ERO - Ero Copper: Strong Prospects But Shares May Become Cheaper

2023-06-07 12:56:14 ET

Summary

- Ero Copper Corp. has attractive growth potential but could face near-term challenges due to an expected recession weighing on copper demand.

- The company's share price is likely to be negatively impacted by the recession, but this could create a more attractive entry point for investors.

- Ero's growth plans include doubling annual copper production and increasing gold production, making the company an attractive investment for exposure to both markets.

Ero Copper Corp. Earns a Hold Rating for Now

My analysis supports a Hold rating for Ero Copper Corp. ( ERO ) ( ERO:CA ) as I believe more attractive share prices are likely to form than the current ones.

This Canadian copper and gold producer promises a significant improvement in its mining activity later this year. But things might not turn out well for copper, one of the commodities the company trades.

Demand for copper is likely to be dampened by the likely recession later this year and that doesn't bode well for Ero Copper as its business is heavily dependent on the base metal. Thus, despite the operational improvement, the positive impact on the company's balance sheet could remain largely muted. However, this could lead to the formation of a cheaper share price than the current one and create an opportunity to increase exposure to this copper operator with promising growth prospects by spending less.

Ero Copper and Its Metals

Also, since there is a clear positive relationship between ERO stock price and the development of the copper price in the market of futures contracts, I think that, if the metal deviates significantly from its current price level as analysts expect, the stock price will come under negative pressure.

As of this writing, copper futures expiring in July 2023 (HGN3) are trading at $3.7595 per pound and analysts expect copper prices to fall to $3.64 per pound towards the end of the current quarter and then further down to $3.41 a pound by this time next year.

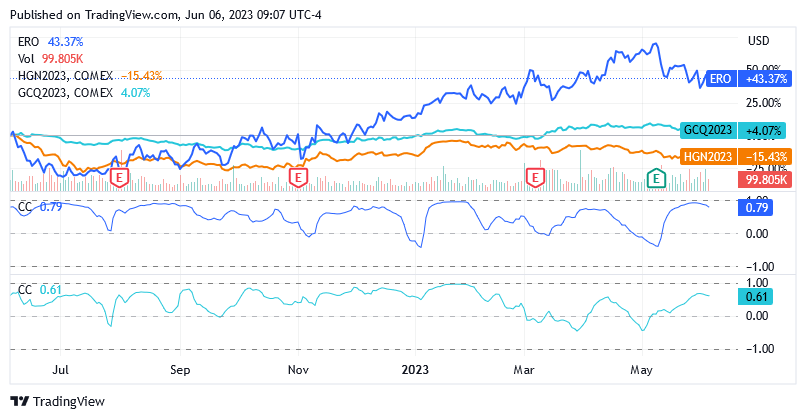

The chart below shows the positive correlation between ERO and Copper Futures - Jul 2023 (HGN3), as the correlation coefficient [CC] curve develops almost exclusively in the upper portion of the chart, i.e., above the zero line.

{kind=link}

Source: Seeking Alpha

It's also been a while since the positive correlation is also very strong. Now the index has a very high reading of 0.79 compared to the -1.00 to +1.00 range.

The correlation between ERO and the price of gold, represented in this analysis by gold futures with maturities in August 2023 (GCQ3), is quite strong and positive too, and gold is likely to rise amid recession headwinds.

While I believe the recession will not have a positive effect on copper demand, it should instead reinforce gold's safe haven status to counter the bearish market sentiment likely to emerge as investors become more risk-averse in a weak economy.

No doubt a potential bull market in gold prices will bode well for Ero Copper Corp's profitability. However, weaker copper is unlikely to be fully offset, as more than 80% of the company's operating cash flow comes from red metal production and trading.

How Copper and Gold Businesses Are Performing at Ero

During the first quarter of 2023, the company produced 9,327 tons of copper or 20.6 million pounds of copper concentrates at a C1 cash cost of $1.70 per pound of metal produced.

In the gold segment, a production record of 12,443 ounces was achieved, resulting in a C1 cash cost of $436 and an all-in-sustaining cost [AISC] of $946 per ounce.

Ero Copper Corp operates its metals business in Brazil. Specifically, in the Curaçá Valley in the northeastern state of Bahia, Ero Copper Corp produces and sells copper concentrate as a result of the exploitation of the Caraíba mineral deposit.

The Caraíba mineral deposit has measured and indicated copper reserves of 1.018 million tons of copper with a grade of 1.46% underground and 283,000 tons of copper with a grade of 0.59% in open pits. At the end of December 2022, approximately 55% of the underground copper resources were in the upper category of proven and probable reserves, while approximately 83% of the open pit copper resources were in the upper category of proven and probable reserves.

Ero Copper Corp indirectly owns the Caraíba mineral property, as the Canadian operator holds a 99.6% interest in Mineracao Caraiba SA, the sole owner of the Caraiba business.

Despite the higher ore volume processed, grade deterioration impacted copper production volumes in Q1 2023, which decreased 26.3% sequentially and 4.7% year-on-year. C1 cash cost of produced copper per pound was also impacted by this negative operating momentum as it increased 20.6% sequentially and 29.8% year-on-year to reach $1.70 in Q1 2023.

