ERMAF - Eramet Is Transforming To Become A Leading Battery Metals Producer With Manganese Nickel And Soon Lithium

2023-04-14 06:47:24 ET

Summary

- Eramet has a global portfolio of mining assets with the majority of revenues currently coming from manganese, with revenues also from nickel and mineral sands.

- New projects in the pipeline include the JV 24,000tpa Centenario-Ratones Lithium Project targeting production from early 2024 (ramped mid-2025). Also a battery recycling project and Sonic Bay nickel-cobalt project.

- The valuation is very attractive on a 2024 PE of 4.9. The current consensus analyst rating is a 'buy' with a price target of Euro 150, representing 56% potential upside.

- The usual mining risks apply plus moderate to high sovereign risk with projects in Gabon, Indonesia, New Caledonia, Senegal, and Argentina.

- We rate Eramet as a well-valued buy suited for a 5-year+ time frame.

This article first appeared in 'Trend Investing Group' on March 14, 2023, but has been updated for this article.

Eramet [FR:ERA] (ERMAY) (ERMAF) is a French company with current manganese, nickel and mineral sands production and near-term plans for lithium production, battery recycling and new nickel-cobalt production. The Company has been performing very well boosted by strong revenues from manganese, but also nickel and mineral sands. Valuation looks attractive plus there is a strong growth outlook for new projects.

Eramet [FR:ERA] 5 year price chart - Price = Euro 96.05 ( source )

Yahoo Finance

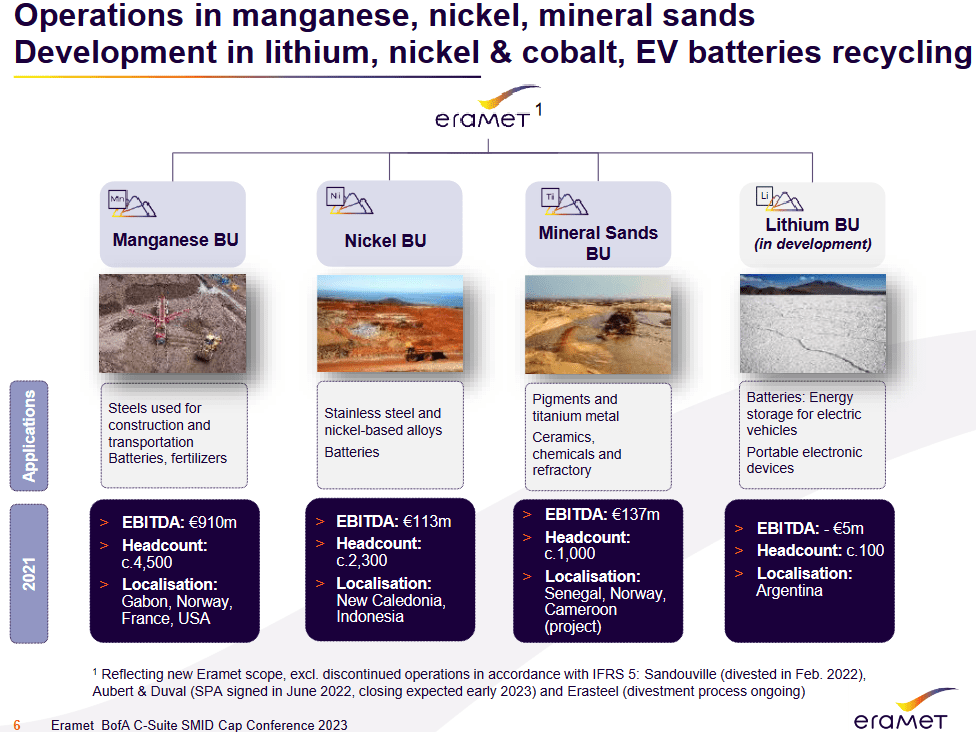

Eramet's global operations

Eramet has the following operations:

- 100% owned subsidiary Comilog Moanda manganese mine in Gabon. Moanda is one of the largest high-grade ore deposits in the world with 25% of the world's manganese reserves. The mine produced 7.5 million tonnes of manganese ore in 2022. Details here .

