EBKOF - Erste Group: Higher Profits Met With A Cheaper Valuation

2023-06-23 06:16:52 ET

Summary

- Erste Group's net interest income has surged due to higher rates in the Eurozone and other non-Euro area markets, boosting earnings and profitability.

- Credit quality also remains very strong, supporting higher profits for the bank.

- With the shares flat since first coverage back in mid-2021, the stock's valuation has actually decreased notwithstanding higher profitability at the business level.

- Even assuming lower through-the-cycle returns on equity, these shares look too cheap at their current discount to book value.

Returns from Erste Group ( OTCPK:EBKOF )( OTCPK:EBKDY ) have been relatively muted since I first covered the bank two years ago, with the shares ultimately flat around the €31 mark over that period.

Fellow shareholders will be forgiven for feeling hard done by here. These shares were ticking along nicely until the war in Ukraine began last February, reaching the €42 per share area before selling off sharply over fears regarding the macroeconomic impact of the conflict.

{kind=link}

Source: Google

While the shares remain well below levels immediately prior to the war, Erste's business has more than held its own in that time. Net interest income ("NII") has surged on the back of higher interest rates in the Eurozone and Erste's other non-Euro area markets, while credit quality has thus far remained surprisingly benign. That is leading to a nice boost in earnings and profitability for the bank.

While Erste's net income and return on equity have headed upwards since my last piece, as has book value per share, the relatively flat share price means that the bank's valuation has headed in the opposite direction over the same period. With these shares now well below their recent historical average multiple of book value, I'm reiterating my initial Buy rating here.

NII Close To Topping, But Guidance May Be Too Conservative

For a brief overview on Erste I will point readers to my initial article on the bank. The two chief points worth reiterating are, firstly, that Erste is predominantly a lender, with NII making up two-thirds of its top line. Secondly, its funding profile is fairly attractive because it is quite deposit rich, reducing reliance on more expensive (and economically sensitive) wholesale funding. Note that overnight deposits fund around 50% of its asset base, with relatively sticky household deposits accounting for the bulk of those.