Ero Copper Corp produces gold in Mato Grosso from a mine located approximately 400 miles from the city of Cuiaba. These operations are called Xavantina Operations and are exploited by Ero Copper Corp through its 97.6% interest in NX Gold S.A., the owner of the gold operations.

Xavantina Operations has a total of 436,400 ounces of gold which are contained in measured and indicated resources grading 10.73 grams of gold per ton of mineral. Approximately 83% of these resources were proven and probable reserves.

Gold production, on the other hand, fared better as production increased both sequentially by 5.6% and year-on-year by 41.5% while costs decreased, likely thanks to better gold grade as the mineral material processed was significantly lower. C1 cash costs per ounce of gold produced decreased 2% sequentially and 31.7% year-on-year. AISC per ounce of gold produced decreased 13.7% sequentially and 13.4% year-on-year.

What to Expect in the Near Future

Ero Copper Corp. is a very interesting player to take a position with a longer time horizon. The operation is on track to double annual copper production to 100,000 tonnes in two years.

The company could then expand its presence in the copper market and benefit from a robust long-term outlook for the copper demand. The latter is likely to gain momentum over the years as copper is a key product in the transition to renewable resources to reduce dependence on fossil fuels.

But the company will also increase its exposure to gold price trends by aiming to increase sustainable production to 55,000 to 60,000 ounces of gold per year by 2024. As such, it will benefit from higher gold prices, which are becoming increasingly likely in a global context where heightening geopolitical tensions will reinforce the precious metal's safe-haven properties.

The company wants to meet production targets with two major growth projects, the Tucumã Project, and the Pilar Mine project. These were 20%-30% complete in the first quarter of 2023 and are therefore on track to meet targets on schedule.

Located in the southeastern state of Pará, Brazil, the Tucumã Project is expected to yield 27,170 tonnes of copper per year at a C1 cash cost of $1.36 per pound over an initial mine life of 12 years. Whilst the ongoing expansion of the Pilar mine at Caraíba aims to provide logistical support for sustained annual ‘ore’ production well in excess of 3 million tonnes.

Currently, these projects cost no more than originally estimated and the company can always rely on a fairly solid financial position if needed. As of March 30, 2023, net debt was $174.2 million, a slight increase compared to previous quarters. However, an Altman Z-Score of 2.47 and an Interest Coverage Ratio of 4.7 indicate a very low probability of bankruptcy, while the company can very easily afford the financial cost of the outstanding debt. The Interest Coverage Ratio is calculated based on a 12-month operating income of $102.6 million (numerator) and a 12-month interest expense of $21.9 million (denominator).

The Stock Valuation

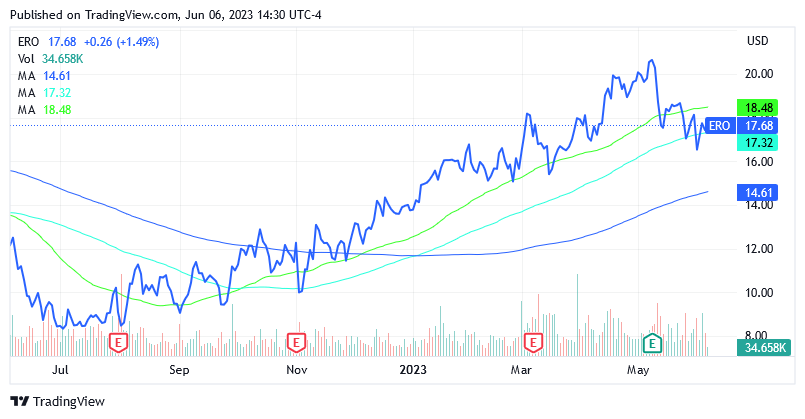

The stock price was $17.68 per share, which translates to a market cap of $1.64 billion at the time of writing. Current stock price levels could present an opportunity to participate in the above production improvements while paying significantly less than a few weeks ago.

Currently, shares are well below the 50-day simple moving average of $18.48 and at the level of the 100-day simple moving average of $17.32. The stock has a 52 Week Range of $8.07 to $20.99.

{kind=link}

Source: Seeking Alpha

Ero Copper Corp. [ERO:CA] also trades on the Toronto Stock Exchange and shares changed hands at 23.54 versus the 50-day moving average of 24.96 and the 200-day moving average of 19.74. The 52-week range is between 10.54 and 28.05.

How the Stock Price Might React to Evolving Macroeconomic Conditions

I expect these prices to settle down over the next few weeks due to the effects of the recession, which is certainly not positive for the price of copper, which the Ero Copper business is almost entirely exposed to.

The economies of the developed world are expected to enter a recessionary phase as central banks have tightened monetary policy to combat high inflation.

In this regard, some economic indicators are already showing signs of a slowdown in economic activity and are expected to gain momentum as the rate hikes implemented so far continue to impact consumption and investment. In addition, further rate hikes by the US Federal Reserve may be required after the expected pause at its next meeting on June 14 as long as robust labor market conditions allow core inflation to be resilient.

