SRE - ERH: Some Concerns About The Distribution But Otherwise A Good CEF

Summary

- Utilities have long been a favorite asset class of conservative investors due to their financial stability and high yields.

- Allspring Utilities and High Income Fund invests in a portfolio of both utilities and high-yield bonds, which works pretty well for both high income and a degree of safety.

- The closed-end fund is a bit heavily weighted towards one company, but it is reasonably diversified overall.

- The distribution does not appear to be sustainable and may need to be cut in the near future.

- The valuation is reasonable, but investors may want to wait a bit until we get more clarity on the distribution.

For a very long time, utilities have been among the favorite investments of conservative investors, such as most retirees. There are some very good reasons for this, including the fact that utilities tend to be very financially stable and have fairly high dividend yields. However, the very high valuations in today’s market have caused even these stalwarts to have fairly low yields. In fact, the U.S. Utilities Index ( IDU ) only has a 2.36% yield as of the time of writing. At that yield, even a $1 million portfolio would only generate $23,600 in annual income, which is nowhere close to enough to support the lifestyle of anyone with the wherewithal to amass a portfolio of that size.

Fortunately, there are some ways to invest in utilities in today’s environment and still get a respectable yield. One of the best of these methods is to purchase shares of a closed-end fund ("CEF") that invests in the utility sector. These funds are not particularly well followed in the market, but they provide easy access to a diversified portfolio of utility securities that can typically pay out a much higher yield than any of the companies actually possess.

In this article, we will discuss the Allspring Utilities and High Income Fund ( ERH ), which is one such CEF that falls into this category. As of the time of writing, this fund boasts a 7.70% yield, which kicks the income from our $1 million portfolio up to $77,000 annually, which is much closer to the level that is needed to enjoy a comfortable lifestyle in most areas of the country. This is admittedly at the low end of the yields that we typically target here at Energy Profits in Dividends but it should still be attractive enough to be appealing. This fund offers more than just a respectable yield, though, as it also boasts a very attractive valuation at the current price.

Therefore, let us investigate and see if the Allspring Utilities and High Income Fund could be a good addition to your portfolio.

About The Fund

According to the fund’s webpage , the Allspring Utilities and High Income Fund has the stated objective of providing investors with a high level of current income, but only moderate capital appreciation. This is not particularly surprising for a utility fund, since the companies in this sector do not typically grow particularly fast. In fact, as I pointed out in a recent article , it is quite rare for a utility to deliver a total return above 11% and 6% to 8% earnings growth is a relatively high target for the sector.

This is mostly because most people already have utility services and populations in the United States do not grow particularly quickly. This is one reason why utility stocks tend to be among the highest-yielding sectors as their low growth rates do not often result in especially high valuations. This fund does not solely invest in utilities, though. In fact, the fund states that it will invest about 30% of its assets into high-yield debt (“junk bonds”). Fixed-income securities in general only offer very limited potential for capital appreciation so the presence of these securities in the portfolio will further decrease the fund’s potential for capital gains. Thus, we should not expect much in the way of capital gains, but even if the fund’s market price remains relatively stable, the yield is sufficient to ensure us a decent return on our invested capital.

As many of my readers are likely aware, I have spent a great deal of time over the past few years discussing utility stocks on Seeking Alpha. I admittedly do not discuss them very much here at Energy Profits in Dividends due to their yields being too low for our purposes, but I imagine that many people read my work on both services. As such, most of the largest positions in the fund’s portfolio are going to be somewhat familiar. Here they are:

CEF Connect

I have discussed many of these companies a few times over the years, although admittedly not all of them. I have never discussed Sempra Energy ( SRE ), Duke Energy ( DUK ), Southern Company ( SO ), Dominion Energy ( D ), or Xcel Energy ( XEL ). However, these are among the largest utilities in the United States and many of them may even be your utility company so information should not be hard to find. On a somewhat humorous note, if any of these are your utility then an investment in the fund is sort of like getting a pretty large discount on your own power bill!

