EBKDY - Erste Group Bank: Staying On The Sidelines Despite Good Q1 Results

2023-05-02 11:31:43 ET

Summary

- On April 28 Erste Group Bank reported strong results for Q1 2023 with net profit up 32.3% YoY.

- Guidance for 2023 was not only confirmed but raised.

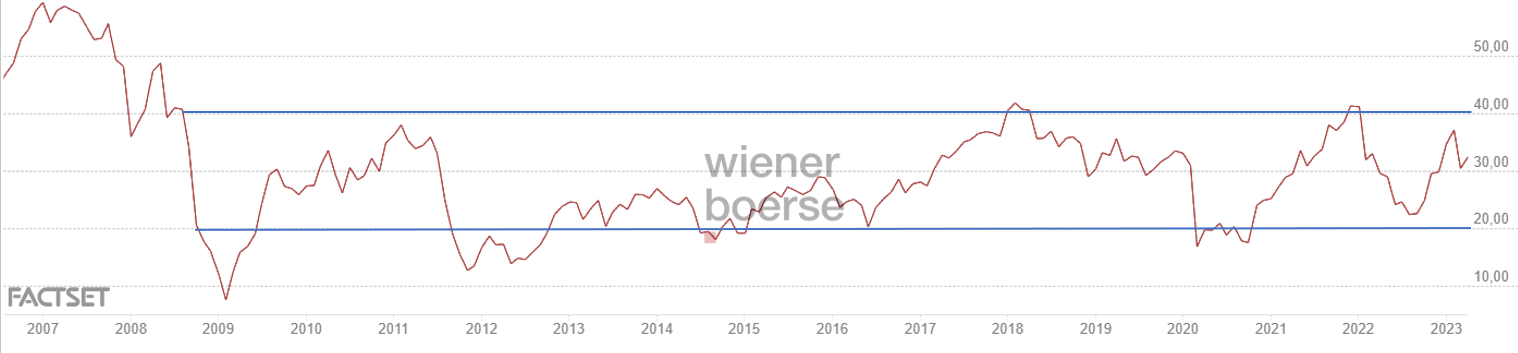

- Shares have been stuck in a trading range between 20-40 euros for the last decade. Within this range there is currently a maximum upside of 20%.

- Despite the strong results, I do not think there will be enough market momentum for shares to break out and go above the upper end of the range.

- New investors should still wait for a lower entry point that could come in H2.

(Note: all amounts in the article are in EUR. At the current exchange rate 1 EUR is around 1.1 USD.)

Investment thesis

Erste Group Bank (EBKDY) (EBKOF) announced Q1 2023 earnings on April 28. While the Q3 results were strong and above expectations, I maintain the Hold rating from my previous article .

Shares are trading at a relatively low valuation, but more or less in line with European peers. For example, UniCredit (UNCFF, UNCRY) also has significant exposure to the CEE region though its Bank Austria subsidiary and is priced like Erste Bank. The forward looking P/E for UniCredi t is 6.39 versus 6.3 for Erste Bank. Based on the 2022 dividend UniCredit has a dividend yield of 5.5%, versus 5.8% for Erste Bank, but UniCredit is usually more generous regarding share buybacks.

Erste Bank shares are close to the upper end of a range between 20 and 40 euros where the stock has been stuck for more than a decade now. The stock price reached 37 euros at the beginning of March this year, but as I predicted in my last article, it bounced back to below 30 and is now around 33.

Erste Group Bank stock price (Source: Wiener Boerse)

{kind=link}

I expect that considerable positive market momentum will be needed to make Erste Bank move above the upper end of this long-term trading range. Currently I do not see this momentum, rather the opposite. While increasing interest rates are driving profitability now and probably for the next 2-3 quarters, this could very well change at the end of the year. Interest rate decreases and recession and credit risk fears could negatively influence the market sentiment towards banks. As the market is forward looking, I see limited upside for Erste Bank now despite the good Q1 results and the relatively low valuation.

Therefore, I am staying on the sidelines and will wait for a lower entry point. My buying range is between 22-25 euros, depending on market conditions. I accept that it could take some time until we get there again.

Q1 2023 results

Net profit in Q1 2023 increased by 14.7% QoQ to 594mn (net profit in Q4 2022 was 518mn). The YoY increase was even stronger with an increase of 32.3% (net profit in Q1 2022 was 449mn).