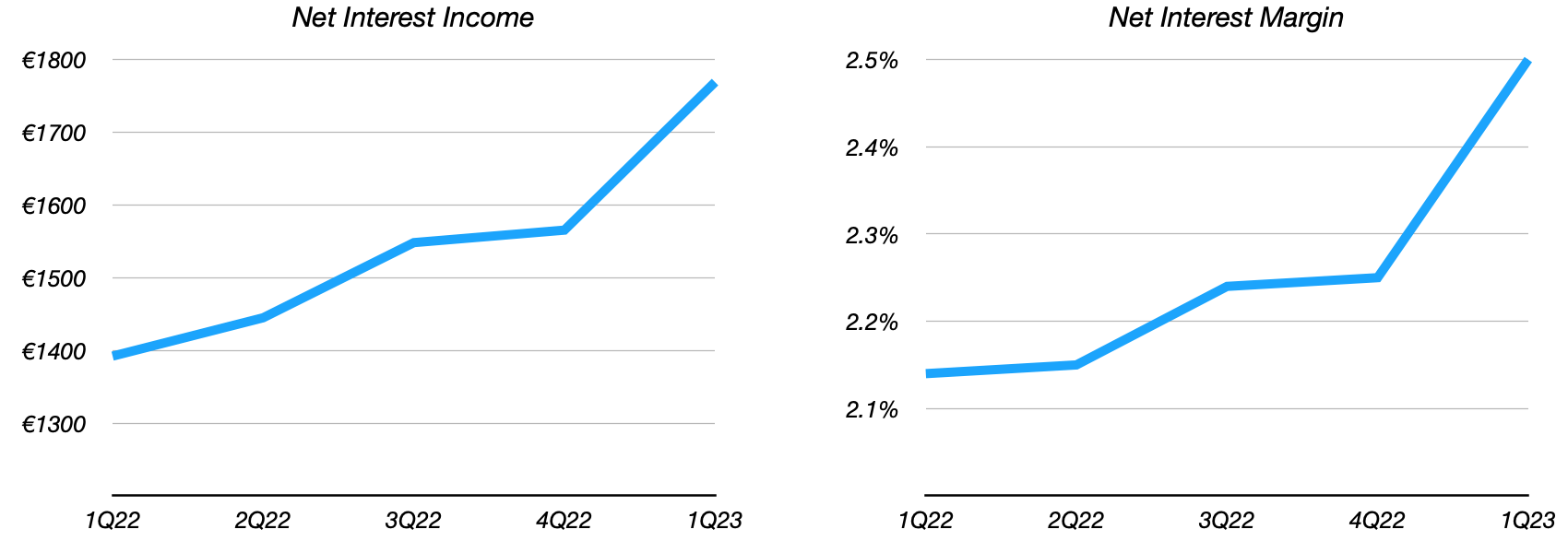

With that, Erste has been enjoying the benefits of higher interest rates in recent quarters. Q1 FY23 NII was around €1.77B, up sharply on the circa €1.28B in quarterly NII the bank was generating back at initial coverage in Q2 FY21. That has been driven by both higher margins and interest-bearing asset growth, with net interest margin ("NIM") expanding from 2.13% to 2.50% and loans to customers advancing around 6% in that time (from €191.5B to €202.7B).

Erste Group: Quarterly NII & NIM

{kind=link}

Data Source: Erste Group Quarterly Earnings Releases

NII growth looks set to moderate sharply in the coming quarters, albeit management still upped FY23 guidance to 15% YoY growth versus 10% YoY previously. That would imply total FY23 NII of at least €6.85B (FY22 NII: €5.95B), which given the current quarterly run rate would further imply that NII has likely topped out. However, in response to analyst questions on the Q1 earnings call management stated that NII growth would likely still be positive in Q2 and possibly even Q3. This would make the 15% YoY growth guidance overly conservative, with FY23 NII likely to land closer to the €7B mark in my view.

Personally I would expect that we have not yet seen the peak but rather that might come in either Q2 or Q3, at least when it comes to 2023.

Stefan Doerfler, CFO

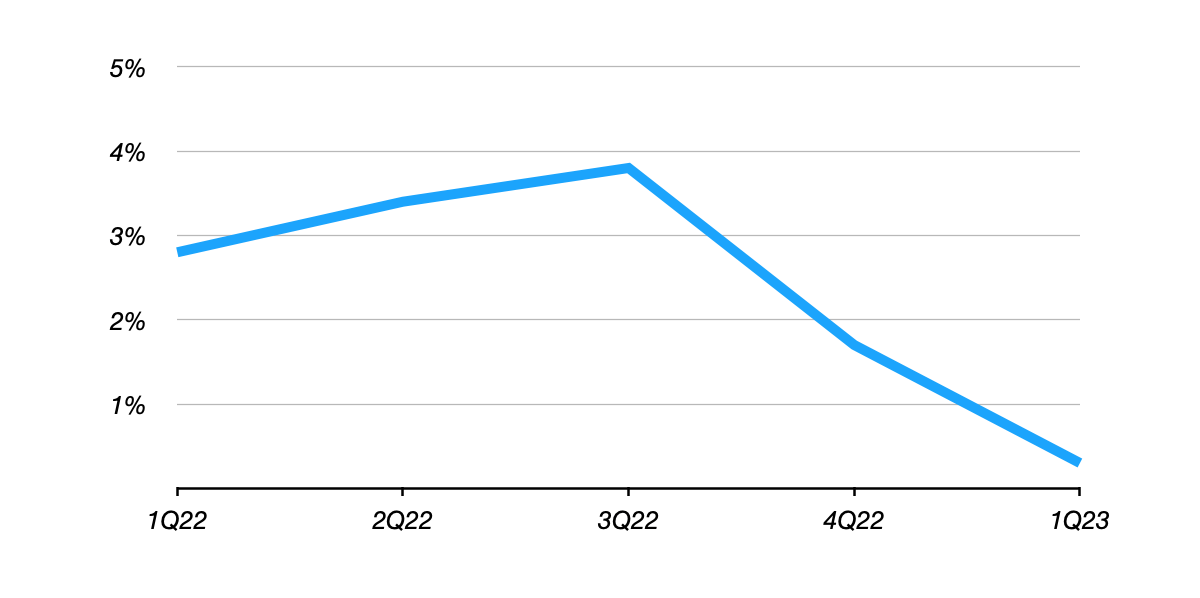

Even so, NII growth is clearly slowing, which is not surprising given that sequential loan growth has also slowed markedly:

Erste Group: QoQ Loans To Customer Growth

{kind=link}

Data Source: Erste Group Quarterly Results Releases

Credit Quality Supporting Higher Profits

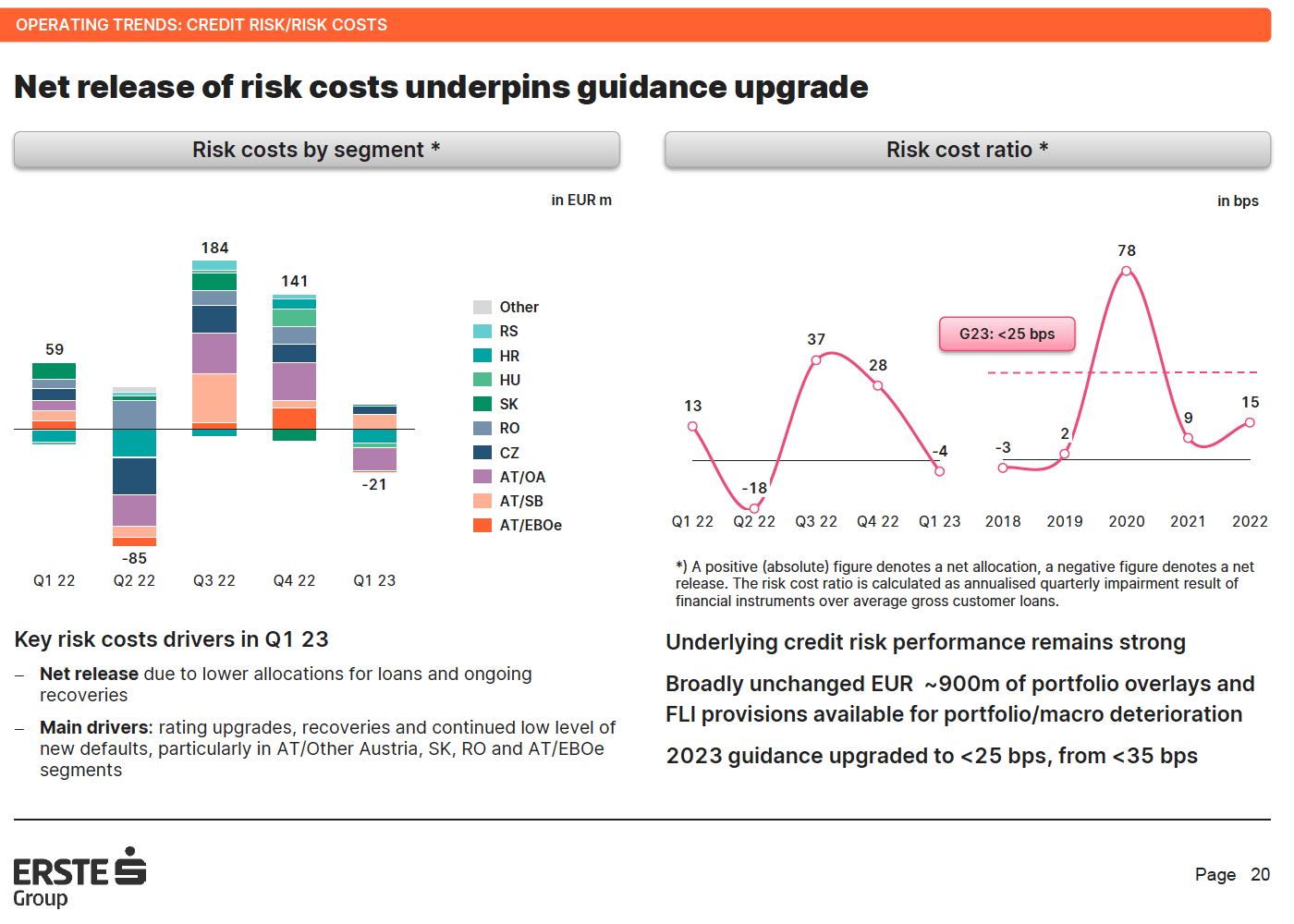

The credit quality environment remains surprisingly benign. Non-performing loans were just 2.1% of gross loans in Q1, which is actually 40bps lower than back in Q2 FY21. Risk cost guidance also remains low, with management expecting under 25bps for FY23, upgraded from previous guidance of 35bps.

{kind=link}

Source: Erste Group 1Q23 Results Presentation

The combination of higher net interest income and the benign credit quality environment is boosting profitability. With my estimate of NII at around €7B, plus management guidance on fee income (5% YoY growth, implying ~€2.6B), operating expenses (+9% YoY, implying just under €5B) and cost of risk (below 25bps as per above), FY23 return on equity ("ROE") would land a little above 13%. That is around three points higher than the FY18-FY22 average. This also chimes with management guidance, which sees FY23 return on tangible equity ("ROTE") in the 13-15% range (N.B. My FY23 ROE estimate above corresponds to a circa 14.4% ROTE).

Valuation Now Historically Cheap

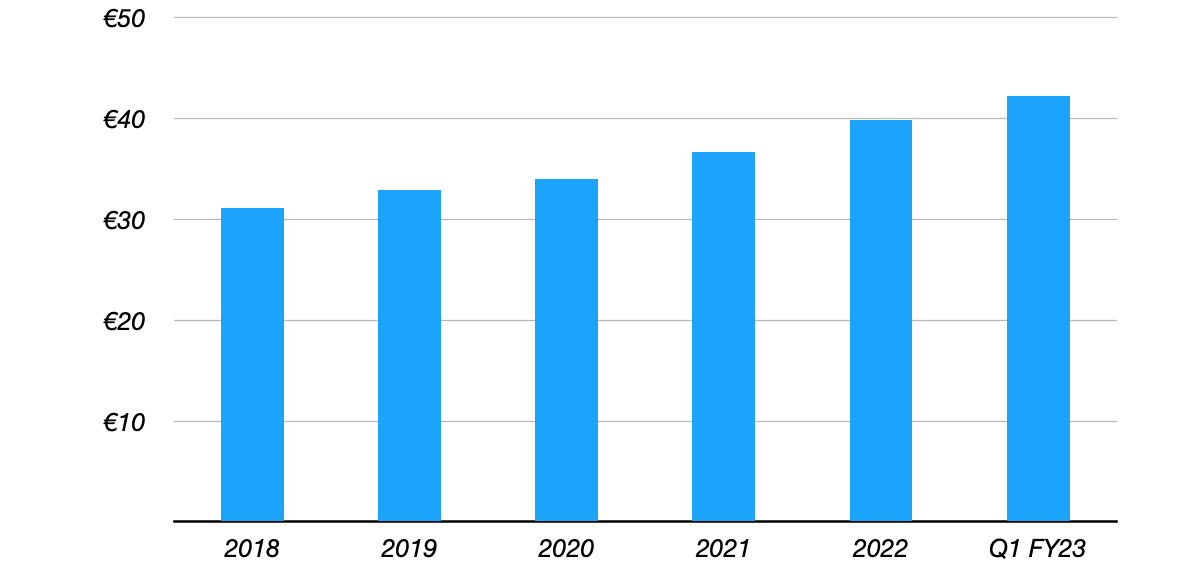

While Erste's share price is roughly the same as it was two years ago, its price relative to book value is actually lower as book value has grown in that time. At €30.96 in current trading in Vienna, Erste now trades for just 0.7x book value per share ("BVPS").