One thing that we do see here is that quite a few of these utilities are leaders in the deployment of renewable energy solutions. For example, NextEra Energy ( NEE ) is among the largest developers of renewable generation capacity in the country, and both American Electric Power ( AEP ) and DTE Energy ( DTE ) have devoted considerable resources to green energy conversion. As we have discussed in various previous articles, the “green energy” trend is not likely to be nearly as strong as politicians or media activists want you to believe but it is still important to have some money allocated to this sector of the energy economy as it is likely to be a major source of growth going forward. Indeed, as I pointed out in a recent article , the global demand for renewable energy is likely to grow by 345% over the next two decades, which is more than the projected demand growth for any conventional fuel. The fact that this fund will provide some exposure to this is, therefore, quite nice to see.

As my long-term readers on the topic of closed-end funds are likely well aware, I do not generally like to see any individual asset in a fund account for more than 5% of the fund’s portfolio. This is because this is approximately the point at which that asset begins to expose the fund to idiosyncratic risk. Idiosyncratic, or company-specific, risk is that risk that any asset possesses that is independent of the market as a whole. This is the risk that we aim to eliminate through diversification but if the asset accounts for too much of the portfolio, then this risk will not be completely eliminated. Thus, the concern is that some event will occur that causes the price of a given asset to decline when the market as a whole does not, and if that asset accounts for too much of the portfolio, then it may end up dragging the entire fund down with it. As we can see above, only NextEra Energy accounts for an outsized proportion of the portfolio. This is something that would have been a very serious concern about two years ago because the stock looked dramatically overpriced at the start of 2021 but it has since come back to earth and now possesses a very reasonable price relative to its peers. We can see this by looking at the price-to-earnings growth ratios for the top holdings in the fund:

| Company |

| PEG Ratio |

| NextEra Energy |

| 2.82 |

| Sempra Energy |

| 3.14 |

| Duke Energy |

| 3.40 |

| American Electric Power Company |

| 2.96 |

| Southern Company |

| 4.72 |

(All data courtesy of Zacks Investment Research.)

Thus, the huge weighting towards NextEra Energy is not as big of a concern as it once was due to the stock’s reasonable valuation. However, it would still be preferable to see the fund pare down this position somewhat and use the money to add another company or two to the portfolio.

Earlier in the article, I stated that the Allspring Utilities and High Income Fund aims to only invest 70% of its assets into the utility sector with the remainder allocated to high-yield bonds. It currently has slightly more than 30% in bonds, however:

CEF Connect

At first glance, the fund appears to be allocating more to bonds than it is supposed to. With that said, the fact that bonds account for only 46 basis points above its official objective is something of a rounding error and so not really a big deal. We also have the possibility that some of those bonds are actually utilities. The fund does directly state that 70% of its portfolio will be invested in common equities, preferred equities, and bonds issued by utility companies. Thus, if even a handful of those bonds are issued by utilities, then it easily brings the fund back in line with its mandate. The fund does not disclose exactly what percentage of its bond holdings are issued by companies in a given sector. We do know that the common stocks are all utilities, though.

Overall, the allocation to bonds could be somewhat attractive to more risk-averse investors, who are likely to be the biggest investors in a fund like this. This is due to the fact that bonds are generally less volatile than common stocks. The reason for this is obviously the fact that bonds do not have a direct correlation to the financial performance of the company itself unless the company is considered to be at a high risk of defaulting. After all, bond payments do not vary depending on the financial performance of the company issuing them. Rather, the company must make its bond payments in order to remain solvent. In addition to this, bond yields tend to be somewhat higher than even utility common equities. Thus, the presence of the bonds in the portfolio should reduce the volatility of the fund and boost its income somewhat. We can appreciate this for obvious reasons.

