VNQ - Equity Residential: Discounted Price Spells Opportunity

2024-01-18 08:10:22 ET

Summary

- Apartment REITs have underperformed in the past year, including Equity Residential, which has seen minimal share price growth.

- Equity Residential was founded by Sam Zell, and is one of the largest multifamily REITs, focused on prime markets in Tier 1 cities.

- Despite short-term headwinds, EQR has a strong balance sheet, consistent dividend payments, and potential for long-term growth, making it an attractive investment at present.

Apartment REITs haven’t had an easy go over the past year, as they were among the worst performing property sectors in 2023, despite coming off mid-single digit growth and double-digit bottom line growth in the years 2021 and 2022.

This brings me to Equity Residential ( EQR ), which I last covered here back in September of last year with a ‘Buy’ rating, noting its long history of respectable shareholder returns and presence in in-demand Tier 1 markets.

While the stock has given investors a respectable 5% total return since then, it remains relatively flat over the past 12 months with just a 1% rise in the share price, and trades well below its normal historical valuation. In this article, I provide an update and discuss why EQR remains an appealing high quality pick for durable income and potentially strong returns from here, so let’s get started!

{kind=link}

Why EQR?

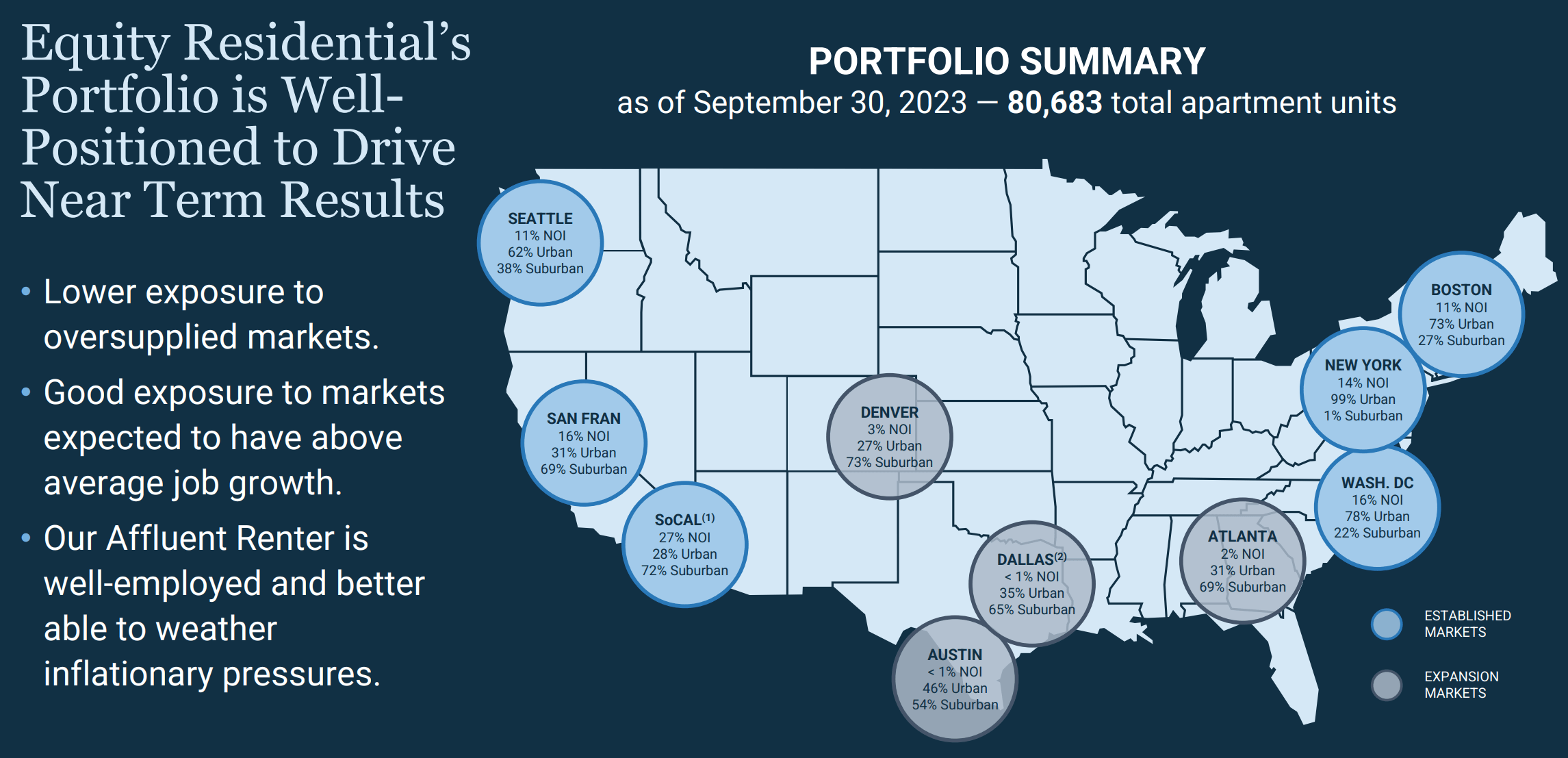

Equity Residential is an S&P 500 ( SPY ) company and is one of the largest multifamily REITS on the market today, alongside peers like AvalonBay Communities ( AVB ) and Essex Property Trust ( ESS ). Like it's large peers, EQR is focused on prime markets with 305 properties in Tier 1 cities like New York, Boston, Washington D.C., Seattle, and San Francisco, as shown below.

{kind=link}

EQR was founded by the famed real estate investor, Sam Zell, who served as Chairman of the company and passed away last year. Sam was well renowned for his deep understanding of value creation and real estate cycles, and this is perhaps best exemplified by his perfect timing of the sale of Equity Office in 2007 to the Blackstone ( BX ) just before the real estate crash of 2008-2009 at a price "he couldn't refuse".

