ERC - ERC: Global Fixed Income CEF 10.5% Yield

Summary

- Allspring Multi-Sector Income Fund (ERC) is a global fixed income closed end fund.

- The fund has three main investment buckets consisting of U.S. High Yield, International Sovereign Bonds and U.S. Investment Grade Securities (MBS, IG Bonds, Securitized IG).

- The U.S. High Yield bucket represents two-thirds of the fund followed by Sovereign names at 15%.

- The fund usually trades at a discount to NAV but is currently priced at a premium.

- This article covers CEFs from our suite of products - we focus on macro portfolio allocation, CEFs, and yield-generating options strategies, targeting overall yearly portfolio returns of 9%+.

Thesis

The Allspring Multi-Sector Income Fund ( ERC ) is a fixed income closed end fund. The vehicle falls in the multi-sector asset space and has a global reach. The fund has current income as its main objective and that is reflected in its dividend yield and NAV track record.

The fund usually allocates its assets in three separate "sleeves":

1) High Yield Debt (can be from 30% - 70%). Current allocation is 64%

2) Foreign Securities (can be from 10% - 40%). Current allocation is 14.5%

3) Other U.S. IG Debt (can be from 10% - 30%, includes MBS, Investment Grade Corporate Bonds). Current allocation is 21.5%

Despite its name on the Seeking Alpha platform, the fund is not affiliated with Wells Fargo:

Effective on November 1, 2021, the sale transaction of Wells Fargo Asset Management by Wells Fargo & Company to GTCR LLC and Reverence Capital Partners, L.P. was closed. In connection with the closing of the transaction, Wells Fargo Asset Management became known as Allspring Global Investments (“Allspring”) and various entities that provide services to the Fund changed their names to “Allspring”, including Allspring Funds Management, LLC (formerly Wells Fargo Funds Management, LLC), the adviser to the Fund, Allspring Global Investments, LLC (formerly Wells Capital Management, LLC) and Allspring Global Investments ( UK ) Limited (formerly Wells Fargo Asset Management (International) Limited), both sub-advisers to the Fund. These name changes have been reflected within this report.

Source: 2021 Annual Report

The fund's main risk factor is U.S. High Yield, followed by emerging markets credit spreads. Both risk factors have been pummeled in 2022, with the fund's performance of -16% year to date reflective of that. The vehicle has an unsupported 10.5% dividend yield and a low long term annualized total return which clocks in at around 5%. These returns are obtained with a very low Sharpe of 0.11.

An interesting development occurred after the violent market sell-off in June - the fund for some reason moved from a roughly -8% discount to NAV to a premium to NAV of around 1.4% now. We expect this to reverse. We also expect another leg of the current bear market to develop which is going to result in wider credit spreads and thus lower NAV for ERC. New money entering the space would do well to avoid ERC since its analytics are not compelling. Individuals already in the fund should think about trimming some exposure.

We now rate ERC as a Sell expecting another -10% down in the next months from wider credit spreads and a reversion to a discount to NAV.

Analytics

AUM: $0.284 billion.

Sharpe Ratio: 0.11 (5Y).

St Deviation: 11.5 (5Y).

Yield: 10.5%.

Expense Ratio: 1.19%.

Premium/Discount to NAV: 1.4%.

Z-Stat: 0.32.

Leverage Ratio: 33%.

Risk Factor: U.S. High Yield / International Sovereign

Holdings

The fund is overweight U.S. high yield names:

Holdings (Fund Website)

In terms of credit quality the fund is overweight below investment grade names, both via its High Yield and Sovereign sleeves:

Ratings (Fund Website)

Outside of the Sovereign portfolio the fund is very granular:

Top Holdings (Fund Website)

We can see that the top holdings are mostly the international sovereign bonds, which have been bought with fund weightings above 1%.

