ERMAY - Eramet: Battery Metals Stock With 50% Upside Potential On Lithium Integration

2023-07-12 05:40:50 ET

Summary

- Eramet owns the world's largest manganese and nickel mines and is looking to add lithium to its portfolio to become close to a one stop shop for battery metals.

- Eramet has seen tough headwinds in the most recent quarter, as pricing on manganese alloys and class II nickel plummeted.

- However, the long-term market trends and forecast look positive, and yet the stock appears to be significantly undervalued.

- The valuation, however, hinges on the assumption that the company successfully executes its lithium integration strategy.

Investment Thesis

Eramet S.A. (FR:ERA) (ERMAY) (ERMAF) is among the world's largest producers of nickel and manganese, and plans to ramp up lithium production in mid-2025 - three key minerals found in every electric vehicle battery. There are not many companies in the entire world better positioned to exploit the global electrification race than Eramet, and yet for some reason the stock is trading significantly below its intrinsic value.

A Growing Battery Metal Giant

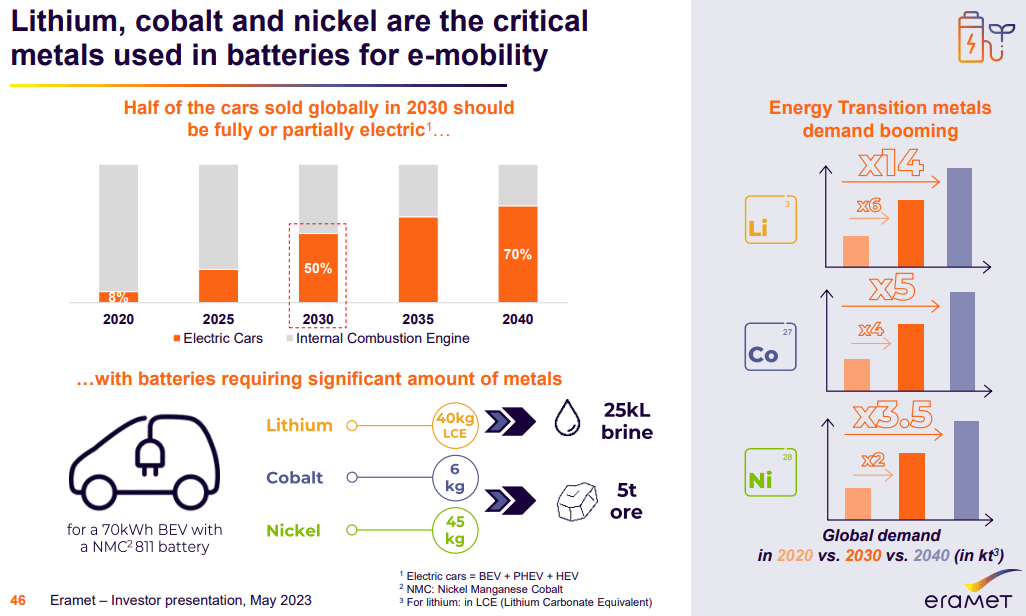

Battery metals are obviously in high demand amid the green transition, with most countries in the world making significant investments in the hopes of reducing emissions to net-zero. Just think, by 2030 about 50% of cars sold will likely be either fully or partially electric. And now consider that each car will need an electric battery that is made of minerals like nickel, manganese, lithium, and cobalt. In fact, demand for nickel is expected to double by 2030 from where it was in 2020, while lithium requirements will grow by a factor of six during the same timeframe.

{kind=link}

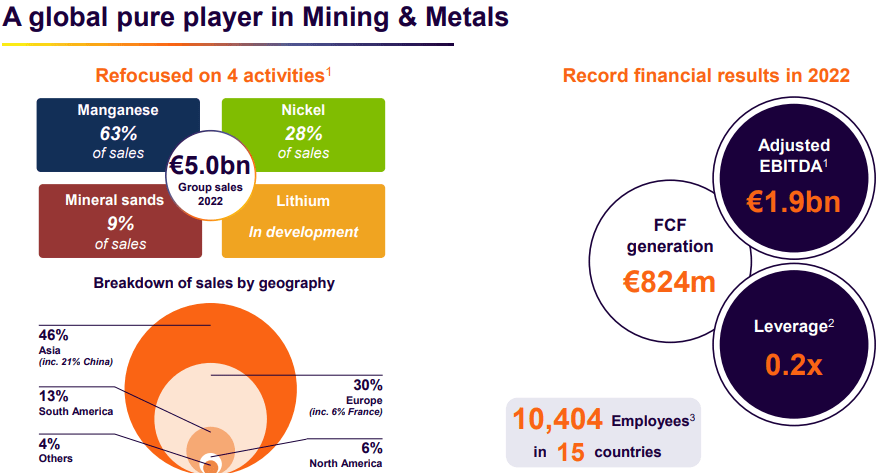

Eramet recorded about $5.5 billion in sales in 2022, 63% of which derived from manganese and 28% from nickel. And, by the end of the decade, after a two-phased lithium project is fully ramped up in Argentina, lithium could end up accounting for over 22% of Eramet's revenue.