As already mentioned though, the bonds in the portfolio are high-yield bonds. These are colloquially called “junk bonds,” and may be a point of concern for some investors. This is due to the fact that these bonds are generally perceived to be at a fairly high risk of default. Fortunately, this may not really be the case. We can see this by looking at the credit ratings of the bonds in the portfolio. These are letter-grade ratings that are assigned by the major rating agencies (Standard & Poor's, Moody’s, and Fitch) that theoretically tell us the likelihood of an issuing company defaulting on a given bond issue. Here is a high-level summary of the bonds that comprise the entire portfolio:

CEF Connect

An investment-grade bond is anything rated BBB or above, which as we can see comprises only a negligible portion of the fund’s bond allocation. However, 87.40% of the portfolio’s bonds are rated either BB or B. These are the two highest ratings for speculative-grade bonds and as such are quite nice to see. This is because these securities are at a fairly low risk of default. According to the official bond ratings scale , a company whose bonds have one of these two ratings has the financial capacity to meet its current obligations, although it may strain more than an investment-grade company in the event of a prolonged economic shock. Thus, the overall risk of these bonds is probably pretty low and we should not really have to worry too much about them.

Thus, the fund’s portfolio is probably safe and secure enough for most investors, although I would still like to see that huge allocation to NextEra Energy reduced.

Leverage

Earlier in this article, I stated that closed-end funds can frequently use certain strategies to generate a higher yield than any of the underlying assets possess. One of the ways through which it does this is the use of leverage. In short, the fund borrows money and uses that money to buy shares of utilities and junk bonds. As long as the returns that it receives from the purchased assets are greater than the interest rate that it pays on the borrowed money, the strategy works pretty well to boost the overall returns of the portfolio. The fund can then pay out the capital gains and extra dividends and bond payments to the investors, resulting in a higher yield than it could otherwise accomplish. As the fund can borrow at institutional rates, which are considerably cheaper than retail rates, this will usually be the case.

However, the use of debt is a double-edged sword because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much debt because that would expose us to too much risk. I generally do not like to see a fund’s leverage above a third as a percentage of its assets for this reason. Fortunately, the Allspring Utilities and High Income Fund satisfies that requirement as its levered assets currently comprise 20.57% of the fund’s portfolio. This is a very reasonable ratio that is lower than many other funds. Therefore, there might be some room here for the fund to increase its leverage. Overall, though, it is striking a pretty good balance between risk and reward.