Performance

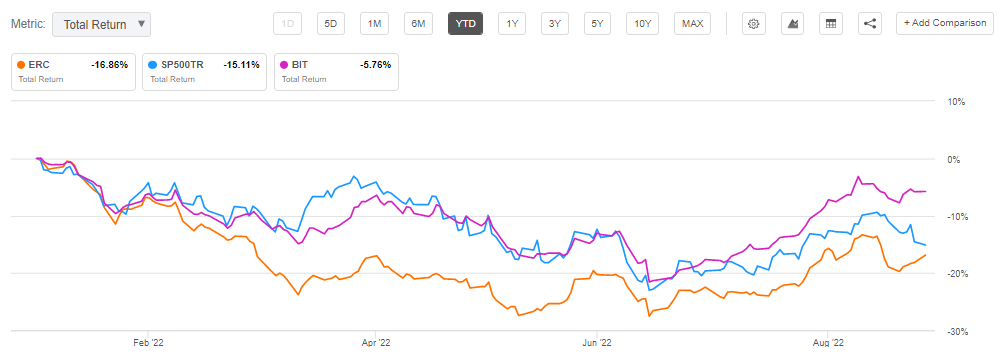

The fund is down over -16% year to date:

{kind=link}

We can see from the above graph that the fund is the worst performer from the cohort, severely lagging both ( BIT ) which is another multi sector fixed income fund and the S&P 500 index.

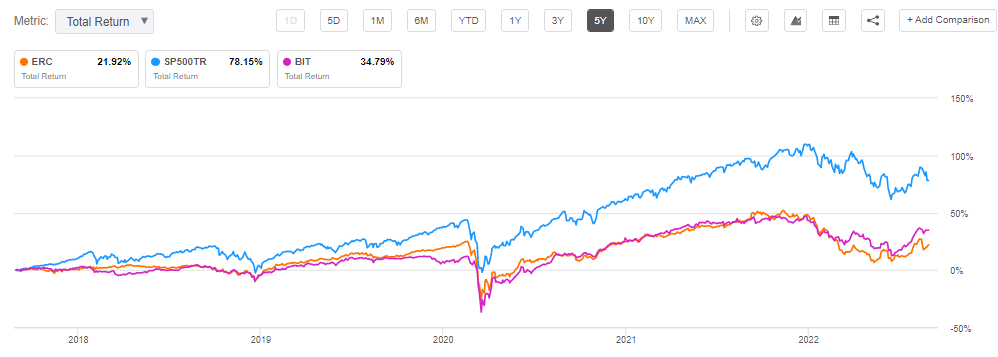

On a 5-year time frame the picture is similar:

{kind=link}

BIT is at the bottom of the performance chart even on a five year basis. Expect long term annualized total returns here closer to 5%:

{kind=link}

Given its substantial annual NAV give-up and trading activities the fund actually provides for a true annual total return closer to 5% as we can see from the above performance chart.