{kind=link}

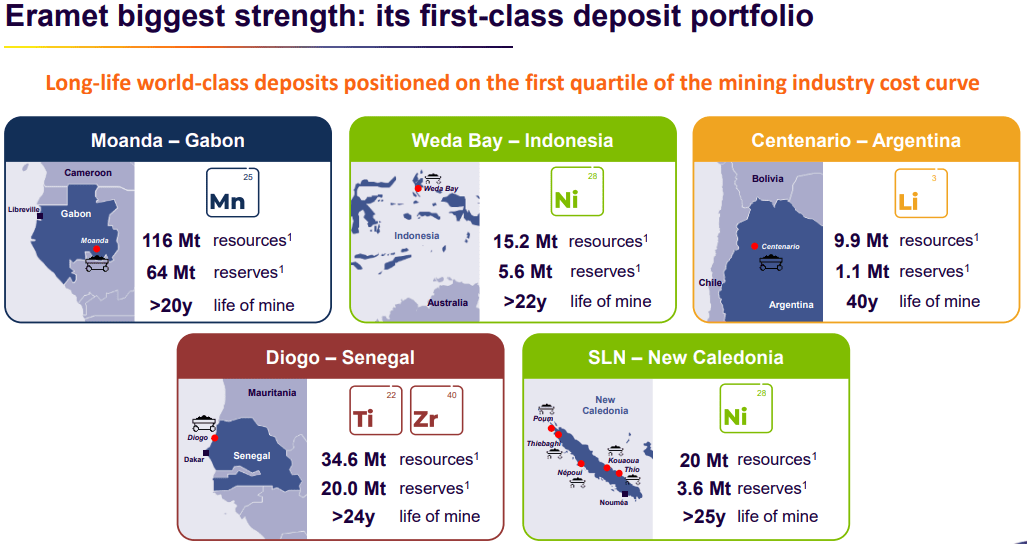

The company has seventeen mining and metallurgical sites worldwide, including the world's largest manganese mine (Gabon) and the world's largest nickel mine (Indonesia). Eramet has more than 20 years worth of manganese reserves, over 25 of nickel, and 40 in lithium carbonate equivalent (LCE).

{kind=link}

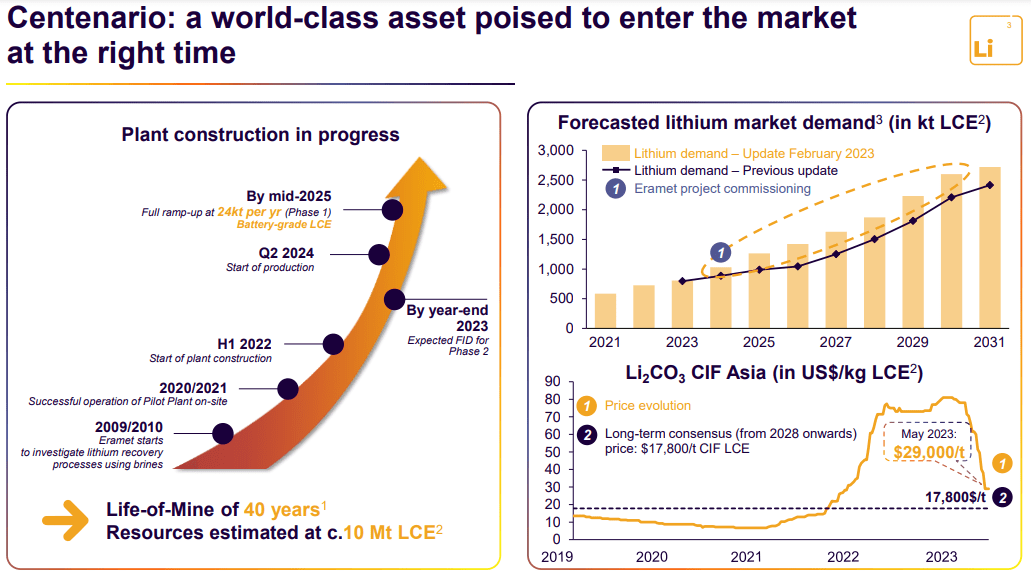

They are looking to ramp up production at the Centenario lithium mine in Argentina beginning in Q2 of 2024 but don't expect to hit the full run rate of 24kt/year until mid-2025. A phase 2 Centenario initiative will raise lithium capacity by an additional 50kt per year, bringing the total potential annual output to around 75kt.