Erste Group: Book Value Per Share

{kind=link}

Data Source: Erste Group Annual & Quarterly Results Releases

Of course, Erste is probably over-earning right now due to the combination of higher rates and very strong credit quality outlined above. Even though non-performing loan coverage is sound (around 95% excluding collateral) and Erste generates significant levels of pre-provision income to absorb bad debt charges, higher cost of risk would still eat into profitability.

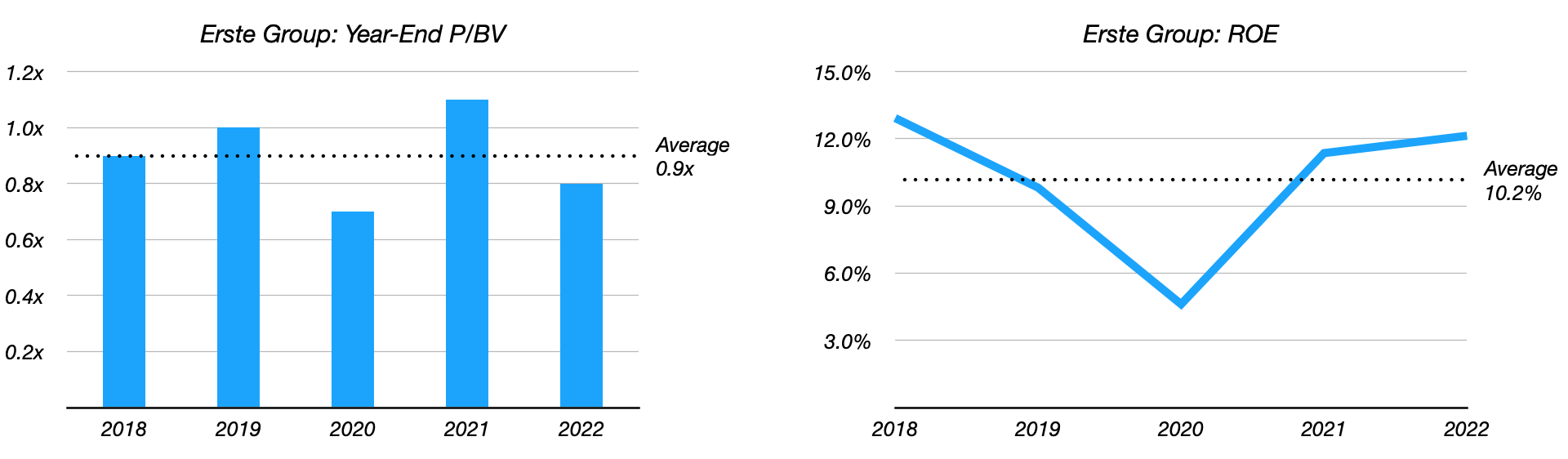

This is more than covered by the current discount to book value. Over the past five years, Erste's average year-end P/BVPS was around 0.9x, which is commensurate with its average ROE (~10% as per the previous section) over the same period. Even if you assume that the bank is currently over-earning due to favorable macro conditions, there is still considerable upside assuming a mean reversion to a circa 10% through-the-cycle ROE. A corresponding 0.9x BVPS multiple would imply around 35% upside to fair value in the €42 per share mark (circa $23 per ADR).

{kind=link}

Data Source: Erste Group Annual Reports And Author Calculations

While I do expect the stock to migrate towards that valuation over time, note that multiple expansion is not necessary in order to achieve attractive returns here. With that, management targets a dividend payout ratio of around 40-50% of net earnings. A ~13% ROE for FY23 maps to EPS of around €5.70, which would imply an FY23 dividend per share of around €2.25 at the low end. At the current share price that implies a forward dividend yield of circa 7.25%. Assuming Erste can reinvest retained earnings at its historical 9% return rate, implied annual shareholder returns would be in the 12% area even absent valuation multiple expansion. With that, I retain my Buy rating on the stock.

For further details see:

Erste Group: Higher Profits Met With A Cheaper Valuation