Premium / Discount to NAV

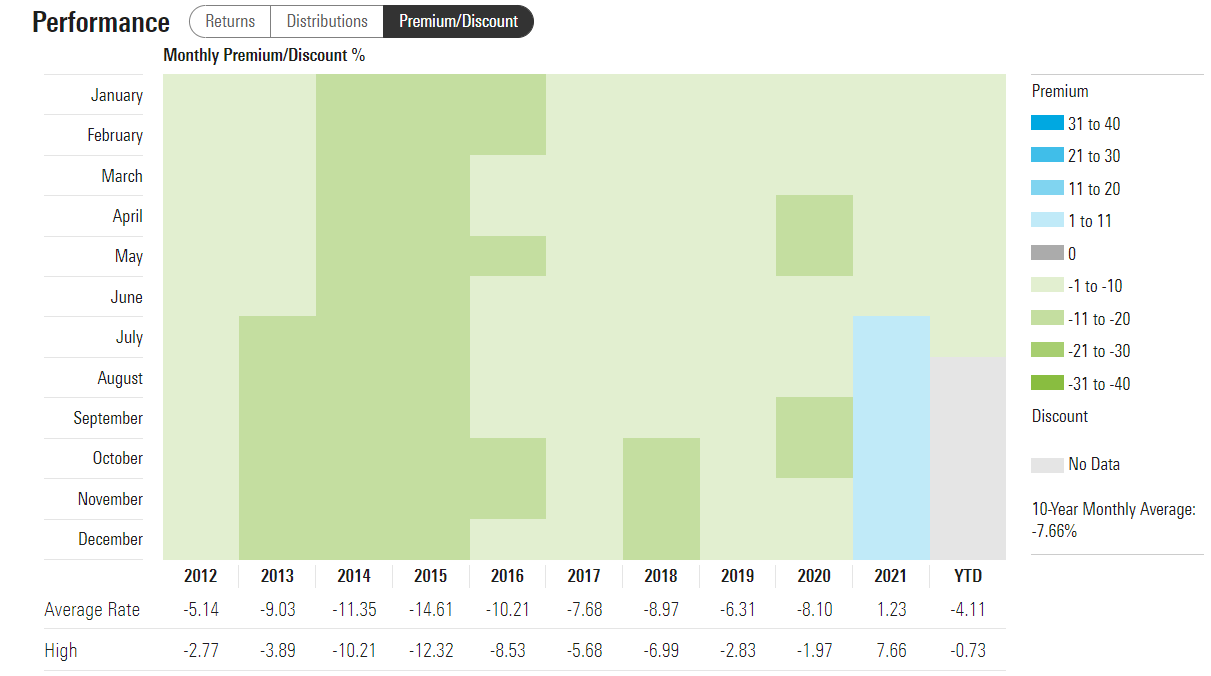

Outside the zero rates 2021 environment the fund has always traded at a discount to NAV:

{kind=link}

We can see that the vehicle usually trades at discounts to NAV of -5% to -10%. During the Fed induced zero rates environment in 2021 the fund traded at a premium to net asset value for the first time in the past decade.

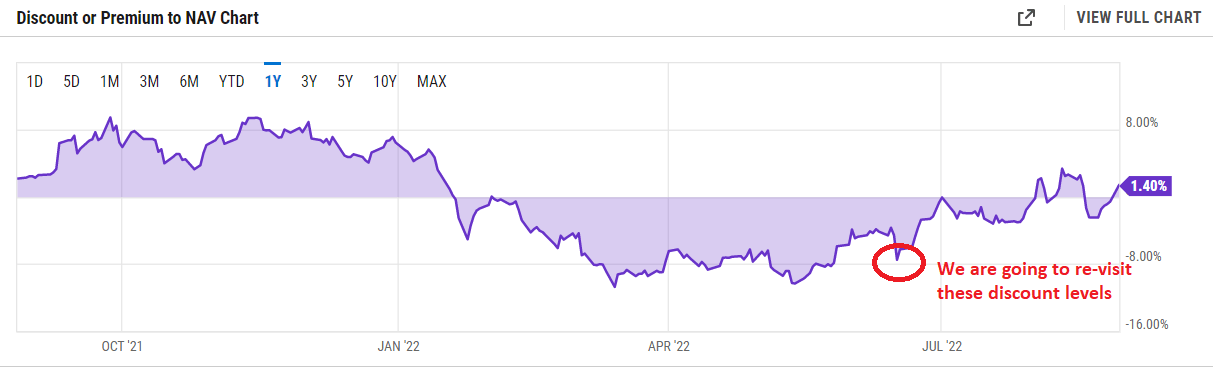

Surprisingly the fund is now trading at a premium to NAV again:

{kind=link}

We can see from the above chart that the fund was trading at substantial discounts to net asset value in the beginning of the year when we saw figures exceeding -8%. Post the July/August market rally we now have the vehicle at a premium to NAV. We do not think this is sustainable or a true reflection of the risk inherent in the underlying assets. We feel we are going to revisit a discount level as the next risk-off move comes along.

Distributions

The fund has a managed distribution plan as outlined in its 2022 Update Release :

Effective with the distribution to be declared in August 2022, the plan will provide for the declaration of monthly distributions to common shareholders of the fund at an annual minimum fixed rate of 8% based on the fund’s average monthly net asset value ( NAV ) per share over the prior 12 months. Under the managed distribution plan, monthly distributions may be sourced from income, paid-in capital, and/or capital gains, if any. Shareholders may elect to reinvest distributions received pursuant to the managed distribution plan in the fund under the existing dividend reinvestment plan, which is described in the fund’s shareholder reports.