Increase in net interest income drove profitability in Q1

The key driver was net interest income which increased by 27.1%. Accordingly, the net interest margin increased to 2.5%, showing a nice upward trend over the last quarters - in line with the generally increasing interest rate environment.

Erste Group Bank Net interest margin (Source: Erste Bank)

Other key ratios also went in the right direction. The Cost/Income ratio was below 50% at 49.7%, but the bank guided for a somewhat higher C/I ratio of ~51% for the full year. Still, the development shows that the bank has a good record now of revenue growth outpacing cost increases.

As I noted in my last article, cost discipline used to be not one of the strong suits of the bank, but this has improved. Erste Bank is now more or less in line with European peers regarding cost management, if not already better. But the bank is still far behind cost leaders like its Austrian peer BAWAG Group (BWAGF). BAWAG Group, which is my top pick for European banks currently, reported a C/I ratio of 32.5% in Q1 2023 .

Erste Group Bank C/I ratio (Source: Erste Bank)

RoTE improved to 14.6% but was still below the Q2 2022 value of 17.5.%. I think there is headroom here. The bank confirmed its 2023 RoTE guidance at 13-15% and said that it targets the upper end of the range.

Solid deposit inflows, but lending slowed further

The bank saw solid deposit inflows of 14.1bn in Q1 2023, a positive testament to the strength of the Erste Bank brand in the CEE region. The liability side of the balance sheet is dominated by retail deposits, which come to 236.6bn compared to a total balance sheet size of 342.9bn.

On the other hand, loan growth slowed due to weaker corporate demand. Corporate business had been a key growth driver for most of 2022 but slowed already in Q4 2022 and this trend continued in Q1 2023.

Risk cost

On a group level the NPL ratio was 2.1%, down 20pp from 2.3% YoY, but up 10pp QoQ. Q4 2022 was a historic low for the bank regarding non-performing loans, so I would not worry about the small increase. In its Q1 report the bank says the marginal 10pp increase was driven by single defaults in Austria.

With assets of 43.7bn (12% of the total), Erste Bank has a sizeable real estate exposure, especially as the mortgage loan business with private individuals, which totals 72.3bn, is not included in this number.

Looking at the split into IFRS 9 stages, stage 2 comes to 18% of the total, but the bank notes that 2/3 of the stage 2 exposure results from management overlays and FLI, and is not due to portfolio deterioration.

Real estate exposure split by IFRS 9 stages (Source: Erste Bank)

Although I am not too worried about the real estate exposure, investors should be aware of it. A deterioration in real estate prices in the CEE region, especially in the core AT and CZ markets, would at a minimum result in increased risk provisions.

Capital position and balance sheet metrics

Not surprisingly, with the good Q1 numbers Erste Bank maintains a solid balance sheet.

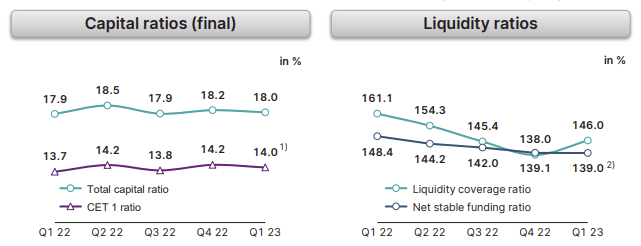

With 14% the CET1 ratio is in a safe place. The same goes for the Liquidity coverage ratio which was 146%. There is certainly nothing to complain about here.

Erste Group Bank Capital and Liquidity ratios (Source: Erste Bank)

{kind=link}

Conclusion

I am still on the sidelines with Erste Bank despite the good Q1 results, I doubt that there is enough market momentum to push the stock above its long-term trading range and with a current share price above 33 euros I see a limited runway.

I am generally not very bullish on bank stocks now, despite the low valuations. I think there is a significant risk that the market focus will turn from interest income growth to recession fears and lending/risk issues in the second half of the year. Therefore, I am sticking to the trading approach I have described in my previous article:

I have been buying and selling Erste Bank several times over the last years. My approach is to buy in a range of 20-25 euros and sell at 35-40. The exact numbers depend on how I see the overall market at a specific point in time. While not perfect, this has worked reasonably well for me in the past.

For further details see:

Erste Group Bank: Staying On The Sidelines Despite Good Q1 Results