ERMAF - Eramet: Metals Miner Focused On Decarbonization

2023-03-10 16:13:22 ET

Summary

- Eramet is France's premier metals & mining player with interests in manganese, nickel and mineral sands.

- The French firm is currently going through a strategic transformation with select investments in battery minerals.

- But the current economic climate may provide headwinds as the firm navigates pivotal moment of strategic change.

Company Introduction

Eramet (ERMAF) is France's leading new age metals and mining player with operations in manganese ore and alloys, nickel ore and mineral sands. The French firm produces ferronickel, high quality alloy steel, manganese alloys, titanium dioxide, high purity pig iron, and zircon.

The €2.7B company has embarked on a strategic journey to be a key player in battery minerals through targeted investments in Latin America's renowned lithium triangle. The company has complimented this operation with battery recycling activities.

Its growing ambitions to become a leading player in the new age of metals are centered on decarbonization and global sustainability, presenting an opportunity for investors to capitalize on a shifting portfolio of projects. The French miner posted annual sales of €5.1B at a 5-year CAGR of 7.5%.

It posted 2022 EBITDA at €1.5B and has seen steady growth driven by favorable pricing structures and progress on Weda Bay, the company's flagship nickel play. The venture continues to put funds to work to deleverage its balance sheet and shore up its finances.

{kind=link}

Eramet aims on embarking upon a strategic transformation underpinned by battery minerals.

Despite the compelling decarbonization focused strategy and a solid portfolio of assets, it is hard to presently get too excited about Eramet. Still reeling from years of lackluster performance at its New Caledonian SNL nickel operation, Eramet faces challenges on several fronts.

Its ambitious foray into lithium comes at a time where multiple projects are coming online, and the world economy is teetering on the brink of a global recession.

The battery electric vehicles industry is starting to show tell tale signs of rolling over and a slowing of the Chinese economy has started to have a widespread impact on commodity prices. We are actively keeping an eye on Eramet but could not rate it an all-out buy right now.

Lithium Prices

Prices for lithium carbonate have shed roughly 40% since the start of the year as dampened consumer sentiment and growing supply start taking its toll. More recently, the Chinese have begun rolling back incentives for battery electric vehicles while automotive demand is starting to show signs of decline.

Output is expected to increase as new projects come online with top producer, Australia, expecting a 30% increase in lithium produced in 2023. Currently, lithium carbonate prices are hovering around the 357k RMB mark ($51K USD)

{kind=link}

Global lithium prices continue to roll over.