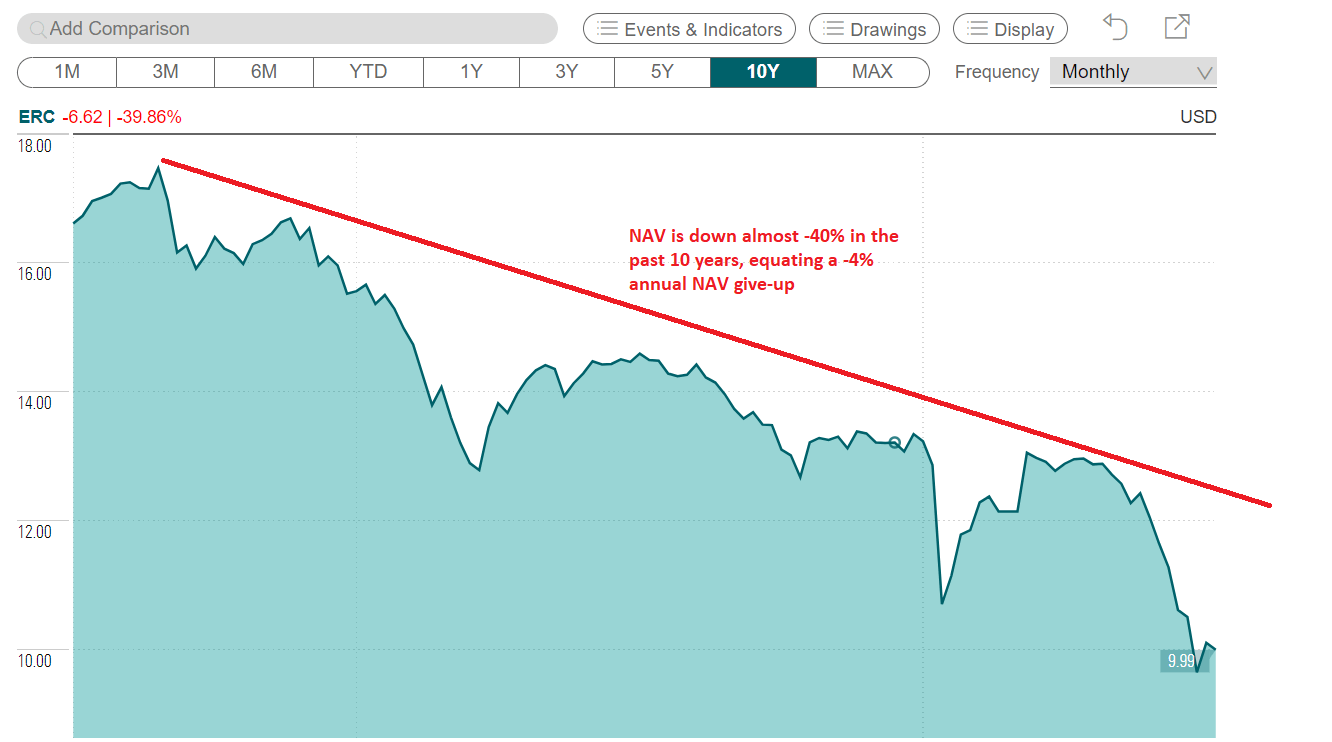

To note that the fund has a 9% target distribution rate until the August 2022 changes. We could not find public Section 19a notices for ERC, so we took a look at its NAV performance in the past decade:

{kind=link}

We can infer from the fund's NAV performance that it overdistributes. For fixed income CEF's vehicles which exhibit a stable NAV over long periods of time are the ones who disburse what they make. A CEF is a vehicle that employs leverage to juice up the underlying yields and offer investors a higher distribution. When that distribution does not come from cash flows but from return of capital (i.e. ROC) we always see substantial NAV erosions through time because there is less and less capital available in the fund. This is the case here.

Conclusion

The Allspring Multi-Sector Income Fund ( ERC ) is a fixed income closed end fund falling in the multi-sector asset space. The fund has three main investment buckets consisting of U.S. High Yield, International Sovereign Bonds and U.S. Investment Grade Securities (MBS, IG Bonds, Securitized IG). The U.S. High Yield bucket represents two-thirds of the fund followed by Sovereign names at 15%. The fund has a 10.5% dividend yield but it is unsupported. A retail investor should expect something closer to a 5% annualized total return here. The fund usually trades at a discount to NAV but is currently priced at a premium. We expect this to mean revert during the next risk-off leg in what we consider a bear market. We now rate ERC as a Sell expecting another -10% down in the next months from wider credit spreads and a reversion to a discount to NAV.

For further details see:

ERC: Global Fixed Income CEF, 10.5% Yield