Recession fears are also looming in Europe, where the ECB appears determined to keep interest rates at restrictive levels as inflationary pressures are still seen as too high compared to the commitment to bring them back to an annual rate of 2%.

As for recent signals from some economic indicators that could predict the next trend in copper prices, the S&P Global US Composite PMI reading of 54.3 in May 2023 pointed to a weaker recovery in manufacturing activity. Factory orders are also declining, and one of these negative trends, in particular, is the decrease in orders for computer and electronics products, as well as electrical equipment, appliances, and other products and components that predominantly use copper in their production.

A lower share price for Ero Copper stock presents an opportunity to increase exposure to the copper market and to some extent the gold market, through a company that is on track to achieve significant growth targets in a few years at most.

The Risk of Not Buying Today

There is a risk that the share price will not be more attractive than the current one, despite the recessionary headwinds. In fact, in the case of Ero Copper, the stock market could place more positive weight on operational improvements, which will be particularly noticeable in the second half of 2023 after the start-up of the new ball mill at Caraíba Operations and the start of mining of a new vein at Xavantina Operations.

With the addition of these mining assets, Ero Copper anticipates that annual copper production for the full year 2023 will be between 44,000 and 47,000 tonnes, resulting in lower costs than in the first quarter of 2023. This operational guidance implies quarterly copper production of 11,560 to 12,560 tons of metal (vs. 9,327 tons in Q1 2023) at a C1 cash cost of $1.40 to $1.60 per pound of copper produced (vs. $1.70 in Q1 2023) for the remaining quarters of 2023 with a higher degree of confidence in the estimate moving into the second half of the current year.

However, it should also be taken into account that this may not be enough if the copper price does not support operational activities. Indeed, as reflected in operating and financial results for Q1 2023, Ero Copper was able to maintain profitability afloat despite a sharp reduction in production by 26 3% and a sharp 20.6% increase in C1 cash costs per pound thanks to higher average copper price ($4.08 in Q1 2023 vs. $3.64 in Q4 2022). The intertwining of production, price and cost trends was reflected in an EBITDA margin of 51.3% in Q1 2023 compared to 50.3% in Q4 2022.

Operating cash flow for the first quarter of 2023 decreased to $16.4 million from $34 million in the fourth quarter of 2022, primarily due to the application of a $15 million outflow from the ‘Changes In Accounts Payable’ item. Because when it came to net income, this was $24.2 million in Q1 2023, up, albeit slightly, from the net income of $22.2 million in the prior quarter.

So the next copper price will be very important.

As the recession approaches, analysts expect the price of the base metal to weaken, and the stock is unlikely to escape unscathed due to a clear positive correlation between the two assets.

Risk Quantification

The recession is also influencing sentiment among analysts at Trading Economics, who expect the stock market to decline over the next 12 months. This is reflected in their estimates of the US stock market index [US30]. Compared to the current price of $33,503, analysts are estimating a price target of $32,783.64 by the end of the second quarter of 2023 and a price target of $30,011.72 in about a year.

I believe that the expected bearish sentiment in the stock market will significantly reduce the risk of a strong recovery in Ero Copper stock price as Seeking Alpha assigns Ero Copper stock a 24-month beta of 2.06. That means if US-listed stocks fall, say, $1, shares of Ero Copper fall $2.06, on average.

So with the above in mind, the opportunity to increase exposure more conveniently to Ero Copper's growth prospects should not fade.

Country Risk: This Is Low

As for the risk that operating in Brazil can pose for Ero Copper, as for any other mining company, many believe that with the return of Luiz Inácio Lula da Silva to the presidency of the South American country, national policy on mineral exploitation will become less tolerant, as mining usually leads to environmental degradation.

This may be true from an ideological point of view, since Luiz Inácio Lula da Silva, as a left-wing political leader, is close to the ecologists, but at the moment legislative and governmental activity seems to point in a direction more favorable to industrialists and companies than to green issues.

Recently, the Chamber of Deputies in its plenary session approved the bill that will change the system for demarcating the country's indigenous lands, known as “Marco Temporal”, giving hope to agribusiness, but I think likely other sectors as well. The bill must now be approved by the Senate before it goes into effect. So if the bill becomes law in the Senate, the demarcation of Indigenous lands will be limited to those already occupied by Indigenous peoples before the 1988 Constitution came into force.

Conclusion

Ero Copper Corp. is a copper and gold producer in Brazil and its growth plans make its stock a very attractive investment vehicle to gain exposure to the copper and gold markets.

Copper is an important metal in the transition to less polluting human activities and clean energy sources. Gold is increasingly sought after as a safe haven to avoid real asset devaluation as geopolitical tensions become more prevalent in the global context and so financial headwinds for portfolios intensify. The stock is affordable but is likely to get cheaper in the coming weeks as recessionary winds strengthen, boding ill for copper demand, on which this stock is heavily dependent.

For further details see:

Ero Copper: Strong Prospects But Shares May Become Cheaper