- Nickel operations - 100% owned subsidiary La Société Le Nickel ("SLN") (New Caledonia) and PT Weda Bay Nickel (43% Eramet: 57% Tsingshan Holding Group) in Indonesia - Ferronickel production. Details here . Also plans for a new Sonic Bay JV (51% Eramet: 49% BASF) in Indonesia. Details here and later in the article.

- Grande Côte Opérations ("GCO") mineral sands (Senegal) and Norwegian plant (production of titanium dioxide slag and high-purity pig iron). More details here .

- High Performance Alloys division - Details here .

A summary of Eramet's operations + under construction lithium JV Project ( source )

{kind=link}

Eramet's Moanda mine in Gabon holds 25% of the world's manganese reserves ( source )

Eramet website

Eramet's current sales and cash flow are dominated by manganese

As shown below manganese is by far the number one contributor to Eramet's financials, both by sales and cash flow. In future years nickel should contribute more and we are expecting to see lithium revenues starting in 2024.

Breakdown of Eramet's sales by metals (noting lithium may join in 2024) ( source )

Company presentation

Eramet's 2022 free cash flow was mostly driven by manganese sales ( source )

{kind=link}

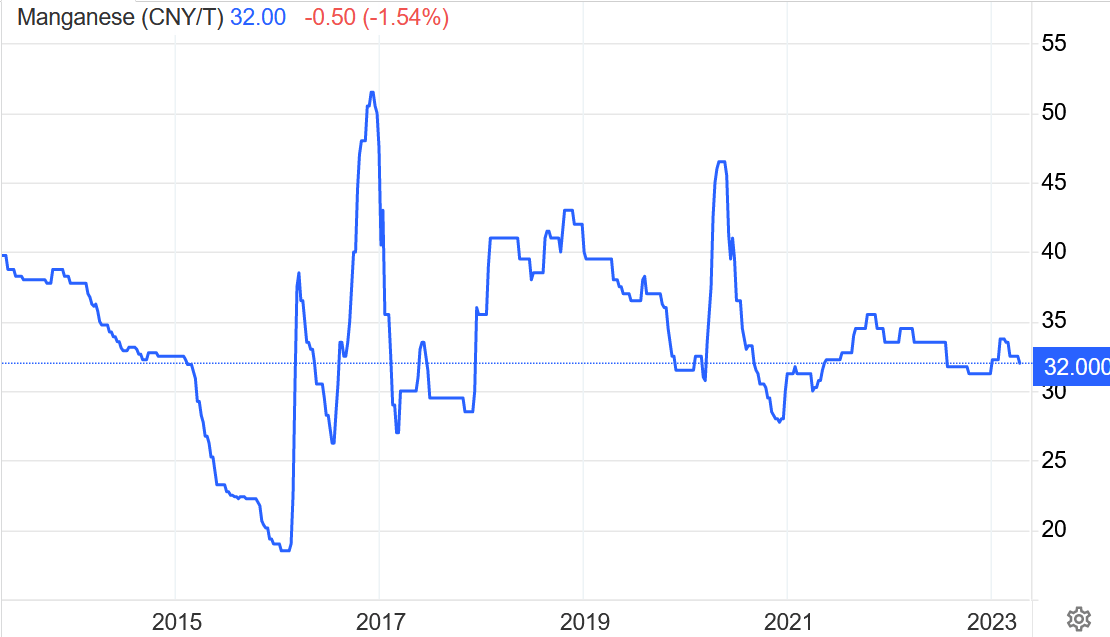

Manganese prices have not changed a lot in recent years, now at CNY32.00/t ( source )

{kind=link}

Eramet's 2023 outlook

Eramet recently announced their 2022 financials and gave the following outlook for 2023 ( source ):

2023 outlook which is in line with a less buoyant and inflationary macroeconomic context: Ore volumes up: more than 30 Mwmt of nickel ore in Indonesia and more than 7.5 Mt of manganese ore in Gabon. Average prices expected to decline compared to 2022, notably for manganese alloys. Energy and reductant costs to remain at a high level. Group adjusted EBITDA expected at around €1.2bn in 2023, including the proportional contribution of Weda Bay.

Analysts are forecasting Eramet's net income will fall back in 2023. See valuation section chart by Market Screener further below.