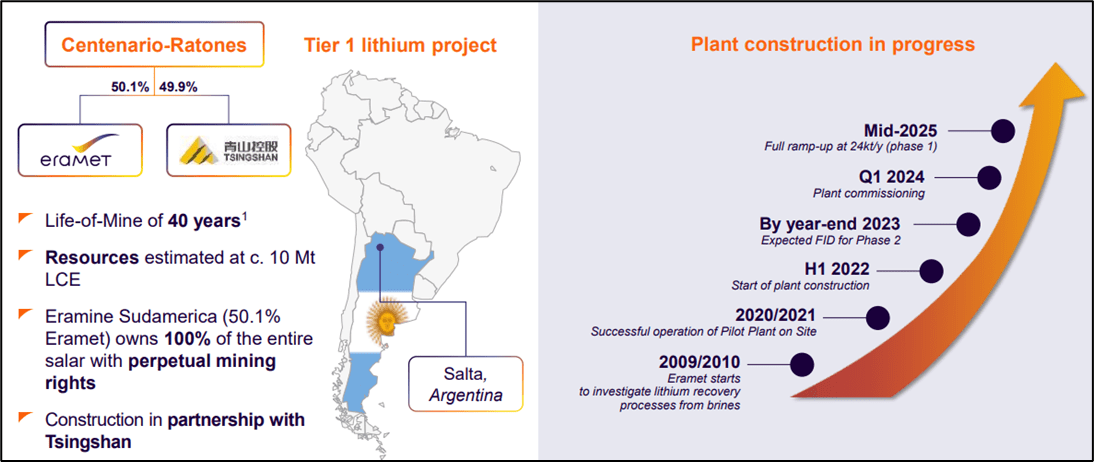

Lithium Business Unit: Centenario Ratones Lithium Project, Argentina

Deeply anchored in South America's prolific lithium triangle, the French miner's nameplate lithium discovery is geared to capitalize on the growing appetite for battery minerals and lithium-ion batteries. With long term consensus pricing for lithium carbonate equivalent nearing $18,000 per ton, the project will swing into action in roughly one year.

Centenario Ratones is a joint venture with Chinese partner, Tsinghshan and boasts resources of circa 10Mt of lithium carbonate equivalent and a life of mine over 40 years. Construction continues to progress with full ramp up planned for mid-2025 (24kt per annum). The company plans on using direct extraction lithium technology which allows enhanced recovery rates, better process efficiency, and reduced water usage.

{kind=link}

Centenario Ratones is an exciting JV between French miner Eramet & Chinese industrialist Tsingshan.

Project capex is expected to total around $550M with $375M financed by Chinese JV partner Tsingshan. Earnings projections at full ramp up will be around $300M assuming a $18k CIF price for each ton of lithium carbonate equivalent produced.

In addition to Eramet's Latin American lithium ambitions, the French miner is partnering with Electricite de Strasbourg to deploy its direct lithium extraction process at an industrial hub in France. The project remains in its infancy with only a memorandum of understanding for lithium development in the Alsace region signed thus far.

Manganese Business Unit: Moanda Manganese Mine, Gabon

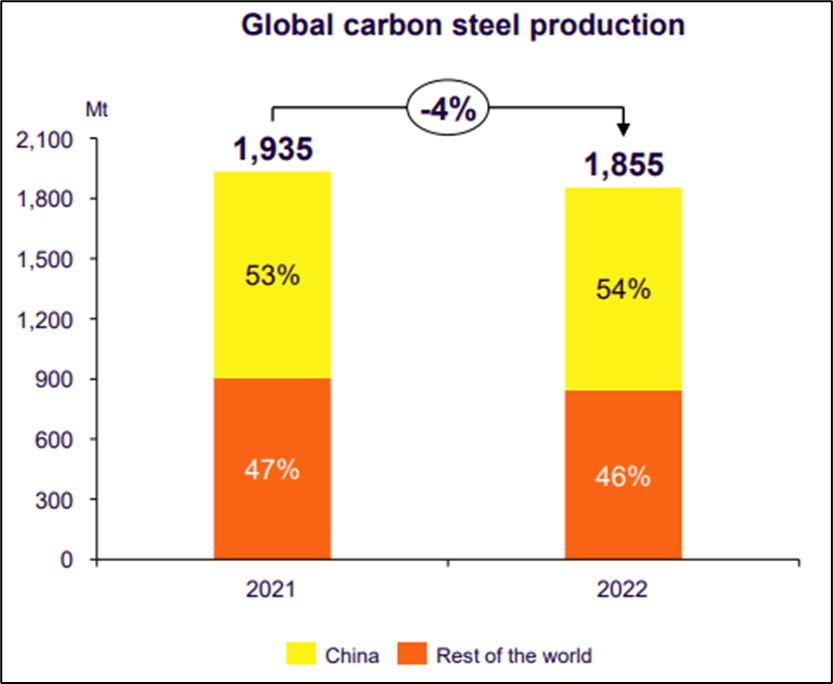

Comilog, a subsidiary of Eramet, operates the Moanda mine in Southeastern Gabon. Strong alloy prices have allowed the company to successfully ramp up production with 7.5Mt produced in 2022 (4.3M in 2018) translating into 1.4B€ in EBITDA. The manganese operation represents the lion's share of the company's free cash flow.