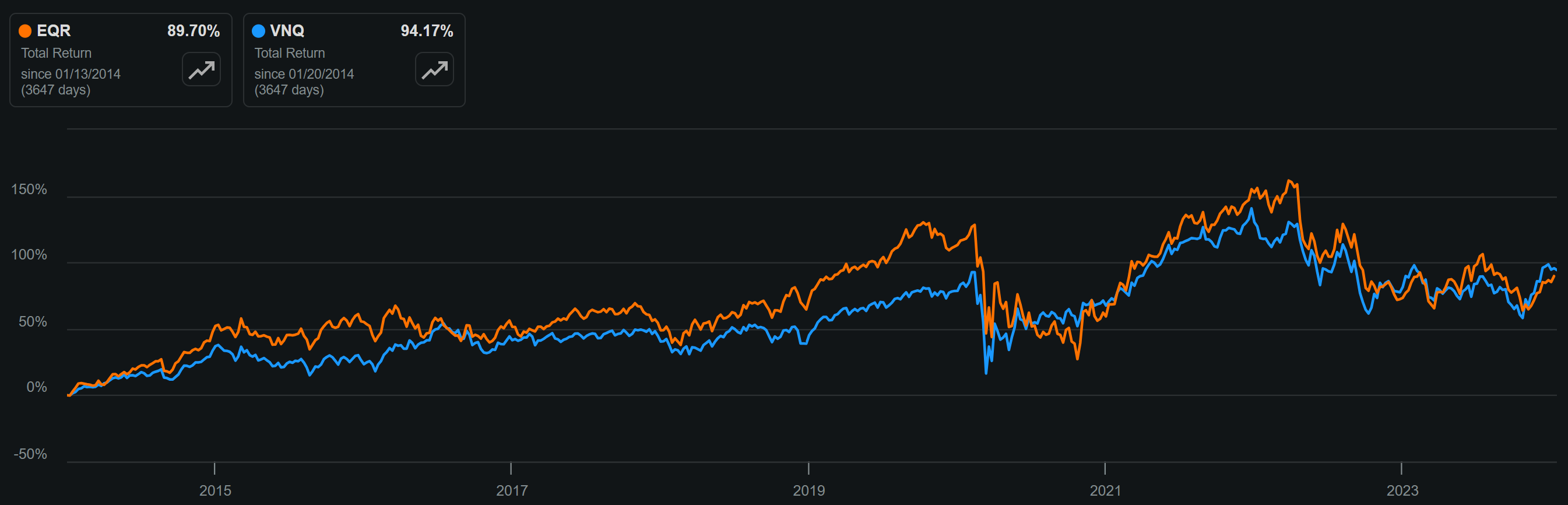

The same track record of value creation happened at Equity Residential, as reflected by EQR outperforming the Vanguard Real Estate ETF ( VNQ ) over much of the past 10 years, as shown below.

{kind=link}

Of course, investors who track the multifamily segment know that apartment REITS haven't been solid performers in terms of price appreciation over the past 12 months, as reflected by EQR's 1% share price gain over this timeframe, well underperforming the S&P 500.

EQR's underperformance isn't completely unwarranted, with investors baking in slower growth. This is reflected by a slowdown in same-store NOI growth to 4.6% and 6.6% YoY for the third quarter and first nine months of 2023, respectively. This is comparatively lower than the robust 14.1% same store NOI growth that EQR saw in the full year 2022, as the net population migration back into EQR's markets has slowed and new supply have pressured rental increases. Weakness in growth was pronounced in EQR's San Francisco and Seattle markets, which underperformed compared to the rest of the portfolio, as well as evictions taking longer in Los Angeles (from 2-3 months pre-pandemic to over 6 months at present).

Risks to EQR include potential for a faster than anticipated slowdown in leasing activity for Q4 and beyond, which could put pressure on the share price. However, recent data points from RealPage, an apartment analytics firm, recently indicated this month that while apartment completions jumped to a 36-year high in 2023, demand was "surprisingly" strong during the fourth quarter with a net absorption of 58K units. This made Q4 of 2023 the 3rd strongest fourth quarter in 25 years, and it brings the full-year total net absorption 234K units, which is similar to pre-COVID levels.