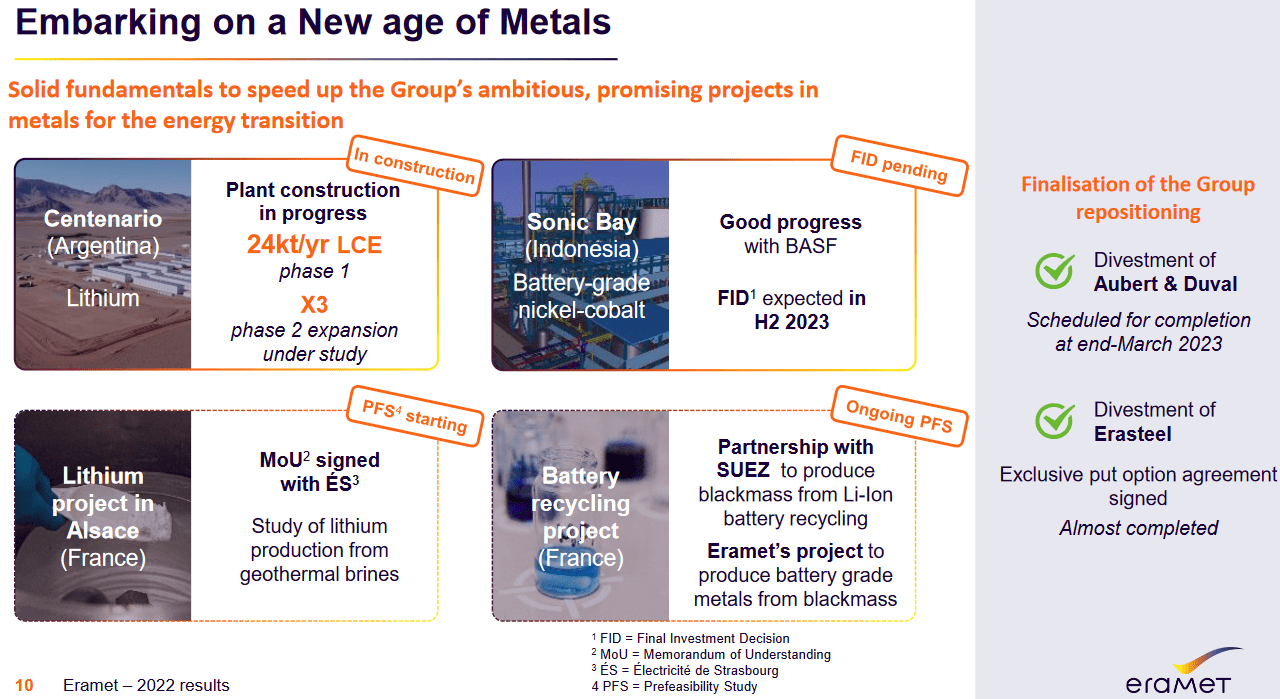

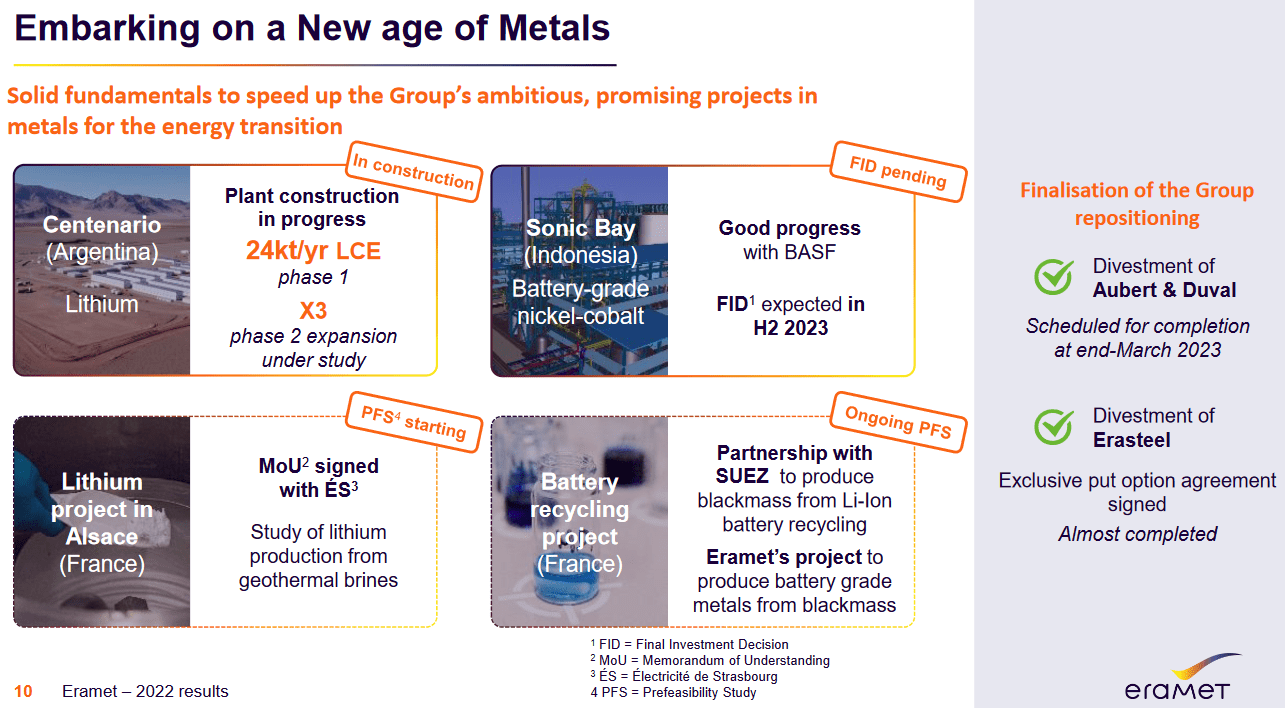

Eramet's growth plans

Eramet has numerous growth plans. The chart below gives the main growth plans, notably Centenario-Ratones Lithium JV Project in Argentina, lithium-ion battery recycling project, and the Sonic Bay nickel-cobalt Project in Indonesia.

Eramet's new growth project plans - Lithium (DLE JV in Argentina), Lithium (geothermal JV project France), nickel-cobalt in Sonic Bay Indonesia, battery recycling ( source )