As we shall see, it is the lithium play that makes Eramet's stock an attractive investment. Without at least phase 1 ramping up within a reasonable timeframe, the stock is probably overvalued at its current trading price.

Valuation

The price of lithium has been quite volatile over the past couple years and forecasters suggest it will remain volatile for the foreseeable future. The mineral hit as high as $80,000 ton last year before falling sharply and is now at about $40,000/t. According to Eramet, the long-term consensus has lithium coming down to $17,800/t from 2028 onwards.

Eramet Lithium Project Assumptions (Eramet May Investor Presentation)

{kind=link}

Assumptions around the price of lithium and projected timing of the Centenario phases will be pivotal in forecasting future cash flows. Another key consideration is the higher margins lithium will bring to the table as well. Eramet said that even at a price of $17,800/t, the EBITDA on 24kt of lithium would be about $300mln, implying an EBITDA margin of 70%.

The company based this projection on an ex-works cash cost of $3,500/t. This will explain the rising operating margin in our discounted cash flow model. Consider that last year's EBITDA on manganese for Eramet was 44% and nickel 31%.

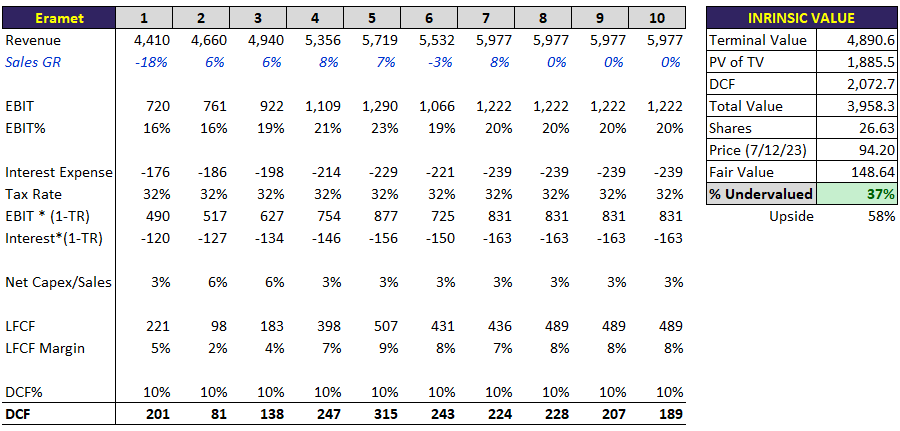

Based on the below DCF calculation, I found the stock 37% undervalued, implying an upside of 58%.

Key DCF Assumptions:

Lithium Prices - In the end, I decided to start with lithium at $29,000/ton and lowered it to the consensus target cited by Eramet of $17,800/ton.

Revenue Growth - The top-line for the first 3 years of the model I relied on analyst consensus estimates sourced from Seeking Alpha. I then simply calculated the revenue based on the new lithium volumes and pricing for years 4-10.

EBIT Margins - Operating margins starts at 16% in year 1 before gradually rising as lithium comes online.

Capex - For capex I relied on company guidance for year 1 and the investments Eramet projected for the lithium ramp up. So in years 2 and 3 you will notice the net capex rise dramatically before reverting back near the mining and metals industry average (which is actually 2.34% per Professor Aswath Damodaran's sector data ).

Discount rate - 30-year nominal return of the S&P500 with dividends, which amounts to about 9.85% (which I then round up).

{kind=link}

Key Risks

Although the long-term demand picture looks quite positive, near-term headwinds have been problematic. Eramet's sales were down 24% in Q123 , largely due to an expected drop in commodity prices. The decline was especially significant for manganese alloys and class II nickel.

And I would like to again stress that the valuation is based on the assumption that phase I of the lithium project will be hitting full run-rate in mid-2025 and phase II comes online a few years later. Without lithium in the equation, the stock is probably overvalued.

Finally, one other concern is the illiquidity of the OTC tickers. The average daily trading value of ERMAF over the past 30 days is about $8,000 while ERMAY is under $35k. However, Eramet's primary listing , ERA, on the Paris stock exchange, has an average daily trading value of nearly $5mln. This is just to underscore that Eramet isn't a "fly-by-night" operation. And there is certainly sufficient information publicly available for making informed investing decisions. That said, with lower volume comes the risk of higher volatility.

Conclusion

There are few companies on earth better positioned to exploit the boom in battery metals than Eramet, considering it owns the largest manganese and nickel mines in the world and will start adding lithium to the collection next year. Integrating lithium will also boost the company's operating and levered free cash flow margins. Based on the assumption that the company executes on its lithium integration strategy, Eramet stock looks about 37% undervalued, implying an upside of 58%.

For further details see:

Eramet: Battery Metals Stock With 50% Upside Potential On Lithium Integration