Both the manganese ore and manganese alloys business continue to fire on all cylinders despite some H2 weakness in prices observed in China across manganese and nickel business units. High input costs have dragged on financial performance primarily driven by energy prices.

Input cost inflation is expected to decline somewhat into 2023. It is worth noting the marginal decline in global carbon steel production (~1,855 Mt)

{kind=link}

Global carbon steel production, a major consumer of manganese, has marginally declined.

Nickel Business Unit: Weda Bay, Indonesia & SLN, New Caledonia

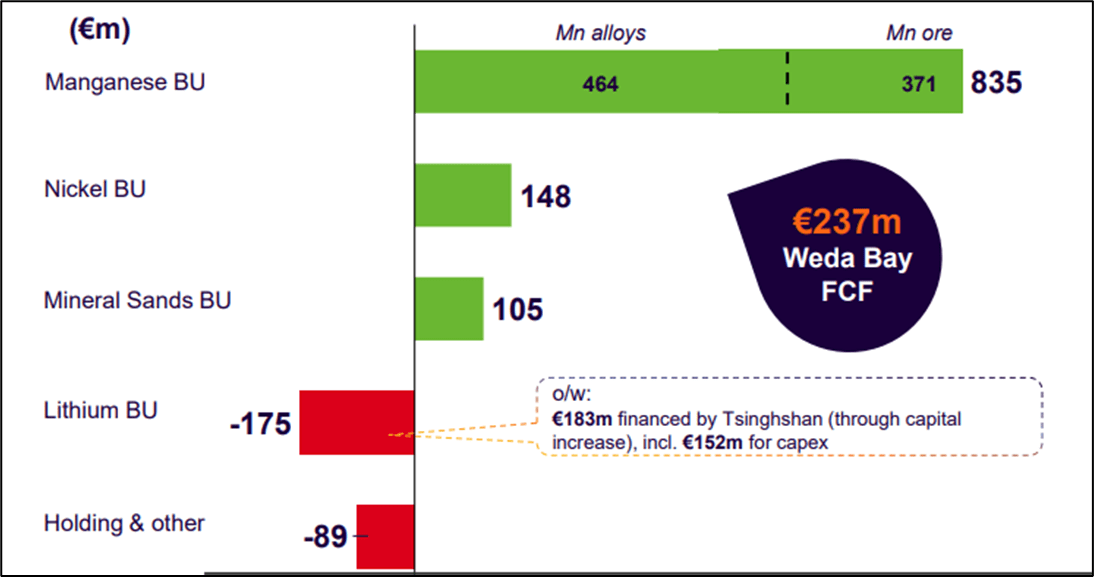

Eramet's operating performance for its nickel division has been a tale of two stories - its Weda Bay, Indonesia operation continues to go from strength to strength, bolstered by a doubling of project specific adjusted EBITDA (from €153M to €344M YOY)

Oppositely, SLN, the company's legacy nickel operation in New Caledonia continues to be mired in operational issues and impacted by weather conditions. The New Caledonian site has been a problem child for the company since inception - project cost overruns, power supply issues, social license challenges and difficulties with the local government have translated into a cash bonfire.

Recently, the French government stepped in to provide the New Caledonian mining company a €40M loan to solve near-term liquidity woes. Competitor Vale experienced similar operational challenges in New Caledonia, ultimately electing to throw in the towel and retreat from its Pacific Island nickel ambitions.

Indonesia's Weda Bay does show real promise with the operation scaling up into strong nickel prices. Price strength has been supported by an insatiable demand for batteries (+37% since 2021) offset by a slowing in stainless steel consumption.

{kind=link}

Nickel demand could be impacted by a slowing of sales of battery electric vehicles and a widespread decline of the global economy.