{kind=link}

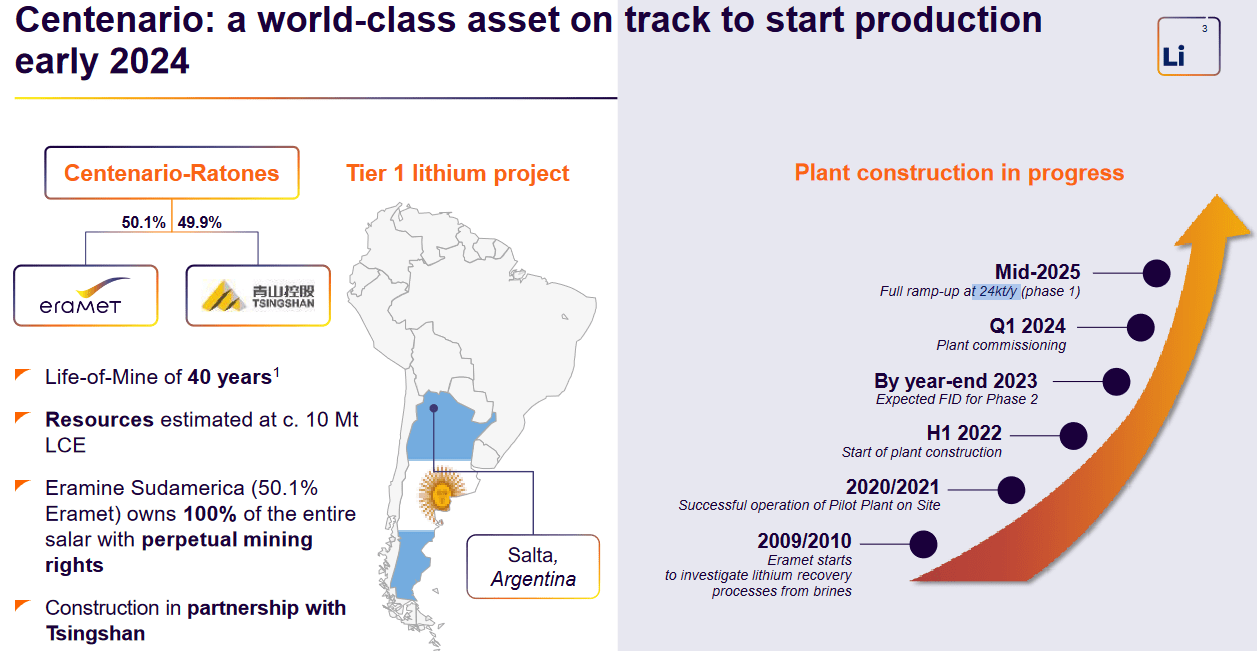

The Centenario-Ratones Lithium Project (Argentina) (using "DLE")

The Project is a JV ("Eramine Sudamerica") 50.1% owned by Eramet and 49.9% owned by Tsingshan and is located in Salta, Argentina.

The Resource size is an estimated 10 Mt LCE with a 40 year mine life .

The Project CapEx (excludes the US$185m spent by Eramet on acquisition etc) has been mostly funded by Tsingshan as a way of earning into the Project. Total CapEx is estimated at US$550m with Tsingshan contributing the first US$400m, after that the remaining CapEx (US$150m) is to be financed on a pro rata basis. OpEx (cash costs) are estimated at US$3,500/t.

Construction is ongoing with first production targeted for early 2024 with Phase 1 planning to ramp to 24,000 tpa LCE by mid-2025. A Phase 2 Feasibility Study will look at an additional 50,000tpa.

Lithium production will use direct lithium extraction ("DLE") which Eramet has tested continuously for 3 years on site with good success.

The Centenario-Ratones Lithium Project highlights ( source )

{kind=link}

{kind=link}

For more details about the geothermal brine JV Project in Alsace France (10,000tpa LCE late this decade) you can read here .