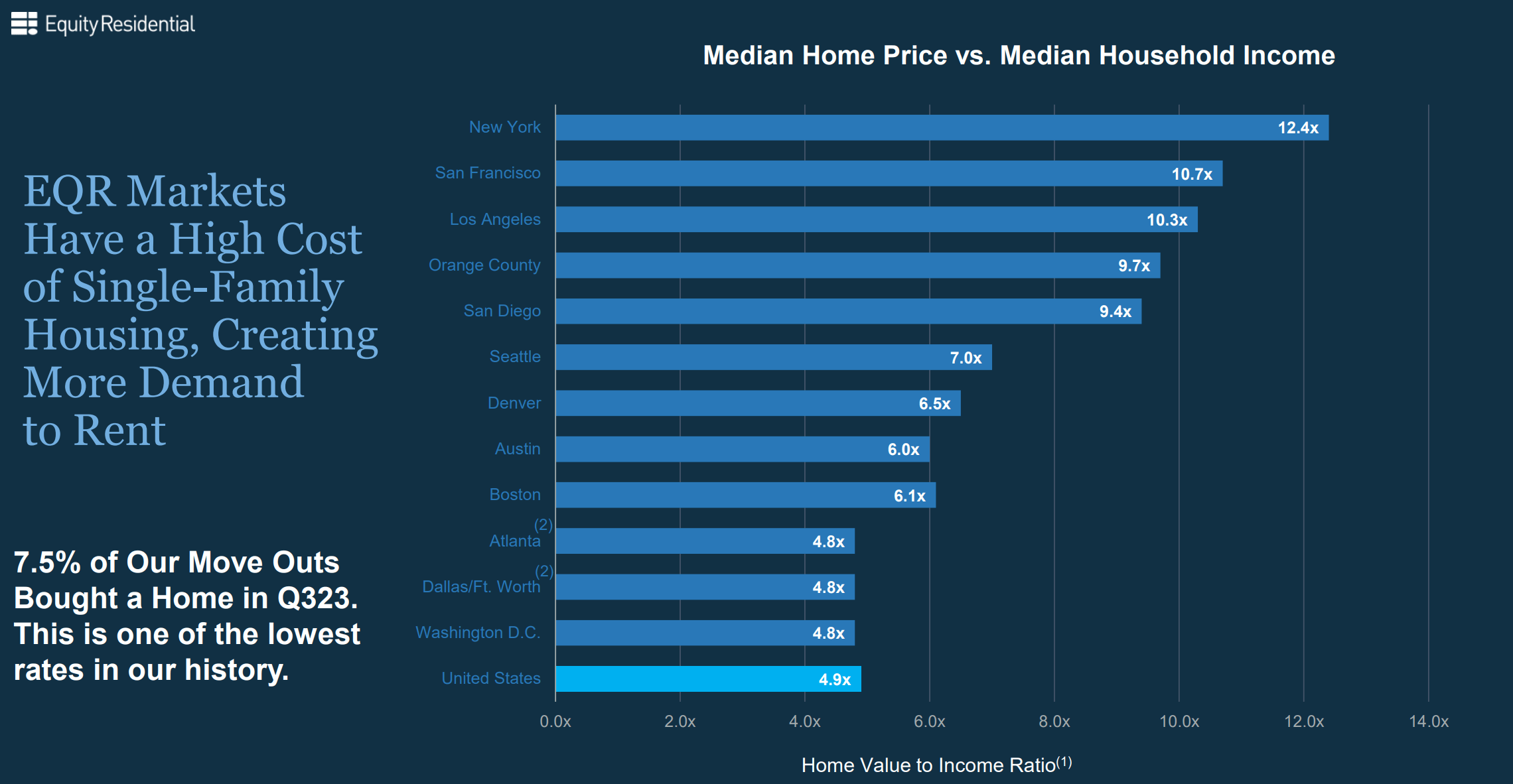

Moreover, EQR could see continued tailwinds in 2024 due to low unemployment levels and wage growth in its markets. Additionally, interest rates remain elevated, as Treasury Yields again surpassed the key 4% level this week, giving upward pressure on mortgage rates. This could further strengthen the value proposition behind apartment living. As shown below, the median home price to median household income ratio in EQR's markets remain well above that of the U.S. national average.