Sonic Bay, Indonesia

Eramet is working with German chemicals specialist BASF to become a key supplier in the battery value chain. A large scale hydro-metallurgical complex with high pressure acid leach capabilities is currently being considered - its aim is to produce 60k tons per year of battery grade nickel. A final investment decision on the industrial partnership should be finalized in the second half of 2023.

Mineral Sands Business Unit

A favorable price and currency environment has helped Eramet boost zircon and titanium dioxide production in 2022. Demand continued to be resilient despite showing some signs of weakness into the back end of the year.

All in, increasing prices helped the firm post €184M in EBITDA in 2022 (+34% YOY) and flattish free cash flow (€105M at -3% YOY). Higher input costs for titanium dioxide production in Norway and lower mining content for the firm's Senegalese operations did weigh on overall results.

Financials

The company financials have been strong. The analyst community wager on a return to previous all-time highs with 3 holding a buy rating and 1 holding a sell rating. The 12-month average target among analysts following the stock is €145 which is roughly +42% higher than current levels.

Favorable commodity prices have allowed the company to accelerate sales (€5.1B v €3.7B one year earlier) while maintaining a healthy EBITDA margin (~29%) Net income has doubled (€740M vs €298€) providing the opportunity to bolster cash and marketable securities (€1.6B€ vs €1.1B).

Expect tapered sales into 2023 as commodity price pressures ease and the global economy gradually moves into recession. For certain commodities like lithium, the long run environment continues to remain positive offset perhaps by some short-term economic jitters.

{kind=link}

The manganese business continues to be the main driver of cash flows.

Cash flow from operations has doubled for the past 3 years (€300M FY 2020 vs €643M FY 2021 vs €991M FY 2022). This level of growth is likely to equally be impacted by any near-term commodity price volatility.

Goodwill (€200M), other intangibles (€166M) and other long-term assets (€39M) present a risk to valuation should any of the accounting assumptions they were founded on change. Deferred long-term charges have also doubled over the past several years, now totaling €112M. A close eye needs to be kept on what Eramet considers long-term assets along with assumptions regarding valuation.

The company recently rolled some of its debt burden with €398M of long-term debt being repaid and an additional €167M (long-term) and €98M (short-term) being raised consequently. Eramet continues to invest in new projects with €491M deployed in capex during 2022, taking it back to pre-covid levels of capex expenditure.

Eramet remains an extremely lucrative venture (EBTIDA ~29%, return on equity 51%, and 20% return on total capital) and trades at 5.9x forward price to earnings. This puts it in a comparably favorable light to its peer group - Anglo-American (8x NTM), Glencore (6.1x NTM), Boliden (10.8x NTM) and Ferroglobe (8.1x NTM).

Risks

The company's strategic ambition is heaped with risk. It is presently developing a lithium project due to come online in one year at a time when near-term lithium prices are getting hammered. Financial assumptions for the project have helped collateralize risk ($18K/t LCE assumptions with current prices North of $50K/t) but the project is being partially financed by Chinese industrial giant Tsingshan - that spells sizable geo-political risk during the 40-year life of mine.

SLN continues to be Eramet's Achilles heel monopolizing time, efforts, and funds to get right. The company has a political interest in getting the project right given New Caledonia's French colonial history so walking away from the serial loss maker may be a tall ask.

Finally, the company is embarking on a strategic transformation during a time when the global economy may be losing steam - this makes project finance more costly, access to credit more difficult and investor sentiment more skittish.

Key Takeaways

Eramet is France's premier mining and metals player presently embarking on a transformation centered on decarbonization and sustainability. Ambitions include being present along the battery minerals value chain, select investments in lithium, a consolidation of its leadership position in nickel and the development of a battery recycling business.

It all bodes well for a miner benefiting from a commodities boom spurred by inflationary pressures. Yet turbulence in the global economy is likely to make achieving such strategic goals easier said than done and for those reasons, we remain on the sidelines.

For further details see:

Eramet: Metals Miner Focused On Decarbonization