Eramet's battery recycling project

As shown below Eramet has partnered with SUEZ to produce blackmass from battery recycling in France starting in 2024. Refining the blackmass to battery metals by Eramet is targeted for 2025-26.

A summary of Eramet's battery recycling project ( source )

{kind=link}

Sonic Bay nickel-cobalt project JV (Indonesia)

The Sonic Bay Project is a JV between Eramet (51%) and BASF (49%). It will take ore from the Weda Bay deposit and process at a hydrometallurgical complex with a high-pressure acid leach ("HPAL") unit, to produce mix hydroxide precipitate containing 67,000tpa nickel and 7,000tpa cobalt.

Production is targeted to start in early 2026 , subject to a final investment decision.

Summary of Eramet and BASF JV planned project in Sonic Bay, Indonesia ( source )

{kind=link}

Valuation

Eramet's current market cap is Euro 2.75b . Eramet reports end 2022 net debt at Euro 344m .

2023 PE's is 6.3 and 2024 is 4.9. 2023 net profit margin is forecast to be 10.2%.

Current consensus analyst rating is a 'buy' with a price target of Euro 150.00 , representing 56% potential upside.

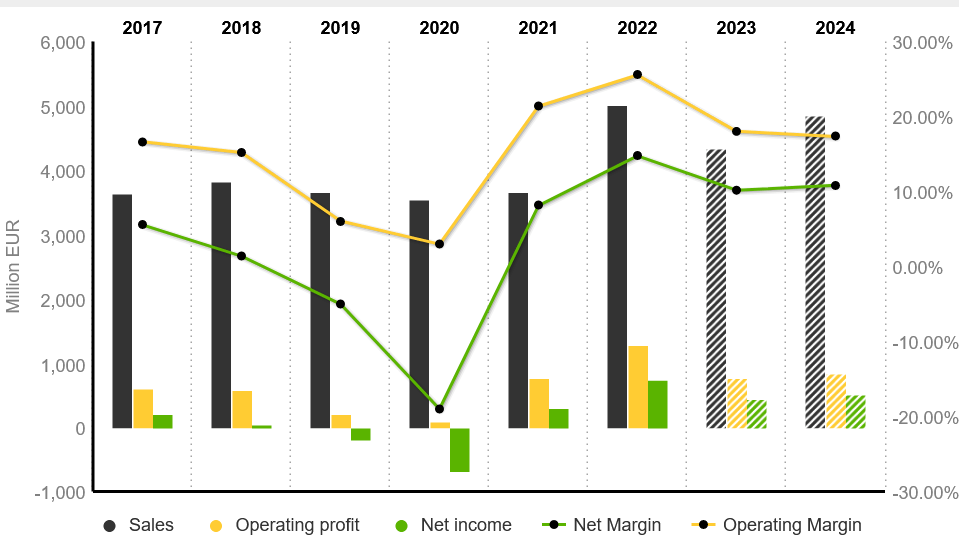

Eramet's financials and forecast financials ( source )

