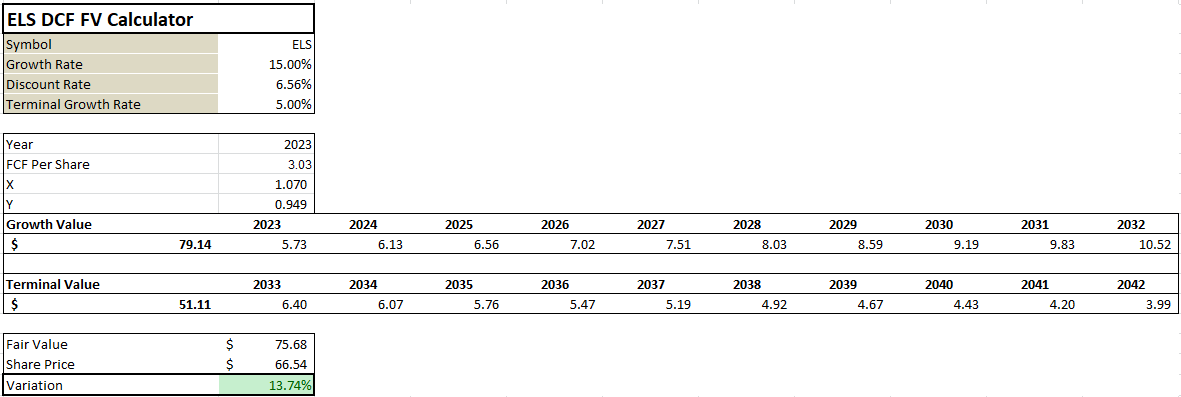

Below is my DCF output model using this WACC as the discount rate and the other assumptions specified above.

{kind=link}

According to the results of my model, the company has a fair value of $75.68, indicating a 13.74% potential upside. These findings point to a bullish trend, which I believe will be bolstered by the company’s strong growth levers. These results indicate that the company is trading at a discount to its intrinsic value and has the potential to grow by double digits, making it an appealing investment. My findings are consistent with a Finbox DCF model , which estimates the company’s fair value at 73.94 with a 13.5% upside potential. This lends credence to my assertion that ELS is trading below its fair value, and therefore, potential investors should leverage this cheap entry point.

Risks

Even though investing in ELS has the potential to be profitable and rewarding, there are risks that you should be aware of and ready to deal with. Possible risks include:

Exposure to natural disasters and climate change: One of the greatest risks is ELS’s exposure to natural disasters and climate change, which could destroy its properties and interrupt its operations. It owns and manages properties in areas vulnerable to hurricanes, floods, wildfires, earthquakes, and other extreme weather events. For example, ELS reported $8.1 million in property damage and $2.4 million in income loss due to hurricanes and wildfires in 2020. Climate change may increase the frequency and intensity of these occurrences.

Dependence on property segment : Another key risk, in my opinion, is ELS’s reliance on the performance and reputation of its property segment, which represents 90% of total revenue. Any adverse publicity, customer dissatisfaction, or litigation concerning ELS or its properties may jeopardize the company’s reputation and operations.

Suppose these risks occur and negatively impact the company, causing the upward trajectory to shift to a significant downward trajectory in the absence of a defined turnaround strategy from the company. In that case, my optimistic attitude will shift to a pessimistic stance.

My Investment Position

Based on my analysis, this company is a good investment opportunity given its attractive returns to investors; its upside potential is backed with solid growth levers in its strategic positioning and relevance to diverse and dynamic consumer needs. Further, its current affairs inspire my confidence regarding the company’s future performance. Based on this information, I confidently rate the company a buy and recommend it to potential investors seeking to diversify in this industry.

For further details see:

Equity LifeStyle Properties: Strategically Positioned In A Dynamic And Growing Market