{kind=link}

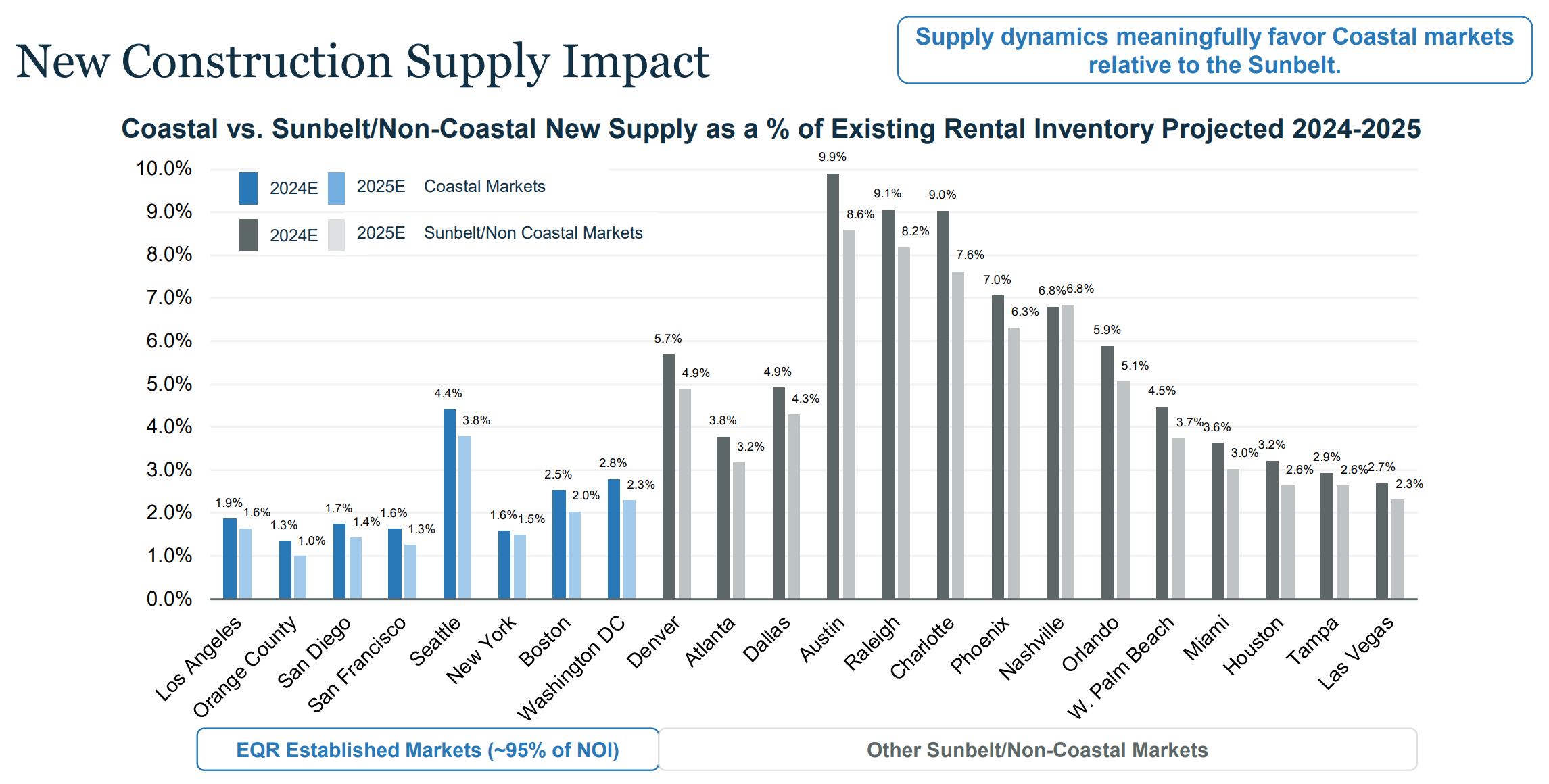

EQR should also see benefits from lower deliveries of new supply in its established markets compared to expectations of elevated deliveries in the Sunbelt markets over the next few years. As shown below, projected new supply in 2024-2025 as a percentage of the total market in EQR's cities are pronouncedly lower than that of Sunbelt markets.

{kind=link}

Importantly, this isn't the first time that EQR has seen a slowdown in rental growth due to new supply/lower demand, as previous troughs have been marked with a strong uptick in demand in the following years as supply/demand imbalances normalizes, as noted during the last conference call :

It is a volatile market. And that's part of why we've been saying since 2018, we wanted to lower exposure. But you get paid for the volatility. So, for example, post-GFC, EQR same-store revenues in San Francisco, they were down over 2% each year for two years in a row. So, we got hammered a little bit there. But for the next five years, on average, our same-store revenue was up 9% a year. I think our shareholders got paid back for taking that risk and volatility.

I think the conditions in the job market in San Francisco can improve pretty rapidly, along with Redmond, Washington, the center of the artificial intelligence employment boom that we hope is coming. But I will fully concede there's an elongated recovery going out in San Francisco. And this management team is responsible. If it's responsible for anything, it's responsible for being optimistic. And some of the things we saw in the middle of the year in that market made us feel like that recovery was coming right now. We still have faith that will come.

Meanwhile, EQR maintains a very strong balance sheet with $2.5 billion in liquidity and is only a handful of REITs with A-/A3 credit ratings from S&P and Moody's. This is supported a net debt to EBITDAre ratio of just 4.2x, sitting well under the 6.0x level generally considered safe by ratings agencies. EQR also has a strong 6.1x fixed charge coverage ratio and low debt to total assets ratio of just 27%, sitting below the 50% mark generally considered safe for REITS.