{kind=link}

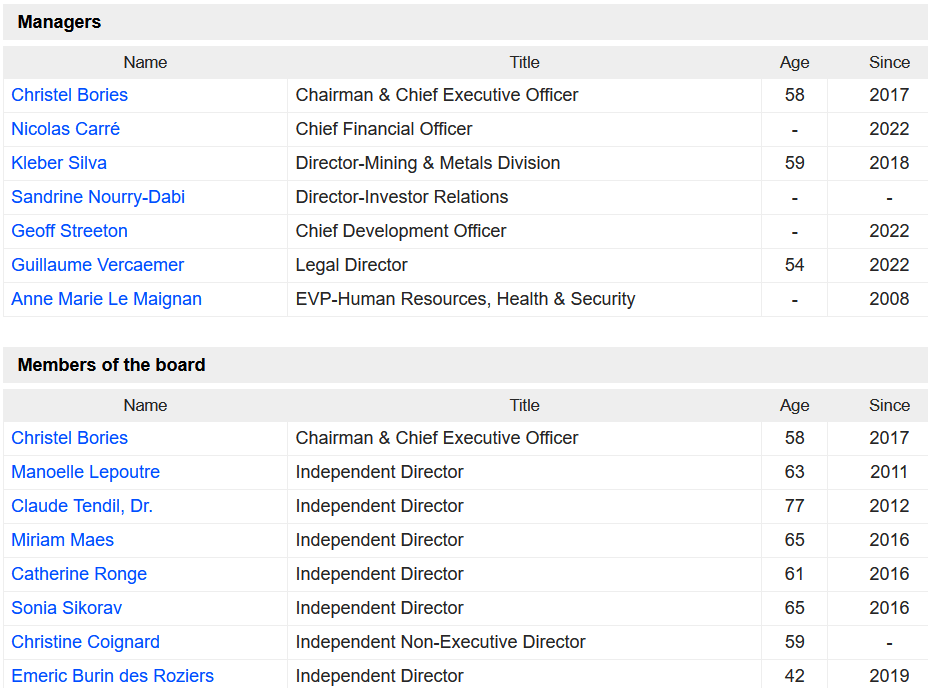

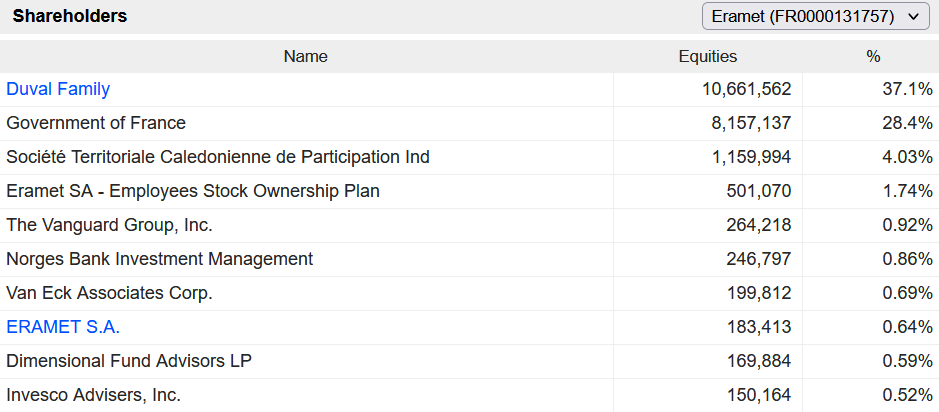

Management and top shareholders

Eramet is led by Chairman & Chief Executive Officer Christel Bories . You can read some details here .

You can read more details on the board and management here .