Distribution Analysis

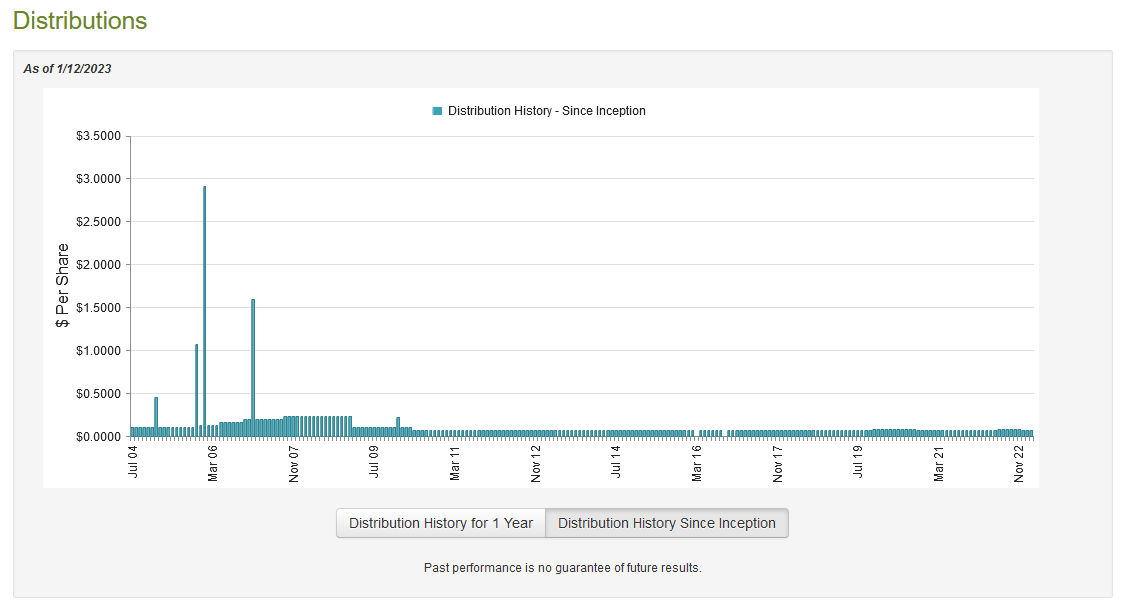

As stated earlier in this article, one of the reasons why investors purchase utilities is because of the high yields that the stocks possess. This is because these companies have fairly low growth rates and so endeavor to deliver a larger proportion of their total investment return through direct payments to the stockholders. As the fund invests in a levered portfolio of both utilities and high-yield bonds, which are by their very nature high-yielding entities, we might assume that the Allspring Utilities and High Income Fund boasts a similarly high yield. This is certainly true as the fund pays out a monthly distribution of $0.0744 ($0.8928 per share annually), which gives it a 7.70% yield at the current price. The fund has strived to be generally consistent with this distribution over the years, although it has fluctuated a lot over the past twelve months:

{kind=link}

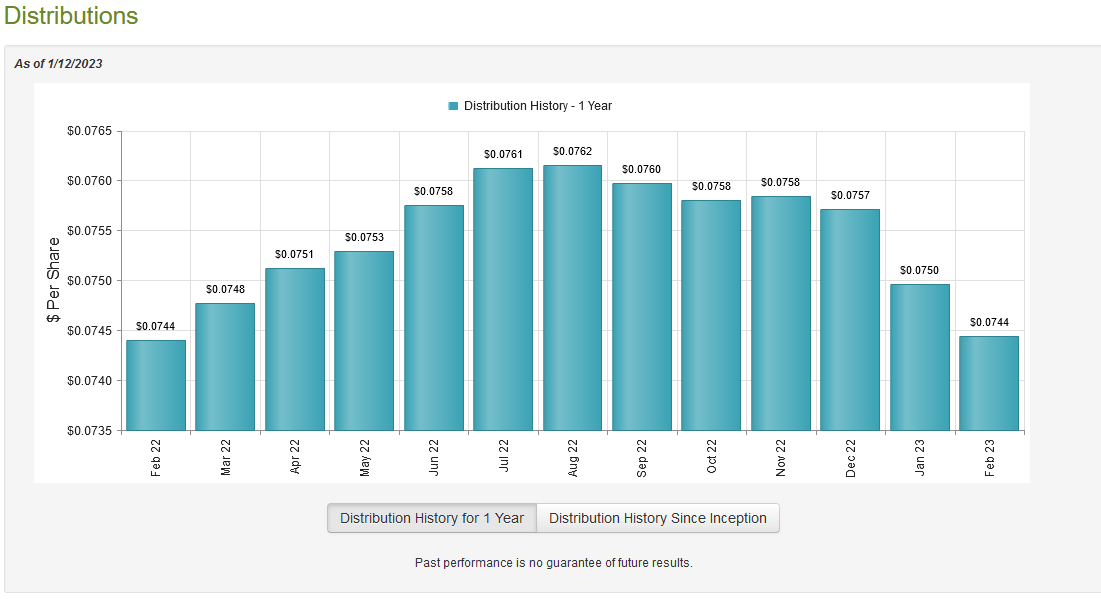

Here is the distribution history over the past twelve months, to give a better view of how much it has varied recently:

{kind=link}

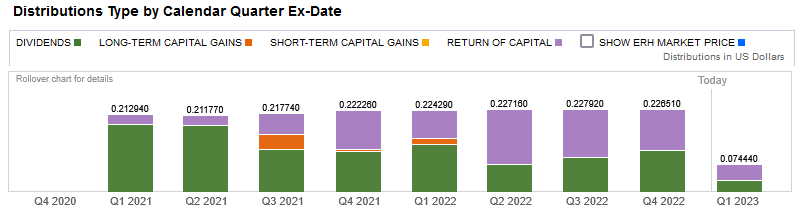

This is something that may prove to be a bit of a turnoff for those investors that desire a stable and secure source of income to use to pay their bills, even though the fund did pay out the same amount during both the starting and ending months of the period and was remarkably stable over a longer term period. In recent quarters, the fund has also made a large number of return of capital distributions, which is something else that may be concerning for some readers:

{kind=link}

The reason that this may be concerning is that a return of capital distribution can be a sign that the fund is returning the investors’ own money back to them. This is obviously not sustainable over any sort of extended period. However, there are other things that can cause a distribution to be classified as a return of capital, such as the distribution of unrealized capital gains. Thus, we should investigate exactly how the fund is financing its distributions in order to determine how sustainable they are likely to be.

Fortunately, we do have a reasonably current document that we can consult for this purpose. The fund’s most recent financial report corresponds to the full-year period ending August 31, 2022. Although this report will not include any information from the past few months, it is still more recent than many other funds have provided us. The Federal Reserve started to tighten monetary policy in March 2022, which was the event that caused all the market weakness during the year. This report is almost perfectly dated to show us how well the fund handled both the formerly loose policy and the first few rounds of tightening, which is very nice to see. During the full-year period, the Allspring Utilities and High Income Fund received a total of $2,839,532 in dividends and another $2,679,890 in interest from the securities in its portfolio. When we combine that with a small amount of income from other sources, the fund brought in a total of $5,530,451 during the period. It paid its bills out of this amount, leaving it with $4,028,760 available for investors. Unfortunately, this was not nearly enough to cover the $8,351,359 that the fund actually paid out in distributions during the period. At first glance, this is something that will likely be quite concerning.

However, there are other ways that the fund can obtain the money that it needs to pay its distributions. For example, it can pay out any capital gains that it managed to generate. The fund certainly had some success at this over the year. While it did have net realized losses of $94,809, this was more than offset by net unrealized capital gains of $858,474. While the capital gains are nice, the fund still paid out more than it managed to earn and its assets decreased by $3,450,102 during the period. This is very concerning as the fund failed to cover its distributions, which is not sustainable over time. It is somewhat unlikely that it managed to fix this problem in the last few months given the conditions in the market so the fund is probably still overdistributing. It may therefore be forced to cut the distribution in the near future. Investors are therefore advised to be cautious.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the Allspring Utilities and High Income Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all of the fund’s assets minus any outstanding debt. This is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund’s assets for less than they are actually worth. That is certainly the case with this fund today. As of January 12, 2023 (the most recent date for which data is currently available), the Allspring Utilities and High Income Fund has a net asset value of $12.35 per share but the fund’s shares actually trade for $11.60 per share. This gives the shares a 6.07% discount at the current price. This is a reasonable price but it is not nearly as attractive as the 7.21% discount that the shares have possessed on average over the past month. It might be worth waiting to see if a more attractive price soon becomes available, especially since it appears that the fund cannot sustain its current distribution.

Conclusion

In conclusion, the Allspring Utilities and High Income Fund looks pretty attractive for most risk-averse investors on the surface. The fund has a good strategy of investing in reasonably safe utilities and high-yield bonds, although the portfolio is overly weighted towards NextEra Energy. The fund is also quite conservative with its leverage but still manages to boast a respectable yield. The fund also has a pretty attractive valuation at the current price. Unfortunately, it appears to be struggling to maintain the current distribution and may have to cut soon. It thus may make sense to wait a bit until the fund cuts the distribution or fixes its financial problems before buying. Other than that, Allspring Utilities and High Income Fund looks like a pretty good fund for most people.

For further details see:

ERH: Some Concerns About The Distribution But Otherwise A Good CEF