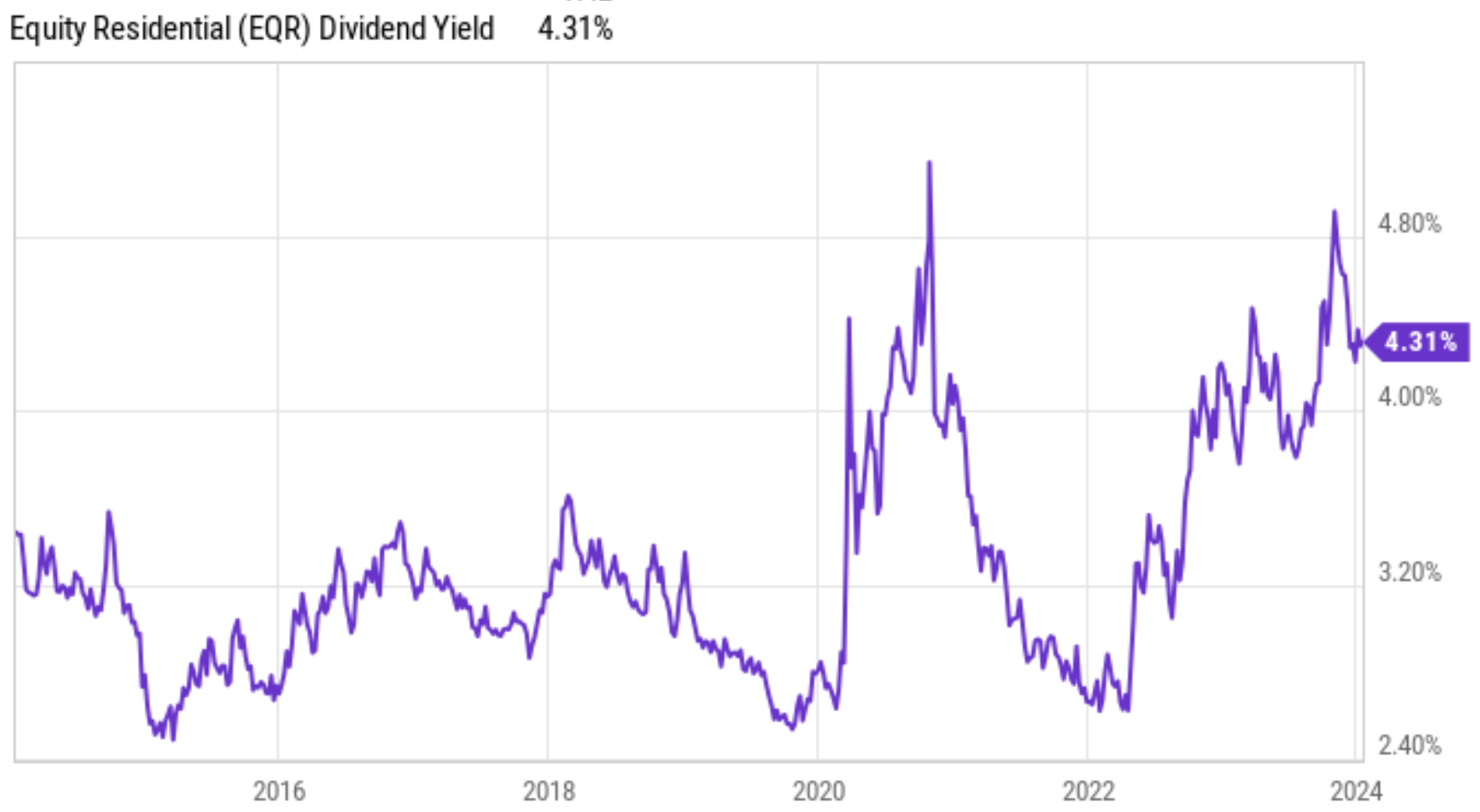

Importantly for income investors, EQR currently yields 4.3% and the dividend is well-covered by a 70% payout ratio. EQR raised its dividend by 6% in 2023 and has paid an uninterrupted or growing dividend every year since 2010 (when including the special dividends in 2016). As shown below, EQR's current yield sits at the high end of its 10-year range.