Management, board and shareholders ( source )

{kind=link}

{kind=link}

Latest key news

- February 23, 2022 - Eramet: 2022 full-year results presentation

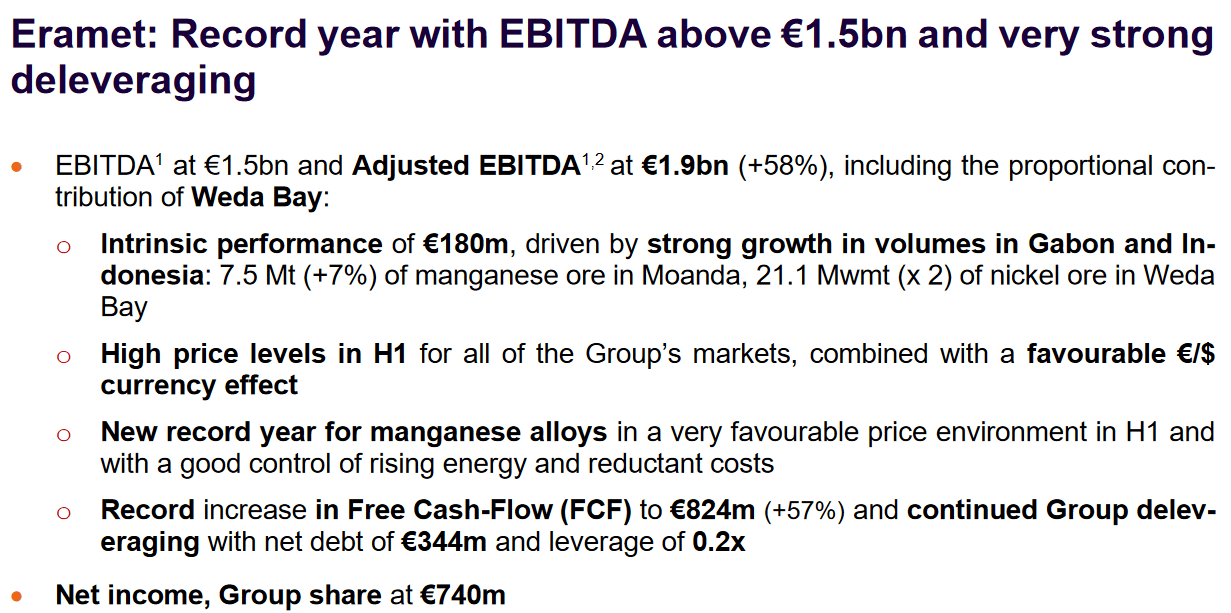

- February 22, 2023 - Eramet: Record year with EBITDA above €1.5bn and very strong deleveraging. 2022 net income was Euro 740m.

{kind=link}

Upcoming Catalysts

The key catalysts are quarterly earnings results and start of production of new projects:

- 2023 - Centenario-Ratones Lithium Project Phase 2 (additional 50,000tpa) Feasibility Study results. FID for Phase 2 by year end 2023.

- Early 2024 - JV 24,000tpa Centenario-Ratones Lithium Project commissioning and ramp by mid-2025.

- 2024 - Eramet's battery recycling project blackmass targeted production. Target to be producing battery materials by 2025-26.

- Early 2026 - Sonic Bay nickel-cobalt project JV to begin subject to FID.

- Late this decade - Geothermal brine JV Project in Alsace France (10,000tpa).

Risks

- A global and/or EV sales slowdown may reduce demand for Eramet's products.

- Production risks.

- New projects risks - Cost blowouts and project start delays, meeting production targets. Technical risks with DLE and cost blowouts with HPAL.

- Partner risks.

- Competition.

- Company risks (management, funding, debt, liquidity and currency risks).

