EBKDY - Erste Group Bank: Mixed Q3 Results

Summary

- Positive evolution of Net Interest Income thanks to higher rates.

- Despite that, Erste disclosed an important increase in its cost of risks (still at very low levels).

- The company is still trading at a Book Value discount 0.6x versus its historical average of 0.8x. Our buy rating is confirmed.

Our readers know that we have a good grip on the European banking sector. In our initiation of coverage, we were more cautious about Erste Group Bank's development and we provided a neutral rating ( OTCPK:EBKOF ). After our half-year report comment, we decided to increase the company to overweight and since then, the Austrian-based bank is up by more than 20%, outperforming the S&P 500 results on a year-to-date basis. Our wait and see approach clearly paid off and we hope you get on board with us.

{kind=link}

Source: Mare Evidence Lab's previous publication

{kind=link}

Source: Mare Evidence Lab's previous publication

Q3 results

Today, we are back to comment on the company's latest performance. All in all, the bank recorded a good set of numbers. However, we can note that there was a deceleration in Q3 profits.

Q2 to Q3 net profit development

Source: Erste Group Bank AG Q3 results presentation

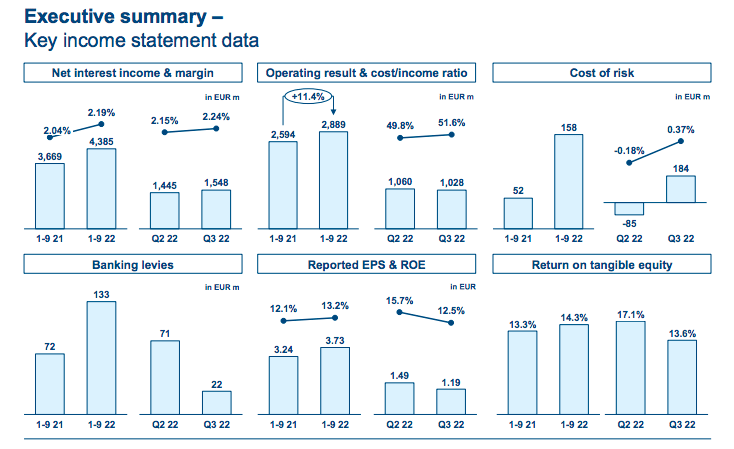

At the aggregate level and looking at the nine-month accounts, the company positively benefits from the higher interest rate environment, especially in Romania, Hungary, and the Czech Republic. NII increased from €3.69 billion to €4.35 billion, thanks to a positive contribution coming from all the geographical areas and in particular in the corporate client activities. On commission income and net fee, Erste also experienced a positive development. Numbers in hand, the company increased its accounts from €1.69 billion to €1.82 billion thanks to higher contributions in payment services and better performance in the asset management division in the Czech Republic and Austria. Despite that, we should also note the negative numbers. SG&A increased mainly for higher salaries and personnel costs, in addition, there were important expenses in the IT department. In detail, other admin expenses reached €1 billion compared to €850 recorded last year. This resulted in a higher cost/income ratio that exceeded the 50% mark once again. More critical to report was the cost of risks evolution that increased by more than 50 basis points. Although default rates remained at extremely low levels, here at the Lab, we are not excluding that the bank might decide to adopt a more prudent approach also following the recent indications of the EU regulator. Therefore, in our number, we estimated an average cost of risk of 35bps.

{kind=link}

Source: Erste Group Bank AG Q3 results presentation

As already mentioned in our Italian banking coverage , we decided to raise the bank profit estimates by 11% in Q4. This takes into account a more realistic scenario on interest rates (average 3-month Euribor at 2.2%-2.4% respectively in 2023 and 2024). Of course, this is partially offset by higher cost of risks and higher loan loss provisions (incorporating a default rate of 1.5%-2%) due to a possible economic slowdown.

Conclusion and Valuation

Last time, we concluded that " based on a 2023 expected Return on Tangible Equity, we value Erste at €30 per share ". Today, Erste almost reached our target price. However, on the Stock Exchange, the company's valuation continues to be contained, with the bank trading at an average tangible price/capital multiple in the area of ??0.6x ( versus its historical average of 0.8x ) Although the medium/long-term prospects appear to be better, the risks are mainly linked to the evolution of the macro context. Despite Erste's CET1 ratio being solid, we believe that other banks provided better risk rewards. We still maintain our buy rating target, but we believe that other EU banks offer more upside: UniCredit and Credit Agricole are two clear examples with dividend/buyback yields of more than 8% (versus Erste at 5.5%).

For further details see:

Erste Group Bank: Mixed Q3 Results