{kind=link}

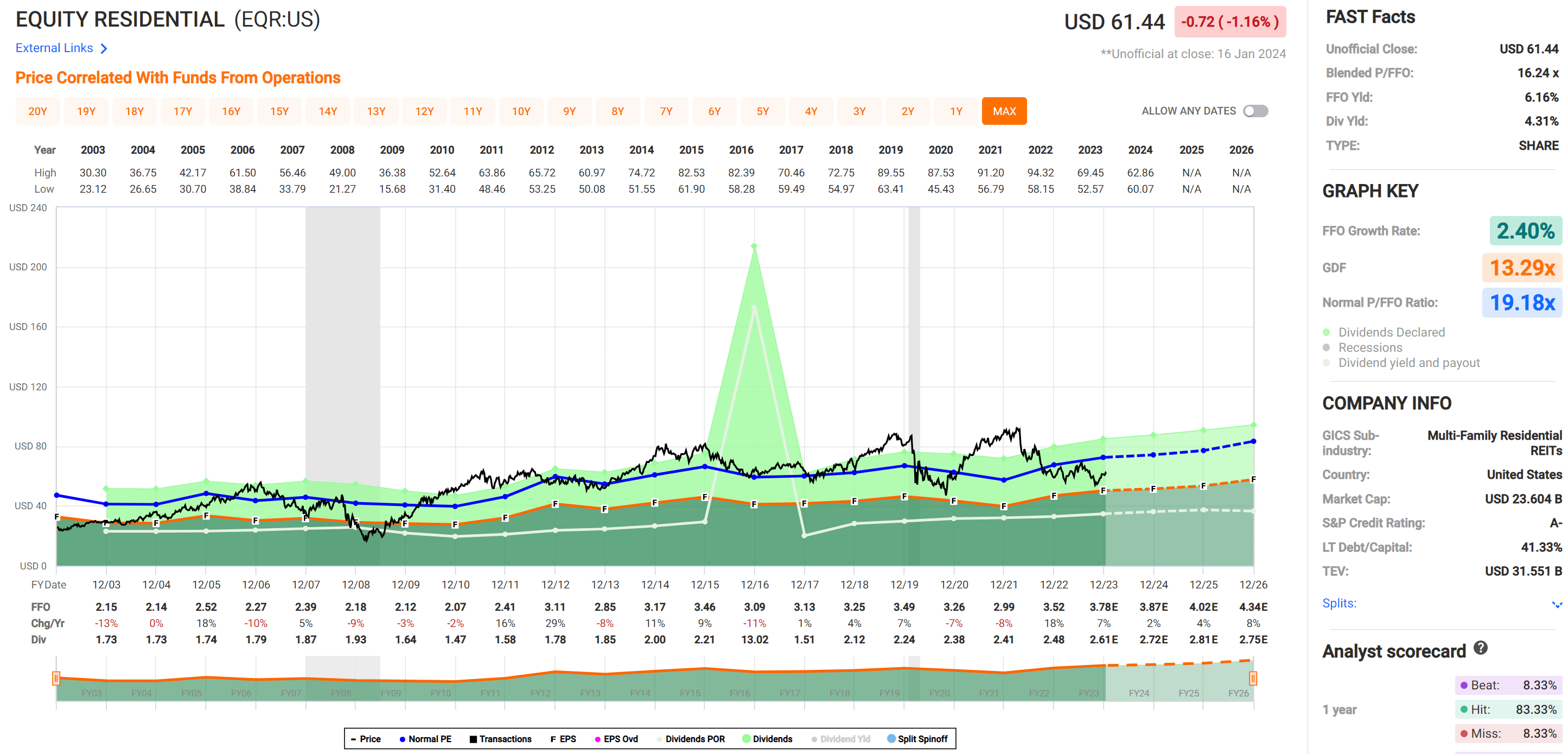

Lastly, I continue to see solid value in EQR at the current price of $61.33 with a forward P/FFO of 16.3, sitting well below its normal P/FFO of 19.2. The market also seems to be overly-pessimistic around the recent headwinds for EQR. While analysts expect just 2.7% FFO/share growth this year, growth is expected to pick up in the 2025-2027 timeframe with estimated annual FFO/share growth I the 4.5% to 9.2% range.