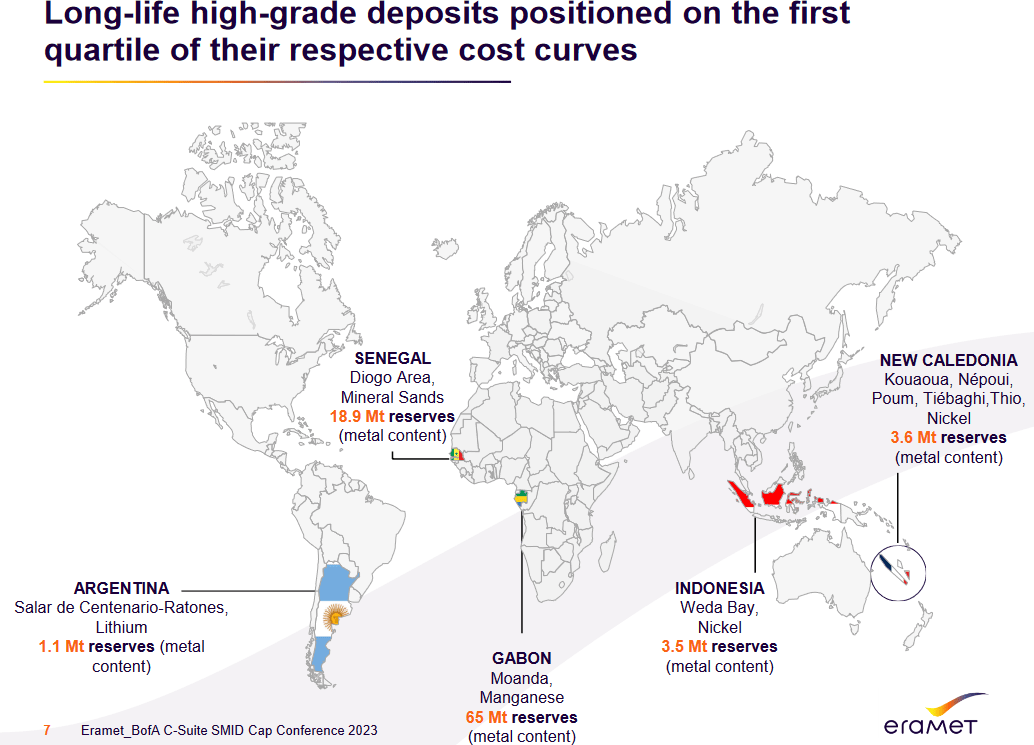

- Sovereign risk - Moderate to high (Gabon, Indonesia, New Caledonia, Senegal, Argentina).

- Supply risks - Some companies may not wish to buy Eramet's products that are sometimes sourced from non ideal countries and methods.

- Stock market risks - Dilution, lack of liquidity, market sentiment.

Further reading

- July 2022 - CATL Will Start Producing LFP Batteries With 15 Percent More Energy, Thanks To Manganese

- Feb. 2023 - Eramet: Record year with EBITDA above €1.5bn and very strong deleveraging.

- Feb. 2023 - Eramet 2022 results company presentation

- March 2023 - Eramet in Argentina Centenario-Ratones Lithium Project

- Eramet: Metals Miner Focused On Decarbonization

Summary of Eramet's global assets (country risk is moderate to high) ( source )

{kind=link}

Eramet is transitioning to becoming a leading battery metals producer ( source )

{kind=link}

Conclusion

Eramet had a great 2022 with record financial results driven mostly by manganese, but also nickel and mineral sands. 2023 may see some pullback if key commodity prices weaken.

Eramet has a strong portfolio of growth projects ahead including moving into the lithium sector as a potential 2024 DLE lithium producer in Argentina, a 2025/26 battery recycling metals producer, and a potential 2026+ nickel-cobalt producer at Sonic Bay. The new Argentina JV Project in particular has potential to significantly move the needle higher for Eramet.

Valuation looks very attractive on a 2024 PE of 4.9. Current consensus analyst rating is a 'buy' with a price target of Euro 150.00, representing 56% potential upside.

Risks are numerous. They revolve around achieving production targets and bringing on new projects (technical risks with DLE, cost blowouts with HPAL), commodity price risks (manganese, nickel, mineral sands, and in time lithium), and moderate to high country risks (Gabon, Indonesia, New Caledonia, Senegal, Argentina). Eramet is currently most exposed to manganese which is mainly use is in the steel industry. The PE may remain low due to the cyclical nature of Eramet's mining business and moderate to high country risks.

We rate Eramet as a well valued buy suited for a 5 year+ time frame.

As usual all comments are welcome.

For further details see:

Eramet Is Transforming To Become A Leading Battery Metals Producer With Manganese, Nickel, And Soon Lithium