{kind=link}

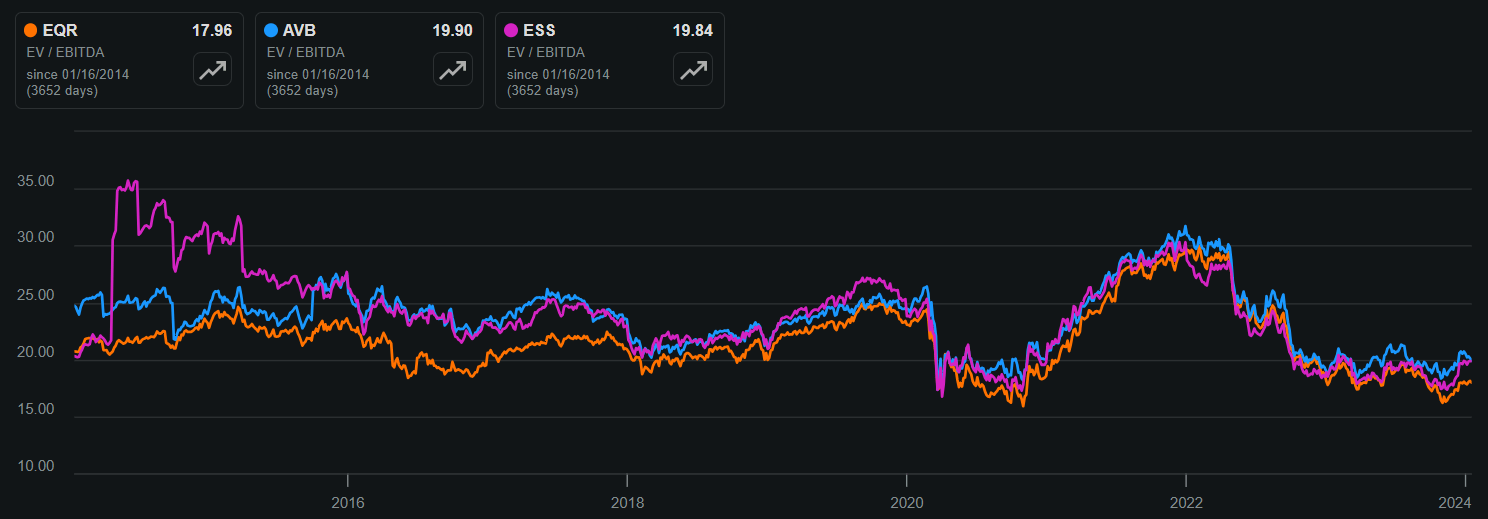

EQR also trades at a discount to its coastal focused peers, AvalonBay Communities and Essex Property Trust, with an EV/EBITDA of 17.96x, sitting below the 19.8x to 19.9x of its peers, as shown below.

{kind=link}

Investor Takeaway

In summary, EQR continues to face short-term headwinds due to a slowdown in tenant demand in some of its markets. However, the long-term outlook for EQR remains strong with tailwinds from low unemployment and wage growth, as well as potential demand recovery as new supply in EQR's markets is expected to be muted compared to others. Additionally, EQR maintains a strong balance sheet and has a track record of consistently paying dividends. At its current discounted valuation, EQR presents compelling value for income investors looking for exposure to the US apartment market. As such, I maintain a 'Buy' rating on EQR stock.

For further details see:

Equity Residential: Discounted Price Spells Opportunity